Zuckerberg starts betting on prediction markets, while Asian countries still view them as gambling.

TechFlow Selected TechFlow Selected

Zuckerberg starts betting on prediction markets, while Asian countries still view them as gambling.

From Elections to Crypto, From Polls to Real Money: How Prediction Markets Become Global Information Infrastructure

Written by: Tiger research

Compiled by: AididiaoJP, Foresight News

Key Points

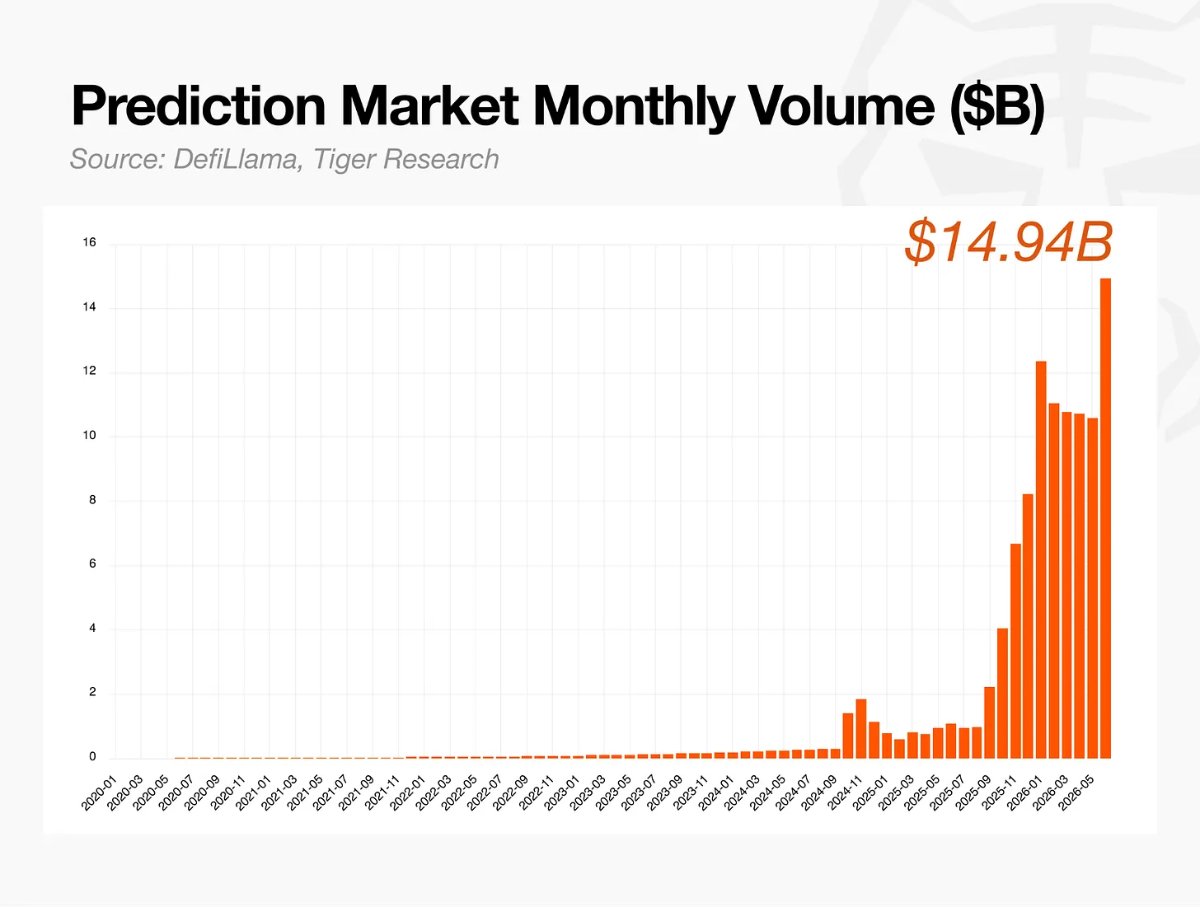

Prediction markets have grown into a mainstream industry, with monthly trading volume reaching $14 billion. The advancement of Meta's own "Arena" project also shows recognition from large tech companies.

The mechanism is simple: if the event occurs, the contract settles at $1; if not, it is $0. Therefore, its trading price is the real-time probability, and the result is confirmed by an oracle after the event ends.

All of this is built on the basis of "skin in the game": participants lose money if they judge incorrectly, which makes their information credible.

Western markets have incorporated prediction markets into the formal financial system, while limited participation in Asia is leading to capital outflow, loss of information sovereignty, and lack of user protection.

The current task for Asia is not to block these markets, but to think about how to responsibly utilize this data within the formal system. Because avoiding discussion actually hands over leadership to foreign countries.

Prediction Markets Have Found Product-Market Fit

For many years, prediction markets mostly stayed at the conceptual stage. The situation changed around 2020, when a few small projects started accumulating significant trading volume and breaking through regulatory barriers one by one, marking the formal formation of prediction markets as an industry.

Growth accelerated thereafter. Currently, monthly trading volume has exceeded $14 billion, and the combined valuation of major platforms is about $40 billion.

Meta's entry further proves it has surpassed the early stage. The New York Times recently reported that Mark Zuckerberg is personally leading a team to develop a prediction market application named Arena. A large tech company investing such resources indicates that this industry has moved out of the experimental phase and established a validated business model.

Where Did Prediction Markets Originate?

Prediction markets are not something new. Before blockchain technology brought them to the public and helped them form an industry, they had been used informally in academia and the financial circle for decades.

Informal Use

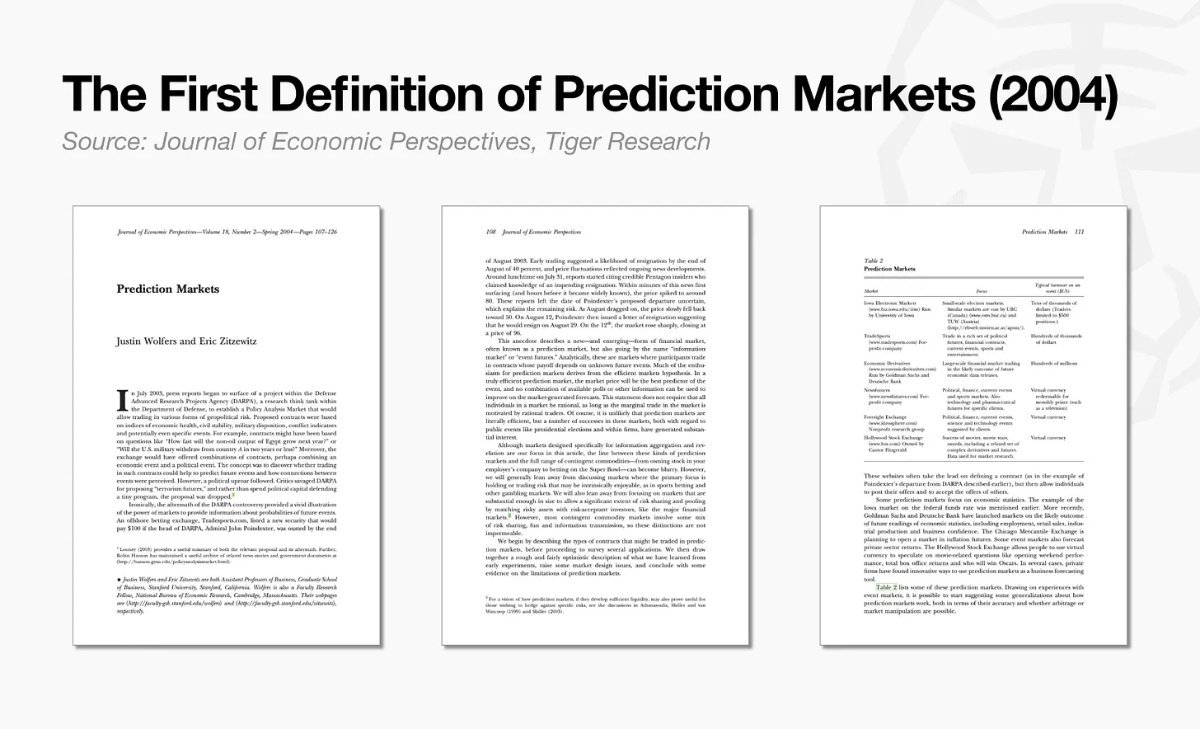

The term "prediction market" itself appeared later than its history. By the 1980s, the concept had various names, such as information markets, decision markets, until an economics paper in 2004 fixed it as "prediction market".

But its underlying practice far predates this name. The earliest form was political betting on election results. In 18th-century London coffee houses, people bet on parliamentary scandals and prime minister changes, and the resulting odds sometimes appeared in newspapers. In 19th-century New York, informal futures markets predicting presidential election results were very active in off-exchange markets near Wall Street.

Academic Use

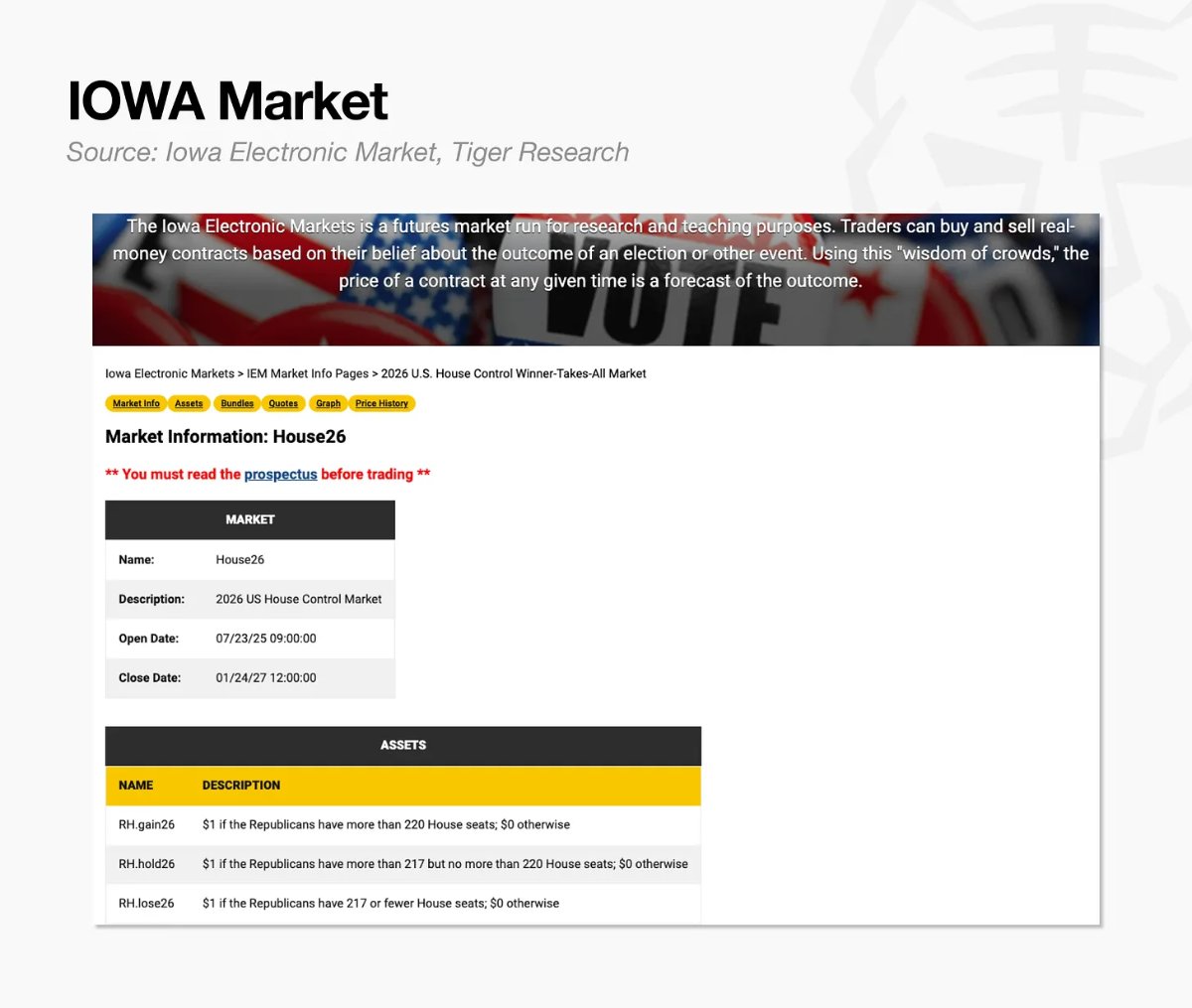

The starting point in academia was three economists from the University of Iowa in 1988. They were confused why polls failed to predict Jesse Jackson's victory in the Michigan primary, so they designed a market where people could directly trade election results. This later became the Iowa Electronic Markets (IEM).

In 1992 and 1993, IEM was approved by the Commodity Futures Trading Commission (CFTC) for research. Anyone who put in $5 could participate. From 1988 to 2004, IEM outperformed traditional polls about three-quarters of the time, becoming a laboratory for aggregating collective judgment into prices. Nevertheless, there was no regulatory framework at the time that allowed it to operate as a public market.

Binary Options

These early prediction markets were very similar to binary options in financial markets: contracts based on yes or no bets on whether the price breaks a certain threshold within a specified time. Its structure—settling at 1 if the event occurs, otherwise 0—is completely consistent with the logic of prediction markets.

Binary options also entered regulated exchanges. Examples include the American Stock Exchange's fixed return options in 2007 and the Chicago Board Options Exchange's binary options based on the S&P 500 in 2008. However, frequent fraud on offshore platforms led multiple major jurisdictions to ban the sale of such products to retail investors between 2017 and 2021. Nevertheless, this yes-or-no binary betting basic structure remains the logical foundation for prediction markets operation to this day.

How Are Prediction Markets Traded Today?

Today, prediction markets cover topics that encompass almost any imaginable event.

Sports events occupy the largest trading volume, thanks to the continuous schedule of leagues and global events, with the ongoing World Cup further boosting popularity. Politics, geopolitics, and macroeconomics range from indicators like inflation data to private company valuation predictions, turning information itself into tradable assets. Cryptocurrency and stock prices, as well as some rumor-driven events, together constitute a complete spectrum from mass interest to professional information demand.

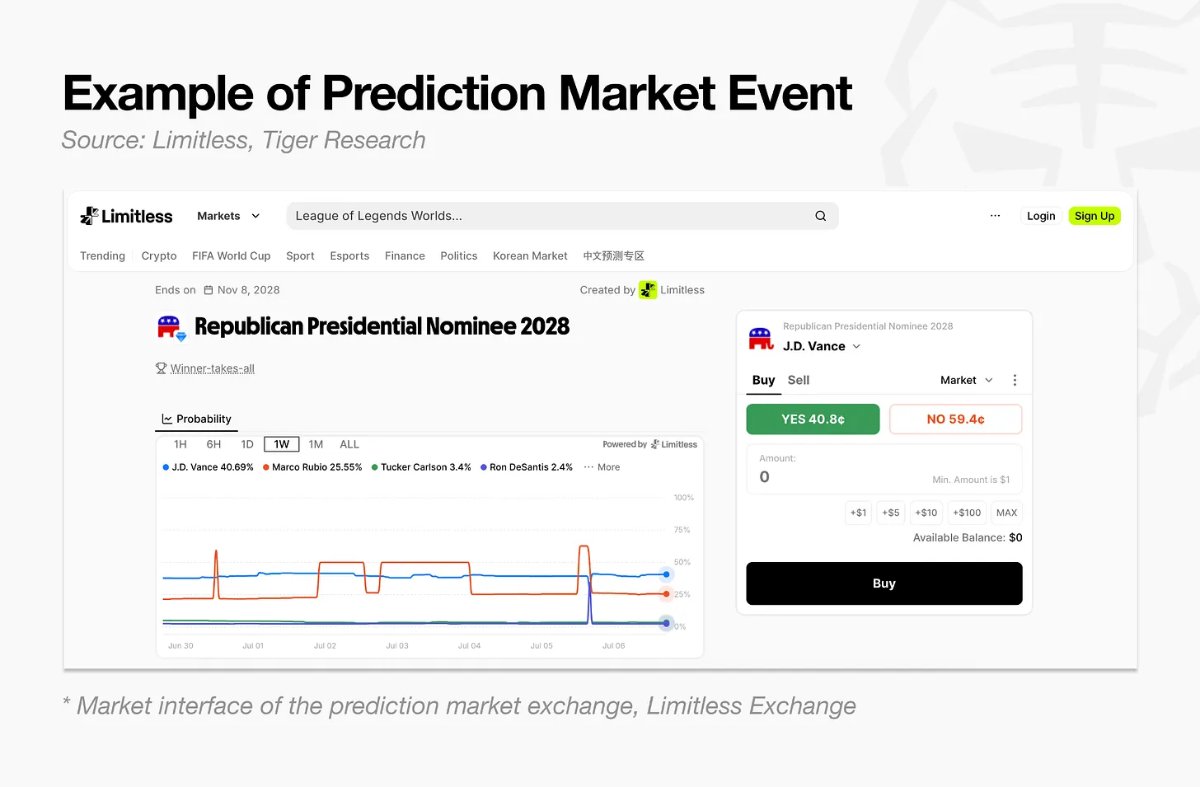

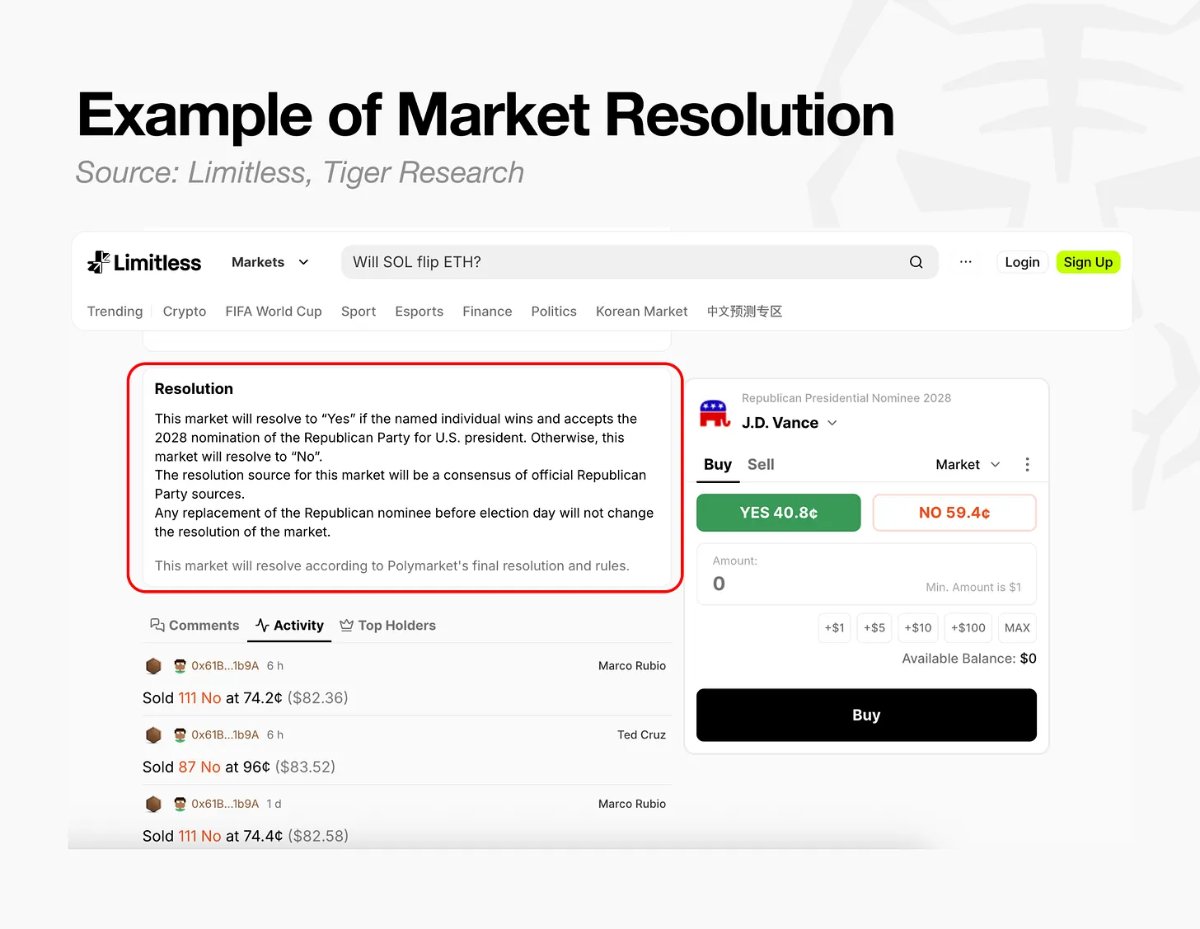

Each contract settles in a binary yes or no manner. Taking whether the 2028 Republican presidential nominee is J.D. Vance as an example: if Vance is confirmed as the nominee, contracts betting "yes" pay $1; otherwise, contracts betting "no" pay $1.

The simplest way to understand this structure is to treat $1 as 100%. The contract pays $1 (100%) if the event occurs, otherwise $0, so the intermediate trading price naturally reflects probability. A 40-cent contract represents 40% of that dollar, meaning the market believes the event occurrence probability is 40%, and the cent value can be directly read as a percentage (ignoring bid-ask spreads and transaction costs).

Prices are formed through an order book, not determined by any central party. Buy orders (e.g., buy at 39 cents) and sell orders (e.g., sell at 40 cents) accumulate at various price levels, and trades are executed where both parties match. Price (and implied probability) is generated in real-time by the capital gaming of numerous participants. Traders can also sell positions before expiration to lock in profits or stop losses, essentially exchanging their views on events for money.

Results are recorded by oracles. No matter how precise the contract price is, after the event ends, someone still needs to determine "yes" or "no", and the oracle is the mechanism responsible for this judgment.

Oracles have two ways of operating:

- Decentralized oracle: Proposers stake margin and submit proposed results; if no one challenges within a specified time, it becomes the final result. If challenged, it enters a re-proposal process, and only after further challenges does it enter voting.

- Centralized: Judgment criteria are set in advance, and after the event ends, the exchange directly applies the official result and settles the market immediately. This method completely hands over judgment power to a single exchange.

For example, on the Limitless platform, once the deadline passes, the result is finalized according to preset rules. Completed by oracle services that report real-world results to the blockchain: most markets tracking crypto prices or stocks are automatically reported via Pyth Network, while custom markets like sports or politics are manually judged by the operations team within 24 to 72 hours.

Prediction markets are essentially an information system that compresses the views of a large number of participants into a single number reflected by price, and judges whether the prediction is correct based on preset rules after the event ends.

The Evolution of Gaming and Information Finance

Prediction markets have surpassed simple betting platforms, evolving into core infrastructure of information finance—transforming future uncertainty into real-time price information. Its fundamental difference from traditional polls or expert predictions lies in the "skin in the game" mechanism, where participants are responsible for their positions with their own funds.

In traditional methods, experts have almost no reputation cost for wrong judgments, and polls cannot filter out respondents' indifference or strategic misreporting. Prediction market prices have a real cost for errors—wrong positions lose money, forcing participants to verify their beliefs with the most objective, latest information. This willingness to bear costs directly translates into market reliability.

The performance of this mechanism in actual data can be seen in multiple fields:

Accuracy of financial and monetary policy predictions: A February 2026 study by a Federal Reserve economist explained the reason. Since 2022, prediction markets' interest rate expectations before Federal Open Market Committee meetings have been statistically highly consistent with actual results, superior to Fed funds futures and Bloomberg consensus. The reason is that participants lose money immediately if wrong, thus analyzing available information more strictly and pricing accordingly.

Transparent probability estimation for politics and elections: In the June 2026 South Korean local elections, Polymarket correctly predicted 14 out of 16 major cities and provinces winners. Where exit polls could only say "too close to call", prediction markets gave real-time probabilities bet by participants with real money, which is the result of many participants comprehensively judging multiple variables, rather than simple prediction.

Response to market events and company valuations: When the stablecoin interest income cap issue arose in March 2026, prediction markets immediately priced the probability of Coinbase stock price decline at 97.6%, as a real-time risk indicator rather than post-event analysis, showing participants' sensitive response when their own funds are at risk. Academic research also reached similar conclusions: a 2015 study on internal prediction markets for companies like Google and Ford found that compared to official forecast models, prediction errors were reduced by up to 25%, indicating that when insider knowledge combines with risk capital, prediction accuracy improves.

Information asymmetry remains a limitation. In the January 2026 Venezuela case, someone used confidential information for insider trading, exposing real weaknesses. However, this attempt to distort prices was identified and prosecuted as a crime, also proving that markets aim to operate in a transparent and accountable manner.

In fields where information is widely distributed, prediction markets are precise analysis tools; in fields where information is concentrated in the hands of a few, they are monitoring mechanisms capable of identifying this concentration. Because participants' funds are truly at risk, the prices generated by these markets constitute objective information for evaluating financial asset values.

The Absence of Prediction Markets in Asian Policy Discussions

The nature and trajectory of prediction markets differ greatly due to regulatory frameworks of various countries. The US incorporated them into the regulated financial system through judicial rulings, while major Asian jurisdictions mostly still regard them as traditional gambling categories.

In the US, litigation resolved most regulatory uncertainty. The Commodity Futures Trading Commission attempted to classify Kalshi's election prediction contracts as gambling and sanction the platform, but the court ruled that election predictions are not games of chance, and regulators have no power to ban them. This ruling changed the regulatory posture, becoming a decisive catalyst for entry by traditional financial institutions including ICE, Robinhood, and CME.

In contrast, in major Asian jurisdictions, the mainstream view still equates the binary settlement structure of prediction markets with traditional gambling. The dominant regulatory perspective is gambling control and public order, rather than financial policy. Although approaches vary by country, prediction markets in the region mostly remain outside formal policy discussions, with India and Indonesia as exceptions.

This divergence in treatment ultimately boils down to whether regulators view markets as financial innovation or social control issues.

Prediction Markets at the Crossroads of Regulatory Dilemma and Institutionalization

Prediction markets have become the core of global financial and information infrastructure. A significant gap has emerged between global trends and the rigid stance of Asian regulators. In the present where technical and financial boundaries have basically disappeared, attempts to restrict new markets within old regulatory frameworks have inherent limitations. Current regulatory practices in major Asian jurisdictions have three major problems.

The first is the paradox of regulatory arbitrage.

Prediction markets operate on borderless digital networks; blocking platforms or restricting users in one country cannot eliminate underlying demand. Users will turn to unregulated offshore platforms, bearing greater risks. This leads to capital outflow from the jurisdiction, and regulators simultaneously lose market supervision rights and related taxes, weakening regional financial competitiveness in the long term.

The second is the loss of national information infrastructure sovereignty.

Prediction markets are a sophisticated information infrastructure that transforms complex social problems into precise numerical estimates, rather than simple betting venues. Recent elections in Asia show that prediction markets read public sentiment faster and more accurately than traditional polls. When excluded under the name of regulation, the data that best reflects a society's sentiment accumulates on foreign servers. The result is that foreign media and institutions understand local society more clearly than domestic analysts.

The third is the abandonment of user protection.

Users are in a blind spot, without institutional protection. Policies that simply deny markets without sufficient prior discussion only expose users to risks and push them outside the system.

The focus of discussion needs to shift thoroughly.

The question is no longer how to block this market, but how to healthily utilize this data within the formal system. This perspective shift requires specialized research, but currently relevant discussions are still very limited.

In this field, Limitless Research is filling the gap, processing prediction data from Asian markets like South Korea and Japan into information assets. More participants need to undertake the role of building a healthy data ecosystem in the future.

Regulation should not be a dam blocking water flow, but a channel guiding water flow correctly.

What Asia needs now is not stricter law enforcement, but to launch forward-looking discussions to respond to this shift. Pushing already occurring transactions into the shadows is the worst policy. Incorporating them into the formal system through constructive discussion, establishing transparent supervision mechanisms, and returning data generated in the process as national and social assets requires continuous effort.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News