Clarity Act Outlook: No Yield, No Payment

TechFlow Selected TechFlow Selected

Clarity Act Outlook: No Yield, No Payment

Stablecoin yield generation and liquidity recycling.

Author: Zuo Ye

The Clarity Act is progressing smoothly and may bring multiple benefits for stablecoins, tokenization, and DeFi development by mid-year. However, the prohibition on passive yield generation for stablecoins casts uncertainty over on-chain prospects.

This concern is not unfounded. From ETFs and DATs to Wall Street’s RWA initiatives, all are vying for control over crypto pricing. Compliance often means accepting preexisting frameworks—stability, in name, extinguishes grassroots innovation.

ETFs sacrifice BTCFi; DATs trigger systemic crises; RWAs reject existing public blockchains.

On the surface, the Clarity Act shrinks arbitrage opportunities for offshore USD stablecoins like $USDT—but in reality, by splitting and recombining payment and yield functions, the U.S. is experimenting with a new USD circulation model beyond gold, oil, and credit.

The “payment stablecoin” narrative is essentially over; the era of “yield-bearing stablecoins” is about to begin.

Three Sides Encircled, One Side Left Open: Payment Stablecoins

Setting my heart on money learning pleasure more than Thee.

A lingering question remains: How exactly does the GENIUS Act make the “payment stablecoin” narrative a reality?

This doubt has intensified as Wall Street giants position themselves for tokenization ahead of the GENIUS Act’s passage. Yes—you read that right: they’re building tokenization infrastructure precisely to enable yield-bearing stablecoins.

- On May 8, BlackRock announced plans—beyond BUILD—to launch two new TMMFs (tokenized money market funds): BSTBL and BRSRV.

- On May 13, JPMorgan launched its second TMMF, JLTXX, alongside MONY.

Moreover, BlackRock explicitly stated its new products aim to meet growing demand from stablecoin issuers, while JPMorgan emphasized compliance with relevant GENIUS Act requirements.

A close reading of the bill reveals it indeed expands language around tokenization, permitting tokenized U.S. Treasuries and USD as reserve assets for stablecoin issuance.

Yet this still doesn’t clarify the relationship among stablecoins, tokenization, and payments—we must dig deeper.

Under the GENIUS Act, stablecoin issuer licensing falls under the OCC’s federal charter bank framework. Such banks cannot accept deposits and must hold full reserves—preventing them from encroaching on commercial banks’ credit businesses.

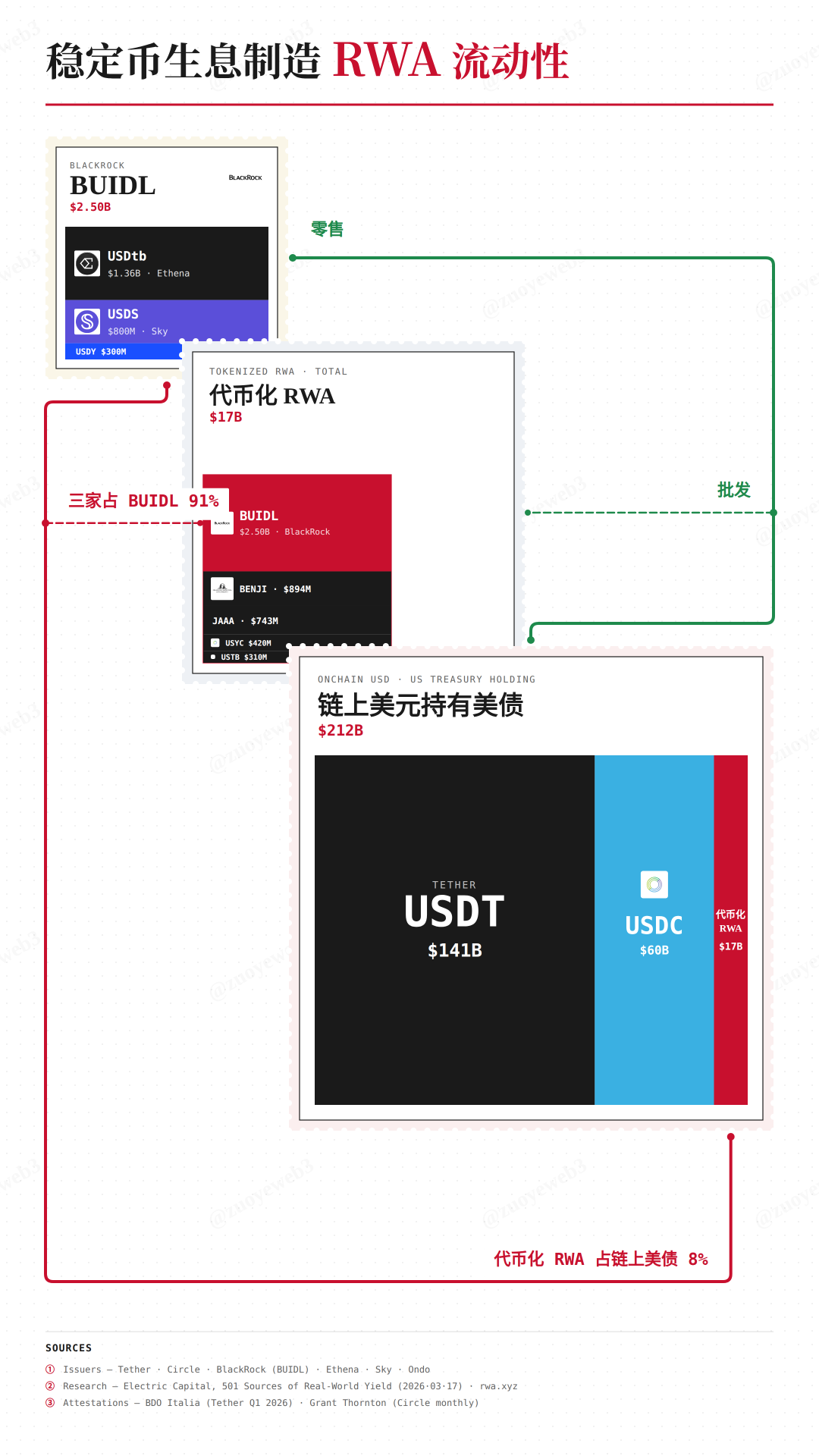

In this context, policy creates market demand: stablecoin issuers either build their own reserves (e.g., USDT and USDC buying U.S. Treasuries at volumes exceeding many sovereign nations), or directly purchase RWAs like TMMFs—a critical advantage for yield-dependent stablecoins such as USDS/sUSDS.

- Eliminates cumbersome Treasury subscription/redemption processes;

- On-chain yield distribution and real-time interest accrual better match user expectations.

According to @ElectricCapital data, 98% of BlackRock’s BUIDL shares were purchased by various yield-bearing stablecoin issuers.

Most cleverly, retail investors cannot directly buy these tokenized products. Policy shapes market structure—that’s the GENIUS Act’s secret to manufacturing “payment stablecoins.”

No single piece of legislation can compel market participants to comply solely through coercion—otherwise USDT would never have remained underground for so long. True leverage comes only from aligning with market trends.

Caption: TMMFs underpin payment stablecoins

Source: @ElectricCapital

Although BlackRock’s tokenized products circulate on-chain, they remain inaccessible to “permissionless” buyers—KYC and accredited investor requirements still apply, effectively limiting sales to B2B channels.

You cannot monitor decentralized individual trades—just as the U.S. government cannot track physical USD cash flows—but monitoring a few major players is straightforward.

By recognizing tokenized assets, the U.S. has skillfully constructed a viable framework linking stablecoin issuers, Wall Street giants, and regulators—ensuring users receive stablecoins usable only for payments, not yield generation.

The GENIUS Act binds stablecoins and tokenization together—answering our earlier question: stablecoins become the retail terminal layer for U.S. Treasuries.

Historically, the dollar relied on commercial banks’ credit mechanisms; going forward, it will rely on intermediation by tokenization firms.

Arbitrage Space: Yield-Bearing Stablecoins

Caring for worldly things more than God.

If the GENIUS Act’s recognition of tokenization enabled payment stablecoins, the Clarity Act’s restrictions on tokenization steer stablecoin yield generation.

Yield matters—not because banks fear deposit outflows (JPMorgan struggles with account openings; Coinbase struggles with profitability).

Observe: Under the Clarity Act, if users opt to stake for yield, stablecoin issuers’ interest income ideally derives solely from Treasury products.

But this raises new issues. Issuers like Sky/Ethena—issuing on-chain stablecoins—don’t necessarily need an OCC banking license first, requiring novel regulatory arrangements for yield generation, especially DeFi-based yield.

Excessively high regulatory costs explain Congress’s “lenient” treatment of DeFi development. Beyond that, the dollar needs stablecoins as a distribution channel.

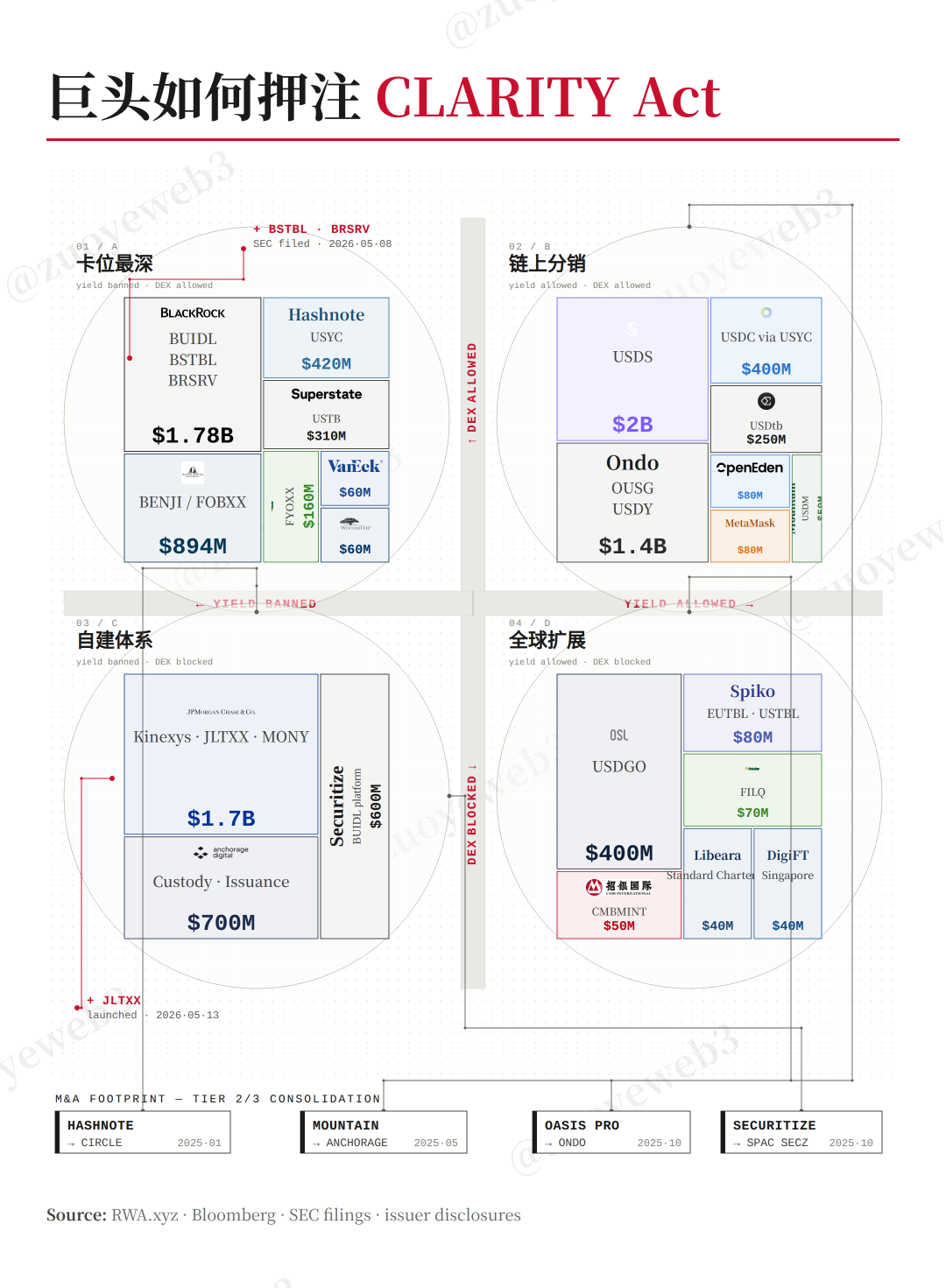

Caption: Giants rush to seize Clarity Act opportunities

Source: @zuoyeweb3

This distribution occurs along two paths: B2B acquisition among giants, and C2C arbitrage issuance across chains and borders.

Among giants, bets hinge on how strictly “passive yield” is prohibited—shaping their intermediary roles accordingly. If DeFi faces similar restrictions, consortium-chain models may revive; if regulation remains relatively permissive, deeper collaboration with on-chain stablecoins becomes feasible.

Further, giants’ intermediary models are hard to bypass: Ondo positions itself as a retail distribution layer for giants; OSL pursues overseas-compliant USD stablecoin markets.

Extending further, Sky’s inclusion of diversified “RWA” assets in USDS reserves is fundamentally leveraged arbitrage—quietly shifting from full-reserve to partial-reserve models.

A key emerging demand: enhancing stablecoin yields atop U.S. Treasuries requires sophisticated financial engineering—the very domain where DeFi yield strategies shine.

Crucially, this yield mechanism targets offshore USD stablecoins like $USDT, replacing their Treasury buyer base with BlackRock’s TMMFs.

For on-chain USD and compliant offshore USD stablecoins, new arbitrage spaces emerge: they cannot reliably capture scalable Treasury yields, forcing them to continually boost utilization—indirectly promoting USD circulation and steady Treasury purchases.

Within this push-pull dynamic, users maximize stablecoin usage—since holding depreciates value, while usage-generated yield flows back into the U.S. financial system, anchored by Treasuries.

That is the Clarity Act’s true purpose: generating global, individual-level demand for the dollar—stablecoin issuance requires Treasuries; stablecoin yield generation requires Treasuries; the loop is complete.

Conclusion

To transcend sovereign constraints, one must rely on payments—a non-negotiable necessity.

Yet driving stablecoin adoption demands yield—a direct incentive mechanism.

Both the GENIUS Act and the Clarity Act center on the entanglement of stablecoins and yield. Since DeFi and cross-border arbitrage remain ungovernable, Wall Street steps in as yield regulator—offering reassurance: whether or not the Clarity Act passes as scheduled, arbitrage never sleeps.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News