Bitget UEX Daily | US Commerce Secretary Urges South Korean Storage Giant to Expand Production in the US; Waller Forms Expert Team to Review Monetary Policy Framework; SK Hynix Lists on Nasdaq Today

TechFlow Selected TechFlow Selected

Bitget UEX Daily | US Commerce Secretary Urges South Korean Storage Giant to Expand Production in the US; Waller Forms Expert Team to Review Monetary Policy Framework; SK Hynix Lists on Nasdaq Today

The overall consensus is "finding structural opportunities amidst divergence," rather than a comprehensive rebound in risk appetite.

I. Hot News

Fed Dynamics

Fed Chair Warsh Forms External Expert Team to Comprehensively Review Monetary Policy Framework

- Kevin Warsh announced the establishment of five independent working groups (inflation, balance sheet, employment, data, communication), led by well-known economists and former central bank officials (including Chetty, Anderson, Mankiw, etc.), aiming to assess whether tools, analysis methods, and frameworks adapt to rapid economic transformation.

- The working groups will submit fact-oriented analysis to the FOMC, emphasizing that the commitment to price stability and full employment is "unwavering".

- Market Impact: The review signal shows the Fed is proactively adapting to AI and structural changes, strengthening expectations for policy flexibility in the short term, helping stabilize interest rate path pricing, and reducing excessive hawkish concerns.

International Commodities

US-Iran Conflict Escalates Again: Trump Announces End of Ceasefire and Resumption of Strikes

- Trump stated that due to Iran's continued attacks on ships in the Strait of Hormuz, the ceasefire has ended; the US military struck at least 170 military targets in Iran within 48 hours, and Iran countered by attacking US bases. Israel shared intelligence on a "new Iran assassination plot against Trump," and Trump temporarily changed planes after the NATO summit (preventive security measures).

- Pakistan and Qatar continue to mediate; US officials say technical negotiations are ongoing, and Iran must never possess nuclear weapons. Some Republican lawmakers worry rising oil prices will drag down the midterm elections.

- Market Impact: Geopolitical risks push up short-term oil price volatility and risk-aversion sentiment, but actual supply shock is limited; the decline in oil prices shows market expectations for rapid escalation are cooling, and precious metals receive temporary support.

Macroeconomic Policy

US Temporarily Does Not Impose Additional Tariffs on Commercial Aircraft and Jet Parts; OpenAI Officially Launches GPT-5.6 and Negotiates Adjustments with Government

- After completing the investigation, the Department of Commerce decided not to impose taxes for now, turning instead to negotiate with trade partners; if no effective agreement is reached within 180 days, Trump may take further action. OpenAI released the Sol/Terra/Luna model series, adjusted after consultations with Lutnick, Bessent, etc., and opened to the public in phases.

- Former Fed Chair Bernanke joined the Anthropic Long-Term Interest Trust, responsible for overseeing AI social impact and board appointments.

- Market Impact: The tariff suspension alleviates aviation supply chain pressure; AI regulatory collaboration signals are positive for the long-term certainty of large model companies, while highlighting the government's deep involvement in AI infrastructure.

II. Market Review

Commodities & Forex Performance (Real-Time Update)

- Spot Gold: 4120 USD/oz, -0.09%

- Spot Silver: 60.02 USD/oz, +0.14%

- WTI Crude Oil: 71.95 USD/bbl, -0.18%

- Brent Crude Oil: 76.00 USD/bbl, -0.24%

- US Dollar Index (DXY): 100.819, -0.14%

Despite the escalation of the US-Iran conflict (Trump resuming strikes, changing planes, and assassination intelligence) triggering geopolitical concerns, crude oil only recorded a slight decline; analysts generally believe the market has fully digested the risk premium—actual supply shock is limited, coupled with weak global demand and easing expectations brought by Pakistan and Qatar mediation. Institutions such as Goldman Sachs had previously lowered the 2026 oil price center; current price action confirms the "conflict controllable" narrative. Gold dipped slightly, Silver rose slightly, showing divergence: safe-haven buying was offset by strong US tech stocks and rebound in risk appetite, while Silver was supported by industrial demand; analysts from MUFG etc. pointed out that Fed Chair Warsh's framework review and meeting minutes show policy divergence, higher-for-longer expectations limit precious metals' upside space. The US Dollar Index softened simultaneously, reflecting risk asset rebound dominance. The overall linkage logic is clear—geopolitical disturbance remains, but macro liquidity and institutional consensus on "limited escalation" dominate short-term pricing, crude oil under pressure, precious metals range-bound.

Cryptocurrency Performance

- BTC: 63100 USD, 24h +1.5%

- ETH: 1744 USD, 24h +0.25%

- Total Cryptocurrency Market Cap: 2.26 trillion USD, 24h +约 1.7% (approx. 1.7%)

- Market Liquidation Situation: 24h total liquidation approx. 175 million USD, short liquidation approx. 108 million USD

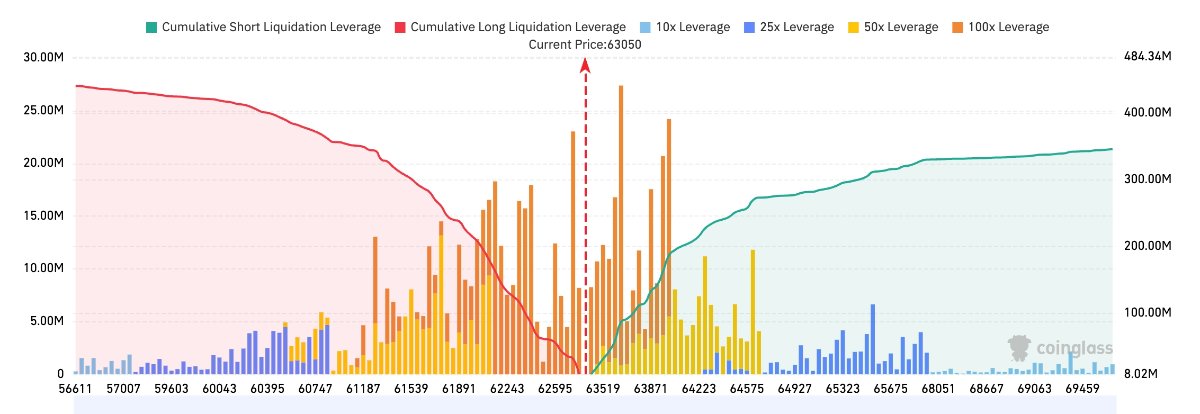

- Bitget BTC/USDT Liquidation Map: Current BTC price is approx. 63,050 USD, a large amount of short liquidation is gathered in the 63,500–64,500 USD area above, where leverage positions are most dense near 63,800–64,000 USD; if this range is broken, it may trigger a new round of short squeeze 行情 (market). Below, there is a noticeable long liquidation band in the 62,000–62,800 USD area, but the overall cumulative liquidation scale below is weaker than above, so short-term market liquidation pressure still leans towards the upside direction.

- Spot ETF Net Inflow/Outflow: BTC Spot ETF net outflow of 0.15 billion USD yesterday, current 24h dynamic net outflow of 0.15 billion USD.

Driver Analysis: BTC performance is relatively strong, ETH sideways, total market cap moderately rebounded, reflecting risk appetite remains resilient amidst geopolitical disturbance. ETF turned to slight outflow yesterday, leverage liquidation scale is controllable and long/short relatively balanced, showing market deleveraging has been phased completed. Macro level Fed framework review and tech stock strength form support, but oil price decline and USD stabilization limit large upside. Overall trend leans towards oscillation repair, BTC leading over ETH differentiation continues "institutional preference for large-cap coins" characteristic, technical side focus on upside liquidation pressure release situation.

US Stock Index Performance

- Dow Jones: 52487.41 (+0.27%), continuous moderate close up

- S&P 500: 7543.64 (+0.81%), broad-based steady upward

- Nasdaq: 26206.89 (+1.30%), tech and chip sectors drive obviously

Tech Giants Dynamics

- NVDA: approx. 203.50 USD, -0.8%

- AAPL: approx. 316.00 USD, +0.4%

- MSFT: approx. 392.00 USD, +1.3%

- GOOGL: approx. 357.00 USD, -1.4%

- AMZN: approx. 245.00 USD, +0.4%

- META: approx. 615.00 USD, +4%

- TSLA: approx. 407.00 USD, +3.2%

- SPCX: 152 USD, +2.6%

- MU: 991.64 USD, +4.52%

Performance Summary and Driver Analysis: Tech sector overall strong but significant differentiation: Storage and AI infrastructure (MU, AMD, AVGO) lead, benefiting from Commerce Secretary urging Korean firms to expand US capacity and Micron's $250 billion investment plan; META surge stems from Zuckerberg denying compute oversupply and emphasizing cloud business commercial potential; TSLA boosted by Optimus mass production guidance. NVDA slight pullback reflects valuation digestion and competition concerns, GOOGL under pressure from specific events. Driver factors significantly differentiated—policy and capacity landing benefit storage, company strategic narrative benefits META/TSLA, rather than unified "AI optimism" logic.

Sector Movement Observation

Memory Chip Sector Up Over 3%

- Representative Stocks: Micron Technology (MU) up 4.52%, AMD up nearly 6%

- Drivers: US Commerce Secretary Lutnick publicly urged SK Hynix and Samsung to expand US memory capacity, coupled with Micron significantly raising local investment, alleviating AI HBM/memory shortage expectations, funds quickly poured in.

Semiconductor Equipment Up About 2%

- Representative Stocks: Broadcom up over 3%

- Drivers: AI capital expenditure continuity expectations rebound, coupled with SK Hynix IPO approaching boosting sentiment.

III. US Stock Deep Dive

1. SK Hynix - Nasdaq Secondary Listing Launch

Event Overview: SK Hynix ADR final pricing 149 USD/share, fundraising approx. 26.5 billion USD (slightly reduced from previous 28-29 billion USD target), oversubscribed over 7 times, showing institutional demand in AI storage track is extremely strong. Lead underwriters are BofA, Citi, Goldman Sachs, JPMorgan, expected commission pool over 140 million USD. Stock will start trading on Nasdaq on July 10 with SKHYV code on when-issued basis,转为 (turn to) regular trading code SKHY from July 13. Simultaneously, US Commerce Secretary Lutnick publicly urged SK Hynix and Samsung to expand US memory chip capacity to alleviate global AI key component shortage, and plainly said "hope to bring competitors to set up factories in the US," even if Micron CEO may not welcome it. Prospectus shows, this fundraising is mainly used for new factory construction and equipment expansion, to match AI explosion demand for HBM and other high bandwidth memory.

Market Interpretation: Wall Street generally views this as one of the largest foreign company IPOs in history (second only to SpaceX), institutions view it as "AI supply chain core target", valuation expected to be revalued due to US stock liquidity and analyst coverage (previous Korean stock discount was obvious). Multiple investment banks pointed out, oversubscription and high commissions reflect long-term optimism on HBM supply-demand tension, but there are also voices warning large-scale listing may trigger institutions to sell Micron, Nvidia and related targets for position adjustment, causing sector volatility in short term. Lutnick's statement is interpreted as US "chip reshoring + ally capacity sharing" policy accelerating landing, beneficial for global memory leaders, but intensifies Micron competition pressure.

Investment Implication: Listing day liquidity and volatility will be extremely intense, long term then benefits from US local capacity and AI HBM super cycle dual drive, focus on its share contest with Micron.

2. Meta Platforms - Zuckerberg Denies Compute Oversupply and Advances Cloud Business

Event Overview: Zuckerberg clearly denied "compute oversupply" tone in latest statement, plainly said "I don't know who in the industry thinks their compute is oversupplied," and confirmed Meta is seriously considering renting part of AI infrastructure to external enterprises, cloud business "definitely has commercial potential". Company simultaneously officially launched paid version Muse Spark 1.1 model (first AI model charged to enterprises), API pricing aggressive (input approx. 1.25 USD/million Token, far lower than competitors), and provides new users 20 USD free quota. Zuckerberg emphasized the model performs excellently on agentic tasks, coding, tool use etc. benchmarks (e.g. MCP Atlas 88.1%), and criticized peer pricing "too extreme". Previous shareholder meeting already revealed "cloud business definitely on the table", external enterprises almost every week come to inquire buying compute or API services.

Market Interpretation: Institutions generally interpret as Meta from "pure burning money AI investment" to "potential high profit cloud/API revenue" narrative key turn. Multiple analysts believe, aggressive pricing expected to grab developer share, form network effect similar to ad business; simultaneously deny oversupply + confirm cloud plan, effectively alleviates market concern on 145 billion USD level capital expenditure "overconstruction". Short term stock price elasticity significant, some investment banks raise confidence on Meta AI monetization path, believe it can use ad cash flow advantage to fight price war.

Investment Implication: Cloud business if landing, will reshape Meta valuation logic, from "social + ad" to "AI infrastructure + model" diversified evolution, short term catalyst clear but need observe actual signing progress.

3. Micron Technology - US Investment Exceeds $250 Billion Before 2035

Event Overview: Micron July 9 officially announced, will raise US local investment total to over 250 billion USD (by 2035), increased approx. 50 billion USD compared to previous commitment, target is to raise US DRAM capacity proportion to 40%. Same day simultaneously held New York Clay super factory "first shovel concrete" ceremony (US largest semiconductor manufacturing base), Idaho factory expected 2027 mid produce first wafers, 2028 end second plant production. New York project expected create 50,000 jobs (including 9,000 direct positions), US total over 90,000. CEO Sanjay Mehrotra thanked Trump, Lutnick etc. government officials support, emphasized "data and memory are modern economy cornerstone", and simultaneously added max 3 billion USD supply chain strengthening funds.

Market Interpretation: This move is viewed by Wall Street as most direct response to US "CHIPS Act" and Trump government "manufacturing reshoring" policy, and also "first move layout" to Lutnick urging Korean firms expand capacity. Institutions generally give positive evaluation: capacity landing will significantly raise Micron in AI HBM and advanced DRAM global share and profit rate stability, simultaneously create employment and supply chain safety premium. Some analysts pointed out, large-scale investment short term may suppress free cash flow, but long term supply-demand tension (AI demand explosion) will convert to pricing power and valuation revaluation. Stock price same day surged over 4%, reflecting market quickly pricing policy and demand dual catalyst.

Investment Implication: Long term capacity and policy dividend clear, short term benefits from sentiment and sector rotation; focus on 2027 first wafer realization progress and HBM share change.

4. Tesla - Optimus Gen3 Mass Production Target Issued

Event Overview: According to LatePost and other multi-party supply chain messages, Tesla recently issued Optimus Gen3 specific part procurement guidance to suppliers, requiring September capacity raise to 1000 units/week, year end further reach 2000-2500 units/week (corresponding to annualized approx. 100,000 units part supply capacity). Musk previously already reviewed and approved latest Gen3 design at executive meeting, means after over three years R&D formally walk out of lab. Supply chain ahead approx. two months see August hundreds of units orders, Fremont factory will first start mass production (initially slower), Austin dedicated factory simultaneously under construction (long term plan ten million level capacity).

Market Interpretation: Institutions and supply chain analysis generally believe, this is Optimus from "concept demo" to "true mass production realization" key node. Nomura, UBS etc. previously already raised short term shipment expectations (2026 approx. 25,000 units), this hard index further verifies execution power. Market interprets as robot business starts contributing substantive revenue expectations (single unit target price approx. 20,000 USD), expected to become TSLA valuation from "auto + energy" to "embodied intelligence" leap new pillar. Short term supply chain orders landing boosts sentiment, but mass production ramp initial yield and cost still exist uncertainty.

Investment Implication: Robot from narrative to delivery inflection point nearing, if September capacity meets standard will significantly raise long term valuation anchor; short term volatility still affected by auto delivery and macro influence.

5. Oracle - Credit Rating Downgraded to Edge of Investment Grade

Event Overview: S&P Global Ratings July 9 downgraded Oracle long-term issuer credit rating from BBB to BBB- (investment grade lowest tier), outlook stable. Main reason is AI infrastructure business rapid expansion leads to overall business risk rise and cash flow significantly weaken: expected 2027 fiscal year capital expenditure surge to 90-95 billion USD (previous expectation approx. 60 billion), free operating cash flow deficit or expand to approx. 42 billion USD. Company debt scale has reached approx. 160 billion USD, simultaneously customer concentration (OpenAI, xAI, Meta etc.) risk rises. Despite this, Oracle cloud contract backlog orders still as high as 638 billion USD, stock price same day rose against trend.

Market Interpretation: Institution views significantly differentiated: rating agencies emphasize "AI burning money" impact on traditional software giant financial flexibility structure, remind investors focus on high leverage expansion fragility; but most buyers and analysts more focus on its huge cloud backlog orders and AI infrastructure first-mover advantage, believe short term cash flow pressure can be covered by long term contracts, downgrade instead creates buy opportunity. Some investment banks pointed out, this is AI era "asset-heavy transformation" typical growing pains, similar phenomenon or appear on other traditional tech companies.

Investment Implication: AI investment return cycle lengthens, high debt expansion companies face rating and financing cost pressure; focus on its FCF inflection point and customer contract conversion rate, short term volatility or exist structural opportunities.

IV. Cryptocurrency Project Dynamics

1. Bloomberg reported, South Korea memory chip manufacturer SK Hynix completed American Depositary Receipt issuance, total fundraising 26.5 billion USD, per share 149 USD, total issued 177.9 million ADRs, surpassing Alibaba to become US history third largest IPO, second only to Alibaba's 25 billion USD record. Issue price compared to Seoul stock Thursday close price premium approx. 3%, subscription over seven times, nearly half ADRs by top ten order accounts subscribed, demand close to 200 billion USD. SK Hynix occupies 57% share in global HBM market, this issuance coincides with AI infrastructure investment boom, company will participate in South Korea government led 880 billion USD investment plan with Samsung Electronics. ADR expected to start regular trading on July 13.

2. According to CoinDesk report, only June one month, US spot Bitcoin ETF net outflow 4 billion USD, led by BlackRock IBIT, funds turn to AI trading and SpaceX IPO etc. opportunities. Bitcoin second quarter fell approx. 14%, broke below 60,000 USD, recorded continuous third quarter loss. However, this outflow is dwarfed before 2 trillion USD private credit market. Second quarter private credit redemption requests reached 15.6 billion USD, 16 business development companies had 10 break 5% quarter limit, most investors only partially paid. Fitch expects future months redemptions will continue, unmet requests will make multiple companies continue under pressure.

Bitcoin ETF liquidity strong, outflow directly affects BTC price; private credit BDC then opposite, belongs to non-liquid long-term tools. Both simultaneously suffered redemptions, reflecting market on liquidity and risk wide concerns. Energy market similarly sent risk-aversion signals, US strategic petroleum reserve at 1983 since lowest. QCP Capital summarized: "Different fields, same pattern: market buffer space is narrowing." And pointed out strategic petroleum reserve bottoming, Strategy first sell BTC pay dividend, private credit redemption break threshold, three together show risk assets face harder environment.

3. Insiders revealed, US "Clarity Act" unified version may earliest be published next week, merged Senate Banking Committee and Agriculture Committee work results, expected July 20 week submit Senate full vote.

4. Bitwise Senior Investment Strategist Juan Leon said, current Bitcoin bear market with previous cycles fundamentally different, institutional adoption is accelerating. Bitwise customers divided into two types: already held Bitcoin over two years investors view decline as "add position opportunity", while other large capital still waiting for clearer regulatory signals. Leon said this round 50% decline is Bitcoin "mildest structural bear market", compared to 2022 78% and 2018 84% decline, "bottom every cycle is lifting".

5. Cathie Wood under Ark Invest Thursday bought 217,896 shares Circle stock, value approx. 13.7 million USD, CRCL same day fell 1.65% to 63.01 USD. Ark simultaneously sold 85,319 shares Robinhood stock, value approx. 9.8 million USD, HOOD same day rose 1.39% to 115.11 USD.

V. Today's Market Calendar

Data Release Schedule

Important Event Preview

- SK Hynix Nasdaq Listing Trading Start: All day - Memory sector sentiment barometer

- US-Iran Conflict Follow-up Statements and Mediation Progress: Anytime - Oil price and risk-aversion asset volatility source

Institutional Views:

Past 24 hours US stock tech and memory strong, oil price decline, precious metals strong, crypto oscillation repair, known investment banks overall views positive but cautious: most believe US-Iran conflict although disturbance but did not change AI capital expenditure main line, storage and compute related targets (MU, AMD, SKH related) obtained policy and demand dual catalyst; BofA etc. reaffirmed Nvidia fundamentals not reversed, valuation discount enticing; on crude oil then more bearish short term geopolitical premium fade. Crypto aspect institutions generally pointed out ETF outflow and liquidation controllable, BTC relative resilience shows institutional configuration still in, but need wait for macro data further clear. Overall consensus is "find structural opportunities in differentiation", rather than comprehensive risk appetite rebound.

Disclaimer: The above content is organized by AI search, manual verification only for publication, not as any investment advice. Data in the text inevitably has deviations, please refer to market instant data.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News