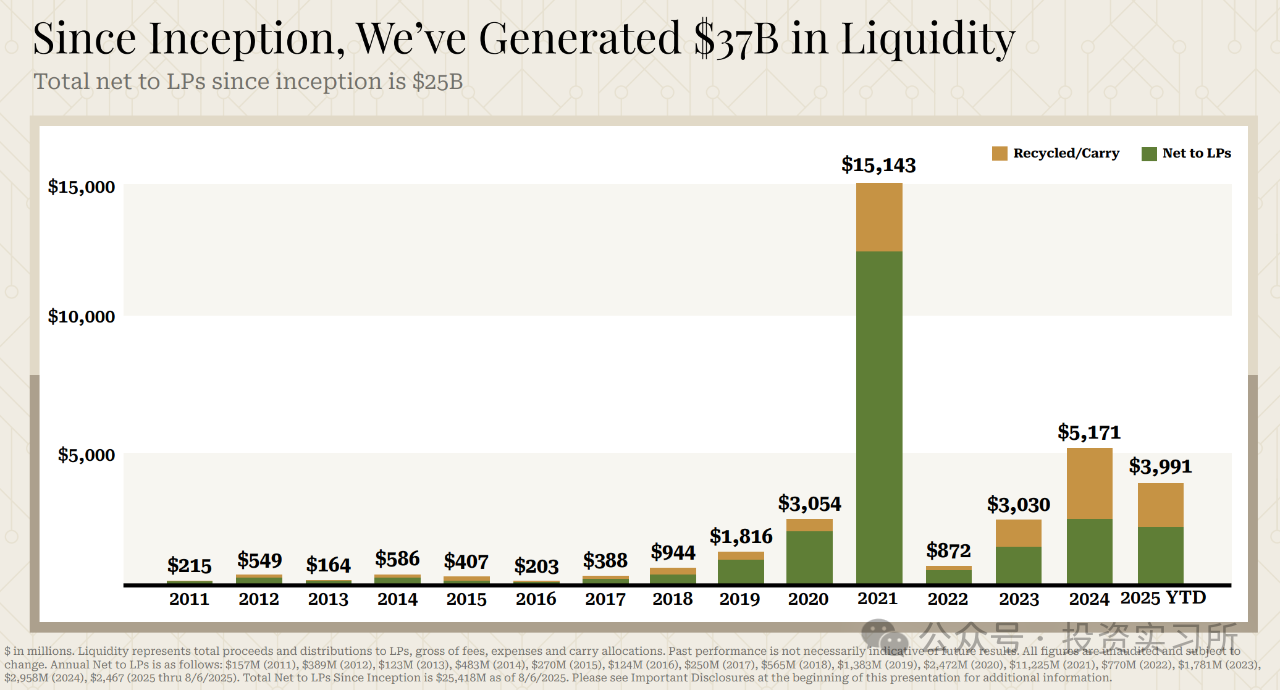

a16z has delivered $25 billion in net returns to LPs, with 4 minimalist but profitable products

TechFlow Selected TechFlow Selected

a16z has delivered $25 billion in net returns to LPs, with 4 minimalist but profitable products

The idea that non-consensus investments are where alpha lies is actually quite dangerous in the early stages, as subsequent capital tends to become increasingly consensus-driven.

a16z has become a highly unique player in the VC industry, but it's actually drifted quite far from traditional venture capital. Its scale continues to grow—after raising $7.2 billion last year (a16z's new fund raised $7.2B beyond target, signaling a shift in investment paradigms), they plan to raise another $20 billion this year, focusing heavily on AI.

Recently leaked slides show that since its founding in 2009, a16z has delivered $25 billion in net returns to LPs, with $11.2 billion of that coming in 2021 alone. 2021 was the peak of the SaaS wave, and a16z emerged as the biggest winner of that bubble.

I did a quick check: a16z’s largest exits in 2021 included:

-

Coinbase IPO: a16z first led Coinbase’s Series B round (around $20 million) at the end of 2013 and participated in multiple follow-on rounds. At IPO, Coinbase had a market cap of about $85.8 billion. a16z held approximately 25% of Class A shares and 14.8% of Class B shares, cashing out around $4.475 billion upon listing (retaining ~7% stake), yielding over $7 billion in profit.

-

Robinhood IPO: a16z participated in Robinhood’s seed round back in 2013 (co-investing $16 million with Ribbit and others).

-

Roblox IPO: valued at around $42.6 billion at IPO. In February 2020, a16z led Roblox’s $150 million Series G round, securing around 5% equity.

-

Marqeta (payment card issuance platform) IPO: valued at approximately $15 billion at IPO. a16z participated in multiple funding rounds.

-

Stack Overflow acquired by Prosus for about $1.8 billion. a16z led Stack Overflow’s Series D round in 2015.

-

Affirm IPO: valued at around $11.7 billion at IPO. a16z participated in Affirm’s $100 million Series D round in April 2016.

According to GP Leslie Feinzaig, if you sum up all of a16z’s fund fees under standard industry terms (2% management fee and 20% carry), their annual management fees alone would reach $700 million this year—excluding carry, which would make it even higher.

However, according to Erick Schonfeld, former editor-in-chief of TechCrunch, a16z’s fee caps are not 2% and 20%, but rather 3% and 30%, meaning they charge significantly more.

Leslie Feinzaig argues that these large VCs are no longer true venture capitalists. First, legally speaking, firms like a16z, Sequoia, Insight, General Catalyst, Thrive Capital, and Lightspeed aren’t pure VCs—they are registered investment advisors (RIAs).

Second, their investment strategies have diverged greatly from those of traditional VCs. True VCs historically pursued early-stage companies with alpha potential—high risk, high reward, emphasizing contrarian, non-consensus bets.

But a16z’s approach is entirely different. Martin Casado, a16z GP leading AI investments, recently posted a widely discussed tweet stating that large funds now favor consensus investing over contrarian bets. In early-stage investing, having the courage to back "non-consensus" ideas isn't enough—you must also have the foresight to judge whether that "non-consensus" point can eventually trigger broad market "consensus":

The idea that non-consensus investing equals alpha is actually quite dangerous in early stages, as follow-on capital increasingly trends toward consensus.

Turner Novak, founder of Banana Capital, offers a vivid analogy that reflects current market reality: massive capital flooding into top-tier startups already tells the story.

Even ignoring large models like OpenAI or Anthropic, AI applications such as Cursor are reportedly raising new funds at starting valuations as high as $20 billion, driven by early investors already achieving partial exits in secondary markets at that valuation.

Leslie Feinzaig labels giant VCs like a16z as "Consensus Capital," characterized by the following:

-

Focusing exclusively on massive returns—forget unicorns, they’re chasing trillion-dollar outcomes;

-

Believing only one type of founder can achieve such results—what she calls the "consensus" founder;

-

Being completely price-insensitive toward this founder type, willing to pay premium prices at very early stages;

-

Operating massive funds capable of deploying tens or even hundreds of millions in a single early round.

Consensus capital flows to founders with highly distinctive, predictable backgrounds: graduates from a handful of elite schools, employees at a few select startups, or contributors at a small number of AI labs. They’re easy to spot—you could literally build an AI agent to identify them before they raise. Leslie Feinzaig says many consensus investors already do exactly that.

If you’re one of these founders, raising from consensus capital should be effortless. Multiple funds will fiercely compete, driving up your valuation and effectively erasing any alpha in their own portfolios.

If you’re not this founder type, it may be harder. But there are still plenty of alpha-seeking early-stage investors—true VCs—and once your business gains traction, consensus capital will eventually follow.

For ordinary developers, targeting minimal, narrowly-defined needs can still yield solid returns. Recently I’ve seen several products with extremely simple, seemingly insignificant functions that nonetheless generate strong revenue. Some use cases have given me real inspiration. They don’t rely on complex algorithms or large teams, but precisely solve...

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News