Morgan Stanley Research Report Analysis: GPU Shortage to Last Until at Least 2027, Meta's Self-Built Cloud is Ironclad Proof of Shortage

TechFlow Selected TechFlow Selected

Morgan Stanley Research Report Analysis: GPU Shortage to Last Until at Least 2027, Meta's Self-Built Cloud is Ironclad Proof of Shortage

This is not a vague "long-term bullish view"; it is a supply constraint that can be pinpointed to specific years.

Written by: Rita

TechFlow Digest

Meta is developing internal cloud services to compete with Azure and AWS; the core of this competition lies not in market share, but in GPU capacity. Bloomberg's report superficially points to a cloud service war, but essentially reflects the pressure of GPU shortages across the industry. Morgan Stanley believes this is the most direct proof of the long-term GPU shortage. When companies prefer to build their own infrastructure rather than procure from third parties, the market is already in a state of extreme scarcity. Although May SIA data showed a year-over-year growth of 16.1%, lower than the expected 22%, this is more due to memory chip supply constraints rather than demand decline. The report maintains a bullish stance on NVDA and AMD, while pointing out that DRAM shortages will continue at least until the end of 2027, and the NAND shortage effect will push up industry gross margins.

Meta's Self-Build and the Truth Behind the Global GPU Shortage

Meta's move seems abrupt, but the logic is clear. If the market GPU supply were sufficient, companies would not need to undertake self-building with high costs and complexity. Morgan Stanley explicitly pointed out in the report that large cloud computing customers like Meta, Google, and Anthropic are all procuring GPUs independently and developing hyperscale data centers. This is not strategic diversification, but a forced choice made when market supply cannot meet demand. The driving factor is that GPUs are too scarce, not that demand is too weak. This stands in sharp contrast to some arguments in the market about the chip cycle peaking.

The key is that companies like Meta have extremely strong self-building capabilities; they have the lowest technical and cost thresholds. If even they are building themselves, it shows that the capacity left for foundries and SMEs in the market is negligible. The report emphasizes that although individual manufacturers perform differently, overall, the most cost-effective use of GPUs is to rent them out to others. This precisely proves that the market is in a state of supply falling short of demand. If GPUs were sufficient, companies would prioritize procuring standard products from the open market rather than building themselves at the risk of integration and maintenance costs.

During Computex, NVIDIA publicly stated that the token cost of NVIDIA chips (cost per unit of computing power) far leads competitors, and combines a longer product lifecycle and a more stable cost curve. This statement seems conventional, but against the backdrop of severe GPU shortages, cost advantages should have been overwhelmed by supply shortages. NVIDIA daring to publicly emphasize token cost indicates their confidence in long-term pricing power, and this confidence comes from clear supply constraints. Morgan Stanley believes that although AMD Helios has higher cost-performance in certain applications, NVIDIA's combination of "more computing, lower cost" remains the market's first choice. This is a strong positive for NVDA's sustained premium potential.

Memory Shortages and the Countersignals from Inventory Structure

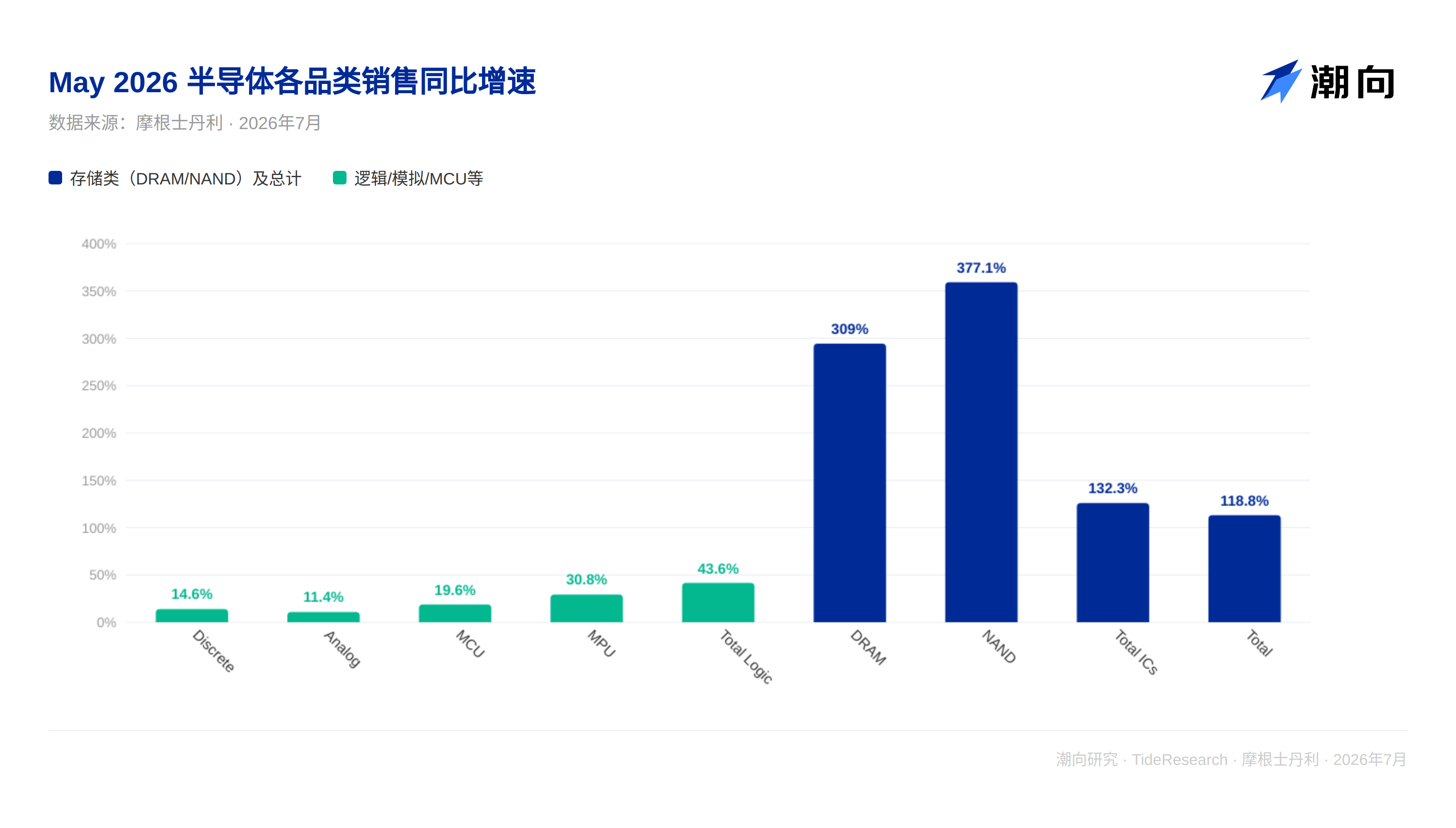

The soft performance of May SIA data is easily misread as a recession signal. Morgan Stanley broke down the performance of various categories: discrete chips fell 6.9% (1% lower than expected), analog chips fell 7.8% (2% lower than expected); these two items are indeed weak. But the key lies in memory, which is precisely the market's blind spot.

Although DRAM's year-over-year growth rate of 27.7% was lower than the expected 43%, seemingly missing expectations, the month-over-month growth in May was 54.8%, refreshing a historical high since 2001. The meaning of this number needs to be understood: DRAM monthly sales from April to May grew by 54.8%, the largest single-month increase since 2001. This is not a slow recovery, but a scramble to buy. This does not signal sufficient DRAM supply, but rather a manifestation of extremely tight inventory and purchasers scrambling to buy.

Regarding NAND, the 3-month average year-over-year growth rate stabilized at 15.5%, which is an extremely rare double-digit growth rate in the chip cycle. The price increase of 281.6% (previous months) is enough to show that the supply side holds absolute pricing power. The report further pointed out that DRAM prices have risen since the second half of the year, but the increase is far from enough to stimulate significant industry capacity expansion. This is a key contrast: prices have risen, but capacity has not kept up. Manufacturers remain doubtful about the certainty of subsequent demand, preferring to let prices rise slowly rather than daring to invest heavily in new production lines. This indicates caution about the persistence of the AI cycle, rather than pessimism about demand.

The inventory structure shows the true face of supply constraints. Morgan Stanley tracked the inventory levels of chip companies, agents, and end customers. May data shows chip company inventory at 114 days (up 2 days, but still 23 days lower than the historical median), agent inventory at 61 days (down 2 days, but still 7 days higher than the historical median). This asymmetric distribution has deep implications. Upstream inventory is pressed extremely low, indicating that the production side is strictly controlling shipments to prevent inventory accumulation. Downstream inventory is raised very high, indicating that customers are hoarding, locking in capacity even at high inventory costs. This is not a traditional inventory recession cycle, but a standoff where the supply side is under continuous pressure and the client side is continuously tight. To put it more plainly, this is a battle for capacity at the cost of expenses.

NVIDIA Cost Dominance and AMD's Window of Opportunity

Meta listed AMD Helios on the early adopter list; this is not only technical validation but also implies exquisite economic logic. The warrant issued by AMD to Meta allows exercise at a 75% discount to the stock price at the time, which is a strong incentive from an economic perspective. How aggressive is this discount? If AMD's stock price is 100 yuan, Meta can exercise at a price of 75 yuan at some point in the future. If AMD's stock price rises to 150 yuan, Meta buying at 75 yuan is equivalent to a 50% discount. This is the price AMD is willing to pay to bind Meta and ensure procurement commitments from early large customers.

Meta has sufficient motivation to deploy Helios in the early stage to exercise these high-discount warrants. From the perspective of capital operation, this is more cost-effective than directly procuring NVIDIA. The report points out that this may push up AMD's adoption rate in the AI chip market. Although it will not shake NVIDIA's absolute leading position in the short term, it provides clear incremental support for AMD's market share. More importantly, Meta's endorsement has a demonstration effect. Once Meta proves the usability of Helios in a production environment, the risk cost for other large cloud vendors to follow up will drop significantly.

However, this does not change NVIDIA's dominant position. NVIDIA's token cost advantage, software ecosystem accumulation, and customer stickiness cannot be shaken by a warrant incentive. AMD's Helios is more about getting a share of the pie against the backdrop of severe GPU shortages, rather than completely changing the market landscape.

2027 Constraints and Long-term Investment Implications

Morgan Stanley adjusted the full-year forecast, lowering the 2026 memory chip market forecast from 103% to 99%. This adjustment seems tiny, but behind it is a fine trade-off between demand and supply. The forecast for 2027 is 24% growth to 1.95 trillion, which means that after the rush buying in 2026, the industry will enter a relatively normal inventory replenishment cycle. But the key constraints remain: DRAM shortages will continue until the end of 2027 under the continuous demand of the AI cycle, while NAND will maintain high gross margins due to slow capacity release.

Why does the report dare to give such a clear time frame? Because the capacity construction cycle of memory chips is known. New DRAM wafer fabs take 3 to 4 years from planning to mass production, and NAND takes longer. When looking at May data, the report was already able to track the capacity plans of upstream manufacturers. The constraint at the end of 2027 comes from the fact that even if capacity expansion starts now, new production lines cannot release significant capacity before 2027. This is a physical constraint, not market sentiment.

The report maintains its judgment on the long-term prosperity of memory chips, believing this is a structural constraint rather than cyclical fluctuation. Structural means that even if AI investment enthusiasm declines, memory demand will remain high because the parameter count and training data volume of AI models are growing exponentially. Memory is not used to support short-term computing power competitions, but to carry long-term data accumulation.

TechFlow Perspective

The report's judgments on both GPU and memory dimensions point to the same logic: shortage rather than surplus. The market began to worry about the chip cycle falling back when seeing the soft May SIA data, which reflects typical superficial thinking. They only saw year-over-year growth lower than expected and assumed demand decline. But they ignored the counter signals of inventory structure, the one-way upward trend of prices, and customers' scramble to build themselves. These phenomena point to completely opposite conclusions.

From an investment perspective, the value of this report lies not in validating existing consensus, but in providing a clear time frame. GPU shortages will extend at least until the end of 2027, and memory shortages will structurally extend to around 2028. This is not a vague "long-term bullish", but supply constraints that can be precise to the year. The implication for target selection is clear: do not be frightened by the fluctuations of single-month data, but track those enterprises that can guarantee shipments during the long-term shortage cycle. NVDA's token pricing power, AMD's warrant binding, MU and SNDK's capacity rhythm are all core variables under this logical framework. The excess returns of the previous two years will not disappear in 2027, but will deepen further along the shape of capacity constraints.

Disclaimer

This article is a compilation and interpretation of third-party brokerage research reports by TechFlow Research. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage analysts, represent only the position of their affiliated institutions, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions need to be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News