Bankless Co-Founder Hoffman on Why He Sold His ETH

TechFlow Selected TechFlow Selected

Bankless Co-Founder Hoffman on Why He Sold His ETH

Not because I am bearish on ETH, but because the argument that “ETH is money” has become outdated.

Author: David Hoffman

Translated by TechFlow

If you missed last week’s news: I sold my Ethereum.

For someone whose career, community, identity, and business are all built around Ethereum, this decision was not easy.

The choice to sell demands a far more thorough explanation than a few scattered tweets.

It’s best to read this article from Bankless.com.

However, if you prefer the less polished reading experience of native X posts, here’s the full text.

tl;dr

The “ETH is money” thesis hasn’t failed… it’s been validated. Ethereum has reached its fair price. I don’t expect ETH’s valuation as an asset to be meaningfully reassessed—neither upward nor downward.

PS: I’m extremely bullish on Ethereum. I expect the Ethereum network to thrive spectacularly in the future. But I believe only a small fraction of Ethereum’s success will accrue to the Ethereum token (ETH) price.

Here’s the full article:

ETH-as-money was always a long shot

Money is a coordination game—and coordination is hard.

The Ethereum project itself comprises a series of coordination challenges across multiple layers, and the “ETH is money” thesis requires all of them to succeed—and succeed confidently.

ETH can only become money when every layer of Ethereum’s techno-social stack outperforms its competitors.

Given Ethereum’s ambitious scope, achieving its most successful version has always been a formidable challenge. Despite shortcomings, the Ethereum project has achieved remarkable milestones—and its current market cap is well deserved.

Yet the window of opportunity… the hope that Ethereum would be “reassessed” by the market… appears to be closing.

Ethereum is money, in a sense—but not the perfect money we collectively aspire to.

Ethereum is a coordination game

Turing-complete blockchains are such a powerful concept that Ethereum’s maximum potential is nothing less than the entire crypto space—encompassing everything.

The only obstacle to Ethereum achieving 100% dominance across all domains is coordination.

Ethereum’s leadership must be sufficiently decentralized, governance must operate via “rough consensus,” and credible neutrality must be established—to maximize adoption.

Ethereum’s leadership must respond dynamically to market forces and operate like a startup, constantly under threat of obsolescence.

Ethereum L2s must be able to operate independently and make their own market choices—yet remain economically tethered to, and constrained by, the broader Ethereum economy and brand.

The Ethereum roadmap must be executed in a specific sequence to sustain momentum and market dominance—effectively suppressing competition and maximizing confidence in both Ethereum and ETH.

Critical technologies must be researched and deployed rapidly enough to demonstrate Ethereum’s utility externally and maintain its competitive edge.

The “ETH is money” thesis hinges on creating a revolutionary, powerful financial asset—one so uniquely suited as a global store of value that it attracts even the indifferent. The Ethereum brand and ETH’s strength must be compelling enough to make Baby Boomers feel not just safe, but compelled—by Ethereum’s dominant position—to allocate ETH as a core holding in their retirement portfolios.

To achieve “ETH is money,” every upstream component must function at peak efficiency.

Ethereum is not Bitcoin—it chose the harder path. Bitcoin chose to strip all information off its blockchain to elevate itself.

Ethereum chose to add *everything* to its blockchain—to maximize utilization of its blockspace. Only by doing this better than any competitor, and faster, can Ethereum attain global monetary status.

We’ve made real progress—and Ethereum has reached its maximum plausible market-cap share.

Alas, the optimal time to play this game may already have passed.

The environment may never permit it

Looking back over the years, I see Ethereum had to overcome numerous environmental hurdles.

Top-tier assets are inextricably linked to revenue

Though valuing smart-contract L1s by fees and revenue remains difficult… fees and revenue are clearly how such assets build pricing power.

By 2026, we’ll have abundant data proving tight correlations among: L1 activity, L1 fees, and L1 native-asset price appreciation.

- In 2021, ETH dominated—when its L1 revenue market share peaked.

- In 2024, SOL saw uniquely strong growth in L1 revenue market share relative to the rest of the industry—securing its dominance.

- In 2026, NEAR will undergo price re-rating alongside fundamental growth in both L1 revenue and NEAR consumption.

You can also look at assets like BNB and TRX—they’re arguably the highest cumulative revenue generators in history. Their price charts resemble what I’d expect for ETH—if ETH could sustain dominance in the L1 fee market longer than just 2022.

The “strong crypto” version didn’t work

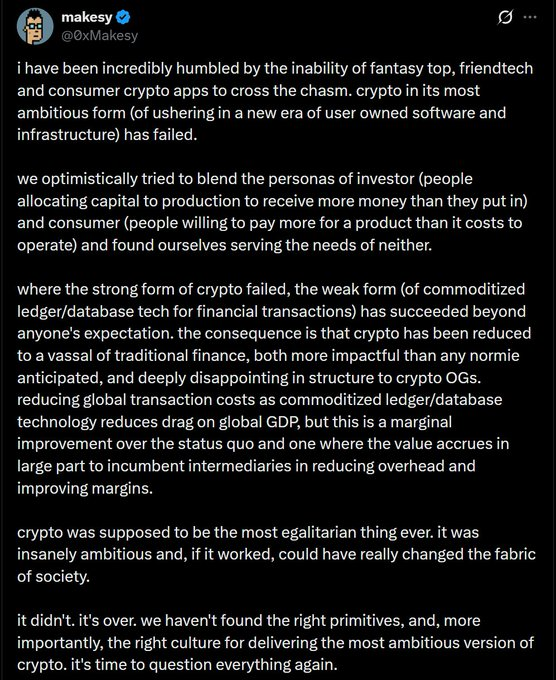

@0xMakesy put it well:

Ethereum represents the “strong crypto” version—where crypto itself is the end goal, self-sustaining and self-perpetuating. DeFi, NFTs, DAOs—we’re rebels building an alternative financial system, created by the people, for the people, turning imagination into money.

There’s also a “weaker” version: efficient ledger infrastructure for financial institutions’ back ends. This weaker version fuels the stronger one—converting demand for internet-native ledgers into internal capital flows: toward crypto, toward Ethereum, ultimately toward ETH.

Perhaps, had Ethereum executed more sharply, moved faster, operated more efficiently—and had crypto attracted fewer scammers and extractors—the industry could have earned the influence and respect it always deserved. But crypto enjoyed genuinely positive public perception for only a brief window: late 2020 through early 2022. Otherwise, crypto’s reputation has remained tied to scams, fraud, get-rich-quick schemes, and irrelevance to ordinary people.

ETH is money dependent on “strong crypto”

Ethereum’s moment to shine as network money arrived precisely when everyone was forced online. The world discovered crypto—and for that fleeting window, it went viral.

Money is a coordination game—a currency’s value rests on collective belief. In 2021, the public broadly believed in Ethereum (ETH): it was cool, disruptive, and popular. Bitcoin shared those traits—and after 2021, held onto them better than Ethereum did.

This raises an unsettling possibility: “strong crypto” may never have reached a stable equilibrium. The pandemic distorted monetary systems abnormally—and Ethereum’s monetary status may have ridden that distortion. If so, Ethereum’s role as money has always depended on the “strong crypto” ecosystem performing better than reality warranted.

Ethereum’s utility also enables other currencies.

Is Bitcoin money? Is the dollar money? Is gold money? It doesn’t matter—any currency gets tokenized on Ethereum.

In 2020, Nick Carter debated “banking the unbanked.”

Stablecoins likely attach to Ethereum—not as native tokens, but as applications. Back then, Ethereum’s stablecoin total stood at $3 billion. Today it’s $163 billion—up 54x.

Ethereum’s utility expands the monetary network to encompass all forms of money—precisely why the U.S. embraces crypto for stablecoins. Ethereum helps sustain dollar hegemony—and leveraging this fact is explicit U.S. policy.

The positive spillover Ethereum clearly delivers far more value than the U.S. government sees in Ethereum’s stablecoin ecosystem.

Ethereum is a giver—not a taker

At its core, Ethereum is a giver—not a taker.

It provides the world’s most secure blockspace to L2s—at cost.

It tokenizes global assets—at cost.

It secures billions of dollars in DeFi—at cost.

No transaction on Ethereum charges any fee.

This is the nature of open-source software—and Ethereum’s source of strength. Ethereum delivers all its immensely valuable services to the world at cost.

Ethereum is noble. Ethereum is good.

Ethereum is the world’s most successful nonprofit organization.

Ethereum naturally achieves massive adoption. It is now—and will likely remain—the most influential open-source software project in human history. “Nonprofit protocol” is one of its core features.

This is why Ethereum’s path to becoming money depends entirely on sustaining extraordinary market dominance.

Ultimately, as blockspace commoditizes, fees fall to zero. As long as Ethereum—not a competitor—drives that commoditization, Ethereum retains its margins and dominance.

Ultimately, “protocol bloat” theory gives way to “application bloat” theory—and applications capture the remaining profit. As long as those applications run on Ethereum—not a competitor—that’s fine for Ethereum.

“ETH is money” clashes with “Ethereum is a giver, not a taker.” Ethereum’s architecture is designed to feed all resources back into the ecosystem—keeping only the minimal resources needed to sustain the network.

Architecturally, Ethereum does not prioritize ETH—not as a flaw, but as a feature. ETH becomes money only if Ethereum wins a game it was never designed to play.

This approach might still work—if Ethereum sustains astonishing market dominance.

The “Ethereum is money” thesis raises many questions about Ethereum.

“ETH is money” requires everything about Ethereum to go right. Its margin for error is far smaller than I initially assumed. Ethereum’s strong momentum in 2021–2022 made “ETH is money” seem inevitable.

Hindsight reveals Solana’s 2021 rise—and rising anti-Ethereum sentiment—as the first major sign that Ethereum and ETH’s coordination game wasn’t proceeding as planned.

European financial groups need decentralization—and space for alternative power structures. But they also need startup-like urgency and responsiveness to market forces—under constant threat of obsolescence.

L2 teams need autonomy—but must also operate within Ethereum and ETH’s broader brand framework. Technical synchronization between Ethereum and its L2 teams needs faster execution.

Smart-contract chain value ties to fees. To escape that model, Ethereum must rewrite the rules—with overwhelming success.

The “Ethereum is money” thesis hasn’t failed

It just hasn’t fully realized its potential.

Ethereum made a noble choice—opting for the hardest, most ambitious, purest vision for its future.

It scored incredible wins—but also suffered setbacks.

Ethereum’s market cap has reached its fair level.

I’m extremely bullish on the Ethereum network and its ecosystem—its architecture is explicitly designed to maximize success for its applications, L2 services, and broader ecosystem. The “big app” thesis means Ethereum apps capture all fees; the rollup-centric roadmap means L2 services capture 97% of profits.

As for ETH the asset—I struggle to imagine its structural valuation shifting meaningfully in either direction—up or down.

So I sold my ETH not because I’m bearish on ETH—but because I believe the “ETH is money” thesis is outdated, and I want to allocate my capital toward other opportunities I see emerging in the market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News