Stablecoin Wars: Can Aave's GHO Stablecoin Help the Protocol Advance Further?

TechFlow Selected TechFlow Selected

Stablecoin Wars: Can Aave's GHO Stablecoin Help the Protocol Advance Further?

How will the Aave DAO and team bring GHO to market and make it potentially as significant as DAI?

Author: Tokenbrice

Translation: TechFlow

A few weeks ago, the concept of the GHO stablecoin was introduced on the Aave governance forum, sparking excitement across DeFi. Indeed, a decentralized, collateral-backed stablecoin natively governed by the Aave DAO makes perfect sense as the protocol’s next step.

In this article, we will explore how the Aave DAO and team might bring GHO to market and position it to become as significant as DAI. Before that, however, let’s first examine GHO’s design. Of course, information is still scarce, so the second part of this article is largely based on my own judgment drawn from DeFi experience.

Introduction to Aave’s Native Stablecoin GHO

Since its early days, Aave’s main challenge has been attracting sufficient stablecoin deposits—because it’s borrowers’ top choice. Therefore, creating a native stablecoin is a natural next step for the project, which should also help reduce borrowing costs. Since this stablecoin would be minted rather than deposited, there would be no need to pay depositors an APR.

Next, let’s dive into the key features of GHO.

Overcollateralized USD-Pegged Stablecoin

GHO is an overcollateralized stablecoin minted using aTokens as collateral. In this sense, it resembles MakerDAO but with slightly higher efficiency, since all collateral consists of productive assets generating yield (aTokens)—depending on borrowing demand.

Interestingly, Aave chose not to include "USD" in the name. Given how strict U.S. regulators can be, this could be legally advantageous. However, this may not be the only reason—Aave founder Stani hinted at potential future peg swaps.

Interest Rate Model and stkAAVE Discounts

Currently, GHO’s interest rate model is its most disappointing aspect. The initial proposal suggested that the Aave DAO would directly set rates, similar to how it works on Maker. However, this would be inefficient and add unnecessary complexity to governance.

Community feedback will shape its final form. Personally, I hope Aave ultimately adopts a market-driven rate model—just like other tokens on Aave—where supply and demand within the pool determine the rate.

If the Aave community insists on involving the DAO in rate-setting—a practice I find absurd, as DAOs are ill-suited for managing system parameters—we could imagine a hybrid model where the DAO votes on a fixed base rate, adjusted dynamically within a range based on market conditions.

Dynamic rate adjustments could actually help protect GHO’s peg by discouraging mass minting events, much like Liquity’s BaseRate protects LUSD from depegging. Initially, fees start at 0.5%, rise during periods of high demand, and gradually fall back to 0.5% when demand stabilizes.

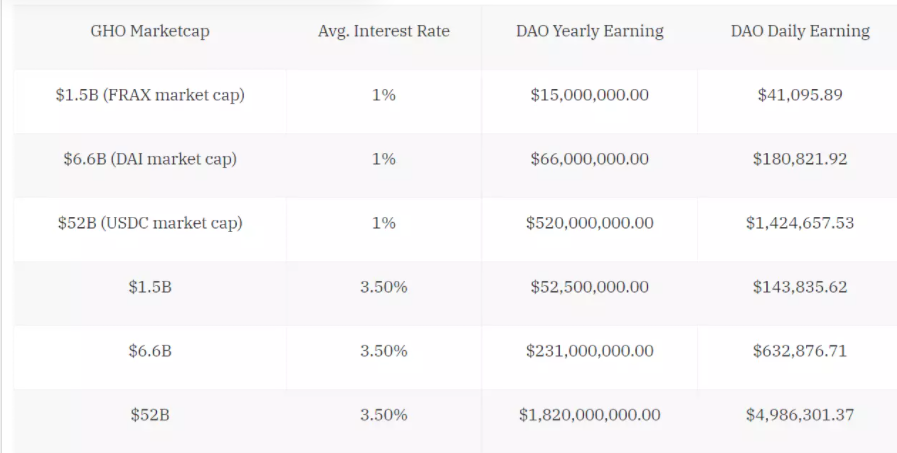

The proposal also mentions discounts for borrowers who stake AAVE tokens as collateral, creating further synergies. Finally, 100% of the interest paid by borrowers goes directly to the Aave DAO (unlike most other tokens, which have reserve factors around 10%), meaning GHO could become a financial goldmine for the DAO if it reaches significant market cap. If GHO’s market cap matches DAI’s and average borrowing rates are 3.5%, Aave DAO could earn nearly $150,000 per day from GHO interest.

Below are some estimates under different assumptions for GHO’s market cap and interest rates:

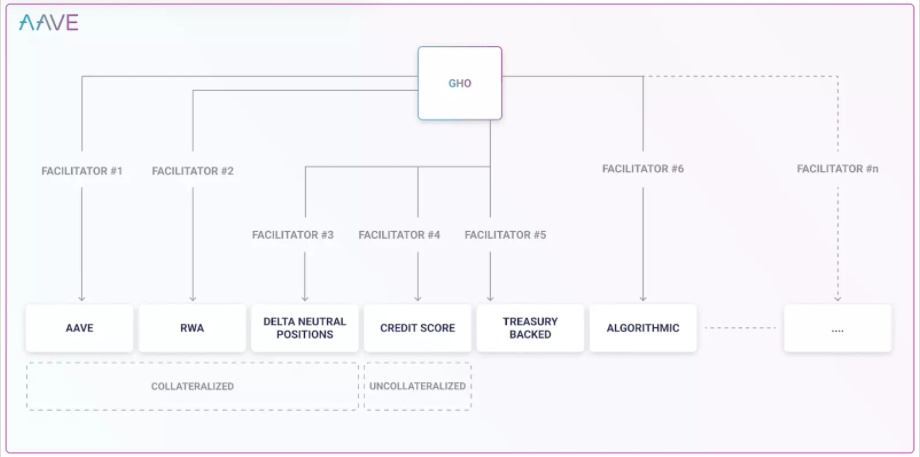

Facilitators and RWA

GHO’s design introduces “facilitators” governed by Aave, which will be authorized to mint GHO. The first facilitator will be the Aave protocol itself, but others—whether protocols or real-world entities—could follow. This aspect is exciting because it expands GHO’s design space. After launch, we may see other protocols apply to become facilitators and build on top of Aave and GHO.

“Decentralization” and Censorship Resistance

GHO is defined by the Aave team as a decentralized stablecoin, with even some mention of censorship resistance.

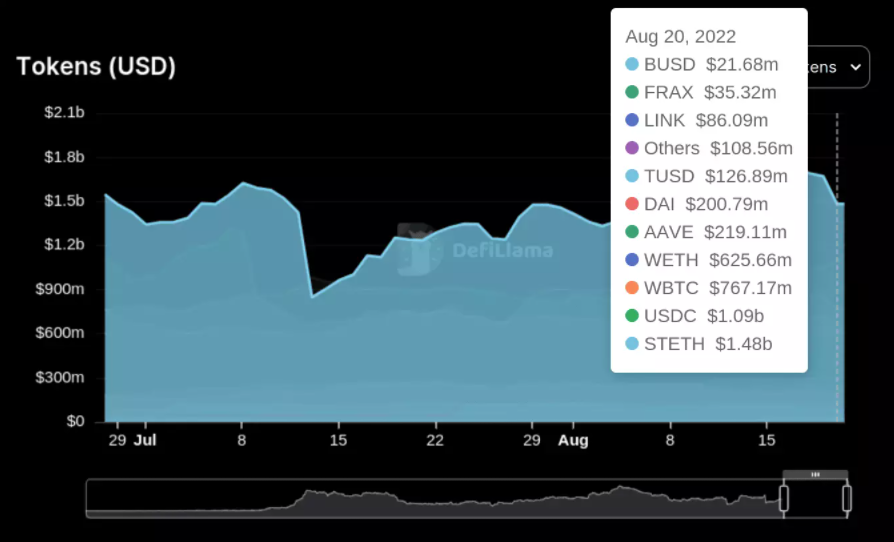

Unless I misunderstand the design, GHO will be as “decentralized” as DAI, but due to its collateral composition, it will have weaker censorship resistance. Assuming all aTokens currently eligible as collateral on Aave will also be usable for borrowing GHO, GHO’s collateral mix will consist mostly of censorable tokens like USDC:

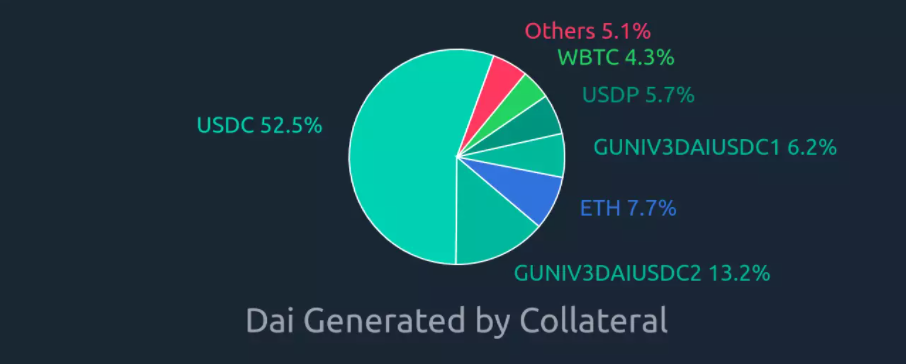

Indeed, stETH and USDC are the top collateral assets used on Aave, followed closely by another trusted token (wBTC). Still, GHO’s collateral composition would be significantly better than DAI’s, which is almost entirely backed by USDC (>50%).

Another ~25% of DAI’s backing comes from other trusted collateral or reflexive positions providing liquidity (such as DAI/USDC LP tokens used as collateral to mint DAI).

GHO Market Entry: What Could AAVE Look Like With GHO?

Now that we understand what GHO is, we can move to the more speculative territory: use cases after GHO’s launch.

In fact, the interaction between the Aave protocol and GHO is quite exciting: while the original post mentioned Aave x GHO and enabling eMode on GHO (offering significant leverage on selected pairs like USDC/DAI), details were sparse.

Here’s my take.

aGHO would be fascinating collateral on Aave, but allowing GHO borrowing against it could create significant reflexive risk. Therefore, I expect aGHO will be blocked from minting GHO to prevent the kind of reflexive support we currently see with DAI.

Nevertheless, it could still enable stablecoin arbitrage loops such as aUSDC > Mint GHO > aGHO > Borrow another stablecoin. With eMode, this could make Aave with GHO a highly efficient stablecoin arbitrage protocol. Additionally, GHO’s interest rate could serve as a “base stablecoin rate,” potentially helping regulate rates on other stablecoins like USDC.

GHO’s Liquidity Strategy

No stablecoin design is complete without a solid liquidity strategy. Since CRV, CVX, and BAL are already accepted as collateral on Aave, the treasury could strategically deploy accumulated CRV, CVX, and BAL. Locking them in their native protocols would allow Aave DAO to direct incentives toward pools involving GHO.

Just as Frax is currently reducing reliance on USDT and DAI and attempting to establish Frax Basepool (FRAX/USDC) on Curve as a pairing asset for other stablecoins, we can envision Aave taking a similar path. Moreover, many projects currently exposed to USDC and DAI are seeking to diversify their liquidity away from them. GHO’s arrival could be the perfect moment for DeFi to reduce its dependence on USDC.

However, while Frax controls substantial governance and gauge voting power in the “Curve Wars,” Aave DAO does not. The current treasury balance of CRV/CVX is clearly insufficient to bootstrap pools to a billion-dollar scale, which may push Aave DAO to seek additional liquidity incentive tokens. Yet, since the DAO will earn substantial revenue from GHO interest rates, it should have ample resources to support adequate liquidity regardless of GHO’s final market cap.

Finally, Aave has historically had close ties with Balancer; after transitioning to the AAVE token, the team adopted an 80% AAVE / 20% wETH Balancer pool for its safety module. The treasury currently holds 200k BAL and plans another acquisition. Thus, we can expect strong GHO integration on Balancer. However, when it comes to stablecoins, Curve remains unavoidable. Without a strategy to engage in the CRV wars, I don’t see how GHO can achieve sufficient growth.

Beyond core protocol incentives (such as dynamic or DAO-managed borrowing rates) and liquidation mechanisms, liquidity strategy may be one of the most critical elements for a stablecoin, as it also affects the stability of the peg.

Conclusion

I hope this article helps you better understand the stakes in the stablecoin wars. The end of this year will be particularly interesting, with GHO’s launch approaching and Curve also hinting at the release of its overcollateralized stablecoin before year-end. The proliferation of stablecoins is a natural next step for DeFi, as most established protocols converge toward similar designs:

- Frax started as just a stablecoin, but now has FraxSwap and soon FraxLend.

- Aave began as a money market, but is about to launch its native stablecoin.

- Curve started as a DEX, and now its stablecoin is coming, enabling efficient lending for liquidity providers.

Ultimately, the primary reason protocols create their own stablecoins is clear: it’s the most profitable domain, and massive demand exists.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News