Grayscale (GBTC) Effect: The Instigator of Institutional Bubbles and Collapses

TechFlow Selected TechFlow Selected

Grayscale (GBTC) Effect: The Instigator of Institutional Bubbles and Collapses

Regardless of the current bill's status, it marks the end of the current cycle.

Written by Ben Lilly

Translated by TechFlow

We're revisiting a story from two years ago, beginning in 2020 — what we call the "Grayscale Effect."

Looking back at these events, we see that 2020–2021 marked the start of a bull market. But simultaneously, it sowed the seeds that would trigger the bear market of 2022.

Today, the bear market continues.

Perhaps crypto observers on Twitter and media are now helplessly waiting for the final apocalypse to arrive — hoping it comes sooner rather than later. Because that Digital Currency Group (DCG) empire is collapsing from within... an empire now infamous for its Grayscale Bitcoin Trust fund...

And what these early clues show us is that we’ve come full circle — the very catalysts that once drove growth are now unraveling before our eyes. We’re witnessing the other side of this double-edged sword.

So today, let’s dive into some recent scandals to make sense of what’s unfolding right now.

The Bubble Begins

Before we begin, there’s one thing I want to address.

I mentioned how we seem to be going in circles, and before anyone suggests all progress from two-and-a-half years ago has vanished, I’d like to quickly dispel that negative mindset.

This isn’t two-and-a-half years ago anymore. What’s happening this year won’t set the industry back three or four years.

Thinking so negatively might reflect where someone’s faith originates — speculation. I believe such thinking does society no good. We’ll soon see many of the harms caused by this behavior.

Therefore, while the current atmosphere may feel gloomy and reflective, let’s not overlook the rapid pace of technological breakthroughs happening every week… This innovation is real. It's the industry’s inherent strength, which speculation cannot roll back by several years.

If anything, the rising energy among Githubs, forums, and passionate teams resembles a volcano ready to erupt. Nothing standing in its way can slow its progression. And once this energy is unleashed upon the world, it will create the most fertile ground for a brighter future.

Innovation and development in this industry represent one of the freest forces across any sector — a force cultivated in freedom, truth, and self-sovereignty. These are truths that won’t simply lose their faith... and they are truths unrepresented and unmentioned in today’s headlines of failure.

So if “the purpose of conquest is to avoid doing the same things as the conquered”… let’s revisit the past, hoping it helps us move forward — so yesterday’s mistakes don’t haunt us tomorrow. We haven’t regressed; we’ve merely understood the distance to our goal.

Act One — The Beginning

It began with DeFi Summer in 2020. Every crypto user immersed in on-chain trading started learning about yield farming, vaults, liquidity aggregation, synthetic tokens, yield-bearing tokens, and more.

Amidst the noise of these tokens and short-term yields exceeding 1,000%, our internal trading and alert AI system flagged unusual demand emerging in the Bitcoin spot market.

This was a major red flag for us because spot demand was pushing prices into new ranges. Derivatives pushed us to the highs and lows of ranges. For anyone recalling 2020, the fear of the March 2020 low remains etched in traders’ minds.

Looking back, it’s ironic that a new species emerged in the form of yield tokens, allowing the ecosystem’s largest whales to move around unnoticed...

These whales were the reason behind the 18-month bull run.

Now, as prices retrace close to where the market stood 18 months ago, we realize the very leverage that started it all is now exiting the stage. This is the double-edged sword we referred to earlier.

The people who started this cycle are the same ones making headlines today.

So who exactly am I referring to? And what?

Let’s pull up a tweet from summer 2020 that caught our attention. At the time, it stood out more than others, likely because this bullish sentiment aligned closely with what our AI had detected.

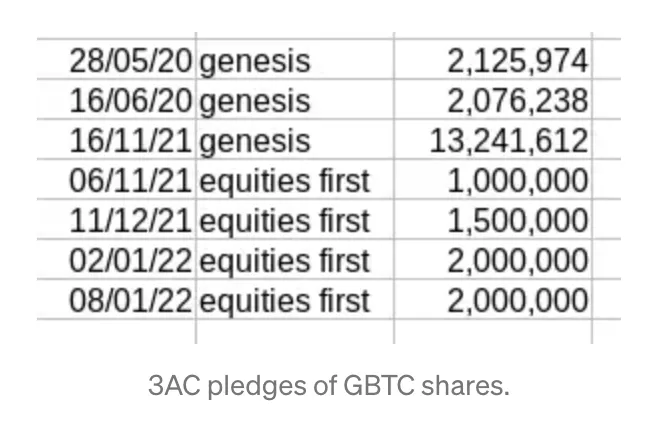

It was a now-deleted tweet from the head of Three Arrows Capital (3AC).

This is a snapshot of 3AC’s books (possibly hedged), showing they were increasing long positions. According to the image, Zhu’s screenshot reflects roughly 2,340 ETH in contracts. At the time, the total value was just over $1 million.

For a multi-billion-dollar hedge fund, this might seem like a small position. But at the time, 3AC wasn’t yet a billion-dollar fund.

According to a report in nymag citing 3AC’s annual filing: “Three Arrows’ main fund returned over 5,900%. By year-end, it managed over $2.6 billion in assets and $1.9 billion in liabilities.”

That means 3AC earned roughly $700 million in profit… meaning the firm achieved returns exceeding 5,900% at some point in 2020, managing approximately $11.5 million.

This makes the screenshot even more indicative of an oversized bet built on conviction.

As it later surfaced that 3AC wasn’t interested in hedging, this ETH position signaled what 3AC intended to do. We don’t even know what their BTC call options looked like — that was a far more liquid options market.

I suspect their BTC option positions were much larger, because anyone trading on Deribit at the time could attest to massive spreads. Filling seven-figure positions took considerable time, especially on illiquid ETH options contracts.

That’s why we also see so many contracts and expiration dates in the snippet above.

Alright, digging deeper into this position, we also know what happened before that tweet was posted.

First, 3AC purchased over 21 million shares of Grayscale Bitcoin Trust (GBTC). We know this thanks to an SEC filing dated June 2, 2020.

Grayscale is an entity under Digital Currency Group, which dominated the market, accumulating a total of 536,000 BTC to date.

Its unique structure made this possible. Essentially designed to hoard Bitcoin, BTC and USD (used to buy BTC) flow in, but cannot be withdrawn.

Grayscale enables this one-way flow through how it issues shares. Accredited investors, or “the wealthy,” can register for private placements to receive shares.

Then, these accredited investors can provide BTC or USD to Grayscale. In return, Grayscale gives them shares of equivalent value. If each share equals 0.001 BTC (actually 0.00095085), then for every BTC sent to Grayscale, the investor receives 1,000 GBTC shares (minus minor fees).

The problem? Private investors must wait six months before selling GBTC on the market. This is where non-accredited retail investors speculate — buyers who aren’t as wealthy.

Exchanging stock for BTC seems fair, but in reality, it isn't. This is because GBTC almost always trades at a premium. Non-accredited investors or retail buyers seeking pure Bitcoin exposure on the stock market don’t pay fair value.

Here’s what I mean… Recently, GBTC closed at $28.25. According to BraveNewCoin Liquidity Index, Bitcoin closed at $22,830. Per Grayscale’s website, each GBTC share equals 0.00095085 BTC. That means GBTC’s fair value is $21.71. The current price carries a 30% premium — solely because the buyer isn’t wealthy. That 30% premium flows directly to the accredited investor who contributed the BTC.

This mechanism is how Grayscale structured its trust — essentially enabling a one-way inflow of Bitcoin. Which Bitcoin-holding accredited investor wouldn’t be interested in increasing their BTC balance? Whether BTC is $5,000 or $20,000 doesn’t matter. As long as there’s a premium, the BTC value grows.

Within six months, this offered nearly risk-free returns of 30%, or 69% annually.

This is substantial. Naturally, economic pressure should drive this premium down to 0%. Yet, for some reason, we haven’t seen that happen.

This implies 3AC likely bought Bitcoin before the June 2 filing. We can estimate the period below based on Su Zhu’s tweet around December 5, 2020, and the next disclosure filed around December 31, 2020 — roughly a 30-day window. The period shown below is slightly over 30 days.

But remember, Zhu held some July ETH call options. They had a strike price of 240, costing 0.0246 ETH per contract.

If these contracts were bought 1.5 months or more in advance, that means the price needed to rise 20% to 40% (estimated) for them to be profitable.

Currently, we can assume these positions were entered within this timeframe.

The key point here is that 3AC likely bought call options before purchasing BTC on the spot market, then sent tokens to Grayscale and filed the SEC documents. This is logical because you can profit from your spot purchase — 21 million shares (~1,000 GBTC shares = 1 BTC) amount to roughly 21,000 BTC.

That much Bitcoin was worth $150–200 million at the time, meaning this was a borrowed amount (from lender Genesis) relative to 3AC’s asset and liability profile.

Now, if we go one step further, we can refine the timeline even more…

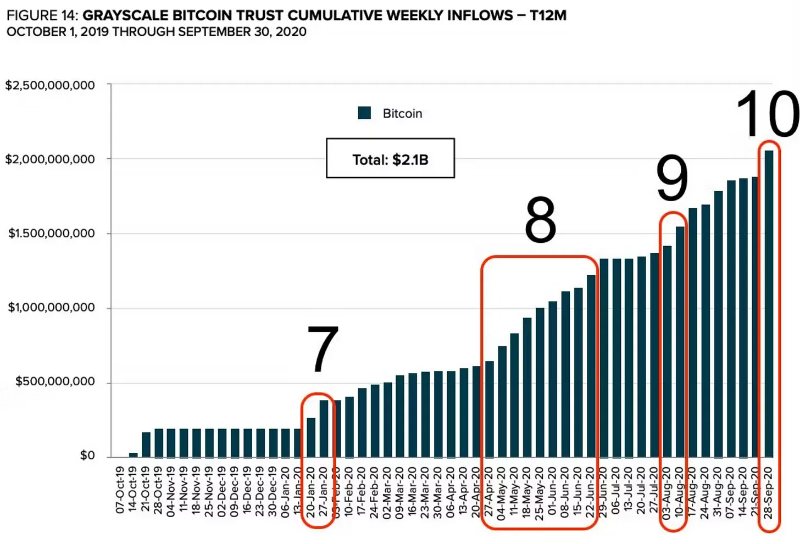

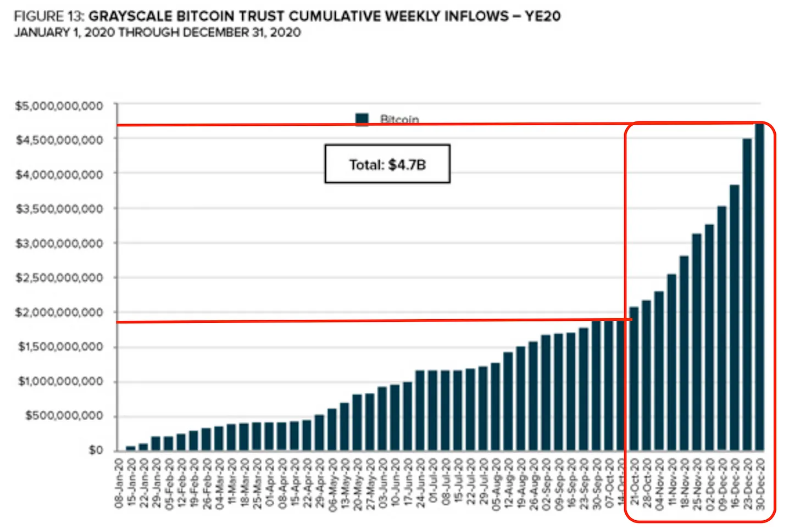

Below is a screenshot of Grayscale’s weekly cumulative inflow chart.

This shows us that inflows may have started as early as the week of May 11. This places us at the starting point of the two boxes in the previous candlestick chart. It also adds further support for the big moves in late April and early May, driven by the 3AC <> Grayscale dynamic.

This part essentially summarizes Su Zhu’s first act.

Interestingly, during Act One, we see signs of fear in Su Zhu’s directional bets. He wanted to lock in GBTC’s premium but worried it would vanish.

Here, he asked SBF of FTX to create a tool around Grayscale’s GBTC Trust. We can only assume this was so 3AC could exit their position in the trust without waiting six months.

This tweet reveals unease due to timing. 3AC filed with the SEC on June 2, and their potential premium profits dropped from ~23% to single digits during June.

While the premium still existed… it foreshadowed the end.

Act Two — Leveraging Up

My initial theory was that 3AC held their GBTC for at least six months before selling.

That would mean 21 million GBTC shares hitting the market in December.

But thanks to some digging by Data Finnovation in this article, my initial view appears incorrect. When looking at the GBTC chart and volume, this also seems consistent… There’s no visible 21 million-share volume spike. After Genesis, Grayscale’s parent company’s lending arm, lent out Bitcoin, dumping 21 million shares… I highly doubt they’d be willing to cause such volatility.

Instead…

Why didn’t 3AC do the opposite — add even more leverage? After all, Bitcoin had already risen, and the premium was growing… So cashing out here would’ve been wise. We’ve heard stories of lenders not even conducting due diligence on 3AC.

So if 3AC were to lever up, the conversation likely occurred in late November or early December. The reason? We can see Zhu growing increasingly confident about what was coming.

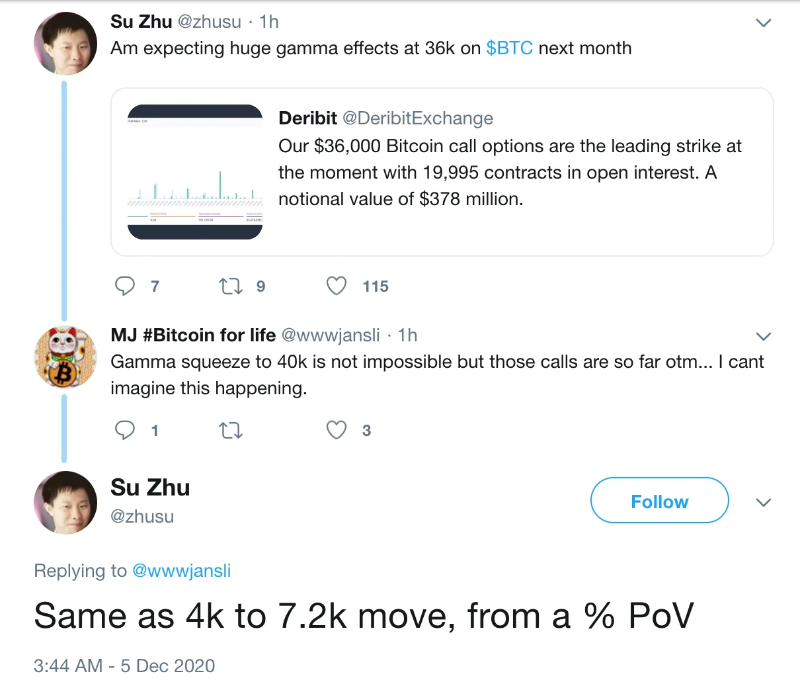

Below is a deleted tweet indicating he believed a gamma squeeze was imminent by month-end. Remember, Zhu held call options at the time.

Su Zhu’s numerous prescient call options suggest the phone call encouraging 3AC to keep increasing leverage may have actually occurred as early as summer 2020.

So stepping back…

On December 5, 2020, Su Zhu expressed strong confidence, predicting gamma would push BTC above $36,000. At the time, BTC was $18.6k — requiring roughly 100% returns in about four weeks. Meanwhile, BTC hadn’t yet reached new all-time highs, making this an even tougher task.

This confidence aligns with the SEC filing submitted on December 31, 2020, stating 3AC then held 38,888,888 GBTC shares.

This means from June 2 to December 31, 2020, 3AC added 17.8 million shares.

This capital flowed into the trust, creating significant room for 3AC and others. The largest inflows coincided precisely with the market heating up. If I had to guess, the biggest surge occurred when 3AC acted on the gamma squeeze they mentioned on December 5.

And honestly, I wouldn’t be surprised if 3AC was the protagonist in that story of a Bitcoin options trader turning $638k into $4M in five weeks. That timing would again be too striking a coincidence.

So by end of 2020, 3AC had $2.6B in assets and $1.9B in liabilities. With 38.8M GBTC shares at ~$32 each, that’s about $1.25B — nearly half their book value.

Adding earlier-year profits of ~$700M, we can assume 3AC survived entirely on the Grayscale effect. The entire market rose. In a trade representing half their book, unhedged positions yielded over 60x returns.

Given 3AC’s $1.9B in liabilities, we can assume they also borrowed BTC to conduct the Grayscale trades we’ve discussed so far.

Borrowing from one DCG subsidiary to help another earn massive management fee revenue.

It’s like allowing a lender to open a store for homebuyers in an upcoming community. None of these buyers actually intend to live there. So the bank gives them money to buy houses… New homeowners must wait six months before the house is built.

Meanwhile, the homebuilder earns a few percent profit on each house.

The key here is there are no other homebuilders in the area… Or in other words, no other way to buy Bitcoin besides this builder.

Therefore, to keep this scheme working, new buyers must enter the market — and they can’t buy directly from the original homebuilder.

How could this be achieved?

Act Three — Narrative Building

In Q1 2021, we began seeing a shift in narrative. To prevent Grayscale’s premium from turning negative… more buyers were needed.

That meant reaching the masses. The key was individuals couldn’t buy homes from the homebuilder (i.e., directly buy shares from Grayscale). They had to buy GBTC from the open market.

That’s where the retail crowd came in.

And they couldn’t attract users willing to learn the trading curve via exchanges like Coinbase, Kraken, or Gemini.

That’s where the appeal of “Drop Gold” came in. Originally launched in May 2019, it targeted exactly the demographic Grayscale needed to lure. More importantly, if you search online, you’ll find that late 2020 and early 2021 marked when users outside crypto started seeing these ads.

Then, to layer narrative upon narrative, Zhu kicked off his “super cycle” narrative in Q1, suggesting people needed to pay high prices for crypto because it would only go up.

Hype was in full swing.

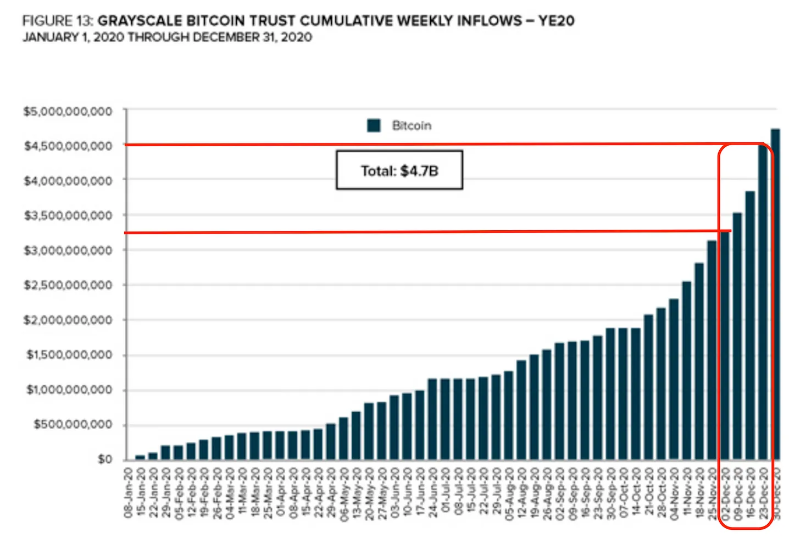

Yet, this wasn’t enough. Grayscale saw over $2.5 billion in inflows during its final 10 weeks of 2020.

It was preparing to list as soon as mid-April. These 10 weeks saw more capital inflow than the previous seven years combined. Read that again… More capital entered the trust in these 10 weeks than in the prior seven years.

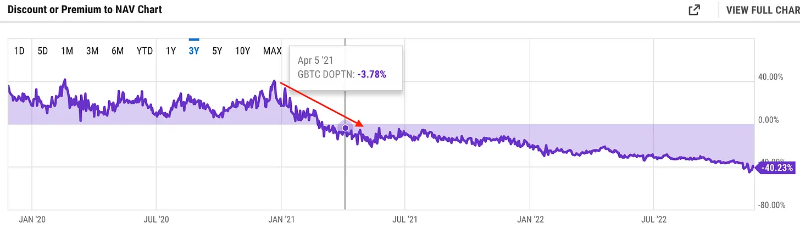

This period coincided with the trust’s Net Asset Value (NAV) turning negative. August inflows caused share prices to drop below the redeemable level of the trust — if the trust allowed redemptions.

This wasn’t just trouble… This was the true beginning of the crash. Just as over $2.5 billion in GBTC was poised to enter the market, how could Grayscale rescue negative NAV?

Act Four — The End

On April 5, Grayscale announced plans to convert the trust into an ETF. If successful, NAV would return to normal.

To restore the trust to par, Grayscale would need to sell BTC into the market. This means anyone buying GBTC below NAV would profit.

This marked the beginning of the end for the trust. When Bitcoin rebounded in Q3 2021, NAV nearly recovered… but NAV never turned positive again. Clearly, the trust was weakening.

Grayscale, DCG, Genesis, and 3AC were all pigs at the trough. If life has taught me one lesson, it’s never to become a pig — because pigs get slaughtered.

And that’s exactly what happened when the market turned in 2022.

Regardless, this is why we now see Grayscale, Genesis, and DCG struggling. Barry Silbert did do many good things in this space.

But he and his vast entities became greedy. If we look closely, we might find Grayscale/DCG at the root of nearly every explosion in crypto. The industry truly is that small.

Perhaps he started well-intentioned, but has now become harmful to the industry. Don’t mourn its demise. I wouldn’t be surprised if Grayscale <> DCG <> Genesis (and even BlockFi) — perhaps more entities — all end up dead.

No matter the current legislation, it signals the end of this cycle. Perhaps, this brings us one step closer to the next.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News