July Price Hike Wave Sweeps Global Chip Supply Chain, Asian Stock Market Semiconductor Sector Continues Upward Trend

TechFlow Selected TechFlow Selected

July Price Hike Wave Sweeps Global Chip Supply Chain, Asian Stock Market Semiconductor Sector Continues Upward Trend

Over ten giants collectively raise prices in July; AI demand squeezes capacity across the entire industry chain.

Author: Claude, TechFlow

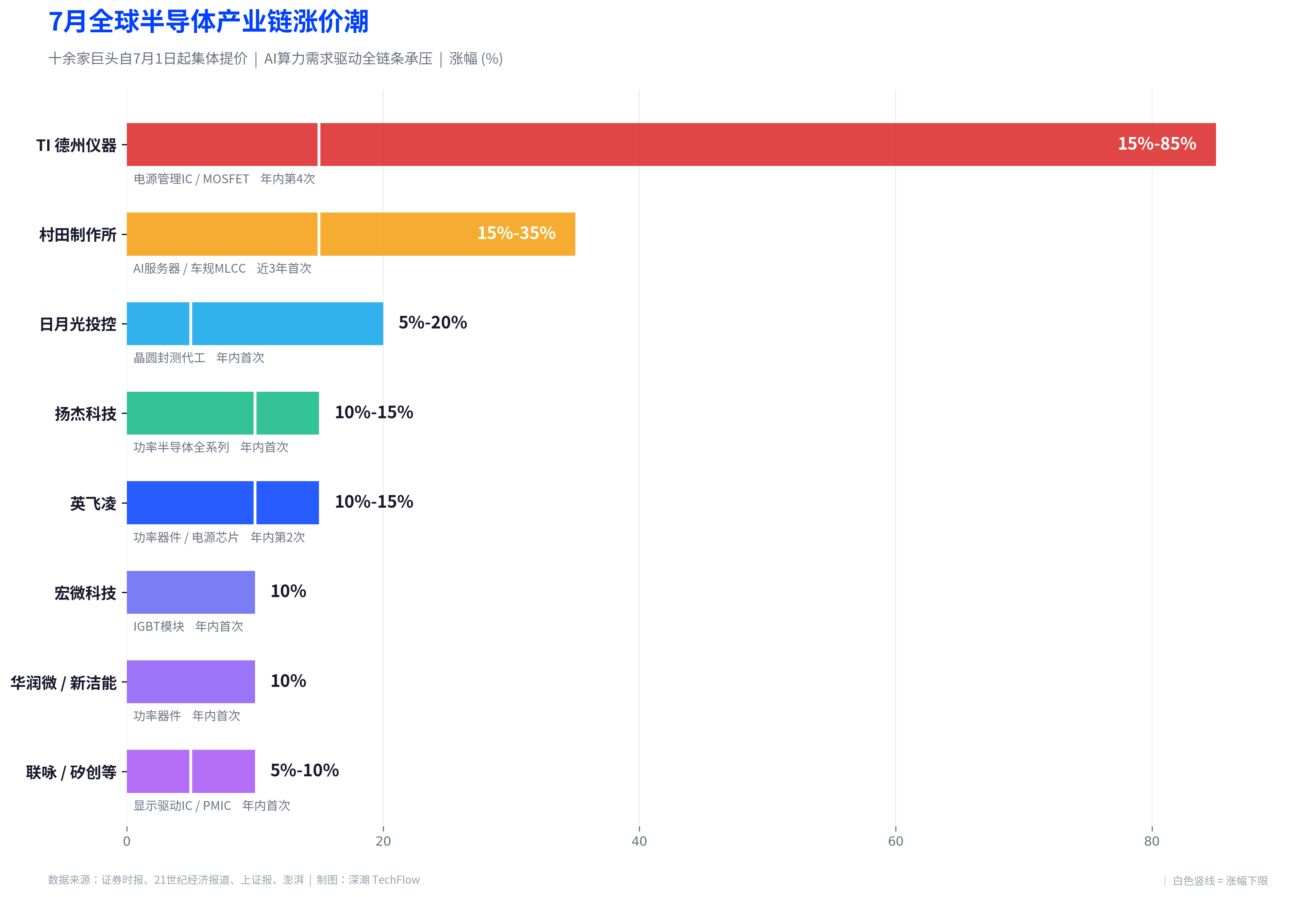

TechFlow Editor's Note: Entering July, the global semiconductor industry chain is ushering in a new round of collective price increases. More than ten giants including Murata, Infineon, and Texas Instruments announced price hikes starting from July 1, with increases up to 40%. On the same day, Samsung Group announced a 1,000 trillion won (approximately 648 billion USD) domestic investment plan for South Korea over the next decade, with chip manufacturing as the core focus. The A-share semiconductor sector continued its upward trend today, with Yinhe Microelectronics hitting the 20cm limit up.

AI computing power demand is rewriting the pricing rules of the global semiconductor industry chain.

According to reports from Securities Times, 21st Century Business Herald, and other media, starting from July 1, Infineon, Texas Instruments (TI), Murata, Yangjie Technology, and more than ten other leading semiconductor and electronic component enterprises will collectively implement a new round of price increases, covering multiple key links from upstream wafer foundry to terminal chips. At the same time, Samsung Group officially announced an industrial blueprint investing 1,000 trillion won over the next decade at the Blue House, the South Korean Presidential Office, on June 29, of which about 300 trillion won is directed towards chip manufacturing. In the A-share market, the semiconductor industry chain continued its upward trend today, with Yinhe Microelectronics hitting the 20cm limit up, and Yangjie Technology, Hongwei Technology, and others rising over 5%.

More Than Ten Giants Collectively Raise Prices in July, AI Demand Squeezes Capacity Across the Entire Industry Chain

The core driver of this round of price hike wave is not the traditional inventory cycle, but the structural squeeze of AI computing power demand on the global semiconductor supply chain.

Infineon has issued notifications to customers to increase prices for some products starting from July 1, this is the company's second price increase within 2026. According to Securities Times, Infineon CEO Jochen Hanebeck stated at the earnings conference call in early May that demand for AI data center power solutions is extremely strong. Infineon's Power and Sensor Systems division sales in the second fiscal quarter increased by 26% year-on-year to 1.26 billion euros, and the company has upgraded its 2026 fiscal year sales outlook from "moderate growth" to "significant year-on-year growth".

Texas Instruments also plans to increase quotes for core products such as power management ICs starting from July 1, this is the company's fourth price adjustment within 2026. According to China Business Journal, in Texas Instruments' previous round of price increases on April 1, core products such as power management ICs saw increases ranging from 15% to 85%. TI's first quarter data center revenue increased by about 90% year-on-year, indicating that AI demand is accelerating from GPUs to power management, server power supply systems, and high-voltage MOSFETs and other fields.

In the passive component field, the world's largest MLCC supplier Murata previously initiated comprehensive price increases for AI server and automotive-grade MLCCs, with increases between 15% and 35%. According to Shanghai Securities News, Murata occupies about 70% of the global AI server MLCC market share, and its President Norio Nakashima publicly stated in February this year that customer order volume is twice the existing capacity, "completely unable to meet".

Domestic manufacturers are following suit simultaneously. Power semiconductor leader Yangjie Technology announced a 10% to 15% price increase for all product series starting from July 1, due to continuous price increases in upstream chip wafers, bulk metals, and packaging raw materials. According to The Paper, this round of price increases almost covers all IC design enterprises in the Taiwan region of China, and multiple Taiwan IC design manufacturers such as Novatek, Sitronix, and Silergy have successively issued price increase notifications.

Bernstein pointed out in the latest tracking report that driven by the triple factors of AI server power demand squeezing capacity, upstream wafer foundries raising prices, and geopolitics pushing up raw material and energy costs, this round of price increases is not an isolated case, but a cyclical resonance across the entire industry.

Samsung's 648 Billion USD 'Largest Investment in History', Chip Manufacturing Takes Core Position

Just as the industry chain price hike wave accelerates and spreads, the world's largest memory chip manufacturer Samsung Group officially announced an investment plan creating a record in South Korean corporate history at the Blue House on June 29.

According to Cailian Press citing South Korea's "Maeil Business Newspaper", Samsung Group will invest over 1,000 trillion won (approximately 648 billion USD) in South Korea domestically over the next decade, equivalent to half of South Korea's GDP. South Korean President Lee Jae-myung hosted this "Korea Great Leap Three Major Super Projects National Report Meeting", and Samsung Electronics Vice Chairman Jun Young-hyun, SK Hynix CEO Kwak Noh-jeong, and other corporate executives attended.

The investment blueprint covers four major fields: semiconductor chips, AI data centers, energy storage batteries, and high-end display panels. According to Investing.com, Samsung plans to invest about 300 trillion won in Jeolla Province in southwestern South Korea to build new large-scale chip manufacturing factories, and will invest over 350 trillion won in AI data center projects. The site selection avoids the capital region industrial cluster, echoing the South Korean government's regional balanced development policy.

Samsung's financial strength supports this scale. According to East Money, Samsung Electronics' operating profit in the first quarter of 2026 reached 57.2 trillion won, a surge of 756% year-on-year. Institutions predict its full-year 2026 operating profit will soar to 550 trillion won, and cumulative operating profit during the 2026 to 2028 semiconductor boom cycle is expected to exceed 1,500 trillion won.

SK Hynix is also increasing investment simultaneously. The company announced this week plans to issue American Depositary Receipts (ADR) on Nasdaq on July 10, raising up to 45.45 trillion won (approximately 200.1 billion RMB), and the raised funds will be used for the Yongin Semiconductor Cluster Phase 1 wafer factory, Cheongju advanced packaging factory construction, and equipment investment. According to Yicai Global, the South Korean government announced on the same day that it will build four chip factories in the southwest, investing about 800 trillion won, and is expected to double DRAM production capacity within five years.

Global Semiconductor Market Size Sprints Towards Trillion USD, 'Structural Inflation' Replaces Cyclical Recovery

The industrial background of this round of price hike wave is that the global semiconductor market is undergoing unprecedented expansion.

According to data cited by 21st Century Business Herald, global semiconductor sales in the first quarter of 2026 reached 298.5 billion USD, a year-on-year increase of 79.2%, and the full year is expected to break through one trillion USD. World Semiconductor Trade Statistics (WSTS) latest spring forecast significantly raised the 2026 global market size to 1.51 trillion USD, a year-on-year increase of nearly 90%. SEMI report shows that global semiconductor equipment shipment amount in the first quarter of 2026 reached 36.55 billion USD, a year-on-year increase of 14%, creating a historical record for a single quarter.

Multiple industry insiders stated when interviewed by China Business Journal that the current situation is not a comprehensive super cycle driven by the comprehensive explosion of consumer electronics from 2020 to 2021, and a more accurate definition is "structural inflation led by AI". AI as the strongest demand engine has raised the cost center and resource threshold of the entire semiconductor supply chain; memory and logic chips rise due to AI, while passive components, power management ICs, etc. rise because they need to make way for AI or are affected by costs.

According to TrendForce statistics, the average 8-inch capacity utilization rate of the top ten global wafer foundry manufacturers in 2026 has rebounded to nearly 90%, a significant improvement compared to nearly 80% in 2025. Capacity tightness is also transmitting to the packaging and testing link, and packaging and testing leader ASE Technology Holding plans to increase 2026 back-end wafer packaging and testing foundry prices, with increases expected to reach 5% to 20%.

A-Share Semiconductors Continue Upward Trend, Year-to-Date ETF Gain Champion Rises Over 136%

Under the dual catalysis of the industry chain price hike wave and Samsung's massive investment plan, the A-share semiconductor sector continued its strong performance today.

According to National Business Daily, on June 29, the semiconductor industry chain continued its upward trend, with Yinhe Microelectronics hitting the 20cm limit up, Shengong Shares rising over 10%, and Hongwei Technology, Yangjie Technology, Yoke Technology, and Fulltech Micro rising over 5%. One week prior, TSMC's notification to increase wafer foundry prices had already triggered a collective rise in the semiconductor sector, and JCET Group hit the limit up three times in four days, continuing to create new historical highs.

From the perspective of ETF fund flows, semiconductors have become one of the largest thematic trades in the A-share market in 2026. According to Securities Times, among the top twenty in the full market ETF gain chart for the first four months of 2026, chip semiconductor thematic products accounted for 12, accounting for over 60%. CSI China-Korea Semiconductor ETF Huatai-PineBridge year-to-date gain reached 66.51%, leading the full market; STAR Chip Design, STAR Chip, STAR Semiconductor Equipment and other sub-sector ETFs gains during the same period all broke through 30%.

Funds continue to pour into the semiconductor direction. In the past five trading days, funds flowing into semiconductor material equipment index related ETFs exceeded 7.1 billion yuan. STAR Chip ETF Harvest circulating scale has grown from 38.6 billion yuan at the end of the first quarter of 2026 to about 45.5 billion yuan.

The risk that needs attention lies in that Goldman Sachs has warned that "a large amount of valuation dividends in the memory sector have been digested in advance", and Hong Hao from Lotus Asset Management also pointed out that memory leaders such as SK Hynix have "significantly increased sensitivity of stock prices to marginal negative news". A-share semiconductor ETF trading crowding is at a high level, and although Samsung and SK Hynix's large-scale capacity expansion plans boost sentiment in the short term, they may change the core narrative of "supply falling short of demand" in the medium term.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News