Bitget UEX Daily Report | Israel–Lebanon Talks Boost Ceasefire Expectations; S&P 500 and Nasdaq Post Seventh Consecutive Gain; Intel–Google Collaboration Sends Stock to New High

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Israel–Lebanon Talks Boost Ceasefire Expectations; S&P 500 and Nasdaq Post Seventh Consecutive Gain; Intel–Google Collaboration Sends Stock to New High

Institutions believe that the current easing of geopolitical tensions and the resonance with the AI theme remain the primary drivers; however, caution is warranted regarding potential disruptions to Fed rate-cut expectations from weekend geopolitical developments and today’s CPI data.

Author: Bitget

I. Top News

Federal Reserve Updates

Confirmation Hearing for Fed Chair Nominee Postponed

- The U.S. Senate Banking Committee has canceled the confirmation hearing originally scheduled for next Thursday for Kevin Warsh, citing incomplete submission of required materials; Warsh’s team is working urgently to expedite preparation.

- The hearing was due to be formally announced today as the final notification deadline. Market impact: Short-term delays in the Federal Reserve’s leadership transition may slightly increase uncertainty around monetary policy continuity, though the overall dovish trajectory remains unchanged.

International Commodities

ICE Significantly Raises Margin Requirements for Brent Crude and European Diesel Futures

- Intercontinental Exchange (ICE) announced that, amid heightened geopolitical tensions involving Iran and resulting volatility across commodity markets, it will significantly raise margin requirements for Brent crude and European diesel futures contracts. Initial margin for front-month Brent crude futures rises to just over $11,000—more than double the prior level—while diesel margins jump to nearly $21,000, an increase of over 400%.

- The new margin requirements take effect after market close on Friday, April 10. Market impact: Sharply higher trading costs will dampen highly leveraged speculative activity, helping curb extreme oil price swings. However, short-term liquidity risks may intensify, especially amid ongoing supply disruption concerns.

Macroeconomic Policy

Trump Warns Iran Against Charging Transit Fees at Strait of Hormuz; U.S.-China Connected Vehicle Rules Unchanged

- On April 9, Trump posted on social media warning Iran not to impose transit fees on tankers passing through the Strait of Hormuz. He also urged NATO Secretary General Mark Rutte to prompt member states to swiftly commit to securing the strait. Separately, Trump spoke with Israeli Prime Minister Netanyahu, urging Israel to scale back its military campaign against Lebanon to facilitate U.S.-Iran negotiations.

- U.S. Trade Representative Sarah Bianchi confirmed the “connected vehicle rule”—which effectively bans Chinese-made vehicles from entering the U.S.—will remain unchanged. Establishing manufacturing facilities in the U.S. remains extremely difficult for Chinese automakers, and automotive issues are not included in the anticipated outcomes of a potential Trump–Xi summit.

- Iran stated it will not enter talks with the U.S. until a ceasefire is achieved in Lebanon. Market impact: Easing geopolitical risk expectations have buoyed risk assets, yet energy corridor security remains uncertain; short-term breakthroughs in U.S.-China auto trade friction remain unlikely, sustaining pressure on the new energy vehicle supply chain.

II. Market Recap

Commodities & FX Performance

- Spot Gold: Down ~0.21% to $4,756.37/oz; technical rebound after two consecutive days of correction, remaining in high-range consolidation amid easing geopolitical concerns.

- Spot Silver: Down 0.38% to $75.14/oz; tracking gold but with greater volatility, facing clear near-term support tests.

- WTI Crude: Up 0.64% to $98.52/bbl, lifted by progress in Israel–Lebanon negotiations; yesterday’s sharp pullback reflected temporary relief from supply disruption fears.

- Brent Crude: Up 0.87% to $96.69/bbl, following similar dynamics; margin hikes further suppress speculation.

- U.S. Dollar Index: Up 0.12% to 98.927; safe-haven demand recedes as risk sentiment improves.

Cryptocurrency Performance

- BTC: +1.79% over 24 hours, currently trading at $71,967.

- ETH: +0.69% over 24 hours, currently trading at $2,194.

- Total Crypto Market Cap: +0.8% over 24 hours, now approximately $2.51 trillion.

- Liquidations: Total liquidations over 24 hours amounted to ~$351 million, with $247 million in short positions liquidated—short-dominant liquidations reflect short-term upward momentum.

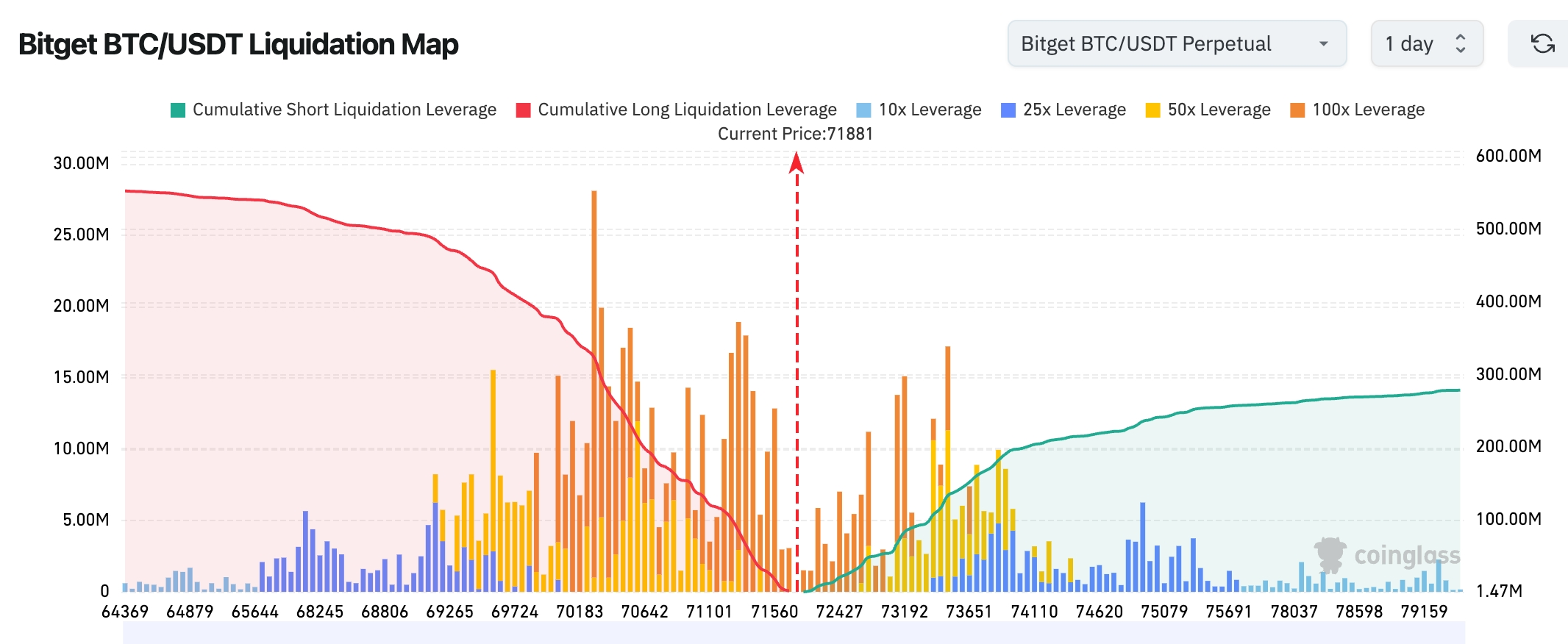

- Bitget BTC/USDT Liquidation Heatmap: Current price (~$71,881) sits in a low-liquidation-density vacuum zone. A dense cluster of long liquidations accumulates between $70,000–$71,500; a break below ~$71,560 could trigger cascading long liquidations. Conversely, a notable concentration of short liquidations lies between $73,200–$74,100; if price breaks above $72,400, upward momentum may accelerate toward this short-liquidation zone, fueling a short squeeze.

- Spot ETF Net Flows: BTC spot ETFs saw net inflows of ~$20.6 million yesterday; ETH spot ETFs saw net inflows of $1.6 million.

- BTC Spot Flows: $2.349 billion inflow vs. $2.249 billion outflow yesterday, resulting in a net inflow of $100 million.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +0.58% to 48,185.80, turning positive year-to-date with stable momentum.

- S&P 500: +0.62% to 6,824.66, marking its seventh consecutive daily gain, lifted by easing geopolitical concerns.

- Nasdaq Composite: +0.83% to 22,822.42, driven by continued strength in semiconductors.

Tech Giants’ Highlights

- NVIDIA (NVDA): +1.01% to $183.91 — robust AI compute demand

- Apple (AAPL): +0.61% to $260.49 — stable consumer electronics demand

- Google-A (GOOGL): +0.52% to $316.37 — deepening collaboration with Intel

- Microsoft (MSFT): −0.34% to $373.07 — relatively soft software sector performance

- Amazon (AMZN): +5.60% to $233.65 — CEO reiterates $200 billion AI investment plan

- Broadcom (AVGO): +1.22% to $355.00 — semiconductor cycle recovery

- Meta Platforms (META): +2.61% to $628.39 — expanding AI infrastructure partnership with CoreWeave

- SanDisk (SNDK): +9.06% to $851.57. Key driver: Confluence of AI capex optimism and de-escalating geopolitical risk boosted tech stocks, with Amazon and Meta leading gains.

Sector Movement Observations

Semiconductor Sector: +2.1%

- Key Stocks: Intel (INTC) +4.7%, Marvell Technology (MRVL) +4.79%

- Catalyst: Intel’s expanded CPU and IPU collaboration with Google, plus its entry into Elon Musk’s Terafab project, reinforcing strong AI data center demand.

Memory Sector: Mixed performance

- Key Stocks: SanDisk (SNDK) +9.05%, Seagate Technology (STX) +0.9%, Micron Technology (MU) +3.63%

- Catalyst: Data center expansion fuels memory demand, though sector-wide divergence remains pronounced.

III. In-Depth Stock Analysis

1. Intel (INTC) – Expanded CPU and IPU Collaboration with Google

Event Summary: Intel officially announced that Google Cloud will launch a multi-year, large-scale deployment of Intel’s Xeon 6 processors and extend its joint development program for custom ASIC-based Intelligent Processing Units (IPUs) to next-generation products—focusing specifically on AI-accelerated offload capabilities and data center network optimization. This collaboration spans critical segments of Google Cloud’s global infrastructure. Additionally, Intel joined Elon Musk’s Terafab mega-factory initiative this week, providing customized chip support for xAI. With these strategic catalysts converging, Intel’s share price surged past the $60 threshold—the highest since 2021—with a single-day gain of 4.7%. Market Interpretation: Multiple Wall Street investment banks view this deepened collaboration as a strong signal that Intel has regained strategic recognition from mainstream cloud service providers in the AI data center hardware space. Its differentiated IPU offerings may gradually erode NVIDIA’s market share beyond GPUs. Entry into the Terafab project further cements Intel’s role in emerging ultra-large-scale AI training clusters. Analysts broadly raised their FY2026 data center revenue forecasts by 15%–20%. Investment Insight: The AI infrastructure capex cycle remains firmly in an upward phase, presenting significant valuation upside for Intel. Investors should closely monitor execution timelines and real-world delivery of these initiatives to assess sustained competitive improvement.

2. Alibaba (BABA) – Preparing Overseas Partnership with Unitree Robotics

Event Summary: An internal Alibaba source confirmed that details of its overseas partnership with Unitree Robotics will be officially announced next week, targeting the embodied AI segment in international markets. The flagship product will be the global rollout of Unitree’s humanoid robot R1 on AliExpress, encompassing supply chain integration, shared marketing channels, and localization adaptation. This marks Alibaba’s first major push into the overseas embodied AI arena following its domestic robotics initiatives. Market Interpretation: The market widely views this as another pivotal step in Alibaba’s robotics and AI hardware ecosystem strategy—capable of rapidly unlocking consumer robotics markets in North America, Europe, and Southeast Asia, thereby boosting overseas growth expectations. Analysts note synergies with Alibaba Cloud and Cainiao logistics, strengthening Alibaba’s integrated global e-commerce + AI hardware competitiveness. Investment Insight: International expansion represents a new growth vector for Alibaba. Investors should watch for catalytic effects on stock price post-announcement. Long-term, embodied AI holds strong potential to become Alibaba’s second growth engine.

3. Amazon (AMZN) – CEO Reaffirms $200 Billion Annual AI Spending Target

Event Summary: In its annual shareholder letter, Amazon CEO Andy Jassy strongly reiterated the necessity of AI infrastructure investment, disclosing plans to invest $25 billion in a new data center in Mississippi and exploring external sales of its in-house AI chips—projecting annual chip-related revenue exceeding $20 billion. The letter also revealed long-term commitments from multiple enterprise clients for AWS AI services, maintaining its FY2026 AI-related capex target at $200 billion. Market Interpretation: Though investors had previously expressed concern about elevated capex, Jassy’s firm stance combined with client commitments has bolstered confidence. Analysts believe Amazon is accelerating its closed-loop AI ecosystem via a dual-track strategy—developing proprietary chips while selling them externally—enhancing its competitive positioning in cloud services. Investment Insight: Amazon’s AI strategy is both clearly defined and execution-strong, promising reinforced long-term competitiveness. Near-term stock elasticity warrants attention; investors should monitor Q2 earnings for evidence of AI revenue realization.

4. Meta Platforms (META) – Expanded AI Compute Partnership with CoreWeave to $21 Billion

Event Summary: Meta and cloud-based AI compute leader CoreWeave have expanded their supply agreement from $14.2 billion (announced September 2024) to $21 billion, bringing cumulative committed spend to ~$35 billion, extending the agreement through 2032. The deal centers on procuring next-generation NVIDIA Rubin platform compute capacity for training Meta’s proprietary large language models and advancing its Llama open-source ecosystem. Market Interpretation: Analysts interpret this as Meta aggressively securing access to NVIDIA’s next-gen Rubin platform, using long-term commitments to lock in top-tier compute resources and further solidify its leadership in open-source AI. Forecast upgrades for META’s AI infrastructure ROI in FY2026–2028 anticipate improved ad targeting precision and accelerated metaverse product development. Investment Insight: Accelerated capital expenditure supports Meta’s long-term growth thesis. Investors should track how compute investments translate into advertising monetization and metaverse synergy. Long-term holding value remains compelling.

IV. Cryptocurrency Project Updates

1. SEC Chair Paul Atkins stated that “Project Crypto” aims to ensure the SEC and CFTC can immediately implement regulatory frameworks once Congress passes the CLARITY Act. However, according to The Block, TD Cowen noted that the White House’s recent stablecoin report is unlikely to resolve political hurdles facing crypto legislation—and the path forward for the CLARITY Act may grow even more challenging.

2. CryptoQuant’s Head of Research observed that recent BTC and ETH rallies were primarily driven by new long positions in perpetual futures markets—not short covering. Within 24 hours of the U.S.-Iran ceasefire announcement, BTC and ETH perpetual open interest rose by $2.1 billion and $2.2 billion respectively—both hitting one-month highs in USD-denominated open interest. Concurrently, the active buy/sell ratio rose above 1, indicating buyer dominance. Coinbase’s premium index turned positive after several weeks of negative readings. CryptoQuant believes that if the ceasefire holds without escalation, BTC’s next key target is $79,000—the “realized price” level historically associated with bear-market resistance.

3. TD Cowen analyst Lance Vitanza issued “Buy” ratings for three digital asset treasury companies, expecting them to outperform spot crypto ETFs. His target prices: Nakamoto ($1), SharpLink Gaming ($16), and Strive ($26), assuming Bitcoin reaches ~$140,000 and Ethereum ~$3,650 by end-2026.

4. AlphaTON Capital, a NASDAQ-listed TON treasury company, plans to raise $43 million through a transaction with U.S. data center operator Vertical Data to expand its AI infrastructure operations; completion is expected in Q2 2026.

5. Onchain Lens reported that Grayscale pledged 83,200 ETH—valued at $183.97 million—hours earlier.

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

- Direct Israel–Lebanon Negotiations: To begin early next week—centered on Hezbollah disarmament and peace implementation; markets continue to monitor ceasefire developments.

Institutional Views:

Multiple investment bank analysts noted that yesterday’s record-setting streak across all three major U.S. indices was driven by improved risk sentiment following the Israel–Lebanon negotiation plan, alongside Trump’s efforts to ease geopolitical tensions—leading to reduced safe-haven demand. Semiconductor sector leadership reflects continued realization of AI capex expectations, further validated by Intel’s deeper collaboration with Google and strong data center demand. While higher margins have increased trading costs in oil markets, temporarily eased geopolitical risks have contributed to lower oil prices—potentially alleviating inflationary pressures. In crypto markets, BTC and ETH posted modest corrections followed by rising total market cap and sustained ETF net inflows. Institutions maintain that the confluence of de-escalating geopolitics and AI themes remains the dominant driver—but caution is warranted regarding weekend geopolitical developments and today’s CPI data, which could shift Fed rate-cut expectations.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News