Bitget UEX Daily Report | Did Korean media hype crash storage stocks? Google added to the Dow Jones Industrial Average; Micron’s earnings report imminent

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Did Korean media hype crash storage stocks? Google added to the Dow Jones Industrial Average; Micron’s earnings report imminent

Overall, the long-term AI narrative remains unchanged. Analysts have raised the S&P 500 target to the 8,000+ range and recommend focusing on earnings season catalysts and macroeconomic data to validate valuation pressures.

I. Top News

Federal Reserve Updates: U.S. June PMI Preliminary Reading Exceeds Expectations, While Employment Indicators Weaken

- Composite PMI preliminary reading rose to 52.2; manufacturing PMI reached 55.7 (a 49-month high), but the employment sub-index fell to a six-year low.

- Services PMI rebounded modestly to 51.3; inventory purchases by businesses hit the second-highest level on record. Market impact: Data reflect underlying economic resilience but emerging labor market stress—reinforcing the Fed’s dual focus on inflation and labor conditions—and potentially influencing expectations for future policy trajectory.

Global Commodities: Hormuz Strait Reopens, Restoring Middle Eastern Crude Supply

- Following the Strait’s reopening, Middle Eastern crude accelerated deliveries into European markets, pushing North Sea Brent benchmark crude prices to a two-year low.

- Concerns over supply surplus intensified amid additional Atlantic Basin cargoes. Market impact: Oil prices faced downward pressure, underscoring how geopolitical de-escalation directly impacts energy supply-demand dynamics—short-term bearish for crude but easing broader inflationary pressures.

Macroeconomic Policy: South Korean Tax Reform Talks Trigger Stock Market Collapse; Memory Chip Rumors Intensify Sell-off

- Cross-party lawmakers in South Korea discussed including unrealized stock gains in comprehensive taxation, triggering a KOSPI circuit breaker; Samsung and SK Hynix led the decline.

- South Korean media reported SK Hynix slowing HBM4 ramp-up and shifting resources toward general-purpose DRAM, citing reduced production forecasts for NVIDIA’s next-generation Rubin platform. Market impact: Combined policy uncertainty and supply-chain rumors weighed heavily on global memory and semiconductor stocks, highlighting how regional policy shifts transmit across the global tech supply chain.

II. Market Recap

Commodities & FX Performance

- Spot Gold: ~$4,090/oz, -0.34%

- Spot Silver: ~$61/oz, -0.33%

- WTI Crude: ~$72.5/barrel, -0.79%

- Brent Crude: ~$76.4/barrel, -0.87%

- U.S. Dollar Index (DXY): 101.427, +0.05%

Drivers Analysis: The reopening of the Hormuz Strait—coupled with resumed Middle Eastern crude shipments—directly intensified supply oversupply in European markets, dragging down North Sea benchmark oil prices and pressuring overall oil valuations. The dollar index held near highs, supported by potential hawkish Fed signals and weak employment data, suppressing precious metal prices. Gold and silver softened amid strengthening dollar and volatile risk sentiment, though geopolitical easing alleviated some safe-haven demand. Institutional views hold that short-term supply-demand imbalances and macro-policy expectations will continue driving correlations—oil’s decline may further ease global inflation pressures, while precious metals lack strong near-term upside catalysts.

Cryptocurrency Performance

- BTC: ~$62,866, -2.17%

- ETH: ~$1,667, -3.8%

- Total Crypto Market Cap: ~$2.24 trillion, -1.9%

- Liquidations: $559 million total in 24h, with $493 million long liquidations

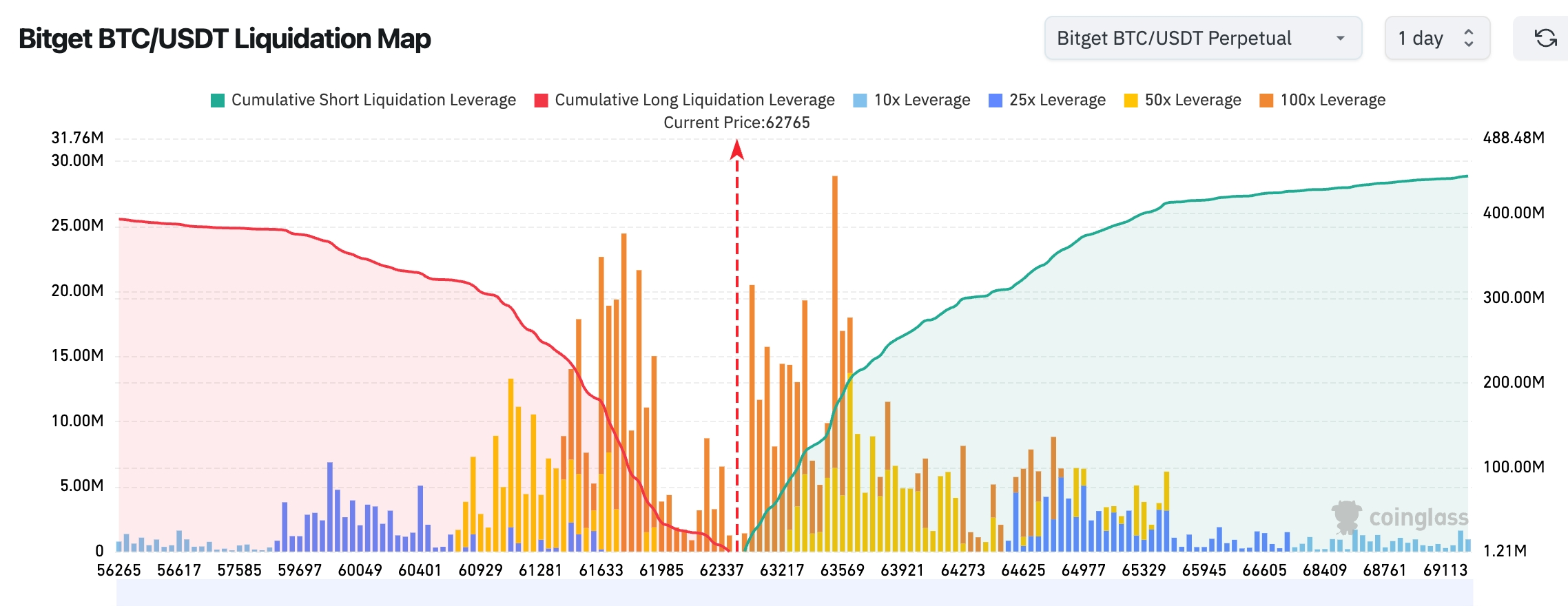

- Bitget BTC/USDT Liquidation Map: Current BTC price ~$62,765; dense long liquidation clusters sit between $61,500–$62,500—further downside could trigger concentrated long stops and amplify volatility. Strong short liquidation resistance lies between $63,500–$65,000, with peak density near $63,500—breakout above this zone may spark short squeezes and propel BTC higher.

- Spot ETF Net Inflows/Outflows: BTC spot ETFs posted $68.3 million net outflow yesterday.

Drivers Analysis: U.S. tech sector pullback spilled over into crypto markets; memory chip rumors amplified risk aversion—BTC and ETH both declined, though BTC proved relatively resilient. Leveraged liquidations were predominantly long positions, signaling stress among elevated holdings; ETFs still saw modest net inflows, reflecting institutional floor support. Macro drivers included dollar strength and geopolitical easing; technically, key supports are being tested. Consensus view holds that short-term volatility is intensifying—but long-term capital inflow trends remain intact. Investors should monitor ETF flows and macro data for guidance on risk assets.

U.S. Equity Index Performance

- Dow Jones Industrial Average (DJIA): ~51,667 points (-0.09%)

- S&P 500: ~7,365 points (-1.44%)

- NASDAQ Composite: ~25,587 points (-2.21%)

Tech Giants’ Moves

- NVDA: $200.04 (-4.13%)

- AAPL: $294.30 (-0.91%)

- MSFT: $373.94 (+1.80%)

- GOOGL: $346.13 (-0.98%)

- AMZN: $234.11 (+0.57%)

- META: $562.20 (-0.29%)

- TSLA: $381.61 (-5.79%)

Performance Summary & Drivers Analysis: Tech giants broadly under pressure; NASDAQ’s sharp pullback stemmed largely from memory chip rumors and broad-based semiconductor weakness (Philadelphia Semiconductor Index plunged). Google’s inclusion in the DJIA reflects symbolic index adjustment rather than fundamental shift; stock-specific divergence was evident—TSLA received tailwinds from specific news, while NVDA and GOOGL suffered from supply-chain concerns. AI’s long-term demand thesis remains intact, but near-term high valuations and rumors amplified volatility. Market attention now pivots to Micron’s earnings as a key catalyst.

Crypto Stock Perpetual Contracts Overview

24H Total Turnover: $23.338 billion (+49.76%)

Total Open Interest: $5.023 billion (-6.82%)

24H Total Liquidations: $49.498 million

Share: Turnover 13.02%, Open Interest 4.73%, Liquidations 8.85%

Sectoral Open Interest Breakdown (Major Sectors)

Technology: $2.606 billion

Financials: $158 million

Consumer Discretionary: $81.46 million

Industrials: $30.26 million

Biotech: $14.93 million

Trend Observation: Technology maintains overwhelming dominance in open interest—but overall open interest declined 6.82%, suggesting profit-taking or waning risk appetite amid active trading.

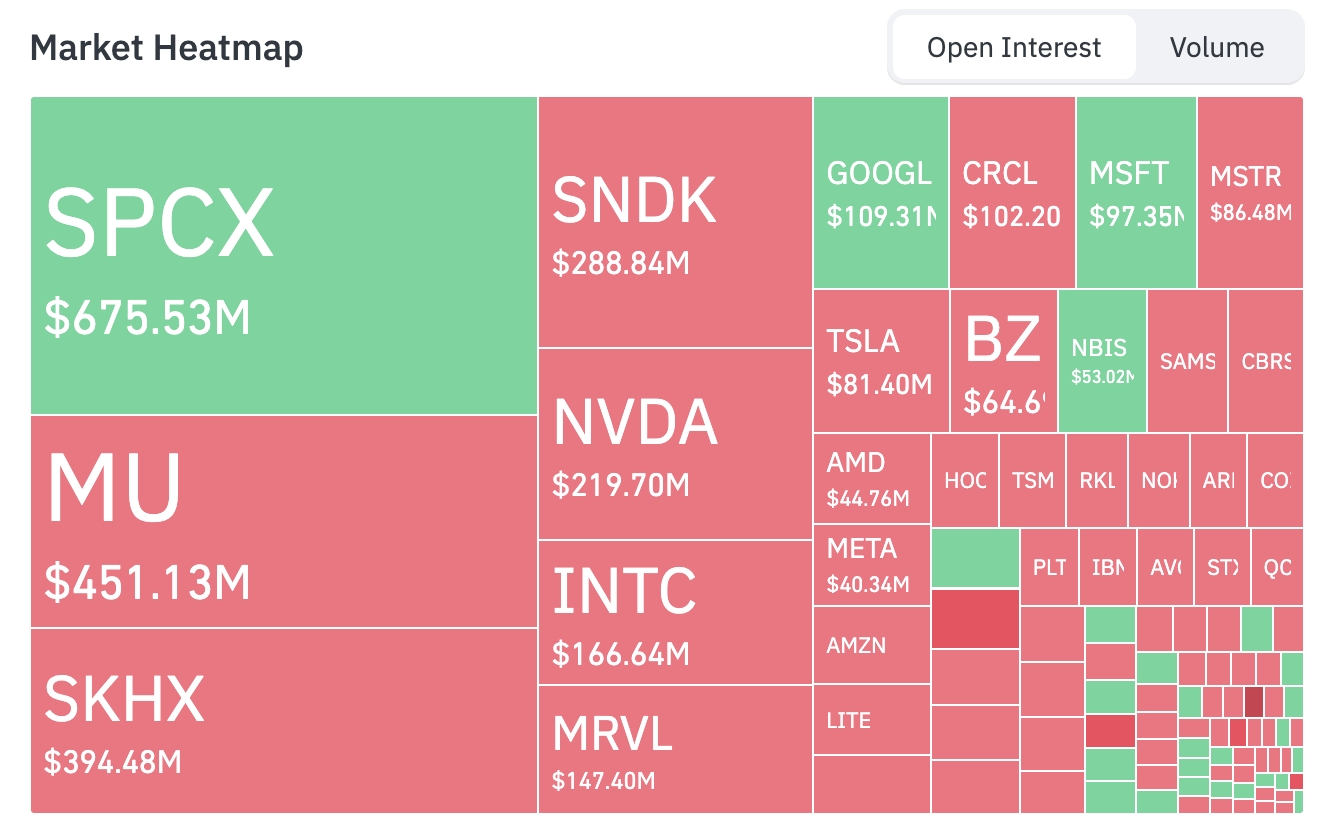

Market Heatmap (Open Interest Focus)

Top Asset Open Interest Rankings (in USD billions):

SPCX: $0.675B — Largest current open interest

MU: $0.451B

SKHX: $0.396B

SNDK: $0.289B

NVDA: $0.220B

INTC: $0.167B

MRVL: $0.147B

GOOGL: $0.109B

CRCL: $0.102B

MSFT: $0.097B

MSTR: $0.086B

TSLA: $0.081B

BZ: $0.065B

Capital flows show accumulation in SPCX, GOOGL, MSFT, and NBIS; outflows or reductions observed in MU, SKHX, SNDK, NVDA, INTC, MRVL, CRCL, and MSTR.

Sector Volatility Watch: Semiconductor/Memory Sector sharply declined (Philadelphia Semiconductor Index down ~7–8%)

- Key stocks: Micron (MU) and Western Digital (WDC) dropped over 13%; SK Hynix ADR led losses; ARM, Qualcomm, WD, Applied Materials fell 7–10%+; NVIDIA (NVDA) fell ~4%; AMD slid >5%.

- Drivers: Multiple headwinds converged to amplify market anxiety. First, cross-party South Korean lawmakers jointly proposed incorporating unrealized stock gains into comprehensive taxation—triggering a KOSPI circuit breaker and hammering heavyweight Samsung Electronics and SK Hynix—raising fears that such policy would dampen enthusiasm for high-valuation tech investments. Second, South Korean media reported SK Hynix slowing its HBM4 mass-production ramp and reallocating resources toward general-purpose DRAM due to continuously revised-down production forecasts for NVIDIA’s next-gen Rubin platform. This “rumor” quickly spread via Bloomberg and CNBC, prompting traders to question AI’s high-end memory demand outlook.

In-Depth Analysis: As the critical bottleneck resource for AI training and inference, HBM had been widely expected to sustain memory giants’ high growth and margin expansion amid tight supply. Yet signals of slowed ramp-up—combined with NVIDIA’s revised demand guidance—have triggered broad skepticism about whether AI capex peaks in late 2026 might arrive earlier—or soften altogether. This supply-chain ripple effect not only pressured memory stocks but spilled over into the entire semiconductor ecosystem, triggering widespread profit-taking in high-valuation AI hardware equities. Near term, sector valuations face clear pressure; medium term, positive guidance from Micron’s upcoming earnings (e.g., rising HBM market share or healthy inventory levels) could alleviate pessimism—but geopolitical policy uncertainty and macro interest-rate environments will continue constraining rebounds. Investors must closely track actual shipment data and major customers’ capex plans to distinguish cyclical noise from structural opportunities.

III. Deep Dive: U.S. Equities

1. Alphabet (GOOGL) – Dow Jones Inclusion Event Summary: S&P Dow Jones Indices officially announced that Alphabet Class A shares (GOOGL) will join the Dow Jones Industrial Average (DJIA), replacing longtime constituent Verizon Communications. Concurrent changes include Honeywell Aerospace entering the S&P 500 and remaining in the DJIA, and IES and Toast replacing constituents in the S&P MidCap Index. Alphabet completed a 1-for-20 stock split in 2022, significantly reducing distortion risks to the DJIA’s price-weighted methodology. Market Interpretation: Multiple institutions note this inclusion transcends technical index adjustments—it reflects a structural shift in the U.S. corporate landscape from traditional telecom to tech-giant dominance. As a price-weighted index, Alphabet’s weight in the DJIA will be lower than its market-cap-weighted influence in the S&P 500 or Nasdaq-100; passive funds tracking the DJIA are relatively small in scale, so actual rebalancing flows are expected to be modest—primarily symbolic. Still, it marks the blue-chip index’s full embrace of AI and digital economy leaders. Investment Implications: Short-term market reaction may be muted—focus instead on fund flows and sector sentiment. Long term, inclusion could lift Alphabet’s allocation appeal among traditional investors and reinforce tech’s weight in blue-chip portfolios. Consider pairing valuation expansion potential with progress in AI search and cloud business growth.

2. Cerebras Systems – Post-Earnings Drop >10% Event Summary: AI chip startup Cerebras Systems reported Q1 FY2026 revenue of $194.3 million (+94% YoY), but posted EPS loss of $0.22. Shares plunged >10% post-announcement, extending semiconductor sector weakness. Market Interpretation: Positioned as an “NVIDIA challenger,” Cerebras showcases innovation in wafer-scale engine technology—but sustained losses amid rapid growth fuel investor concerns about profitability timelines and burn rate. Compounded by SK Hynix’s HBM ramp slowdown and NVIDIA’s Rubin demand revisions, the broader AI hardware ecosystem faces near-term demand scrutiny—amplifying systemic sector-wide pullbacks. Investment Implications: AI infrastructure competition has entered a hyper-competitive phase—short-term earnings volatility is normal. Long-term believers in Cerebras’ technological moat and vertical integration may consider phased accumulation during dips—but must closely monitor gross margin improvement and large customer adoption progress to avoid excessive valuation risk.

3. SpaceX – $25 Billion Bond Issuance Event Summary: SpaceX launched its first public bond offering, targeting $25 billion across maturities ranging from 5 to 30 years. Aimed at testing fixed-income investor confidence in its ambitious roadmap—including rocket manufacturing, Starlink, and AI-related initiatives—the offering attracted nearly $90 billion in orders. Market Interpretation: Investment bankers view this as a critical bellwether for future financing deals. Despite recent tech-stock pullbacks and challenging rate environments, robust demand signals continued investor faith in Musk’s ventures—especially Starlink’s scaling and potential synergies with AI data centers. Banks aim to establish favorable market perception to facilitate future refinancing. Investment Implications: Successful issuance strengthens valuation foundations and optimizes capital structure. Investors should track potential strategic synergies with Tesla (e.g., merger discussions) and Starlink’s cash flow contribution to the broader group—suitable for long-term exposure to aerospace and emerging tech themes.

4. Micron Technology (MU) – Earnings Preview Key Focus Event Summary: Memory chip leader Micron Technology (MU) will release quarterly results after U.S. market close, drawing intense attention to its HBM and DRAM performance amid AI demand, plus inventory digestion and gross margin recovery. Sector already corrected sharply following SK Hynix’s ramp-slowing rumors. Market Interpretation: Institutions widely expect Micron’s report to serve as a direct litmus test for real-world AI capex deployment. Amid ongoing HBM supply constraints, optimistic guidance or improved inventory metrics would ease concerns about memory demand peaking; conversely, weak signals could further depress semiconductor valuations. Analysts emphasize distinguishing cyclical recovery from AI-driven structural growth. Investment Implications: Results will act as a near-term catalyst—monitor HBM market share gains and gross margin guidance closely. For investors bullish on memory cycle upturns, current pullbacks may offer strategic entry points—but remain vigilant against macro and geopolitical headwinds.

5. Microsoft (MSFT) – Wisconsin Data Center Launch Event Summary: Microsoft announced full operation of its first Wisconsin data center in Mount Pleasant, now employing nearly 550 full-time staff and committing $4.7 billion to mega-scale projects in the state through 2024–2028. Equipment went live this April—a landmark milestone in Microsoft’s AI and cloud infrastructure expansion. Market Interpretation: Institutions see this as a powerful signal of Microsoft’s heavy investment in AI infrastructure, closing the loop with Azure cloud services and OpenAI collaboration. The facility boosts compute capacity to meet enterprise AI demand—but ROI and energy cost pressures warrant monitoring during this high-capital-expenditure phase. Aligns fully with broader tech giants’ AI capex trends. Investment Implications: Long-term tailwind for cloud and AI revenue acceleration—track utilization rates and revenue conversion efficiency. As a defensive tech giant, MSFT offers relative stability amid sector volatility—ideal for core portfolio allocation.

IV. Crypto Project Updates

1. Ben Slavin, Global ETF Head at BNY Mellon (BNY), stated that asset managers are accelerating tokenized ETF initiatives—driven primarily by investor demand and “FOMO” around early blockchain finance opportunities.

2. The U.S. House of Representatives passed housing legislation 358–32, including a temporary ban on central bank digital currencies (CBDCs) lasting until 2030. The bill now heads to President Trump for signature. Earlier, the Senate passed the same housing bill containing a four-year Federal Reserve CBDC ban.

3. Viewpoint: Trump’s latest executive order may accelerate post-quantum cryptography R&D—benefiting the crypto industry.

4. CryptoQuant advised Strategy to pause Bitcoin purchases and prioritize rebuilding cash reserves. It recommends Strategy suspend buying until cash reserves and dividend coverage recover—and build a systematic timing model to avoid the market perception of “always buying at local peaks.” It also urges establishing a structured selling framework for future bull markets to lock in profits, reduce leverage, and reserve cash for downturns. Moreno stressed Strategy currently holds ~$10.6 billion in unrealized Bitcoin losses; forced sales would massively crystallize losses and harm shareholder value. The company could signal financial strength by raising dividend payouts or issuing MSTR shares.

5. SpaceX is launching its first bond offering, aiming to raise $25 billion—to test fixed-income investors’ confidence in Elon Musk’s bold vision for the company’s future.

6. The Ethereum Foundation (EF) announced completion of organizational restructuring, cutting staff by ~20% (54 employees departed) and creating five new business clusters: Protocol Layer, Access Layer, User Layer, Community Layer, and Institutional Layer.

V. Today’s Market Calendar

Upcoming Data Releases Schedule

Key Events Preview

June 24 (Wednesday)

- U.S. Economic Data: May New Home Sales, Leading Indicators, etc.

- U.S. Earnings: Micron Technology (MU) reports after market close (memory chip leader—critical validation of AI server HBM demand); Trip.com Group (TCOM), etc. ★★★★

- Other Highlights: NVIDIA (NVDA) Annual Shareholders Meeting (9:00 AM PT)—focused on Blackwell and Vera architecture capacity ramp and AI infrastructure outlook.

June 25 (Thursday)

- U.S. Economic Data: May PCE Price Index (Fed’s preferred inflation gauge; core PCE forecast: +0.3% MoM); Q1 GDP Final Estimate (expected unchanged at 1.6%); Durable Goods Orders, Initial Jobless Claims, etc. (data-heavy day). ★★★★

- U.S. Earnings: BlackBerry (BB) reports before market open.

June 26 (Friday)

- U.S. Economic Data: University of Michigan Consumer Sentiment Final Reading; Fed official speeches (Williams, Kashkari, etc.).

Institutional Views: Prominent investment bank analysts note that although yesterday’s NASDAQ decline reflected semiconductor weakness, the DJIA held relatively firm—indicating non-tech blue-chip resilience. U.S.-Iran tensions easing supports energy stability; oil prices dip short term but long-term demand persists. Crypto markets fluctuate with risk assets, with ETF inflows providing modest cushioning. Overall, AI’s long-term narrative remains unshaken—analysts raised S&P 500 targets to the 8,000+ range, recommending focus on earnings season catalysts and macro data to validate valuation pressures. High-valuation sectors face heightened near-term volatility—but institutions still favor structural opportunities in tech and crypto.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication—not intended as investment advice. Data herein may contain unavoidable discrepancies—please rely on real-time market data for decision-making.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News