Global Long-Dated Bonds Break Down: The Fiscal Illusion of the Low-Interest-Rate Era Is Collapsing

TechFlow Selected TechFlow Selected

Global Long-Dated Bonds Break Down: The Fiscal Illusion of the Low-Interest-Rate Era Is Collapsing

The “low-interest-rate rollover model” that has supported financing in developed countries over the past decade or so is beginning to show cracks.

Author: Claude, TechFlow

TechFlow Introduction: Long-dated bonds in developed economies are collectively collapsing. Markets are no longer repricing fiscal surprises in individual countries—but rather confronting the reality of persistently high debt, large deficits, and higher interest rates coexisting over the long term. As debt growth continues to outpace economic growth, energy shocks reignite inflation, and central banks’ room to cut rates shrinks, the “low-rate rollover model” that has underpinned financing in developed economies for over a decade is beginning to crack.

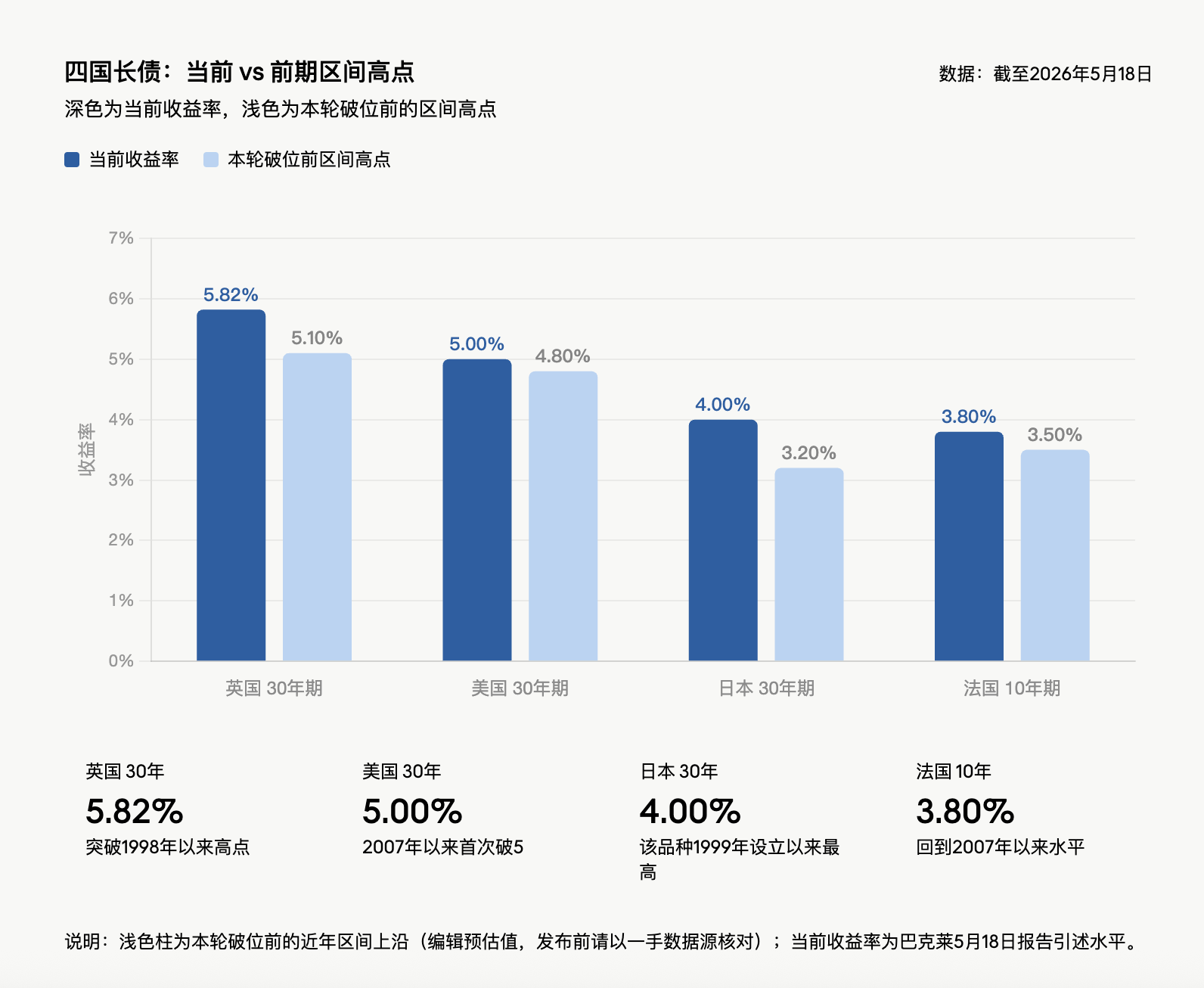

Over the past week, the UK’s 30-year gilt yield surged to 5.82%, the highest since 1998; Japan’s 30-year JGB yield hit 4%, the highest since the series’ inception in 1999; the US 30-year Treasury yield breached 5% for the first time since 2007; and France’s 10-year OAT yield climbed to 3.8%, also reaching its highest level since 2007. This sell-off has weighed on global equities, prompting G7 finance ministers to dedicate this week’s meeting specifically to discussing the current bond selloff.

In a report dated May 18, Ajay Rajadhyaksha, Head of Fixed Income, FX & Commodities Research at Barclays, wrote: “Long-dated bonds weren’t just sold off last week—they’ve broken out of their ranges across the board.” His core assessment is that debt growth is outpacing economic growth, the inflation outlook has deteriorated, and political will for fiscal reform remains weak—meaning even after the recent decline in long-dated bond prices, there is insufficient justification to extend duration.

Priya Misra, Portfolio Manager at J.P. Morgan Asset Management, issued a similar warning: “Long-end rates are rising synchronously across the globe, reinforcing each other—and market narratives now increasingly incorporate expectations of further Fed hikes.”

Synchronized Breakdown Across Multiple Bond Markets: The Collective Unmasking of the “Fiscal Ponzi Scheme”

A single-country bond market selloff can usually be attributed to domestic inflation, fiscal conditions, politics, or central bank communication. But this time, the UK, Japan, the US, and France have all broken down nearly simultaneously—indicating markets are pricing in risks far beyond local factors.

The common denominator is clear: major advanced economies generally carry debt-to-GDP ratios above 100%, while fiscal deficits remain unabsorbed by nominal GDP growth. The US deficit stands at roughly $2 trillion—or 6.5% of GDP—while nominal growth hovers around 4.5–5%; France’s nominal GDP growth for the quarter ending March 2026 was just 2.2%, yet its deficit is approximately 5%; the UK’s deficit exceeds 4%.

This is precisely the core contradiction underlying the “fiscal Ponzi scheme”: governments rely continuously on new debt issuance and refinancing to sustain spending, yet debt expansion outpaces economic growth—and interest costs are rising again. So long as this combination persists, long-dated bonds must offer higher yields to attract buyers.

New spending pressures are mounting further. Last year, NATO agreed in The Hague to raise defense spending targets to 5% of GDP by 2035; European defense spending grew double-digit percentage-wise last year—and may sustain such growth for a decade; the US government has requested $1.5 trillion in defense appropriations for the next fiscal year. None of these expenditures are offset by corresponding cuts.

Hormuz Strait Blockade Ignites Oil-Price Shock and Reignites Inflation

Fiscal and deficit vulnerabilities were already fragile—energy price shocks have further constrained policymakers’ maneuvering space. The Hormuz Strait blockade served as the immediate trigger for this bond-market turmoil. As the world’s most critical oil shipping route faces disruption, oil prices continue climbing—and inflation expectations are reigniting.

Barclays’ base-case assumption is that Brent crude will average $100 per barrel in 2026—a 50% increase over its 2025 average. This directly worsens the inflation outlook, compresses central banks’ scope to cut rates, and could even force them to hike. Higher rates mean rising interest expenses on existing debt—and rising interest expenses make deficit reduction even harder. It functions like a fiscal ratchet: each turn reduces policy flexibility and raises the compensation demanded by bond investors.

Priya Misra, Managing Director at J.P. Morgan, stated bluntly: “Unless the Strait reopens, the entire rate range has shifted upward.”

Looking at short-end data, the US 2-year yield briefly spiked to 4.09%, the highest since February 2025; the 10-year yield stood at 4.58%, near its highest level in a year; overall, US Treasuries have posted negative returns year-to-date—whereas they had risen nearly 2% by late February.

Inflation Narrative Dominates Markets; Term Premiums Undergoing Repricing

Karen Manna, Fixed Income Strategist and Portfolio Manager at Federated Hermes, assesses: “We’re witnessing a world genuinely responding to a new wave of inflation.”

Kevin Flanagan, Head of Investment Strategy at WisdomTree, expects the next CPI report to show annual inflation reaching 4%—the highest since 2023. He directly articulates the market logic: “The inflation narrative is dominating markets, and bond investors now demand higher term premiums to hold newly issued Treasuries.”

Last week’s Treasury auctions confirmed this repricing: the 30-year auction yielded 5%, the highest since 2007—but demand was tepid; investor demand for both the 3-year and 10-year auctions was similarly lukewarm. Even though long-end yields have already risen to year-to-date highs, that alone does not constitute a compelling reason to lengthen duration.

Fed Policy Path Fully Reversed: Market Bets Shift from Two Cuts to March Hike

The inflation storm is reshaping market expectations for Fed policy. Incoming Fed Chair Kevin Warsh confronts an environment starkly different from the “dovish path” envisioned by markets earlier this year.

Traders now view a March 2027 rate hike as highly probable; odds of a December 2027 hike stand at roughly 75%. By contrast, at the end of February, markets still expected two rate cuts in 2026. US Treasury yields have risen broadly by about 50 basis points—or more—since late February.

Official commentary is further entrenching hawkish pricing. Chicago Fed President Austan Goolsbee said last week that broad-based price pressures could even signal overheating; Fed Governor Michael Barr labeled inflation the economy’s “overwhelming” risk. This Wednesday’s release of the Fed’s April meeting minutes will be closely watched for signs of how much support dissenting votes received among officials.

The latest J.P. Morgan US Treasury Investor Survey shows short positions in Treasuries have reached their highest level in 13 weeks—signaling markedly heightened bets on further bond-market declines.

Japan’s Low-Rate System Undergoing Fundamental Repricing

Japan’s 30-year JGB yield hitting 4% may seem unremarkable by US or UK standards—but carries profound implications for Japan. For the past two decades, Japan’s long-term rates hovered near zero, and pension funds, insurers, and regional banks built their balance sheets around this environment.

The Bank of Japan’s current policy rate stands at 0.75%. At its April meeting, three of nine policymakers dissented from the prevailing stance; market pricing implies a 77% chance of a June hike. Even if the BOJ lifts its policy rate to 1%, real rates would remain meaningfully negative.

The rise in Japan’s long-end yields can be interpreted as monetary normalization: deflation has ended, real wages are growing, and the economy is returning to a more typical state. Yet the problem lies in the scale of debt: an economy with debt exceeding twice GDP cannot expect normalization to proceed gently. A 4% 30-year JGB yield isn’t merely a shift in a number—it signals a comprehensive repricing of Japan’s entire low-rate financial system.

UK and France: Political Structures Make Deficit Reduction Nearly Impossible

The UK’s Labour government holds a working majority of over 150 seats in the 650-seat Parliament—giving it theoretical fiscal flexibility. Yet last summer, even a £1.4 billion saving tied solely to winter fuel subsidies triggered backlash within the Labour parliamentary party.

Political pressure is intensifying further. Ninety-seven Labour MPs have called on the Prime Minister to resign—or at least announce a departure timeline; leading challenger Andy Burnham once claimed fiscal policy shouldn’t bow to bond markets—though he later clarified he wouldn’t entirely disregard investor sentiment. The UK has cycled through four prime ministers and five chancellors over the past four years. Bond-market pricing suggests the Bank of England retains over 60 bps of hiking room by year-end—even though Governor Bailey may prefer to wait and see.

France’s fiscal challenges are less headline-grabbing than the UK’s—but equally thorny. France has installed five prime ministers in under three years. The current government has survived two no-confidence votes to push through a budget targeting a 5% deficit-to-GDP ratio. The 2023 reform raising the retirement age to 64 is now under attack—even though 64 remains below the norm across most Western economies. France’s deficit already significantly exceeds nominal GDP growth; voters would punish austerity attempts harshly, and constitutional arrangements make it easier for Parliament to block spending cuts. Everyone knows the deficit must fall—but no one wants to bear the political cost of making it happen.

US Buyer Base Is Changing: Foreign Central Banks Shift to Gold; Private Investors Demand Higher Prices

The US 30-year Treasury yield breaking above 5% for the first time since 2007 stems directly from rising inflation, fiscal expansion, and elevated deficits—none of which are novel. What’s deeper is the changing marginal buyer.

The US federal deficit stands at roughly $2 trillion. The Congressional Budget Office (CBO) projects publicly held federal debt as a share of GDP will climb from over 100% today to 120% by 2036. Yet this forecast may still be overly optimistic. One key variable is tariff revenue: the US effective tariff rate has fallen from a peak of 12% to 7–8%, well below the CBO’s assumed 15%. Even if tariffs ultimately rise to 10%, tariff revenues over the next decade would amount to only ~60% of the $3 trillion deficit-reduction figure assumed in the CBO’s baseline. Assumptions on defense spending and interest costs may also prove too low.

The dollar’s reserve-currency status remains a structural advantage for the US—allowing it to borrow at rates unavailable to peer debt issuers. But that doesn’t make a 6.5% deficit sustainable. Foreign central banks were historically stable buyers of long-duration assets—but after Western nations froze Russia’s foreign reserves, central-bank allocations have pivoted toward gold. Last year, gold’s share of central-bank reserves surpassed that of US Treasuries. Japan—the largest foreign holder of US Treasuries—now finds its domestic market yields more attractive. The Fed remains in quantitative tightening mode. The buyers stepping in to absorb long-dated supply are private investors who are more price-sensitive and demand higher term premiums.

The Fed Is Not the “Fuse” for Long-Dated Bonds

The US Treasury Department has reduced long-dated issuance somewhat over recent years—and may continue adjusting its issuance structure going forward. But such measures only ease supply pressure—they cannot reverse the underlying fiscal and inflation trends.

Some market participants speculate whether the Fed might be forced to restart large-scale asset purchases to prevent further long-end yield increases. Yet Warsh’s prior comments on the Fed’s balance sheet—“the bloated balance sheet can be substantially reduced”—are hardly the language signaling preparation for US-style yield curve control.

Facing persistent selloffs, some investors are choosing to stand aside. WisdomTree analyst Kevin Flanagan says he’s maintaining exposure to floating-rate notes and keeping interest-rate exposure low: “Better to buy late than buy early.” He views the 10-year yield’s 4.5% level as “more of a psychological threshold”; should Middle East tensions escalate again and lift oil prices further, yields could retest last year’s high of 4.62%. Hank Smith, Head of Investment Strategy at Haverford Trust, takes an even more cautious stance: whether the rise in consumer and producer prices is transitory—or “will persist into 2027”—remains an open question.

The forces driving the selloff—deteriorating fiscal conditions, rising defense spending, sticky inflation, and constrained central banks—are not set to vanish within a week or two. Unless economic data clearly weaken—or credible shifts in fiscal trajectory emerge—long-dated bonds in developed economies remain priced against a single, overarching issue: the low-rate financing model of the high-debt era is undergoing fundamental market repricing.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News