The Logic Behind Tungsten Prices Surging 10-Fold: China Supply Cutoff, US Arms Shortage, Niche Metal Becomes Hard Currency

TechFlow Selected TechFlow Selected

The Logic Behind Tungsten Prices Surging 10-Fold: China Supply Cutoff, US Arms Shortage, Niche Metal Becomes Hard Currency

The Logic Behind the 10-Fold Surge in Tungsten Prices: China Supply Cutoff, US Arms Shortage, Why This Niche Metal Became Hard Currency.

Author: 0xKyle

Compiled by: TechFlow

TechFlow Editor's Note: Gold and silver crashed, copper and platinum cooled down, last year's "Commodity Supercycle" fizzled out in less than a year. But this time is different—AI data centers, military rearmament, and de-globalization are exerting pressure simultaneously, and certain niche metals are brewing a real structural shortage. Tungsten, the industrial metal with the highest melting point, greatest hardness, and almost irreplaceable properties, has seen its price rise nearly 10-fold in the past year, behind which lies the triple squeeze of sharp reduction in China supply, surge in US munitions demand, and explosion of new demand from photovoltaic silicon wafer cutting.

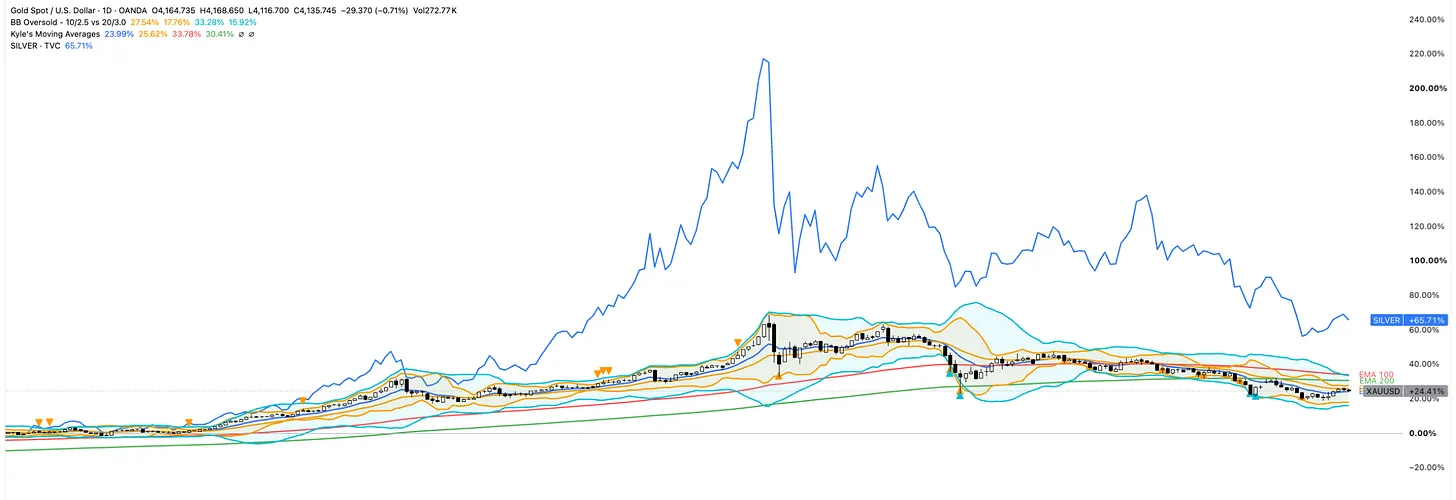

Gold and silver experienced a surge in the past year, but subsequently corrected sharply, both showing double-digit plummet from their highs. The once imminent "Commodity Supercycle" seems to have cooled down—I remember during that period, people were going long on copper (widely used copper wire in data center construction), platinum (shortage story), zinc, aluminum, etc.

Earlier this year, we welcomed "Commodity Supercycle v2"—this time due to the closure of the Strait of Hormuz, people thought we would face an oil shortage, plus weather factors (El Niño), and a large amount of fertilizer needed to be transported through the strait (fertilizer stocks saw a violent rebound, companies like CF rose more than 70% at price peaks), we would lack corn and wheat during this year's harvest season.

Here are a few points to note. First, we are indeed experiencing a shift from bits to atoms—from software to hardware. The main driver is AI, semiconductor construction is in full swing. But beyond that, protectionist measures are being implemented as the US aims to rebuild its manufacturing capacity, repatriate talent, and achieve self-sufficiency again. All this leads to increased demand for various assets, ultimately transmitting down to the raw materials themselves.

Also true is that in the market, neither of these two "Commodity Supercycles" lasted too long—as shown in the chart above, many of them eventually fell back to reasonable levels after the crisis passed. They were all a "large basket trade", metals like platinum, zinc, and aluminum were closely related to supply shortage meeting new demand; once demand was met, they would be significantly repriced.

However, I don't think this is the end. I think it makes sense to prepare for Supercycle 2.0—this time it doesn't look like a single unified boom, more like a set of fragmented independent cycles. Major factors are still at play—de-globalization, AI, and energy transition are driving a broader, more durable cycle, plus supply constraints caused by years of underinvestment. But it is important to pick the right commodities, because each commodity has its own reasons for rising/falling. In fact, many commodities should be viewed as independent assets in the market.

Take gold for example, it has monetary/macro drivers, global central banks are buying, de-dollarization was the core focus at the beginning of the year. Since the initial argument depended on lower interest rates, higher Fed liquidity, and Trump's instability, gold was a safe haven for investors to protect themselves from uncertainty. However, these factors have all reversed—now interest rates are expected to rise, Fed liquidity has decreased, and Middle Eastern countries like Turkey are also selling off because of what is happening in the region.

Silver follows gold's steps, but with industrial characteristics—the market also thinks there will be a huge shortage of silver, because AI, photovoltaics (solar), and fleet electrification all require silver. There was also a period of tight supply, normal channels could not meet delivery demands.

This reasoning can be applied to all commodities. Each commodity has its unique drivers, beyond the "metals/agricultural products/etc." basket they are usually classified into. Therefore, with the help of AI, I screened the range of commodities and locked in some commodities I like. My view on the commodity supercycle, and the conditions a certain commodity must meet, are as follows:

The commodity supercycle will be fragmented, not broad. The market has differentiated into different micro-markets, a few commodities have structural 利好 (tailwinds), the rest trade according to their own unique supply/demand and cyclical forces.

Characteristics have changed—this is a multi-driver cycle, making it more durable but harder to time. Old cycles had clear narratives (China industrialization) and a clear endpoint. This time driven by multiple factors—energy transition, AI, defense rearmament, de-dollarization, manufacturing capacity repatriation, etc., a certain commodity may be pulled by multiple factors simultaneously. This makes winners more durable, but since there is no single demand engine, nor an obvious bell to mark the top, don't even know when it will play out.

Even having a structural bottom doesn't mean no drawdowns. Observing gold/silver/metals + Iran war situation in the past few months lets me see, this path is extremely volatile—highs are much higher than usual, but the boom-bust characteristics of commodities means must take profits decisively.

In short: Just like everything in investing, selection and timing are everything.

The commodity I finally selected is Tungsten. To be honest, AI gave me 5 commodities based on the following factors: 1) Real multi-year structural story; 2) Real public investment methods—liquid futures/physical, or investable producers; it selected: Copper/Uranium/Tungsten/Silver/Gold.

I narrowed the list to Uranium and Tungsten, simply because I intuitively feel they offer more asymmetric opportunities. Gold, Silver, and Copper are all too large and widely covered, I think it's more of a market timing issue, to figure out when they are the best timing. The path they have traveled so far (e.g. Gold from ~3k > ~5k > ~4k) requires trading around it. And they are somewhat "overbought" to some extent, conditions for continued rise currently seem not mature. Therefore—timing issue.

Uranium is content I hope to cover in future notes about nuclear energy. Excluding these, we are left with Tungsten. Before continuing, I want to emphasize that most of this content was generated by AI through multiple sources, mentioned numbers may not be accurate. I fact-checked these as much as possible, many of these viewpoints come from trusted secondary sources to improve reliability. But ultimately, I am just a monkey with access to machine intelligence, these are just my notes. Continue.

About what Tungsten is and what it does:

It has the highest melting point of all metals (~3422 degrees Celsius), extremely high density, abnormal hardness, which makes it very suitable for industrial tools, aerospace components, military ammunition, etc. This also makes it difficult to substitute—few materials can replicate this without losing performance.

It is mainly extracted from two ores—wolframite and scheelite—then refined into intermediate products (Ammonium Paratungstate, tungsten oxide, carbide powder), these intermediate products are then made into final products.

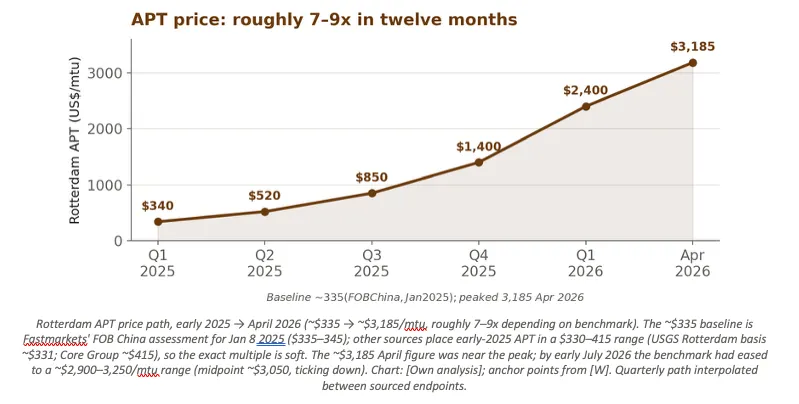

Benchmark intermediate product—Ammonium Paratungstate (APT) rose from about $340/mtu at the beginning of 2025 to a peak of $3185/mtu in April 2026, staying near $3185/mtu as of early July 2026.

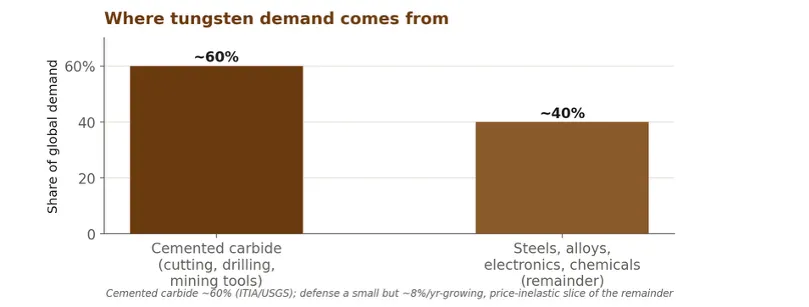

Tungsten is most used in the following applications: Cemented carbide tools (about 60% of demand): Cutting tools, drill bits, and mining/construction blades. Hardness and wear resistance enable them to process steel at high speeds; ceramics, PCD, and CBN only substitute in specific areas, usually at the cost of performance or cost. Defense and ammunition: Density and hardness make it ideal material for armor-piercing projectiles, kinetic penetrators, missile counterweights; one guided multiple launch rocket carries about 50kg of tungsten. Aerospace and superalloys. Heat-resistant alloys used for jet engines, turbine components, and rocket engine nozzles, must withstand extreme temperatures. Semiconductor. High melting point, inertness, and sufficient conductivity make it usable for filling nanoscale connection gaps via chemical vapor deposition (WF₆). Photovoltaic wire. Tungsten wire is increasingly replacing carbon steel wire to cut silicon wafers—finer wire wastes less silicon per cut, this is a fast-growing new demand direction.

Demand/Supply Analysis

The core of this argument is that Tungsten contradicts the argument of demand exceeding supply—this is a supply-dominated shortage, conflicting with growing demand, and building new supply in this market takes years.

Demand Side

Cutting/Cemented carbide tools are in a stable state and hard to substitute. (Note: Tungsten carbide market reports often list automotive or mining/construction as the largest end-user verticals; this is the same demand sliced by downstream industry rather than first-use application)

Substitutes (ceramics, PCD, CBN, molybdenum/niobium carbides) exist, but mostly reduce rather than replace tungsten, usually at the cost of performance or cost.

Supply Side

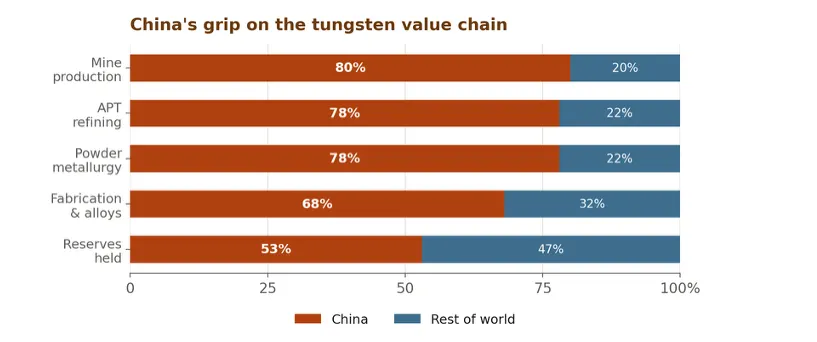

Extreme concentration: About 80-85% of global mineral production comes from China, with an even higher percentage in downstream processing links. In 2025 China mined 67,000 tons out of about 78,000 tons globally—about 86%, and controls 70-85% of every downstream processing stage (USGS data). This concentration even exceeds rare earths, while rare earth origins have gradually diversified. This advantage is converted into leverage—export licensing system implemented for Ammonium Paratungstate and intermediate products starting February 2025 and once completely suspended, later resumed; starting December 2025 tungsten exports restricted to only about 15 approved enterprises.

Geographic depletion: Reported that China's mineral production decreased about 10% year-on-year in 2025 to around 61,000 tons, due to aging mines (some over 30 years), declining ore grades, and environmental rectification; national mining quotas cut by about 6.5%.

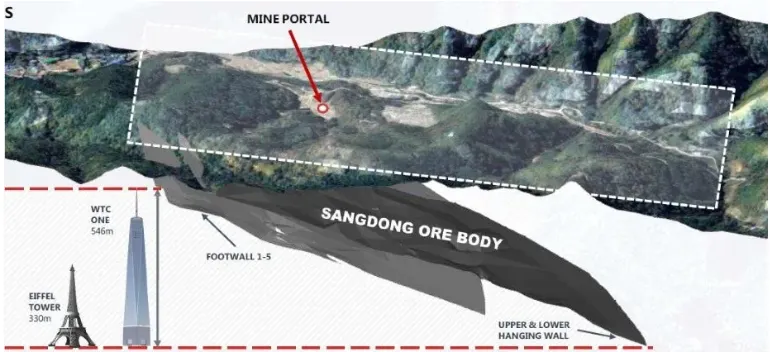

No supply in other parts of the world: The gap persists because supply cannot respond quickly. US has had no commercial tungsten mines since 2015, tungsten mines usually take 5-8 years from discovery to production, due to complex approval processes and specialized metallurgical requirements for low-grade multi-phase ores. Second-layer dependency complicates the problem: most intermediate product refining capacity is still in China, so even mines outside China may rely on Chinese processing. Almonty's Sangdong project (South Korea) is the latest non-China addition—as of July 1, 2026 has entered revenue production stage from development stage. But this is a new project, startup takes time.

Supply/Demand Balance

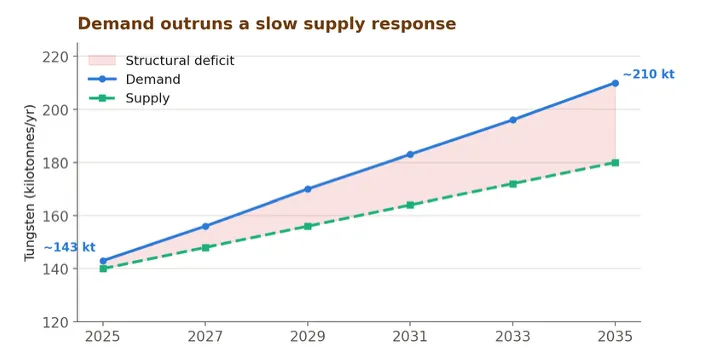

Comprehensive view, structural gap will continue to exist, rather than slow growth of China supply base. Demand grows about 47% by 2035, while supply lags, gaps will continue to appear at least until before 2030.

Gap is huge and narrows slowly: Demand increases from about 143kt to about 210kt by 2035 (Canaccord data), while non-China supply base starts almost from zero. Even if all planned Western projects are realized, incremental tonnage is still limited relative to a market of about 130kt.

Supply structural lag: 5-8 years mine lead time, no mines in US since 2015, most refining still in China, means supply response lags by years rather than months.

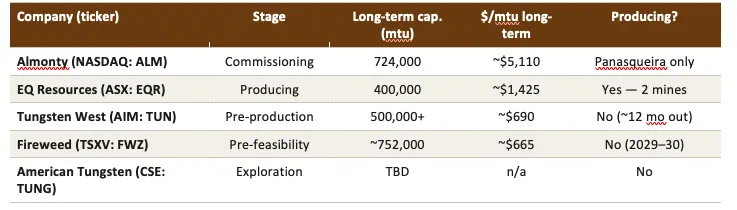

New supply is real but small scale: Sangdong now producing (about 2,300 tons/year, phase 2 about 2027), plus Barruecopardo, Mt Carbine, Hemerdon, Mactung projects—marginal help but cannot fill the gap.

Recycling caps upside space but doesn't fill the gap: About 25-35% demand met by scrap, but only increases after prices maintain high levels for a long time—is a lagged release valve.

Honest warning: Gap size varies by forecaster (CICC predicts about 20,000 MTU in 2028; others predict larger). Direction is well-founded; specific annual tonnage is not conclusive.

Trading Target - ASX: EQR

Since there are no futures contracts and physical ETFs, exposure can only be gained through a few small, illiquid listed mining companies. I personally favor ASX: EQR.

Real producer rather than promise: The only Western multi-mine producer actually selling concentrate—produced 1,678 tons WO₃ in FY2025 at Mt Carbine (Australia) and Barruecopardo (Spain).

Strong revenue inflection: FY2025 revenue 66.1 million AUD, up 146% year-on-year, signed five offtake contracts worth about $124 million (24-month term)—real visibility, in jurisdictions compliant with DFARS requirements.

Huge operating leverage: Based on spot price and about 3,350 tons/year target, forward multiple only about 2x EV/EBITDA (my calculation: about 1.4 billion AUD enterprise value vs about 0.8 billion AUD model EBITDA is about 1.8x). If tungsten price stays high and production ramps up, valuation is cheap.

Currently still losing money: FY2025 net loss 39.2 million AUD (comprehensive loss), group EBITDA negative, ROE about -97%—so "2x" is forward best-case number, not current profitability.

Ramp-up is doubling rather than established fact: This 2x requires production to double from 1,678 tons to about 3,350 tons and spot price to hold. If either condition is not met, multiple will expand.

Balance sheet tight: Net debt about 85 million AUD (70% leverage), current ratio 0.24—net working capital deficit about 97 million AUD—operating cash flow -16.9 million AUD. Still financing through share placement (shares increased 35% year-on-year = real dilution).

Poor liquidity and already surged significantly: Stock price up over 500% within one year.

As mentioned before—each commodity has its own special drivers, in this case, Tungsten is likely to reverse just like oil after Hormuz Strait tensions eased. Specifically:

Policy reversal: The biggest volatility factor is Beijing. Resuming APT exports may dissolve political premium faster than geological gap; structural NATO demand limits drawdown depth but not the fact of sharp adjustment.

First and foremost cyclical commodity: Industrial demand dominates; manufacturing recession historically pulls down tungsten price significantly.

Recycling and inventory release. At this price, scrap recycling and strategic inventory sell-off play a mitigating role.

Thin liquidity, no hedging. No futures system means weak price discovery and two-way volatility; junior miner positions gap during financing events. Therefore position management is important.

Long-term substitution. Currently almost no effective substitutes, but sustained high prices will incentivize conservation and R&D of ceramics/alternative alloys—this is a slow long-term risk.

Tungsten is the clearest realized supply shock in the critical minerals sector: Irreplaceable in core uses, extreme supply concentration weaponized by export policies, real geological depletion, defense deadlines, and supply response in units of years. Pattern structurally bullish, expected gap to last until about 2030.

An honest rebuttal raised by a skeptic is that this is still a weak, unhedgeable cyclical market, leverage driving upside will also drive downside—only public targets are small mining companies, adding execution and financing risk on top of commodity view. The argument is real; the path will not be smooth; "structural" describes multi-year bottom, not protection against violent adjustments along the way.

Thanks for reading Grand Line by 0xKyle! This subscription is free—hope you like this article

If you like this article, share it with people you think will like it

Reports and sources I referenced when writing.

Le Shrub's "Memory Vs Tungsten"

Disclaimer

This article is personal research and commentary, for reference and educational purposes only. This is not investment advice, financial advice, nor a recommendation to buy, sell or hold any securities, commodities or instruments. I am not a licensed financial advisor, content here is not tailored to your situation, goals or risk tolerance. Please conduct your own research and consult licensed professionals before making any investment decisions.

Part of the content of this article—including data, numbers and price levels—was compiled from multiple secondary sources with the help of AI tools (Claude, Gemini). Numbers are approximations, may contain errors, and were fact-checked only on a best-effort basis. Specifically prices, company financial data, production data, deficit estimates and forward multiples should be independently verified against original sources (company filings and named research institutions) before relying on them. Quoted estimates and forecasts belong to their respective authors and may change.

I may hold positions in securities or commodities discussed in the text. I may buy or sell at any time without prior notice. Past performance and historical price trends do not represent future results. You need to be solely responsible for your own investment decisions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News