IOSG | In-depth analysis of stablecoin blockchains: Plasma, Stable, and Arc

TechFlow Selected TechFlow Selected

IOSG | In-depth analysis of stablecoin blockchains: Plasma, Stable, and Arc

Delve into its issuer, market dynamics, and other participants behind it.

Author: Sam @IOSG

Introduction

Artemis' 2025 research report indicates that the economy settled via stablecoins reached approximately $26 trillion in 2024—already on par with mainstream payment networks. In contrast, traditional payment systems operate under a fee structure akin to a "hidden tax": around 3% transaction fees, foreign exchange spreads, and ubiquitous wire transfer charges.

Stablecoin payments compress these costs down to mere cents—or even lower. When the cost of moving funds plummets, business models are fundamentally reshaped: platforms no longer rely on transaction fees to survive but instead compete on deeper value propositions—such as savings yields, liquidity, and credit services.

With the U.S. GENIUS Act now in effect and Hong Kong’s Stablecoin Ordinance offering a similar regulatory blueprint, banks, card networks, and fintech companies are transitioning from pilot phases to large-scale production use. Banks are launching their own stablecoins or forming close partnerships with fintechs; card networks are integrating stablecoins into their backend settlement systems; and fintechs are rolling out compliant stablecoin accounts, cross-border payment solutions, KYC-integrated on-chain settlements, and tax reporting tools. Stablecoins are evolving from exchange collateral into standard payment “infrastructure.”

The current bottleneck lies in user experience. Wallets today still assume users are crypto-native; fee disparities across networks remain significant; and users often need to first hold a highly volatile token just to transfer a dollar-pegged stablecoin. However, gasless stablecoin transfers enabled by fee sponsorship and account abstraction will eliminate this friction entirely. Combined with predictable costs, smoother fiat on-ramps, and standardized compliance components, stablecoins will cease to feel like “crypto”—their experience will truly converge with that of “money.”

Core insight: Public blockchains centered around stablecoins already possess the necessary scale and stability. To become everyday currency, they further require: consumer-grade UX, programmable compliance, and imperceptible transaction fees. As these elements—especially gasless transfers and better fiat ramps—are progressively implemented, competition will shift from “charging for moving money” to “delivering value around the movement of money,” including yield, liquidity, security, and simple, trustworthy tools.

The following sections provide a rapid overview of standout projects in the stablecoin/payment blockchain space. This article focuses primarily on Plasma, Stable, and Arc, delving into their issuers, market dynamics, and other participants—the full landscape of the “stablecoin rail wars.”

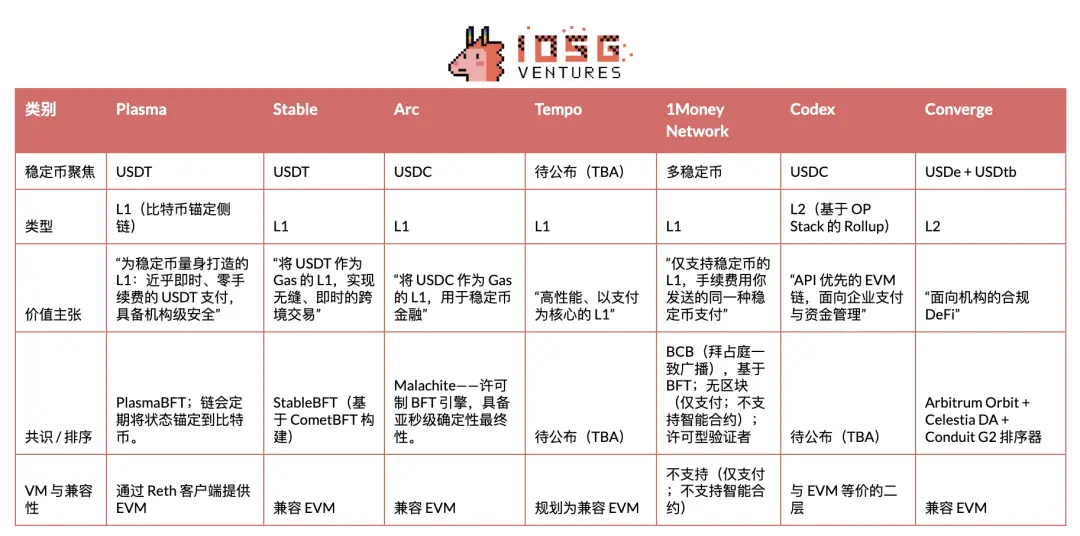

Plasma

Plasma is a blockchain purpose-built for USDT, designed to serve as its native settlement layer and optimized specifically for high-throughput, low-latency stablecoin payments. It entered private testnet in late May 2025, transitioned to public testnet in July, and successfully launched its mainnet beta on September 25.

Within the stablecoin payment blockchain sector, Plasma was the first project to conduct a TGE and achieved a successful market launch: capturing strong mindshare, setting records for day-one TVL and liquidity, and establishing early partnerships with multiple blue-chip DeFi projects—laying a solid foundation for its ecosystem.

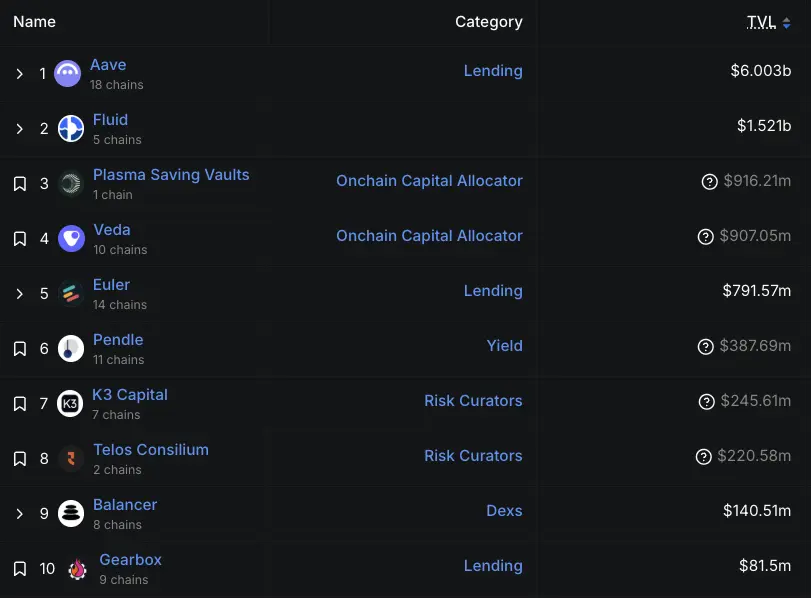

Its growth momentum since mainnet beta has been evident. By September 29, Aave deposits on the Plasma chain surpassed $650 million, making it Aave's second-largest market. By September 30, over 75,000 users had registered for its ecosystem wallet, Plasma One. According to the latest DeFiLlama data, Aave’s TVL on Plasma stands at $6 billion—down from peak levels but still firmly ranking as Aave’s second-largest market, behind only Ethereum ($53.9 billion), and significantly ahead of Arbitrum and Base (both around $2 billion). Additionally, projects such as Veda, Euler, Fluid, and Pendle have contributed substantial locked value.

▲ source: DeFiLlama

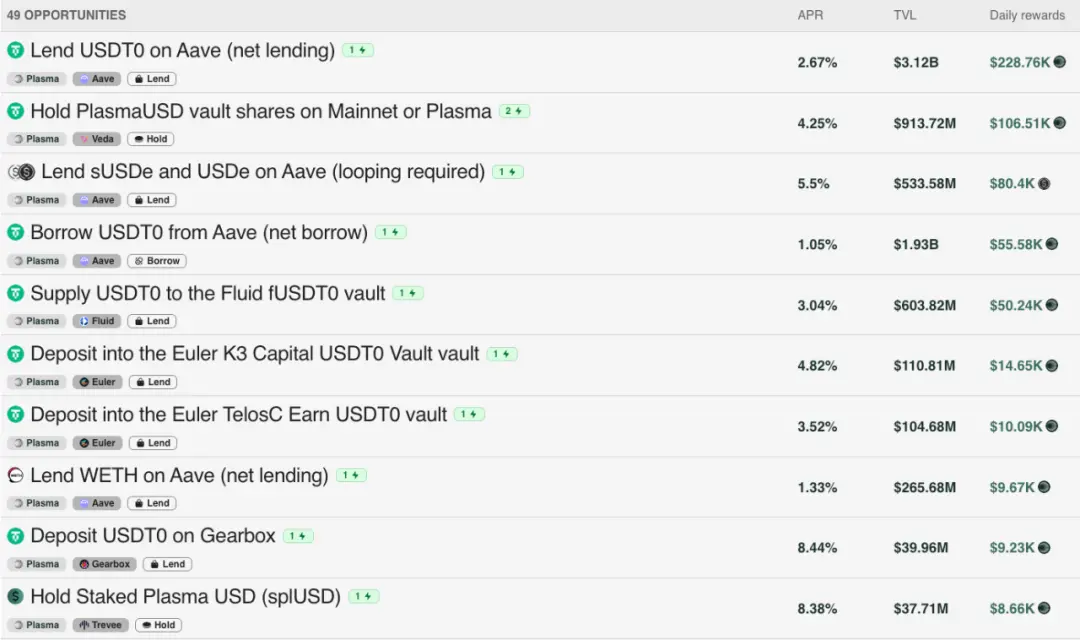

Plasma’s early TVL growth also benefited from incentive budgets: according to its official tokenomics model, 40% of the total XPL supply is allocated to ecosystem and growth funds. Of this, 8% (800 million XPL) was immediately unlocked upon mainnet beta launch to fund partner DeFi incentives, liquidity needs, and exchange integrations; the remaining 32% (3.2 billion XPL) will be released monthly over three years. Currently, major liquidity pools on the Plasma chain offer additional yields of approximately 2–8% through XPL rewards, on top of base yields.

▲ source: Plasma

Naturally, there is external commentary suggesting its early growth was primarily driven by incentives rather than organic adoption. As its CEO Paul emphasized, relying solely on crypto-native users and incentives is not a sustainable model; the real test lies in future real-world usage—which will remain a key focus of our ongoing observation.

Go-To-Market Strategy

Plasma focuses on USDT, targeting emerging markets—particularly Southeast Asia, Latin America, and the Middle East. In these regions, USDT already enjoys powerful network effects, having become an essential tool for remittances, merchant payments, and daily P2P transfers. Turning this strategic vision into reality requires robust on-the-ground distribution: advancing corridor by corridor, building agent networks, delivering localized user onboarding, and carefully timing regulatory entry. It also means defining clearer risk boundaries than Tron.

Plasma views developer experience as a moat, arguing that USDT needs what Circle built for USDC: a friendly developer interface. Historically, Circle invested heavily to make USDC easy to integrate and develop with, whereas Tether lagged—leaving a major opportunity for a USDT application ecosystem, provided the payment rail is properly packaged. Specifically, Plasma offers a unified API atop its payment tech stack, allowing payment developers to avoid assembling underlying infrastructure themselves. Behind this single interface lie pre-integrated partners as plug-and-play foundational modules. Plasma is also exploring confidential payments—achieving privacy within a compliance framework. Its ultimate goal is clear: “make USDT extremely easy to integrate and build with.”

In sum, this corridor-driven go-to-market strategy and API-centric developer approach culminate in Plasma One—the consumer-facing front-end product that delivers the entire vision to everyday users. On September 22, 2025, Plasma launched Plasma One: a consumer-oriented “stablecoin-native” digital banking and card product that consolidates storing, spending, earning, and sending digital dollars into a single app. The team positions it as the missing unified interface for hundreds of millions of users who already depend on stablecoins but still face local friction points—such as clunky wallets, limited fiat on-ramps, and reliance on centralized exchanges.

Access to the product is being rolled out gradually via a waitlist. Key features include direct payments from interest-bearing stablecoin balances (targeting over 10% APY), up to 4% cashback on spending, instant zero-fee USDT transfers within the app, and card services usable at approximately 150 million merchants across more than 150 countries.

Business Model Breakdown

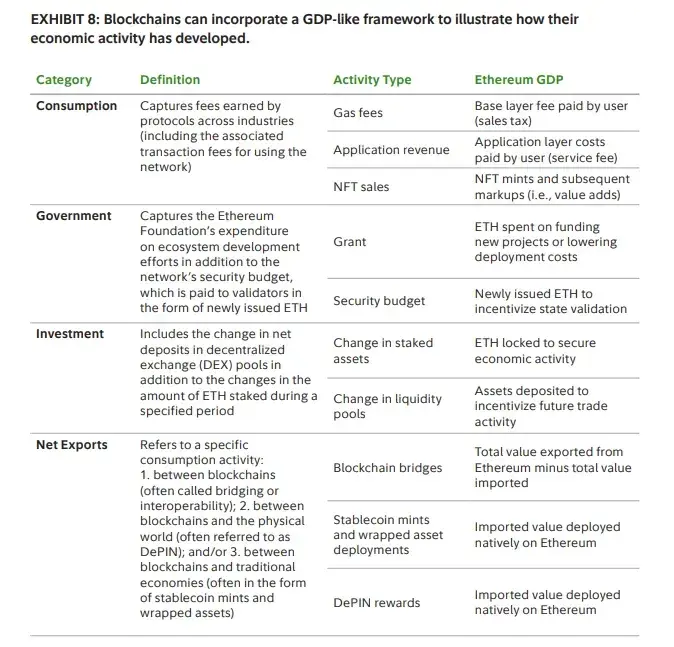

Plasma’s core pricing strategy aims to maximize daily usage while maintaining economic sustainability through other revenue streams: simple USDT-to-USDT transfers are free, while all other on-chain operations incur fees. From a “blockchain GDP” perspective, Plasma intentionally shifts value capture away from per-transaction “sales taxes” (i.e., base USDT transfer gas fees) toward application-layer revenues. The DeFi layer corresponds to the “investment” segment in this framework—aimed at nurturing liquidity and yield markets. While net exports (i.e., USDT bridging in/out) remain important, the economic重心 has shifted from transaction fees to service fees for applications and liquidity infrastructure.

▲ source: Fidelity

For users, zero fees are not just about saving money—they unlock new use cases. When sending $5 no longer costs $1 in fees, microtransactions become viable. Remittances can arrive in full, without middlemen taking cuts. Merchants can accept stablecoin payments without surrendering 2–3% of revenue to invoicing/billing software and card networks.

Technically, Plasma operates a paymaster compliant with EIP-4337. This paymaster sponsors gas fees for calls to the official USDT’s transfer() and transferFrom() functions on the Plasma chain. The Plasma Foundation has pre-funded this paymaster using its native XPL token and employs lightweight validation mechanisms to prevent abuse.

Stable

Stable is a Layer 1 optimized for USDT payments, aiming to solve inefficiencies in current infrastructure—including unpredictable fees, slow settlement times, and overly complex user experiences.

Positioned as a payment-dedicated L1 “built for USDT,” Stable’s market strategy involves directly partnering with payment service providers (PSPs), merchants, business integrators, vendors, and digital banks. PSPs welcome this, as Stable removes two operational burdens: managing volatile gas tokens and bearing transfer costs. Given many PSPs face high technical barriers, Stable currently operates in a “service workshop” mode—handling integrations end-to-end—with plans to later codify these workflows into an SDK for self-service integration. To provide production-grade assurances, it introduces “enterprise-grade blockspace”—a subscription service guaranteeing VIP transactions are prioritized at the top of blocks, ensuring deterministic, first-block settlement and smoother cost predictability during network congestion.

Geographically, its market entry follows existing USDT usage patterns, adopting an “Asia-Pacific first” strategy before expanding into other USDT-dominant regions like Latin America and Africa.

On September 29, Stable launched a consumer-facing app (app.stable.xyz), targeting entirely new, non-DeFi users. Positioned as a simple USDT payment wallet for everyday needs (P2P transfers, merchant payments, rent, etc.), it offers instant settlement, gasless P2P transfers, and transparent, predictable fees denominated in USDT. Access is currently limited to a waitlist. Early traction in South Korea demonstrates market appeal: Stable Pay attracted over 100,000 user sign-ups through offline booths (as of September 29).

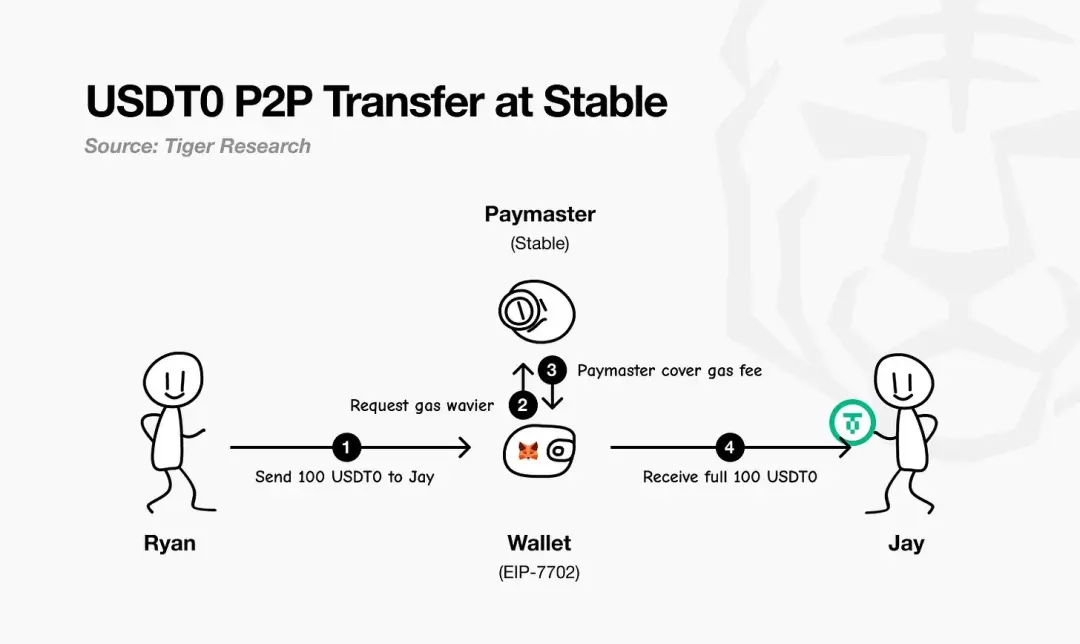

Stable achieves gasless USDT payments via EIP-7702. This standard allows users’ existing wallets to temporarily become “smart wallets” within a single transaction, enabling custom logic execution and fee settlement—all without requiring a separate gas token. All fees are priced and paid in USDT.

As illustrated by Tiger Research’s flowchart: the payer initiates a payment; the EIP-7702 wallet requests gas fee exemption from Stable’s paymaster; the paymaster sponsors and settles the network fee; finally, the recipient receives the full amount with no deductions. In practice, users only need to hold USDT.

▲ source: Tiger Research

On the business side, Stable prioritizes market share expansion over immediate revenue, using gasless USDT payments to acquire users and build payment volume. Long-term profitability will come primarily from its consumer app, supplemented by select on-chain mechanisms.

Beyond USDT, Stable sees major opportunities with other stablecoins. With PayPal Ventures investing in Stable in late September 2025, as part of the deal, Stable will natively support PayPal’s stablecoin PYUSD and drive its distribution, enabling PayPal users to “use PYUSD directly” for payments—with gas fees also payable in PYUSD. This means PYUSD will also enjoy gasless payments on Stable—extending the same ease-of-use that attracts PSPs to USDT payments to PYUSD as well.

▲ source: https://x.com/PayPal/status/1971231982135792031

Architecture Deep Dive

Stable’s architecture begins at the consensus layer—StableBFT. A proof-of-stake protocol custom-built on CometBFT, it aims for high throughput, low latency, and high reliability. Its roadmap is pragmatic: short-term focus on optimizing this mature BFT engine, with a long-term vision to transition to a directed acyclic graph (DAG)-based design for greater scalability.

Above consensus, Stable EVM seamlessly integrates the chain’s core capabilities into developers’ workflows. Dedicated precompiles allow EVM smart contracts to securely and atomically invoke core chain logic. Future performance gains will come with the introduction of StableVM++.

Throughput also depends on data handling. StableDB resolves post-block storage bottlenecks by decoupling state commitment from data persistence. Finally, its high-performance RPC layer abandons monolithic design, adopting a分流 path architecture: lightweight, specialized nodes handle different request types, avoiding resource contention, improving tail latency, and ensuring real-time responsiveness even as chain throughput grows substantially.

Critically, Stable positions itself as an L1, not an L2. Its core belief: real-world businesses should not have to wait for upstream protocol upgrades to launch payment features. Full-stack control over validators, consensus, execution, data, and RPC layers enables the team to prioritize core guarantees for payments—while retaining EVM compatibility so developers can easily port existing code. The result is an EVM-compatible Layer 1 fully optimized for payments.

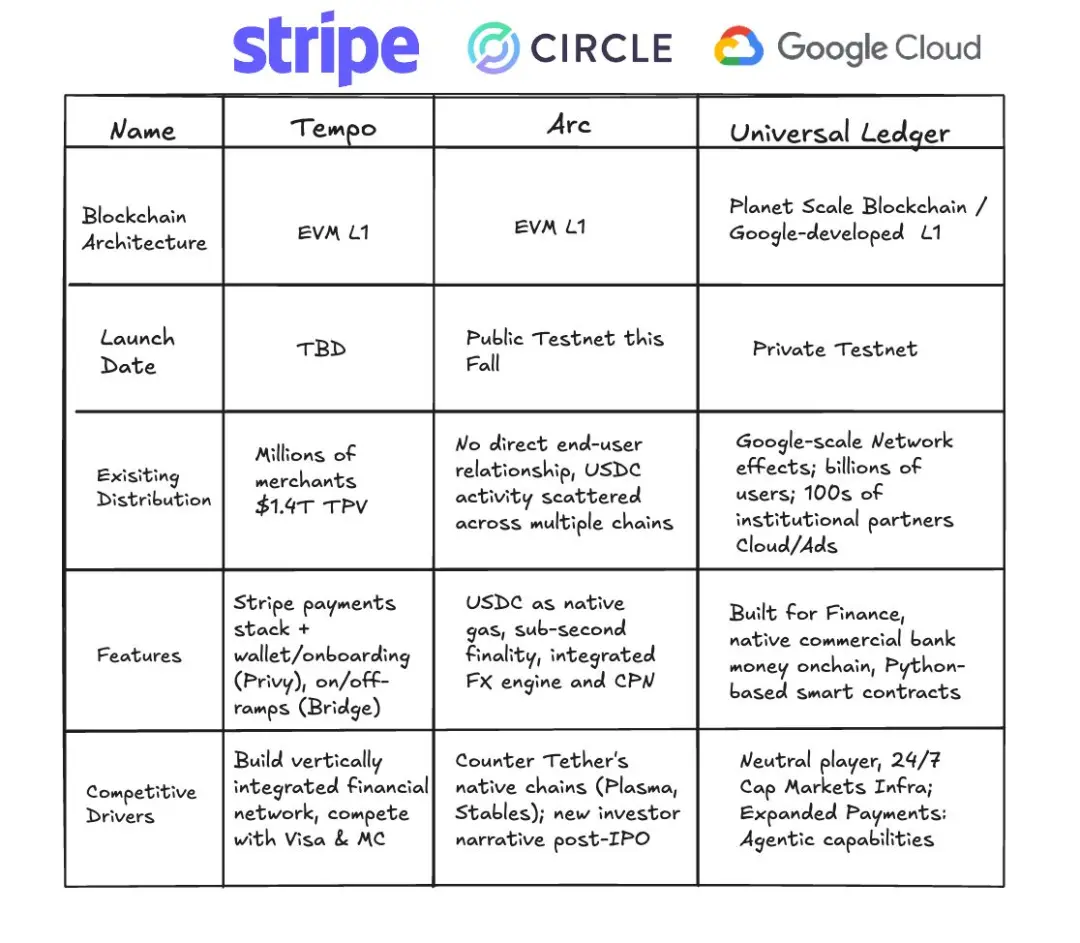

Arc

On August 12, 2025, Circle announced its stablecoin and payments-focused Layer 1 blockchain—Arc—would enter private testnet in the coming weeks, launch public testnet in autumn 2025, and target a mainnet beta launch in 2026.

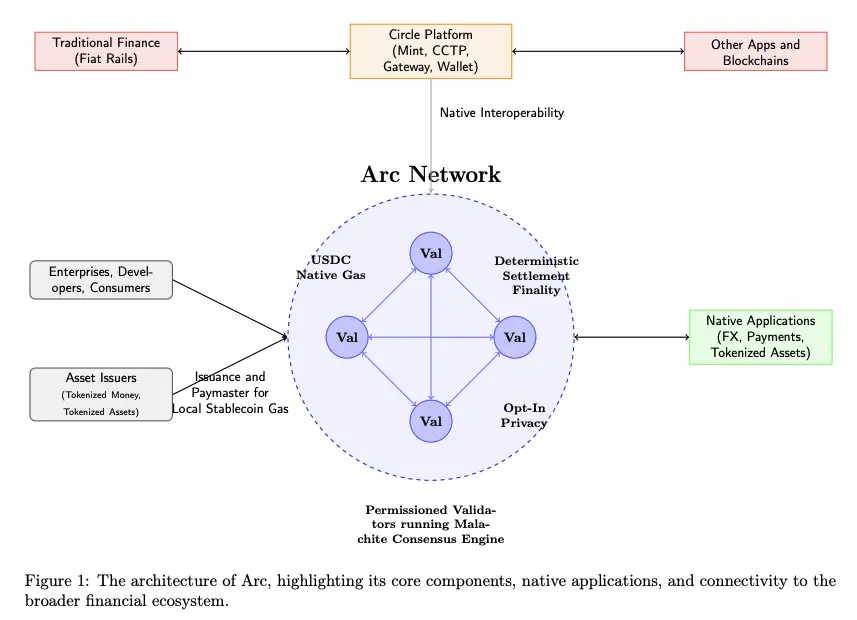

Arc’s key features include: operation by a permissioned validator set (running the Malachite BFT consensus engine) providing deterministic finality; native gas fees paid in USDC; and an optional privacy layer.

▲ source: Arc Litepaper

Arc is deeply integrated into Circle’s entire ecosystem platform—including Mint, CCTP, Gateway, and Wallet—enabling seamless value flow between Arc, traditional fiat rails, and other blockchains. Enterprises, developers, and consumers will transact via apps on Arc (covering payments, FX, asset tokenization, etc.), while asset issuers can mint assets on Arc and act as paymasters to sponsor gas fees for their users.

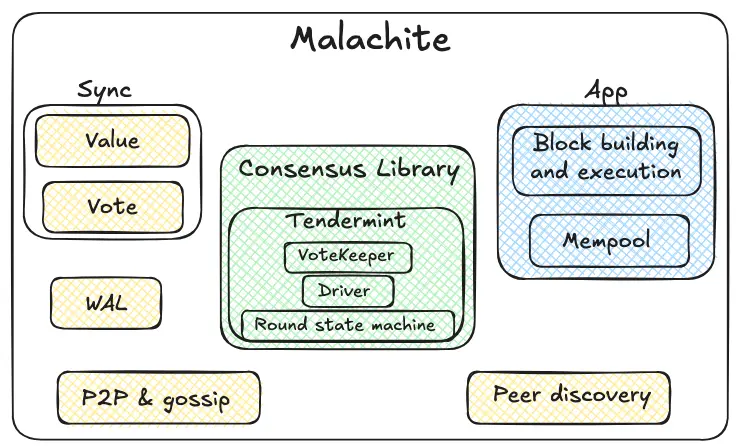

Arc uses a consensus engine called Malachite, based on a permissioned Proof-of-Authority mechanism, with validator nodes operated by known authoritative entities.

▲ source: Circle

Malachite is a Byzantine fault-tolerant consensus engine, allowing applications to embed it for strong consistency and finality across independent nodes.

The green-highlighted consensus library is Malachite’s core. Its internal round state machine follows a Tendermint-style round process (propose → pre-vote → pre-commit → commit). The vote guardian aggregates votes and tracks quorum. The driver coordinates rounds over time, ensuring protocol progress even if some nodes are delayed or fail. The library is deliberately designed to be generic—abstractly handling “values” so various application types can plug in.

Surrounding the core module are yellow-highlighted reliability and networking components. Peer-to-peer and gossip protocols transmit proposals and votes between nodes; node discovery maintains connections. Write-ahead logs persist critical events locally, preserving safety after crashes. The sync mechanism offers dual paths—value sync and vote sync—allowing lagging nodes to catch up either by fetching finalized outputs or by retrieving missing intermediate votes needed to complete pending decisions.

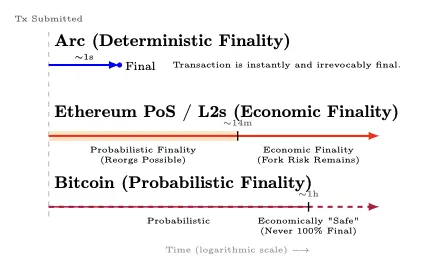

Arc delivers ~1-second deterministic finality—once ≥2/3 validators confirm, transactions are irreversibly finalized (no reorg risk). Ethereum PoS and its L2s achieve economic finality in ~12 minutes, transitioning from a probabilistic phase to “economic finality”; Bitcoin exhibits probabilistic finality—requiring ~1 hour (multiple confirmations) to reach “economic safety,” though mathematical 100% finality is never achieved.

▲ source: Arc Litepaper

Once ≥⅔ validators confirm a transaction, it transitions from “unconfirmed” to 100% final (with no “reorg probability tail”). This satisfies Principle 8 of the Principles for Financial Market Infrastructures (PFMI)—explicit final settlement.

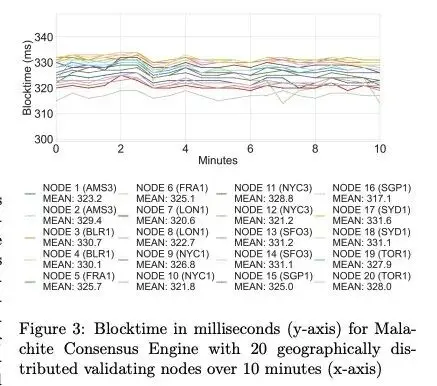

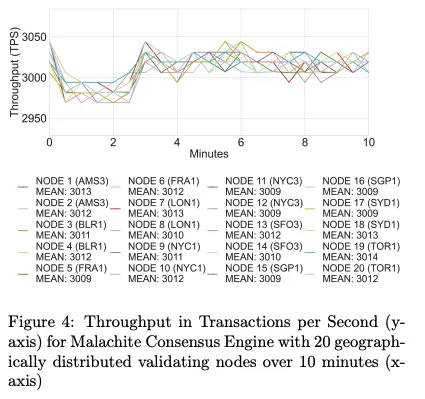

In performance, Arc achieves ~3,000 TPS with sub-350ms finality latency across 20 geographically distributed validators; with 4 such validators, it exceeds 10,000 TPS with sub-100ms finality.

▲ source: Arc Litepaper

▲ source: Arc Litepaper

Planned upgrades to the Malachite consensus engine include multi-proposer support (projected to boost throughput ~10x) and optional lower fault-tolerance configurations (projected to reduce latency ~30%).

Arc also introduces an optional confidential transfer feature for compliant payments: transaction amounts are hidden while addresses remain visible; authorized parties can access transaction values via selectively disclosed “view keys.” The goal is “auditable privacy”—suitable for banks and enterprises needing on-chain confidentiality without sacrificing compliance, reporting duties, or dispute resolution.

Arc’s design choices emphasize institutional predictability and deep integration with Circle’s tech stack—but these come with trade-offs: the permissioned PoA validator set centralizes governance and censorship power among known institutions, and BFT systems tend to halt rather than fork during network partitions or validator failures. Critics argue Arc resembles a bank-focused walled garden or consortium chain rather than a trust-minimized public network.

Yet this trade-off is clear and rational for enterprise needs: banks, payment providers, and fintechs prioritize deterministic outcomes and auditability over maximal decentralization and permissionlessness. Long-term, Circle has indicated a path toward permissioned proof-of-stake, opening participation to qualified stakers under slashing and rotation rules.

With USDC as native gas, institutional-grade quoting/FX engines, sub-second deterministic finality, optional privacy, and deep integration with Circle’s full-stack products, Arc packages the core capabilities enterprises actually need into a complete payment rail.

Stablecoin Rail Wars

Plasma, Stable, and Arc are not simply three competitors in a race—they represent distinct paths toward the same vision: enabling the dollar to move as freely as information. Viewed holistically, the true battlegrounds emerge: issuer camps (USDT vs. USDC), distribution moats on existing chains, and permissioned rails reshaping enterprise expectations.

Issuer Camps: USDT vs. USDC

We are witnessing two parallel races: competition among blockchains and rivalry among issuers. Plasma and Stable are clearly USDT-first, while Arc belongs to Circle (issuer of USDC). With PayPal Ventures investing in Stable, more issuers are entering—each vying for distribution channels. In this process, issuers will shape the go-to-market strategies, target regions, ecosystem roles, and overall direction of these stablecoin blockchains.

Though Plasma and Stable may pursue different market paths and initial targets, both ultimately anchor in markets where USDT already dominates.

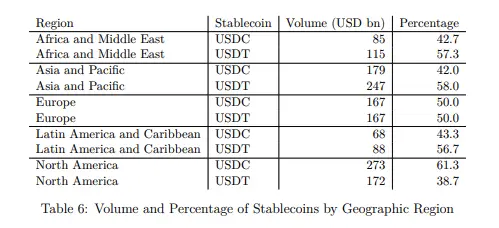

Tether’s USDT performs stronger in regions with more emerging markets, while Circle’s USDC is more prevalent in Europe and North America. Note that this study covers only EVM chains (Ethereum, BNB Chain, Optimism, Arbitrum, Base, Linea), excluding Tron—a major omission given Tron’s massive USDT volume—suggesting USDT’s real-world footprint is likely underestimated.

▲ source: Decrypting Crypto: How to Estimate International Stablecoin Flows

Beyond regional focus, issuers’ strategic choices are reshaping their ecosystem roles—and consequently influencing stablecoin blockchain priorities. Historically, Circle built a more vertically integrated tech stack (wallet, payments, cross-chain), while Tether focused on issuance/liquidity and relied more on ecosystem partners. This divergence now creates space for USDT-focused chains (e.g., Stable and Plasma) to build more of the value chain themselves. Meanwhile, USDT0’s design aims to unify USDT liquidity across chains.

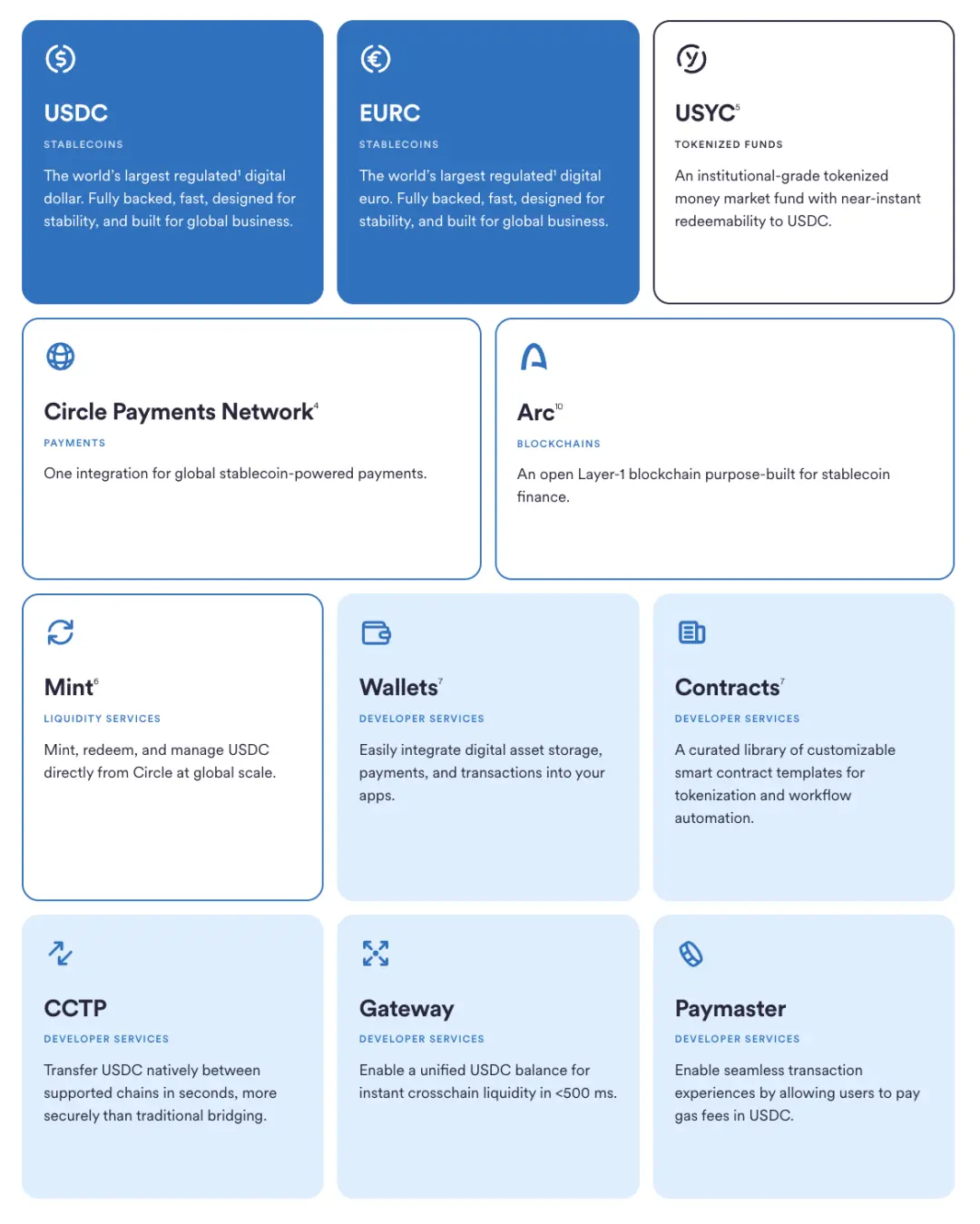

Circle’s ecosystem development has been deliberate and cumulative: starting with USDC issuance and governance, reclaiming control by dissolving Centre and launching programmable wallets, then introducing CCTP to shift from bridge dependency to native burn-and-mint transfers—unifying cross-chain USDC liquidity. With the Circle Payments Network, it connected on-chain value to off-chain commerce. Arc is the latest move in this strategy. Flanking these pillars are services for issuers and developers—Mint, Contracts, Gateway, and Paymaster (gas priced in USDC)—reducing third-party dependencies and tightening the feedback loop between product and distribution.

▲ source: Circle

Response Strategies from Existing Chains

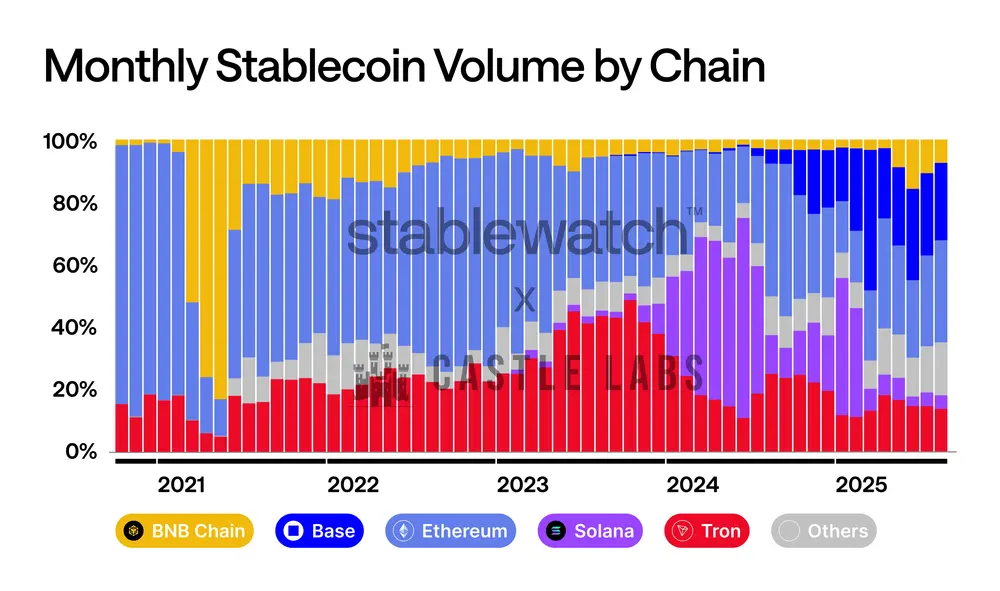

Competition for stablecoin transaction volume has always been fierce. The shifting landscape is clear: early dominance by Ethereum, followed by Tron’s rise, Solana’s surge in 2024, and recently Base gaining momentum. No chain holds permanent supremacy—even the deepest moats face monthly share battles. With dedicated stablecoin chains entering, competition will intensify, but incumbents won’t cede ground easily. Expect aggressive moves on fees, finality, wallet UX, and fiat ramp integration to defend and grow their stablecoin volumes.

▲ source: Stablewatch

Major chains are already acting:

-

BNB Chain launched a “zero-fee carnival” in Q3 2024, partnering with wallets, centralized exchanges, and bridges to fully waive USDT and USDC transfer fees—extended through August 31, 2025.

-

Tron took a similar route: its governance body approved lowering network “energy” unit prices and plans to roll out a “gasless” stablecoin transfer scheme in Q4 2024, reinforcing its positioning as a low-cost stablecoin settlement layer.

-

TON charted a different course, hiding complexity entirely within the Telegram interface. Users experience USDT transfers to contacts as “zero-fee” (costs absorbed internally by Telegram Wallet within its closed system), only paying normal network fees when withdrawing to open public chains.

-

Ethereum L2s focus on structural upgrades over short-term promotions. The Dencun upgrade’s blob space drastically reduced Rollup data availability costs, enabling them to pass savings to users. Since March 2024, L2 fees have dropped significantly.

Permissioned Rails

Alongside public chains, another track is accelerating: permissioned ledgers built for banks, market infrastructures, and large enterprises.

The most watched newcomer is Google Cloud Universal Ledger (GCUL)—a permissioned Layer 1. Google states its target use cases are wholesale payments and asset tokenization. Though public details are scarce, its lead describes it as a neutral, bank-grade chain, with CME Group completing preliminary integration tests. GCUL is a non-EVM chain developed in-house by Google, running on Google Cloud infrastructure, with Python smart contracts. Far from a public chain, its model relies on trust in Google and regulated nodes.

▲ source:

https://www.linkedin.com/posts/rich-widmann-a816a54b_all-this-talk-of-layer-1-blockchains-has-activity-7366124738848415744-7idA

If GCUL is a single cloud-hosted rail, Canton Network adopts a “network of networks” model. Built around Digital Asset’s Daml smart contract stack, it connects independently governed applications, enabling synchronized movement of assets, data, and cash across domains—while maintaining fine-grained privacy and compliance controls. Its participant list includes numerous banks, exchanges, and market operators.

HSBC Orion (HSBC’s digital bond platform) has been live since 2023, hosting the European Investment Bank’s first pound-denominated digital bond—issuing £50 million via a hybrid private-public chain setup under Luxembourg’s DLT framework.

In payments, JPM Coin has offered institutional value transfer since 2020, enabling programmable intraday cash flows on JPMorgan-operated rails. In late 2024, the bank restructured its blockchain and tokenization offerings into Kinexys.

The unifying thread across these efforts is pragmatism: preserving regulatory safeguards and clear governance while adopting the best of public chain design. Whether delivered via cloud services (GCUL), interoperability protocols (Canton), productized issuance platforms (Orion), or bank-run payment rails (JPM Coin/Kinexys), permissioned ledgers converge on one promise: faster, auditable settlement under institutional control.

Conclusion

Stablecoins have crossed the threshold from crypto niche to payment network scale. The resulting economic implications are profound: when the cost of moving a dollar approaches zero, profit margins from transferring money vanish. The center of gravity shifts to the value delivered around stablecoin transfers.

The relationship between stablecoin issuers and blockchains is increasingly becoming an economic tug-of-war over reserve yield capture. As seen in Hyperliquid’s USDH case, stablecoin deposits generate ~$200 million annually in Treasury yields—flows that go to Circle, not Hyperliquid’s own ecosystem. By issuing USDH and adopting Native Markets’ 50/50 split model—half used to buy back HYPE tokens via a grant fund, half for ecosystem growth—Hyperliquid “internalized” this revenue. This may signal another evolution beyond “stablecoin chains”: existing networks issuing their own stablecoins to capture value. Sustainable models will be ecosystems where issuers and chains share economic benefits.

Looking ahead, auditable private payments will gradually become standard for payroll, treasury management, and cross-border flows—not achieved by building a “fully anonymous privacy chain,” but by hiding transaction amounts while keeping counterparty addresses visible and auditable. Stable, Plasma, and Arc all adopt this model: offering enterprises privacy with selective disclosure, compliance interfaces, and predictable settlement—achieving “private when needed, transparent when required.”

We’ll see stablecoin/payment chains introduce more enterprise-tailored features. Stable’s “guaranteed blockspace” is a prime example: a reserved capacity channel ensuring payroll, treasury, and cross-border payments settle with stable latency and cost even during traffic peaks. It’s like cloud reserved instances—but for on-chain settlement.

With next-gen stablecoin/payment chains emerging, new opportunities for applications will unlock. We’ve already seen strong DeFi momentum on Plasma and consumer-facing frontends like Stable Pay and Plasma One—but the bigger wave is ahead: digital banks and payment apps, smart agent wallets, QR payment tools, on-chain credit, risk scoring, and a new class of yield-bearing stablecoins and financial products built around them.

The era where the dollar moves as freely as information is arriving.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News