Finance Needs Speed and Brakes

TechFlow Selected TechFlow Selected

Finance Needs Speed and Brakes

If blockchain can implement strategic braking measures, its speed will surpass that of any other financial infrastructure.

By Prathik Desai

Translated by Block Unicorn

Small annoyances can sometimes save lives.

Consider that persistent beeping sound in your car reminding you to buckle up. It’s irritating—many people complain about it. Yet this very annoyance compels countless drivers to fasten their seatbelts. The result? According to the U.S. Insurance Institute for Highway Safety (IIHS), these constant reminders save approximately 1,500 lives annually in the United States alone. Truly a life-saving feature.

Small irritations can also help you save substantial sums of money.

A frustrating phenomenon in modern banking occurs when you think you’ve completed a wire transfer—only to be interrupted mid-process. You enter the account number, routing number, and recipient’s name. At that point, instead of executing the transfer immediately, the bank pauses to verify whether the recipient’s name matches the account details. This extra step disrupts your flow. In product-team jargon, it’s called “friction.” Yet this pause has become one of the most effective payment security safeguards globally.

Pay.UK’s Confirmation of Payee (CoP) service enables individuals and institutions in the UK to verify recipients before sending payments—and now covers over 99% of transactions across all major payment channels. Its verification volume has surged from 14,000 checks per month in June 2020 to over 70 million per month by July 2025. CoP has reduced “account-mistake” transactions by 59% and cut end-user financial losses by 20–40%.

This is especially critical at a time when finance has spent over a decade striving to make transactions invisible. We’ve seen “tap once,” “swipe once,” and “click-to-pay” efforts—all designed to let money move silently in the background. Finance’s instinct is often to treat every pause as a flaw. As the industry evolves, it grows increasingly obsessed with seamlessness. Yet this evolution repeatedly reminds us that certain so-called “frictions” are in fact essential brakes—preventing systemic collapse.

Traditional Finance’s Need for Brakes

Today, finance has embedded these braking mechanisms into every new infrastructure it builds.

In the U.S., broker-dealers granted market access must implement risk controls to limit financial exposure and ensure regulatory compliance. When the U.S. Securities and Exchange Commission (SEC) adopted Rule 15c3-5, it explicitly stated the rule was intended to address risks arising from automated high-speed trading and prevent unfettered access to exchanges.

The industry keeps relearning this lesson for a simple reason: when brakes fail, the damage often exceeds what institutions can absorb—or recover from.

On Black Monday in 1987, the Dow Jones Industrial Average plunged 22% in a single day. The Brady Commission recommended introducing circuit breakers—a “pause button”—that would halt trading for 15 minutes whenever markets fell by a predetermined percentage. Without such limits, Black Monday alone erased $1.7 trillion in global market value. Adjusted for inflation, that loss equals over $4.7 trillion today—more than Germany’s current GDP, the world’s third-largest economy.

These brakes taught finance that sometimes, the only way to sustain speed is to briefly shut down the machine. In other cases, even a short pause resolves the problem.

In August 2012, Knight Capital Group suffered a software glitch that caused its computers to buy and sell millions of shares within just 45 minutes. The error triggered $440 million in losses in under an hour—nearly bankrupting the market maker. Knight had optimized its systems for speed, which is vital in market-making. But an uncontrolled, brakeless system—even the fastest one—can collapse instantly. The lesson? The faster the system, the more critical the braking mechanism.

Retail finance itself faces mounting challenges.

For years, brokers have relentlessly simplified access to high-risk products to drive retail user growth. Their persistence ultimately eroded trust. In FINRA’s 2021 disciplinary action against Robinhood, the regulator found the firm failed to conduct adequate due diligence before approving customers for options trading—and relied heavily on unregulated, automated “approval bots.” This nonprofit self-regulatory organization, charged with investor protection, claimed Robinhood’s system approved customers based on inconsistent or illogical data—and allowed applicants whose risk profiles were clearly suspect to gain approval.

Robinhood’s system was optimized to process applications rapidly—avoiding potential customer wait times. What it lacked was a meaningful pause between curiosity and safety. Speed, yes—but no brakes.

The Peculiar Case of Cryptocurrency

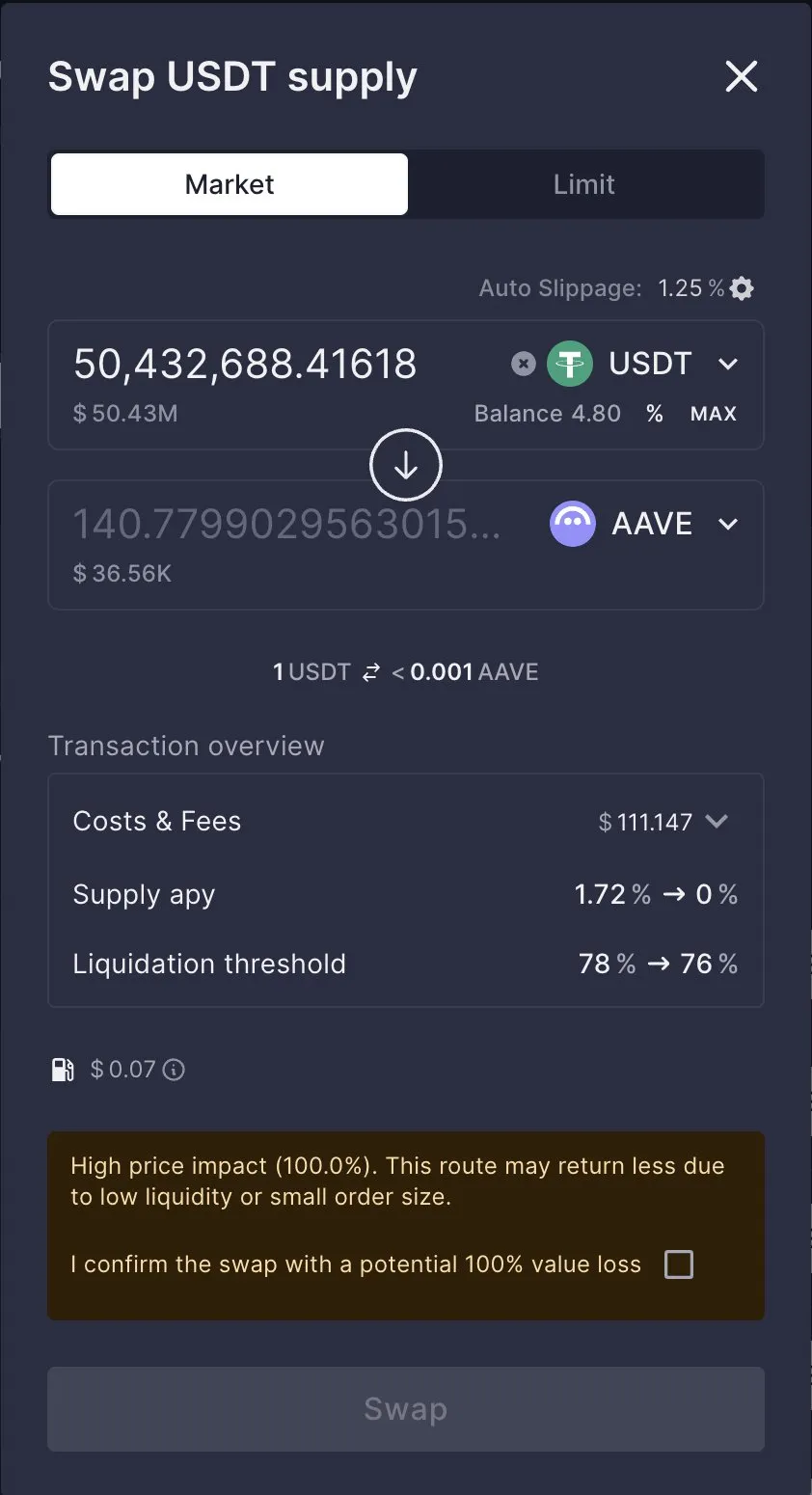

The recent Aave-CoW incident in cryptocurrency has elevated finance’s need for braking mechanisms to an entirely new level.

On March 12, 2025, a user executed a $50 million swap via CoW Swap—an open-source decentralized exchange (DEX) aggregator designed to protect users from frontrunning bots. The trade was integrated into Aave’s frontend. Due to insufficient liquidity, the user received only $36,930 worth of tokens—while paying $50 million.

Although Aave’s post-mortem analysis noted the user ignored explicit “high slippage impact” warnings, Stani Kulechov, Aave’s founder and CEO, posted on X that the Aave team “will explore how to improve these safeguards.”

Setting jargon aside, the conclusion is clear: a fast interface let a catastrophic trade proceed too far before the system could react. While one might question the user’s judgment—or ignorance of warnings—treating this as an isolated event would be both convenient and counterproductive for the development of novel financial infrastructure like blockchain.

If crypto aims to avoid repeating past mistakes, the solution lies in building smarter execution layers. Some decentralized finance (DeFi) protocols are already moving in this direction.

Definitive.Fi, for instance, argues large on-chain trades shouldn’t simply follow the path technically feasible. Instead, they should be simulated pre-submission, stress-tested against real market conditions, split into smaller chunks if needed, and routed across broader liquidity pools. Thus, a robust trading system shouldn’t merely check whether it *can* execute an order—it should identify the *optimal path* to execute it.

For any emerging infrastructure, trust and added safeguards aren’t optional features—especially in finance. A product that makes trading, lending, or fund transfers effortless may fuel rapid adoption—but when it fails, consequences are severe. We saw this pattern across all the traditional finance examples above. Systems strive to minimize visible friction points—even when those frictions are necessary constraints—masking complexity while hoping smooth UX will earn consumer trust.

Yet trust in finance rarely emerges this way. It usually arises when institutions recognize critical moments requiring intervention—and take unpleasant but necessary actions to stop harmful behavior. Pay.UK’s Confirmation of Payee is precisely such a case. Repeatedly verifying a bank account name is certainly not enjoyable—but it does intervene precisely when errors could cause costly, irreversible losses.

Aave’s Stani understands this well—which is why he acknowledged users don’t always grasp how orders flow, who the counterparty is, or whether better execution routes exist. Such awareness is especially vital in nascent sectors like crypto and blockchain, where few users understand technical transaction flows—or the implications of each click. In this context, acknowledging pain points and proactively addressing them is essential to building consumer trust.

The challenge lies in the razor-thin line between braking mechanisms and arbitrary inconvenience or friction. Good brakes don’t slow things down outright—they apply subtle resistance at precisely calibrated intervals. In the Aave-CoW incident, imagine a good brake as an economic reasonableness check: scanning more venues before routing, preventing order intent from falling into malicious hands, simulating outcomes pre-execution, and splitting large orders to avoid punishing users for scale. These mechanisms are foundational to trustworthy financial infrastructure.

That distinction matters because finance still grapples with unresolved pain points: burdensome, pointless paperwork; inefficient compliance processes slowing everything down; hidden fees disguised as part of the workflow; and intimidatingly complex sign-up flows that deter new users.

None of these should be defended. Implementing “brakes” isn’t about justifying uglier products or more pop-up ads—it’s about designing intentional pauses when users are about to make irreversible decisions based on incomplete information. Especially during low-demand periods, when handling large orders, selling high-risk products, exploring new payment methods, or performing one-click actions—where risk is immediate and speed is not the top priority.

There are also commercial insights here.

Finance often claims safeguards should only be built *after* achieving product-market fit. That sequence is backwards. In finance, safeguards *are* an inseparable part of product-market fit. When implemented well, they don’t hinder adoption at all. Pay.UK’s Confirmation of Payee further confirms it’s no longer an optional anti-fraud tool—it’s a practical service users *expect* to see when transacting through the system.

Emerging financial infrastructure—like blockchain—aims to earn trust and withstand errors, scandals, and market stress, just as traditional finance does. But that’s no easy feat. It must proactively consider how to earn trust *before* winning users—because only with trust do users naturally follow. The reverse, however, doesn’t hold true.

If blockchain embraces strategic braking, its speed will surpass *any* other financial infrastructure.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News