How does Frax stand out among algorithmic stablecoins?

TechFlow Selected TechFlow Selected

How does Frax stand out among algorithmic stablecoins?

Frax is not the only algorithmic stablecoin in today's market, nor will it be alone in the future market.

Written by: Jackchong.eth & 0xkowloon.eth

Translated by: TechFlow intern

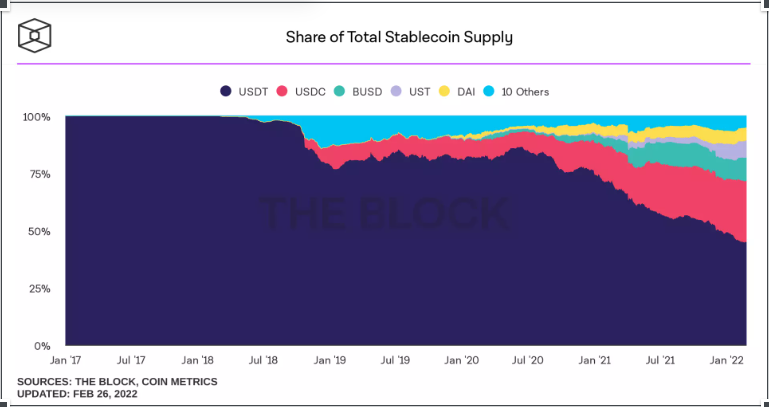

Stablecoins make up a significant portion of the total market capitalization in cryptocurrency, with a market size exceeding $180 billion. In its simplest definition, a stablecoin is a digital currency whose value is pegged to a “stable” reserve asset—typically the U.S. dollar. For institutions, stablecoins serve as a gateway into the broader digital asset market, offering higher yields and faster settlement than fiat while retaining the benefit of low volatility.

Despite the promise of decentralization across crypto, stablecoins today are still dominated by centralized products. Over 80% of the market is represented by fiat-backed assets—such as USDC and USDT, issued by centralized entities Circle and Tether Holdings respectively.

As regulatory scrutiny increases on centralized stablecoins, decentralized alternatives become more attractive. In December 2020, the market cap of fiat-backed stablecoins was 21 times that of algorithmic stablecoins. Today, that ratio has narrowed to just 5 times.

This article is an in-depth analysis of Frax Finance, an algorithmically backed stablecoin whose market cap has grown nearly 530% since October 2021. With a protocol total value of $2 billion, it is currently the fastest-growing protocol.

Building a resilient, algorithmically supported stablecoin is extremely difficult and requires achieving three core capabilities:

Stability (low volatility)

Maintaining a peg to the chosen asset over time

High utility (integration with the broader ecosystem)

In his book *Civilization*, historian Niall Ferguson attributes the West’s economic dominance over other regions to six key factors—including competition, property rights, and medicine—which he calls “killer applications.”

Haseeb Qureshi of Dragonfly likens Layer 1s to cities, while Balaji refers to a digitally native nation as a “crypto civilization.” In this piece, inspired by Niall Ferguson, we refer to Frax as a civilization akin to the West. Hear us out.

We have identified three killer applications that enable Frax to outperform competitors.

Keep reading to learn how Frax beats the competition:

What is Frax?

Collateral Ratio

How Frax Beats Competitors: 3 Killer Applications

Killer App 1: Everyone Wants to Be Curve

Killer App 2: Frax Flex

Killer App 3: Algorithmic Market Operations (AMO)

What is Frax?

According to current stablecoin typology (which lacks a unified paradigm), Frax can be classified as a "partially crypto-collateralized stablecoin" with the following characteristics:

Backed by cryptocurrencies—supported by crypto assets rather than fiat.

Partially collateralized. The value of minted tokens is partially backed by assets held in reserve. This contrasts with over-collateralized tokens (e.g., DAI) or completely uncollateralized ones (e.g., the now-defunct Basis).

Decentralized. Governed by the community and not owned by any central entity (e.g., Tether is owned by Tether Holdings, USDC by Circle).

Dual-token model. The protocol also issues a secondary token, $FXS, used for governance and capturing a share of protocol revenues.

Pegged to the nominal U.S. dollar ($1), not freely floating (unlike RAI).

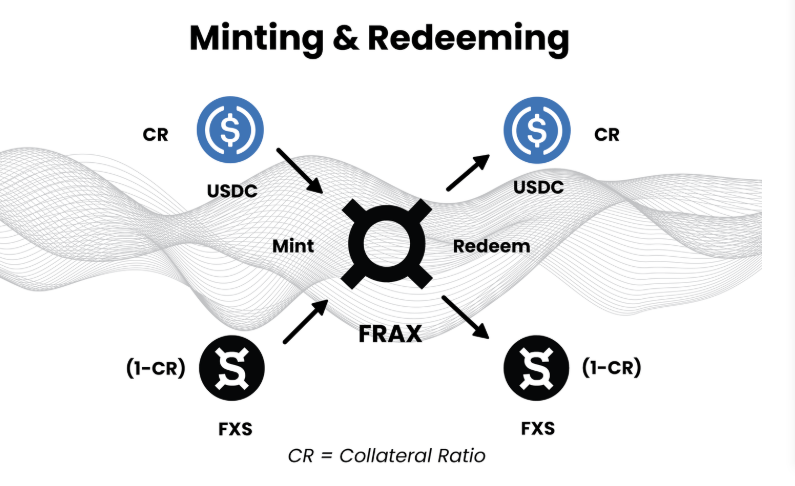

Collateral Ratio

The Collateral Ratio (CR) determines how much collateral users must deposit to mint one FRAX (currently at 85%). FRAX is the stablecoin pegged to $1. FXS, on the other hand, is Frax Finance’s governance token. Together, they form the stablecoin’s fiscal model.

This means that to mint $1 worth of FRAX, you need to deposit $0.85 worth of USDC (or another accepted collateral) and $0.15 worth of FXS. Conversely, if you redeem your FRAX, you receive $0.85 in USDC and $0.15 in FXS.

Frax’s CR is dynamic. It fluctuates based on market supply and demand forces, changing during periods of FRAX expansion or contraction. When rising demand pushes FRAX above its peg, the CR decreases—requiring less collateral and more FXS to mint new FRAX.

Because Frax’s CR mechanism mirrors the operations of central banks, analysts often compare it to an “automatic central bank on-chain.”

Now that we understand the basics of Frax, let’s explore its killer applications!

How Frax Beats Competitors: 3 Killer Applications

Killer App 1: Everyone Wants to Be Curve

Currently, the hottest topic in DeFi is the “Curve Wars.”

It refers to the competition among protocols on Curve Finance—an automated market maker (AMM)—for liquidity dominance. Curve is the most popular decentralized swap exchange, boasting nearly $18 billion in TVL. Its main differentiator compared to competitors is low slippage and fees.

Why is the battlefield Curve instead of Uniswap or other DEXs? The answer lies in Curve’s protocol design around its CRV token. Curve’s tokenomics feature two key aspects:

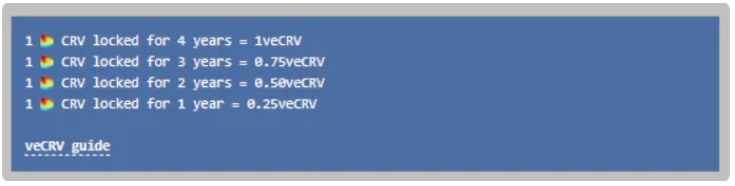

1. Vote-locked Model: When you provide liquidity to a pool on Curve, you earn a share of all trading fees from that pool. Additionally, you earn CRV tokens as incentives for providing liquidity. By staking and “locking” your CRV, you receive veCRV—granting you voting power and governance rights as a token holder.

2. Gauge System: veCRV holders vote on how much CRV emissions each liquidity pool receives—a metric known on Curve as “gauge weight.” The more votes a pool gets, the more CRV rewards go to its liquidity providers. More attractive rewards naturally draw more liquidity providers to incentivized pools.

Why does this matter? For any DeFi protocol, liquidity is paramount. And Curve holds $18 billion in TVL—the top tier of liquidity. A new protocol can deposit its native token paired with another (e.g., FRAX-ETH) into a pool to bootstrap liquidity. Alternatively, a protocol can “cheat” by finding ways to boost CRV rewards for their pool. Others see high APY and naturally become liquidity providers.

Complexity emerges from simple rules.

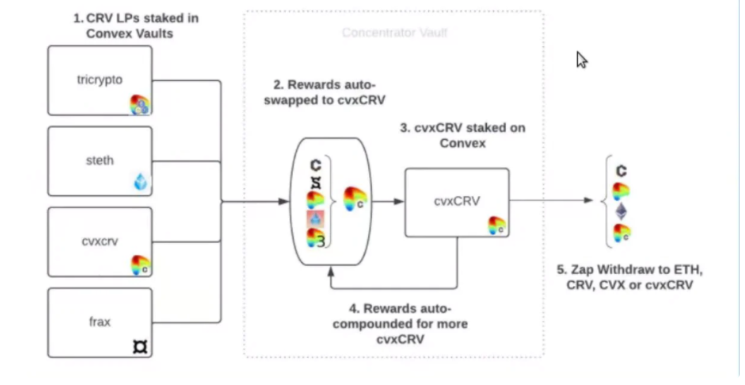

Convex Finance emerged as a CRV aggregator. Here's how Convex works:

You deposit your CRV into Convex and receive cvxCRV in return.

Convex stakes your CRV on Curve to obtain veCRV.

Convex earns rewards from Curve and redistributes them to cvxCRV holders.

cvxCRV is immediately liquid, unlike veCRV on Curve, which requires lock-up.

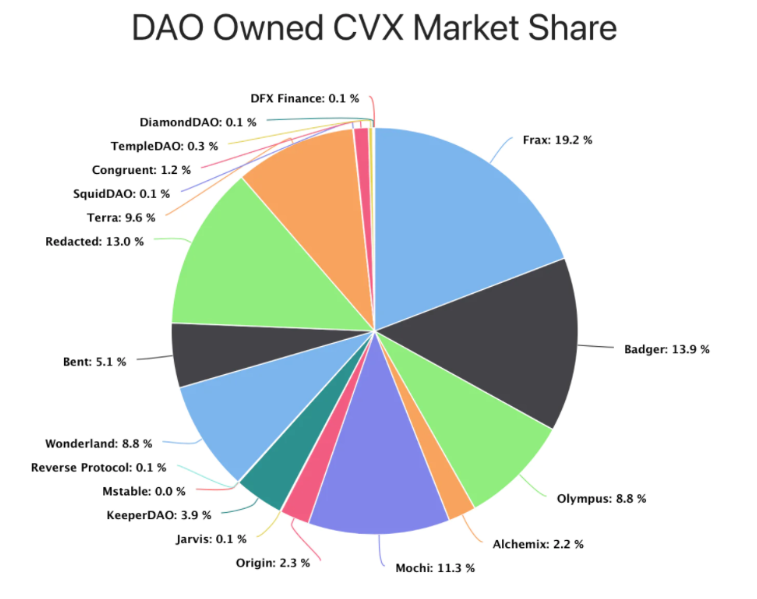

Convex became like Curve itself—but with the added benefit of liquidity. As a result, it accumulated most of the CRV tokens. Today, it controls 52% of Curve’s voting power and has locked 200 million CRV in veCRV since inception. Protocols seeking to incentivize liquidity either buy CVX tokens or “bribe” CVX holders to vote for their gauge.

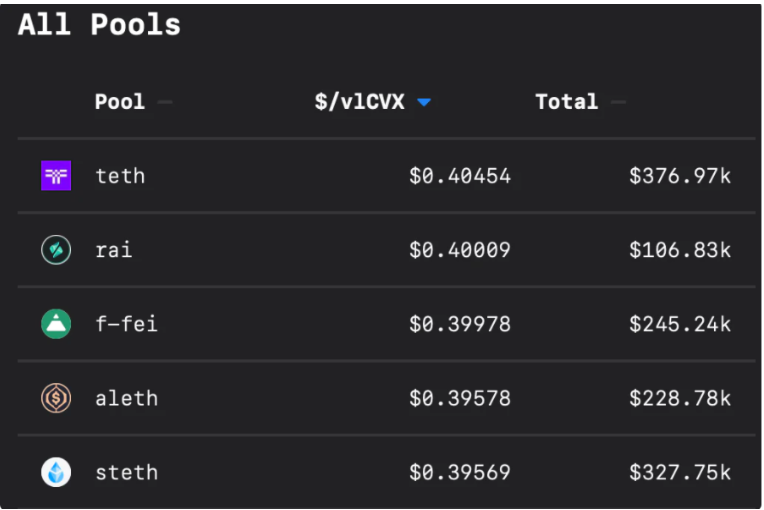

The screenshot above is from the bribery platform Votium. It shows the cost, in dollars, to bribe one dollar’s worth of vlCVX—a vote-locking Convex token allowing holders to vote with Convex’s $veCRV on Curve’s gauge weights. Protocols bribe CVX holders to vote for their liquidity pools. With higher gauge weights, Curve emits higher APY rewards. Higher APY attracts more liquidity.

Winning on Curve’s Turf

Frax has consistently won battles on Curve’s turf.

As the largest holder of CVX, Frax directs its share of veCRV within Convex to steer more CRV rewards toward FRAX-denominated pools.

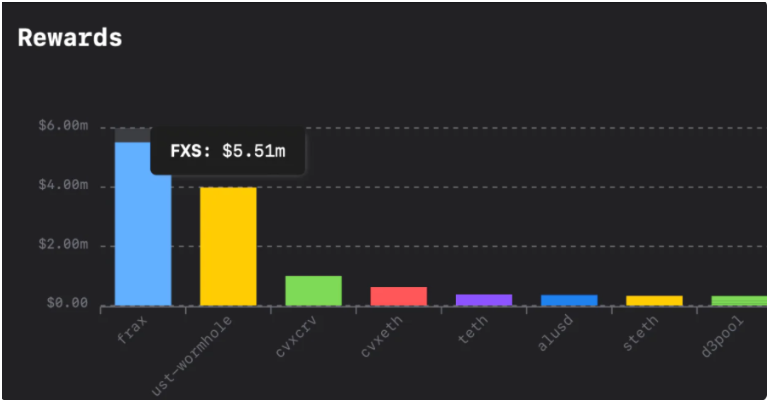

Moreover, compared to other stablecoin protocols, FRAX pays the highest bribes weekly on the Votium platform.

With better rewards (higher APY), Frax attracts more liquidity providers, driving further adoption. Frax’s deeper liquidity ensures a more stable peg.

The largest Frax pool on Curve is the FRAX3CRV pool, allowing users to swap FRAX against the three major stablecoins: USDT, USDC, and DAI. With approximately $1.5 billion of FRAX deposited, large swaps have minimal price impact. This provides FRAX with a buffer against tail-risk sell-offs.

In short, liquidity begets liquidity.

If You Can’t Beat Them, Join Them

Curve’s dominance in the liquidity wars is undeniable. Strategically, every protocol should aim to become like Curve—ideally, having others build on top of them.

However, the Lindy effect suggests Curve may remain unchallenged for some time. Therefore, if you can’t beat Curve, become Curve!

To do so, Frax adopted Curve’s tokenomic model, implementing a vote-locked governance system where FXS holders can lock their tokens to receive veFXS.

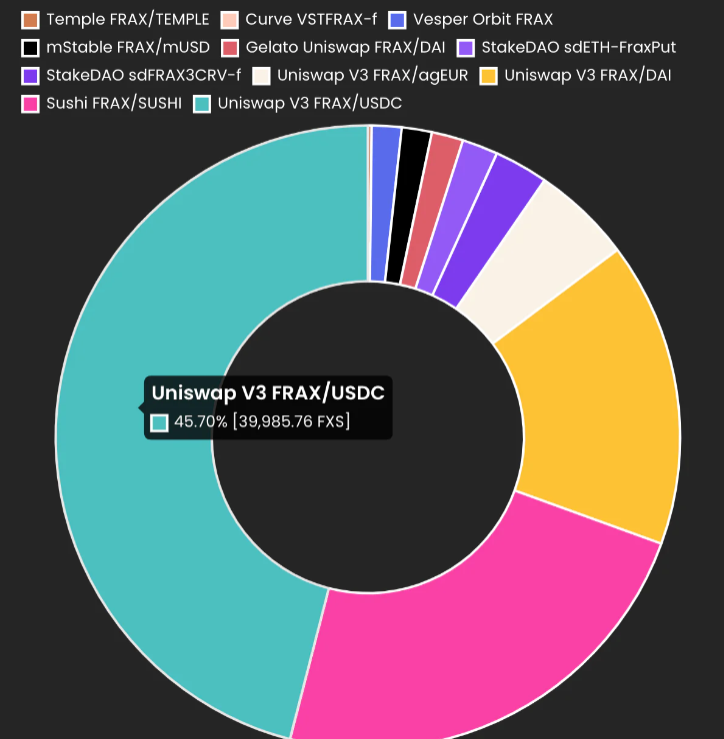

While veCRV holders determine gauge weights for specific pools on Curve, veFXS holders vote on gauges to direct FXS emissions across different pools on various DEXs. For example, the largest pool, Uniswap V3 FRAX/USDC, receives over 45% of emission rewards.

Recently, Convex partnered with the Frax protocol to further align incentive programs—particularly around locking veFXS within the CVX protocol. Convex sees itself not just as a veCRV aggregator but with a broader ambition—to serve as a voting power aggregator for all types of ve-tokens.

By controlling FXS emissions, Frax strengthens liquidity by incentivizing LPs to stake in FRAX-denominated pools—mirroring Curve’s approach. To keep FXS emissions directed to their pools, LPs convert FXS rewards into veFXS governance power. As FRAX penetrates more protocols and trading pairs, its market cap grows. As FRAX’s dominance rises, FXS emissions become more valuable. Soon, every protocol will want a slice of the FXS gauge to directly incentivize their liquidity pair!

In short, the Frax War is the Curve War.

Second, there’s currently a battle among protocols to become the preferred liquidity pairing token for emerging DAOs. We call this the “DAO Liquidity War.” Competitors include Rift Finance, Fei & Rari, OlympusDAO, and other emerging protocols.

If the Curve War is about liquidity, the DAO Liquidity War is about utility.

Every stablecoin wants to become the ecosystem’s default unit of account. If Frax wins the DAO Liquidity War, it locks emerging DAOs into a mutually dependent relationship by offering FRAX as one side of their liquidity pair.

As more trading pairs use FRAX, its utility increases. When FRAX becomes the primary reserve currency of choice for DAOs, it starts functioning as the on-chain dollar equivalent. The winner of the DAO Liquidity War will be crowned king—the trusted denomination for business and trade across the entire ecosystem.

The prize of the DAO Liquidity War is protocol hegemony.

Killer App 2: The Frax Flex

Frax’s Flexibility

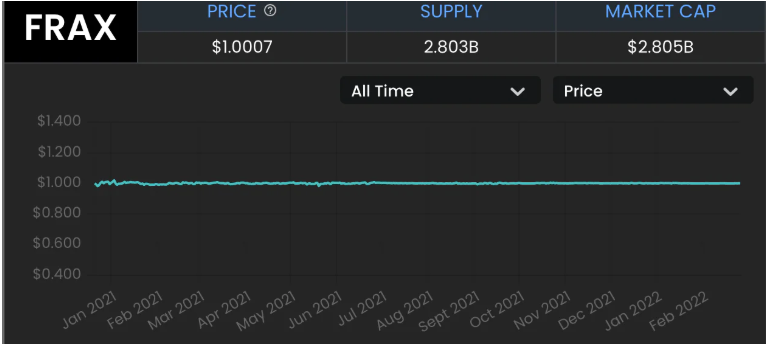

FRAX has never depegged since launch. Compared to peer algorithmic stablecoins like Iron Finance and Fei, this is remarkable.

We attribute its strong peg to its dual-token flywheel design. FXS acts as a complementary token to FRAX, absorbing volatility from the dollar-pegged FRAX while distributing protocol value to its holders. The flywheel works as follows:

FXS has a maximum supply of 100 million tokens

Protocol revenue is funneled to FXS holders via buybacks and burns

Both FXS and USDC serve as collateral for minting FRAX

FRAX becomes indispensable in DeFi, increasing revenue and boosting FXS price

As FXS gains value, the collateral ratio decreases

Eventually, FRAX becomes fully backed by FXS alone—no longer requiring any other stablecoin collateral, let alone centralized USDC

The paradox here is that building a resilient, fully algorithmic stablecoin requires starting with partial collateralization. Yet doing so might even lead to over-collateralization! This non-trivial roadmap resembles Web2’s “bottom-up disruption” strategy.

Frax Price Index (FPI)

Frax continues stacking inflation-resistant features onto its dollar-pegged stablecoin. On January 1, 2022, Sam Kazemian, co-founder of Frax, tweeted that the team was developing the Frax Price Index (FPI)—a new native stablecoin.

FPI will be pegged to a decentralized Consumer Price Index (CPI), built atop Chainlink’s custom CPI oracle designed for FRAX, incorporating crypto-native elements. Token holders will see their balance increase monthly in USD terms, based on reported CPI growth. This is possible because Frax earns yield from the underlying FPI treasury, funded by users minting and redeeming FPI using FRAX.

The exact peg mechanism remains unclear, but early documentation suggests FPI has money-market fund-like properties—it offers a guaranteed quarterly yield with high liquidity. However, maintaining such a peg on-chain may require innovative mechanisms. Sam mentioned in a Twitter Space that by tracking a 12-month trailing CPI (TTM), all volatility within a year is smoothed out. FPI is also backed by deep liquidity from both Frax and Fei. Its goal is to become the unit of exchange for DAO contributor compensation. Ultimately, it aims to create a crypto-native CPI representing the median cost of living from a global basket of goods.

We await further details. This is truly an exciting feature with the potential to pioneer Stablecoin 2.0.

We remain cautiously optimistic: ultimately, stablecoins embody the true destiny of programmable money—one untethered from the nominal dollar!

Killer App 3: Algorithmic Market Operations (AMO)

In March 2021, Frax v2 introduced what is arguably its best innovation to date: Algorithmic Market Operations (AMO).

To understand this, consider the fiat-world analogy.

Central banks (e.g., the Federal Reserve) control money supply through “open market operations.” By buying (or selling) government bonds in the market, the Fed effectively increases (or decreases) the total circulating supply of dollars in the monetary system.

AMOs employ a similar strategy. The Frax protocol influences the supply of FRAX across the broader DeFi ecosystem. Moreover, anyone in the community can propose an AMO strategy through governance.

For any AMO strategy, we can break it down into four key components—de-collateralization, market operation, re-collateralization, and burning.

Let’s examine the Curve AMO strategy:

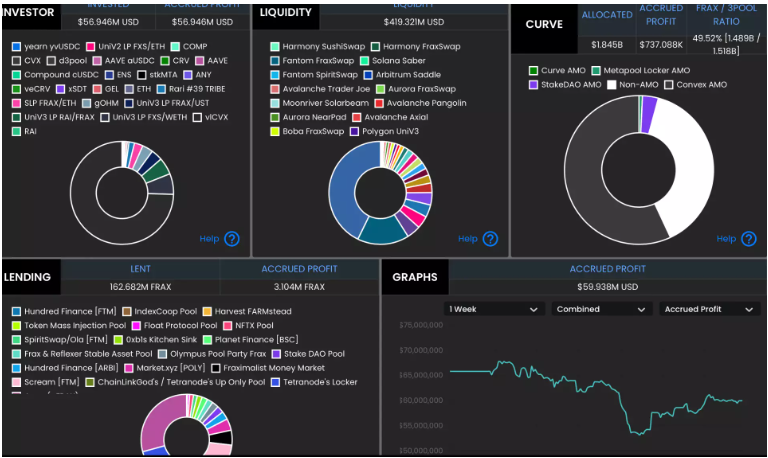

De-collateralization—The algorithm determines how much excess collateral (in USDC and FRAX) currently sits idle in the Frax protocol’s treasury. Excess collateral refers to assets beyond what’s required by the collateral ratio to back the total FRAX supply.

Market Operation—The AMO injects idle USDC and FRAX into the FRAX3CRV Curve pool, strengthening liquidity and reinforcing the dollar peg.

Re-collateralization—When the treasury nears the minimum collateral threshold, the AMO removes liquidity from Curve’s 3pool and re-collateralizes the protocol.

Burning—Using revenue generated from LP swap fees, the protocol mints new FRAX at the collateral ratio, then uses those funds to buy back and burn FXS. This process is governed by the FXS1559 standard.

AMOs allow the protocol to earn LP rewards and trading fees in a capital-efficient manner. Profits are then distributed to veFXS holders. The protocol also actively intervenes in markets to provide liquidity for the FRAX stablecoin, thereby strengthening its peg—similar to how central banks (e.g., Hong Kong Monetary Authority) deploy foreign reserves to maintain currency pegs (e.g., HKD-USD).

Other stablecoins rely on arbitrageurs and speculators to maintain their peg. Frax takes matters into its own hands.

The Blossoming Landscape of Algorithmic Stablecoins

Frax is not the only algorithmic stablecoin in today’s market—and it won’t be alone in the future.

At the end of the day, stablecoins are products fulfilling specific jobs-to-be-done (JTBD). Are you a leveraged speculator? Then over-collateralization suits you—buy DAI or MIM. Are you a DAO managing a $10M+ treasury? Then look to FEI and FRAX. Are you an institutional investor seeking low-risk exposure to crypto? Then consider UST and UXD. Each user has unique needs.

Risk profiles and use cases vary significantly across stablecoins. Nevertheless, we remain optimistic that FRAX will serve as a benchmark for future DeFi protocols due to its three killer applications—Curve-like properties, robust peg mechanics, and AMO.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News