Bitget UEX Daily Report | Energy Sector Rises, Optical Communication Concept Stocks Strengthen; US Dow Jones Index Plunges Over 570 Points; BTC Spot ETF Records Net Inflows for 3 Consecutive Days (July 09, 2026)

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Energy Sector Rises, Optical Communication Concept Stocks Strengthen; US Dow Jones Index Plunges Over 570 Points; BTC Spot ETF Records Net Inflows for 3 Consecutive Days (July 09, 2026)

Short-term volatility may persist, while long-term allocation can still focus on the main themes of AI capital expenditure and institutional fund inflows.

I. Hot News

Federal Reserve Updates

No significant new developments in Federal Reserve updates

- Today, New York Fed President Williams, Dallas Fed President Logan, and other officials will speak. The market will focus on their views regarding the inflation path, labor market resilience, and the potential transmission effect of geopolitical events on inflation through energy prices.

- Institutions generally believe that the Fed's policy path remains highly data-dependent in the short term. Geopolitically driven oil price increases may temporarily push up inflation expectations but have not changed the overall direction of rate cuts unless energy prices continue to rise significantly and translate into core inflation pressure. Market Impact: Trump's remarks have reduced the extreme downside risk for risk assets in the short term, boosting market risk appetite to some extent. However, persistent geopolitical uncertainty will maintain high volatility and potentially disrupt inflation expectations and the Fed's policy reaction function through energy price channels. Institutions suggest focusing on the impact of subsequent developments on the interest rate path for the September FOMC meeting, as well as the transmission intensity of oil prices to core PCE.

International Commodities

Oil prices oscillate at high levels after Trump's cooling remarks, geopolitical premium remains

- Trump's tough stance on the Iran ceasefire agreement triggered a sharp rise in oil prices, followed by cooling remarks that led to violent oscillations at high levels. The daily amplitude of WTI and Brent Crude expanded significantly, indicating high market sensitivity to Middle East supply risks.

- Traditional safe-haven assets such as Gold and Silver retreated slightly, mainly due to阶段性 risk appetite repair brought by Trump's remarks, while a stronger US Dollar Index exerted pressure on precious metals. However, both remain in historically high absolute price ranges, indicating that long-term safe-haven and inflation hedging demand has not significantly subsided.

- The market continues to focus on Middle East supply chain risks, particularly the security status of key energy channels such as the Strait of Hormuz, as well as the potential impact of geopolitical events on global energy trade flows, inventory levels, and refining capacity. Market Impact: Oil prices partially gave back gains after a short-term surge, reducing extreme inflation concerns. However, geopolitical uncertainty will maintain higher volatility in energy prices and potentially disrupt the Fed's policy path through cost-push inflation channels. Institutions believe that the complex linkage between oil prices, risk assets, and the US Dollar Index will continue. It is recommended to focus on the transmission intensity of energy prices to core inflation and their impact on the September FOMC interest rate decision.

II. Market Review

Commodities & Forex Performance

- Spot Gold: Approx. 4,079 USD/oz, -0.05%

- Spot Silver: Approx. 58.50 USD/oz, -0.08%

- WTI Crude: Approx. 74 USD/barrel, +1.11%

- Brent Crude: 78.9 USD/barrel, +1.14%

- US Dollar Index (DXY): 101.002, -0.06%

Driver Analysis: Trump's remarks, first threatening then cooling, directly pushed up oil price volatility, with geopolitical risk premiums dominating energy and precious metals trends. The US Dollar Index strengthened due to risk aversion, exerting pressure on gold, but long-term inflation and safe-haven demand still provide support. Institutional views suggest short-term oil prices are prone to event-driven moves, while gold oscillates in a high range. Focus on whether Middle East developments further cool down or escalate. Asset correlation shows some divergence between risk assets and safe-haven assets; short-term trading should beware of event shocks.

Cryptocurrency Performance

- BTC: Approx. 62,165 USD, -2.12%

- ETH: Approx. 1,738 USD, -2.18%

- Total Cryptocurrency Market Cap: 2.22 trillion USD, -1.8%

- Market Liquidation Situation: 24h liquidations approx. 317 million USD, mainly long positions liquidated at 262 million USD

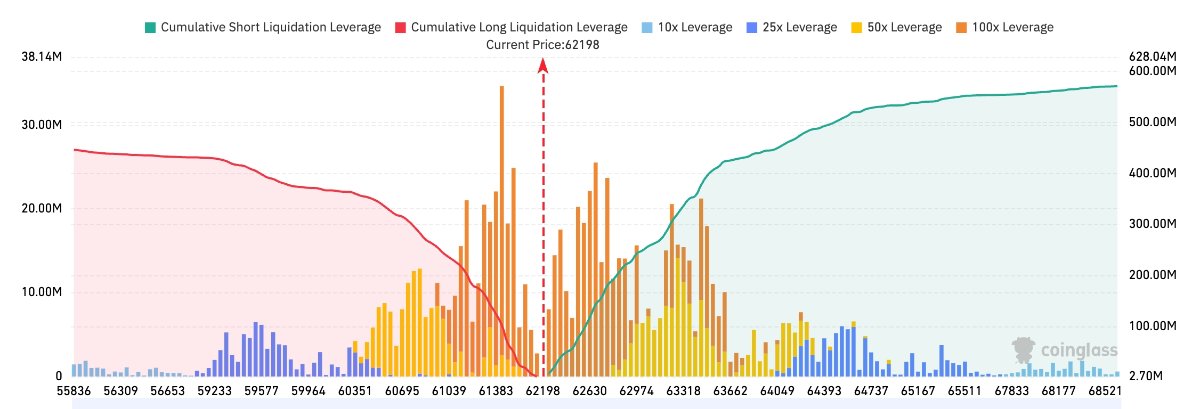

- Bitget BTC/USDT Liquidation Map: Current BTC price is approx. 62,198 USD. The 62,600–63,400 USD area above has the densest short liquidations. If the price continues to rebound and break through this range, it may trigger concentrated short covering, pushing the market further upward. Below, near 61,000–62,000 USD, there is a concentration of long liquidations. If the price falls below the current support range, it may trigger a chain reaction of long liquidations, potentially strengthening short-term downward momentum.

- Spot ETF Net Inflow/Outflow: BTC Spot ETF had a net inflow of approx. 21.5 million USD yesterday, currently showing a dynamic net outflow of 25.8 million USD within 24h.

Driver Analysis: Geopolitical events exerted 阶段性 pressure on risk assets. BTC found support near 62,000 USD. Leverage liquidations were mainly long positions, indicating the market structure remains biased long. Continuous net inflows into ETFs provide important support for spot prices, and institutional capital allocation willingness has not significantly reversed. Technically, BTC is oscillating in the 60,800-64,500 USD range in the short term. ETH is relatively resistant to declines but lacks independent catalysts. The overall trend is still dominated by macro risk sentiment and USD trends. In the short term, focus on the impact of Trump's subsequent remarks and Middle East developments on the leverage market.

US Stock Index Performance

- Dow Jones: Closed at 52,348.39 points (-1.09%), under pressure for two consecutive days

- S&P 500: Closed at approx. 7,483 points (-0.28%), key support range 7,450-7,480

- Nasdaq: Closed at approx. 25,871 points (+0.2%), partial rebound in the tech sector provided support

Tech Giants Updates

- NVDA: 196.93 USD (+0.71%)

- AAPL: 310.66 USD (-0.64%)

- MSFT: 388.84 USD (+0.54%)

- GOOGL: 367.03 USD (+0.16%)

- AMZN: 245.98 USD (+0.75%)

- META: 615.58 USD (+2.55%)

- TSLA: 394.06 USD (-2.19%)

Performance Summary and Driver Analysis: Significant divergence within the sector. META led gains (+2.55%), benefiting from advertising business resilience and AI investment expectations; NVDA rebounded slightly, showing AI themes still attract some capital amidst volatility; AAPL and TSLA were under pressure, with TSLA's larger decline possibly affected by geopolitical and macro risk appetite fluctuations. MSFT, AMZN, and GOOGL performed relatively steadily. Overall, tech giants did not show consistent declines, reflecting unchanged market confidence in the long-term logic of AI capital expenditure, but short-term geopolitical events and a stronger USD exerted pressure on high-valuation stocks. Institutions believe divergent trends will continue and suggest focusing on differences in fundamentals and capital flows.

Sector Movement Observation

Energy Sector rose (driven by oil prices)

- Representative stocks: Chevron (CVX) intraday gain over 2%, Diamondback Energy (FANG) led gains over 3%, Exxon Mobil (XOM) followed up intraday approx. 1.5%, Occidental Petroleum (OXY) gain over 2.5%

- Drivers: Trump's announcement that the Iran ceasefire agreement was "over" directly pushed up geopolitical risk premiums. The market worried about Middle East supply chain disruptions and crude oil supply tightness. The sharp rise in WTI crude prices drove upstream oil and gas company stocks to significantly outperform the broader market. The energy sector was one of the few leading sectors on July 8.

Optical Communication Concept Stocks strengthened

- Representative stocks: Ciena up over 5%, Credo Technology up nearly 5%, Astera Labs up nearly 3%, Lumentum up over 1%, Coherent up nearly 1%

- Main Drivers: Explosion in high-speed optical interconnect demand for AI data centers, volume release of 800G/1.6T optical modules and CPO technology, continued high Capex from cloud giants, capital spreading from GPUs to the connection layer.

III. In-depth Analysis of US Stocks

1. Exxon Mobil (XOM) - Trump's Iran Remarks Push Oil Prices, Upstream Performance Sensitive in Short Term

Event Overview: On July 8, Trump announced the Iran ceasefire agreement was "over," directly triggering a sharp rise in WTI crude prices. The energy sector became one of the leading sectors of the day. As the world's largest listed oil and gas company, Exxon Mobil's upstream exploration and production and downstream refining businesses are highly sensitive to oil prices. Intraday, XOM followed oil prices up, but affected by overall market selling pressure, it closed slightly down to approx. 141.13 USD. The market is closely tracking Q3 inventory data changes and the potential impact of Middle East supply chain risks on the company's capital expenditure plans. Market Interpretation: Institutions such as JPMorgan and Barclays believe short-term oil price surges will contribute extra profits to XOM's upstream business, but if Trump successfully pushes for cooling developments, geopolitical premiums may dissipate quickly. Multiple investment banks upgraded short-term ratings for the energy sector, while emphasizing that event duration is the key variable determining Q3 performance elasticity. In the long term, XOM's low-carbon transition layout and stable high dividend policy still hold allocation value. Investment Implication: Short-term event-driven trading opportunities are obvious. It is recommended to focus on low-buy windows during oil price pullbacks and configure with hedging strategies.

2. Nvidia (NVDA) - AI Capital Expenditure Resilience Highlights Amidst Geopolitical Volatility

Event Overview: Trump's geopolitical remarks triggered market risk appetite fluctuations, and the semiconductor sector showed significant divergence. As the absolute leader in AI GPUs, Nvidia's data center business growth was not directly impacted by geopolitical events. On July 8, the Nasdaq rebounded slightly, and NVDA showed relative resilience. The market continues to focus on Blackwell platform shipment progress and AI capital expenditure guidance from major hyperscalers. Some profit-taking pressure appeared amidst volatility, but the core demand logic remains unchanged. Market Interpretation: Institutions such as Goldman Sachs and Morgan Stanley maintain buy ratings, pointing out that "AI factory construction is the largest infrastructure expansion in human history," and the capex super cycle is still underway. Even if short-term geopolitical uncertainty suppresses risk appetite, long-term training and inference demand is solid. Analysts emphasize NVDA's dominant position in the GPU ecosystem is difficult to shake in the short term. Investment Implication: Focus on allocation value after pullbacks amidst volatility, avoid chasing highs, suitable for investors holding AI trends long-term.

3. Microsoft (MSFT) - Cloud & AI recurring revenue Buffers Geopolitical Shocks

Event Overview: Microsoft showed strong resilience against the backdrop of a sharp Dow Jones decline and S&P 500 pullback. Its Azure cloud business and Office 365, Copilot, and other recurring revenue structures have limited direct impact from geopolitical events. AI infrastructure and enterprise cloud services continue to advance. Even in a risk-averse environment, institutional capital still favors its diversified business and stable cash flow. On July 8, tech heavyweight stocks partially rebounded, and MSFT contributed important support. Market Interpretation: Institutional views believe Microsoft's strong cash flow and highly diversified business (Cloud + AI + Consumer Software) significantly reduce single geopolitical event risks. Investment banks generally maintain overweight ratings, emphasizing its core position in global AI infrastructure and the continued advancement of enterprise AI adoption. Investment Implication: Suitable as a defensive configuration option to reduce overall portfolio volatility; conservative investors can hold long-term.

4. Chevron (CVX) - Oil Price Rise Directly Beneficial, Upstream & LNG Business Benefit Significantly

Event Overview: After Trump's Iran-related remarks pushed up oil prices, upstream weighted energy stocks such as Chevron performed strongly intraday, with gains exceeding 2% at times. Chevron's upstream exploration and production and LNG liquefied natural gas business have high sensitivity to oil and gas prices, and geopolitical premiums directly translate into short-term performance elasticity. The market is focusing on its Q3 production data and Middle East project progress, as well as the impact of low-carbon investments on long-term returns. Market Interpretation: Multiple investment banks pointed out that short-term oil price surges bring extra profits to CVX's upstream and LNG businesses, but the event-driven characteristic is obvious. If developments cool quickly, premiums may be quickly given back. Institutions upgraded short-term ratings for the energy sector, while reminding the need to continuously track the potential impact of geopolitical event evolution on capital expenditure and dividend policies. Investment Implication: Short-term event-driven opportunities are prominent. It is suggested to take profits at high oil prices or re-evaluate allocation during pullbacks, and focus on the use of hedging tools.

IV. Cryptocurrency Project Updates

1. Glassnode released a report pointing out that Bitcoin remains in a deep value region after five months below the real market mean and short-term holder cost basis. Long-term holder realized losses account for 43% of total realized value, peaking at 280 million USD daily, the highest since December 2022; ETF net outflows have eased from June peaks but remain net outflows on a monthly basis, with average daily trading volume of 650 million to 950 million USD, down approx. 80% from October 2025 peaks. Derivatives holdings have cautiously shifted to long, with the put/call ratio at 2026 lows, but the options market remains defensively skewed, with spot prices far below the max pain point of 66,000 USD.

The report believes bottoming conditions are in place—on-chain supply redistribution is underway, institutional outflows are slowing, derivatives are de-risking—but confirmation signals have not yet arrived. The market still needs further cooling of surrender pressure, stabilization of institutional capital flows, and recovery of the real market mean to confirm a pattern shift.

2. Cathie Wood's Ark Invest bought 181,847 shares of SpaceX stock on Wednesday, worth approx. 27 million USD. SPCX fell 0.81% that day, closing at 148.26 USD, down cumulatively 13.5% over the past five trading days.

3. Wall Street Journal reporter Nick Timiraos stated that the Fed's June meeting minutes show分歧 among officials mainly stem from different judgments on future economic trends, rather than fundamental conflicts on rate hike or cut strategies. Two possible scenarios have formed within the Fed: if inflation remains persistently high, almost all officials believe higher rates need to be maintained, or even further tightening; but if inflation falls quickly to the 2% target level, almost all officials also believe current rates can be maintained, or even future rate cuts. He believes the phrase "falls quickly to 2%" is very key, leaving policy adjustment space for the Fed.

4. SpaceXAI released a new artificial intelligence model named Grok 4.5, created in collaboration with AI programming startup Cursor, aiming to narrow the gap with competitors such as Anthropic and OpenAI. Grok 4.5 aims to handle complex, long-running tasks including software engineering, legal, and financial services, and enhances cybersecurity capabilities.

5. According to Bloomberg, South Korean memory chip giant SK Hynix's listing on Nasdaq received over seven times subscription. This issuance involves 177.9 million American Depositary Receipts (ADR), attracting demand from global long-term funds, sovereign wealth funds, and tech sector institutional investors. Bloomberg calculations show this issuance scale is approx. 24.5 billion USD, expected to become the second-largest foreign company listing case in US history, second only to Alibaba's 25 billion USD.

6. According to the latest report from TASS, a senior Iranian source stated that due to US threats, Iran has officially suspended negotiations with the US on a final solution. Previously reported, US-Iran negotiations were scheduled for July 11 in Pakistan, discussing sanctions, frozen Iranian funds, and nuclear issues.

V. Today's Market Calendar

Data Release Schedule

Important Event Preview

- Trump's Follow-up Remarks: Continuously track the latest developments in the Middle East and their impact on oil prices and risk assets.

- Fed Officials' Speeches: Focus on latest signals on inflation path and policy interest rates.

July 9 (Thursday)

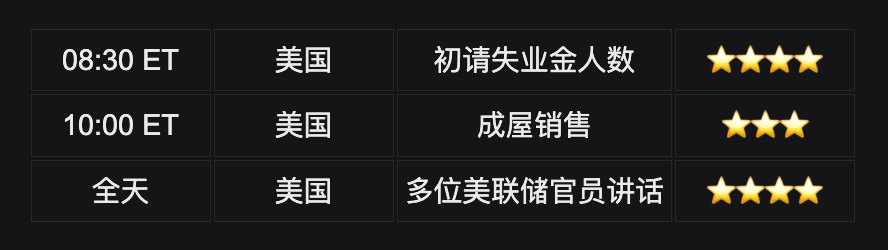

- New York Fed President Williams speaks at 21:00;

- US Initial Jobless Claims for the week ending July 4 released at 20:30.

July 10 (Friday)

- Dallas Fed President Logan speaks at 01:30;

- SK Hynix ADR tentatively lists on Nasdaq on July 10 ★★★★

Institutional Views:

Multiple investment banks believe Trump's cooling remarks temporarily alleviated some of the most pessimistic geopolitical scenarios, but Middle East tensions still constitute a persistent risk premium. Oil and gold volatility will continue to dominate short-term pricing, and a stronger US Dollar Index may exert 阶段性 pressure on risk assets. In the crypto market, continuous ETF net inflows are seen as an important positive signal, with BTC receiving dual support from institutions and leverage capital in the current range. Overall, the market is in a "event-driven + data verification" phase. It is recommended to maintain flexible positions, focusing on Initial Jobless Claims and Existing Home Sales data for corrections to Fed policy expectations, as well as Trump's subsequent diplomatic dynamics and their transmission to energy and safe-haven assets. Short-term volatility may persist, but long-term allocation can still focus on the main lines of AI capital expenditure and institutional capital inflows.

Disclaimer: The above content is organized by AI search,人工仅作验证发布 (manual verification only for publication), and does not constitute any investment advice. Data in the text inevitably contains deviations; please refer to real-time market data.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News