Silver crisis: when the paper-based system begins to fail

TechFlow Selected TechFlow Selected

Silver crisis: when the paper-based system begins to fail

When the music stops, only those holding real cash will be able to sit down safely.

By: Xiao Bing | TechFlow

In December's precious metals market, the spotlight isn't on gold—silver is the brightest star.

From $40, it surged to $50, $55, $60, racing through historic price levels at an almost uncontrollable speed, barely giving the market time to breathe.

On December 12, spot silver briefly touched a record high of $64.28 per ounce before sharply reversing downward. From the beginning of the year, silver has risen nearly 110%, far outpacing gold’s 60% gain.

This rally appears "entirely reasonable"—and that’s precisely what makes it especially dangerous.

The Crisis Behind the Rally

Why did silver rise?

Because it seemed to deserve it.

From the perspective of mainstream institutions, everything made sense.

Renewed expectations of Fed rate cuts have reignited precious metals markets. Recent weak employment and inflation data have led markets to bet on further easing by early 2026. As a highly elastic asset, silver reacted more strongly than gold.

Industrial demand has also played a role. The explosive growth in solar power, electric vehicles, data centers, and AI infrastructure has fully highlighted silver’s dual nature—as both a precious metal and an industrial metal.

Falling global inventories have added fuel to the fire. Mine output in Mexico and Peru fell short of expectations in Q4, and major exchange warehouses are holding fewer silver bars each year.

...

If you only consider these reasons, silver’s rise represents a “consensus”—even a long-overdue revaluation.

But here lies the danger:

Silver’s rally looks logical—but not solid.

The reason is simple: silver is not gold. It lacks the consensus backing gold enjoys, and there is no “national team” supporting it.

Gold remains strong because central banks around the world are buying it. Over the past three years, global central banks have purchased over 2,300 tons of gold—assets recorded on national balance sheets as extensions of sovereign credit.

Silver is different. Global central banks hold over 36,000 tons of gold reserves, but official silver reserves are virtually zero. Without central bank support, silver lacks any systemic stabilizer during extreme market volatility—it’s a classic “island asset.”

The disparity in market depth is even starker. Gold sees daily trading volumes of about $150 billion; silver trades just $5 billion. If gold is the Pacific Ocean, silver is at best Poyang Lake.

It has a small market cap, few market makers, limited liquidity, and scarce physical reserves. Most critically, silver is primarily traded not in physical form, but as “paper silver”—futures, derivatives, and ETFs dominate the market.

This is a dangerous structure.

Shallow waters capsize easily—large capital inflows can instantly disrupt the entire market.

And this is exactly what happened this year: a sudden influx of capital pushed up a market that was already shallow, lifting prices off their fundamentals.

Futures Squeeze

What drove silver prices off track wasn’t the seemingly rational fundamentals mentioned above—the real battle took place in the futures market.

Under normal conditions, spot silver prices should be slightly higher than futures prices. This is easy to understand: storing physical silver incurs warehousing and insurance costs, while futures contracts are merely paper agreements and thus cheaper. This difference is known as “contango.”

But starting in the third quarter of this year, this logic flipped.

Futures prices began systematically exceeding spot prices—and the gap kept widening. What does this mean?

Someone is aggressively pushing up prices in the futures market. This “backwardation” phenomenon typically occurs in only two scenarios: either the market is extremely bullish on the future, or someone is executing a short squeeze.

Given that improvements in silver’s fundamentals have been gradual—photovoltaic and new energy demand won’t explode exponentially in months, and mine output hasn’t suddenly dried up—the aggressive behavior in the futures market points more toward the latter: capital is artificially inflating futures prices.

Even more alarming signals emerged from the physical delivery market.

Historical operating data from COMEX (the New York Mercantile Exchange), the world’s largest precious metals market, shows that less than 2% of precious metals futures contracts result in physical delivery. The remaining 98% are settled in cash or rolled over via new contracts.

Yet over recent months, COMEX’s physical silver delivery volume has surged far beyond historical averages. An increasing number of investors are losing faith in “paper silver” and demanding actual silver bars.

A similar trend has appeared in silver ETFs. While large inflows continue, some investors are redeeming shares—not for cash, but for physical silver. This “bank-run-style” redemption is straining ETF silver reserves.

This year, major silver markets—New York COMEX, London LBMA, and the Shanghai Metal Exchange—all experienced runs on physical supplies.

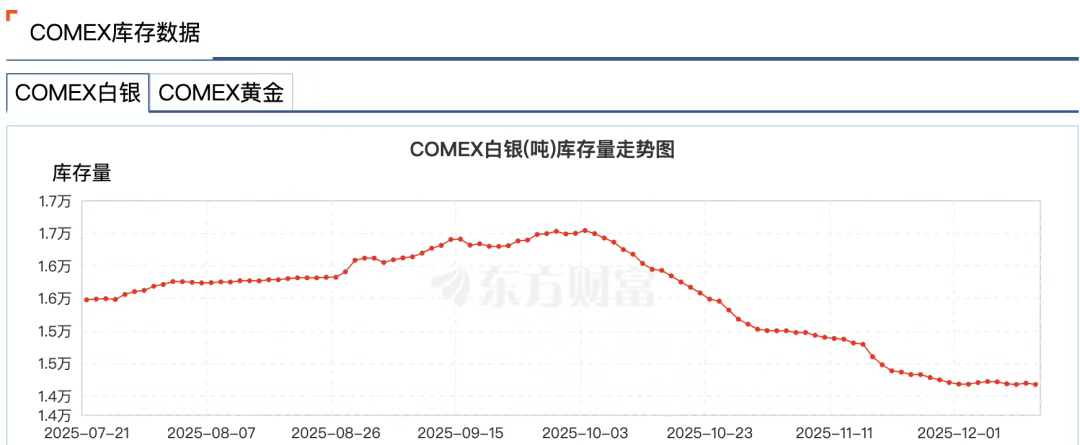

Wind data shows that in the week ending November 24, the Shanghai Gold Exchange’s silver inventory dropped by 58.83 tons to 715.875 tons—the lowest since July 3, 2016. COMEX silver inventory plunged from 16,500 tons in early October to 14,100 tons—a 14% decline.

The reasons aren’t hard to grasp: amid a dollar rate-cutting cycle, investors prefer not to settle in dollars. There’s also a hidden fear—that exchanges may not actually have enough silver to deliver.

Modern precious metals markets are highly financialized systems where most “silver” exists only as book entries. Real silver bars are repeatedly pledged, leased, and used in derivatives globally. One ounce of physical silver may simultaneously back dozens of different paper claims.

As veteran trader Andy Schectman notes, in London’s LBMA, only 140 million ounces of silver are freely available, yet daily trading volume reaches 600 million ounces. Against this 140 million ounces, over 2 billion ounces of paper claims exist.

This “fractional reserve system” works fine under normal conditions, but when everyone demands physical delivery, a liquidity crisis erupts.

When such crises loom, financial markets often exhibit a strange phenomenon—commonly called “pulling the plug.”

On November 28, CME suffered an outage lasting nearly 11 hours due to a “data center cooling issue,” setting a historical record and halting updates for COMEX gold and silver futures.

Notably, the outage occurred at the critical moment silver broke its all-time high—spot silver breached $56, and silver futures surpassed $57.

Market rumors suggest the outage protected commodity market makers exposed to extreme risks and potential massive losses.

Later, data center operator CyrusOne attributed the disruption to human error—fueling even more conspiracy theories.

In short, a rally driven by futures squeezes ensures extreme volatility in the silver market. Silver has effectively transformed from a traditional safe-haven asset into a high-risk instrument.

Who Is Running the Show?

In this squeeze drama, one name stands out: JPMorgan Chase.

For good reason—it’s widely recognized as the dominant player in the silver market.

From at least 2008 to 2016, JPMorgan manipulated gold and silver prices through its traders.

Their method was crude: placing massive buy or sell orders in the futures market to create false supply-demand signals, luring other traders to follow, then canceling the orders at the last second to profit from price swings.

This so-called “spoofing” tactic eventually led JPMorgan to pay a $920 million fine in 2020—the largest single penalty ever issued by the CFTC at the time.

But the textbook case of market manipulation goes deeper.

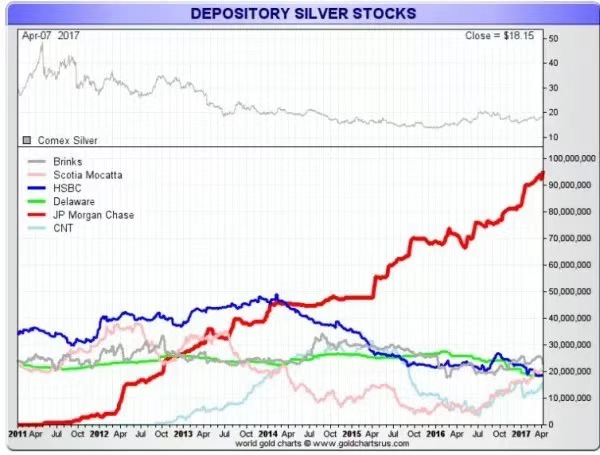

While JPMorgan used short selling and spoofing in the futures market to suppress silver prices, it simultaneously bought up vast quantities of physical metal at the artificially low prices it created.

Starting in 2011, when silver neared $50, JPMorgan began stockpiling silver in its COMEX vaults. While other major institutions reduced exposure, it steadily increased holdings—eventually accounting for up to 50% of COMEX’s total silver inventory.

This strategy exploited structural weaknesses in the silver market: paper silver prices dictate physical prices, and JPMorgan could influence paper prices while being one of the largest holders of physical silver.

So, what role has JPMorgan played in this latest silver squeeze?

On the surface, JPMorgan seems to have “reformed.” After its 2020 settlement, it implemented comprehensive compliance reforms, including hiring hundreds of new compliance officers.

Currently, there is no evidence linking JPMorgan to the current short squeeze. Yet in the silver market, JPMorgan still wields immense influence.

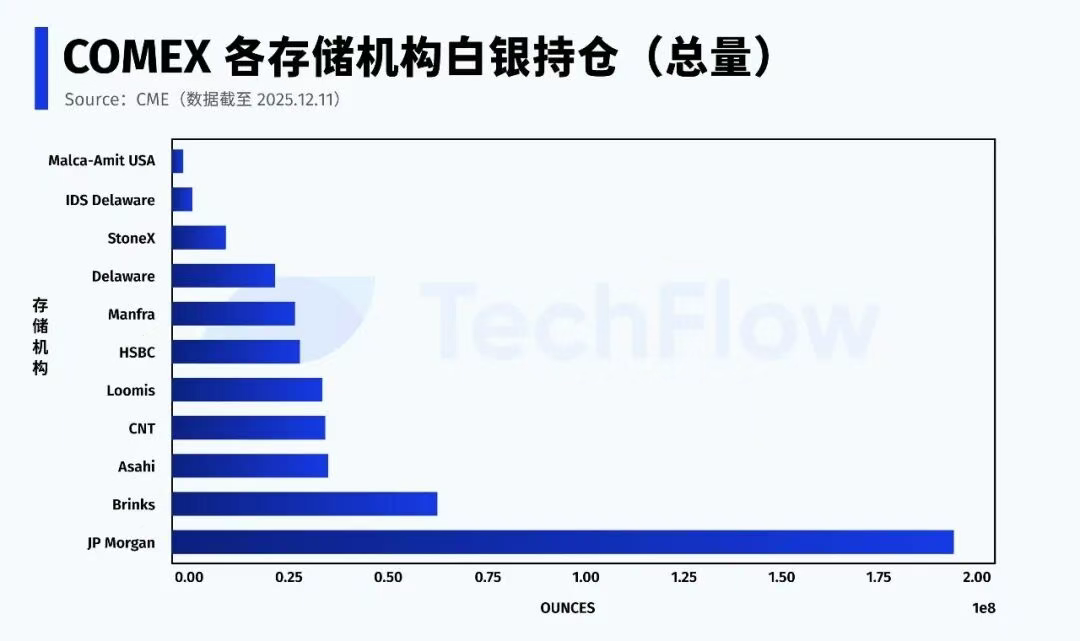

According to the latest CME data from December 11, JPMorgan holds approximately 196 million ounces of silver (proprietary + brokerage) under the COMEX system—nearly 43% of the exchange’s total inventory.

Moreover, JPMorgan holds another unique role—as custodian of the silver ETF (SLV). As of November 2025, it safeguards 517 million ounces of silver, worth $32.1 billion.

More crucially, in the Eligible silver category (qualified for delivery but not yet registered), JPMorgan controls over half of the total supply.

In any silver squeeze, the real game revolves around two questions: who can deliver physical silver, and whether and when that silver will be allowed into the delivery pool.

Unlike its past role as a major short-seller, today JPMorgan sits at the gate of the “silver valve.”

Currently, Registered silver (eligible for immediate delivery) accounts for only about 30% of total inventory. When Eligible silver is heavily concentrated in a few institutions, the stability of the silver futures market ultimately depends on decisions made by just a handful of key players.

The Paper System Is Breaking Down

If one sentence could describe today’s silver market, it would be:

The rally continues, but the rules have changed.

The market has undergone an irreversible shift—trust in the “paper silver” system is eroding.

Silver is not an isolated case. The same transformation has already begun in the gold market.

Gold inventories at the New York futures exchange continue to decline, with Registered gold repeatedly hitting lows. Exchanges have had to transfer bars from the “Eligible” pool—originally not intended for delivery—to fulfill settlement requirements.

Globally, capital is quietly migrating.

For over a decade, mainstream asset allocation favored highly financialized instruments—ETFs, derivatives, structured products, leveraged tools—everything became “securitized.”

Now, increasing amounts of capital are exiting financial assets and turning toward physical assets that don’t rely on financial intermediaries or credit guarantees—the prime examples being gold and silver.

Central banks are continuously and massively adding gold—almost exclusively in physical form. Russia has banned gold exports, and even Western nations like Germany and the Netherlands are demanding repatriation of overseas-stored gold reserves.

Liquidity is giving way to certainty.

When gold supply fails to meet massive physical demand, capital turns to alternatives—silver naturally becomes the top choice.

At its core, this physicalization movement reflects a broader struggle over monetary pricing power amid de-dollarization and deglobalization.

As Bloomberg reported in October, gold is moving from West to East.

Data from the U.S. CME and the London Bullion Market Association (LBMA) show that since late April, over 527 tons of gold have flowed out of the vaults of New York and London—the two largest Western markets—while Asian gold-consuming nations like China have seen rising imports. China’s August gold import hit a four-year high.

To adapt to market changes, in late November 2025, JPMorgan relocated its precious metals trading team from the U.S. to Singapore.

Behind the surge in gold and silver lies a return of the “gold standard” concept. A full revival may be unrealistic in the short term, but one thing is certain: whoever holds more physical metal gains greater pricing power.

When the music stops, only those holding real gold and silver will remain seated.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News