Will stablecoins take the baton from electronic payments to bring about the next decade's economic boom?

TechFlow Selected TechFlow Selected

Will stablecoins take the baton from electronic payments to bring about the next decade's economic boom?

Stablecoins are quietly increasing the velocity of money: changing the frequency of capital use, the direction of flows, and the speed at which economic activity is stimulated.

Author: Level

Translation: AididiaoJP, Foresight News

Stablecoins are reshaping the foundational architecture of the global financial system. As a new form of digital asset, their core value manifests in three dimensions: programmability at the technical level enables integration into smart contracts for automatic execution; borderless nature at the geographical level breaks down regional barriers of traditional finance; and high efficiency accelerates settlement times from traditional finance’s T+1 or even T+3 to near-instantaneous.

However, beyond payment functionality, stablecoins are quietly increasing the velocity of money: changing how frequently each dollar is used, its direction of flow, and the speed at which it stimulates economic activity. The impact of stablecoins on money velocity exhibits a unique "double helix" effect: on one hand, automated clearing via smart contracts releases settlement collateral that would otherwise sit idle in traditional finance; on the other, 7×24 global liquidity pools significantly improve capital turnover efficiency—an effect particularly evident in cross-border B2B transactions.

This phenomenon mirrors the transformation the internet brought two decades ago to early forms of monetary and value circulation. While electronic payments primarily optimized payment efficiency, stablecoins go further by reconstructing the entire closed loop of value storage, transfer, and creation atop enhanced efficiency. To understand the current role of stablecoins, we must return to fundamental concepts.

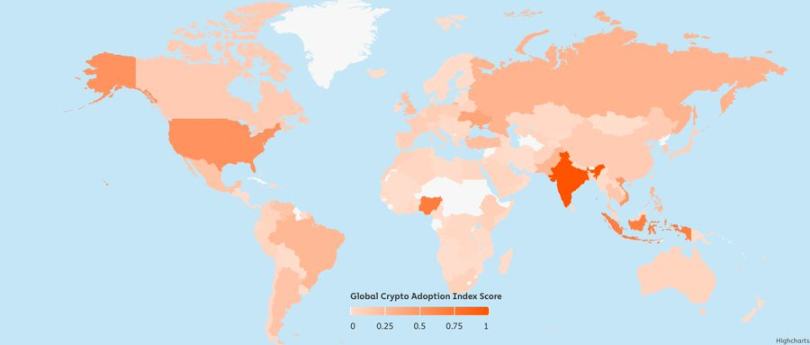

Note: In 2024, Chainalysis' Global Cryptocurrency Adoption Index ranked 151 countries using four sub-indicators measuring usage across various cryptocurrency services. Rankings were adjusted for population and purchasing power parity, averaged, and normalized to a 0–1 range. Data is based on transaction volume estimates derived from traffic to cryptocurrency service websites and cross-verified with local expert research.

Definition of Money Velocity

Money velocity refers to the rate at which money exchanges hands within an economy, typically calculated using the following formula:

Velocity = Gross Domestic Product (GDP) / Money Supply

It measures the productivity of each unit of currency. High velocity indicates frequent use of money in purchasing goods and services; low velocity suggests money is being saved or held idle.

But "money" is not a single concept. Economists categorize it into different layers:

-

M1: Cash + demand deposits, the most liquid form of money.

-

M2: M1 + savings accounts + time deposits under $100,000 + money market funds.

-

M3 (discontinued in the U.S.): M2 + large time deposits + institutional money market funds + other large-scale financial instruments.

Fully fiat-backed stablecoins that are instantly redeemable behave similarly to M1: highly liquid and immediately usable.

The Internet Era and Fluctuations in Money Velocity

From the late 1990s to the early 2000s, the rise of the internet significantly increased money velocity:

-

E-commerce enabled comprehensive消费升级 (consumer upgrade).

-

Email accelerated transactions and contract signing.

-

Market access became globalized.

-

Digital banking made money more liquid.

This early efficiency boost drove growth in M1 velocity.

Yet as the internet matured, another trend took dominance:

-

Capital appreciation created massive wealth.

-

This wealth was saved and invested in stocks, bonds, and real estate.

-

More funds were allocated to investment rather than consumption.

Velocity slowed, yet GDP continued to grow, as capital formation gradually replaced pure consumption.

Annual growth trends of M3 money supply and S&P 500 Index

How Stablecoins Increase Global Money Velocity

Today, stablecoins are introducing a similar dynamic: they greatly enhance the speed, accessibility, and usability of money. But unlike the early internet, this transformation is global from the outset. Here's how it unfolds:

1. 24/7 Borderless Transfers

In cross-border payments, stablecoins enable instant settlement around the clock. Issuers like Circle and Tether have built global payment networks, freeing fund transfers from traditional banking hours and cross-border restrictions. This efficiency gain is especially pronounced in remittances—transfers that traditionally take 3–5 business days can be completed in minutes via stablecoins.

2. On-chain Finance and DeFi

The development of decentralized finance (DeFi) further amplifies the economic value of stablecoins. On platforms like Aave and Compound, stablecoin holders can participate in lending markets, turning idle funds into productive capital. This improved capital utilization directly accelerates money velocity. Platforms such as Morpho Labs and Pendle allow users to deploy stablecoins in lending, yield products, or liquidity provision.

3. Remittances and Payments

APIs developed by startups like Stablecoin enable businesses to integrate stablecoin payments into existing cash flows, supporting 24/7 global instant settlement, reducing foreign exchange costs, and reaching markets underserved by traditional finance.

Another example is crypto debit cards, which let users spend their on-chain stablecoin balances directly in daily life. By connecting with major payment networks like Visa and Mastercard, these cards instantly convert stablecoins into local currency at point-of-sale without additional steps. This bridge between on-chain and real-world usage makes stablecoins active mediums for purchasing groceries, travel, and other daily needs, thereby boosting global money velocity.

4. Permissionless Access to the U.S. Dollar

In countries like Turkey, Argentina, and Nigeria, stablecoins serve as vital financial tools, allowing users to store USD value and transact freely with just a smartphone and internet connection. By reducing reliance on intermediaries and enabling instant, borderless payments, stablecoins more efficiently activate local capital and bring more participants into the economic system.

For small and medium enterprises—whether in manufacturing, agriculture, digital services, or local retail—stablecoins connect international buyers and suppliers directly, reduce friction in cross-border trade, eliminate settlement delays, and protect businesses from sudden local currency depreciation. Stablecoins help individuals and firms keep capital circulating within the local economy, accelerating money velocity while enhancing economic resilience in high-volatility currency environments.

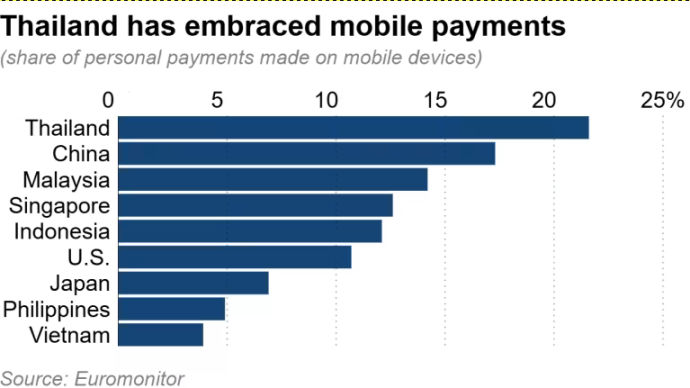

Stablecoin Adoption in Southeast Asia

In emerging markets like Thailand, Vietnam, and the Philippines, stablecoin adoption is accelerating through P2P and OTC channels. For instance, Thailand’s Siam Commercial Bank (SCB), through its innovation arm SCB 10X, partnered with Lightnet to enable cross-border payments and remittances using stablecoins on public blockchains. This marks Thailand’s first stablecoin-based settlement case, setting a benchmark for the regional financial industry. By integrating Fireblocks’ custody infrastructure, the service ensures institutional-grade asset security, building trust among participants. Going forward, SCB and Lightnet plan to extend the service to corporate clients, enable two-way remittances, and offer retail users the same efficiency and cost advantages.

Euromonitor mobile payment data

Short-term Impact: Enhanced Economic Efficiency

In the short term, the increase in money velocity driven by stablecoins brings significant economic benefits:

-

GDP growth: faster circulation of the same capital pool stimulates economic activity.

-

Increased productivity: instant, low-friction payments and faster working capital cycles optimize business efficiency.

-

Greater financial inclusion: gig workers, creators, and merchants can transact using stable USD assets without relying on traditional banks.

This unlocks long-suppressed economic potential in emerging markets. Just as the early internet accelerated commerce by removing friction in communication and distribution, stablecoins are doing the same for value transfer—enabling funds to move freely, around the clock, and at near-zero cost.

Long-term Impact: From Speed to Scale

The long-term effects are more complex.

As users in emerging markets gain access to dollars and stablecoins, some capital is not spent but instead saved or invested:

-

Staked in DeFi for passive income.

-

Used to purchase assets (real estate, tokens, stocks).

-

Reserved for business expansion.

These behaviors remove funds from short-term transaction cycles, reducing local velocity. But this is not a negative outcome. Similar to the early 2000s, it reflects a shift from velocity-driven consumption to wealth accumulation and capital formation—a sign of economic maturity.

Even as turnover frequency declines, capital use becomes more efficient. In early growth stages, emerging economies lean toward consumption, focusing on infrastructure and catching up with advanced economies. As incomes rise and financial tools become widespread, savings rates gradually increase, and households begin accumulating wealth and investing in long-term assets. Stablecoins can accelerate this transition.

Conclusion

Stablecoins are transforming how global capital flows, enhancing both transaction speed and financial inclusion. In the short term, they act as catalysts for money velocity; in the long term, they serve as builders of capital formation.

Money velocity, a key indicator of economic vitality, is calculated as the ratio of GDP to money supply. The emergence of stablecoins infuses new meaning into this traditional economic concept. Fully fiat-backed, instantly redeemable stablecoins exhibit liquidity characteristics similar to M1, yet operate with far greater efficiency than traditional fiat currencies.

It should be noted that velocity does not operate in isolation—its economic impact depends on several factors:

-

Interest rates: higher rates encourage saving, reducing velocity.

-

Inflation expectations: if price increases are anticipated, people tend to spend faster.

-

Tariffs and capital controls: these may limit stablecoin usage in specific regions.

-

Fiscal policy: government transfers, taxes, and subsidies all influence money velocity.

Nonetheless, the result is the emergence of a new form of global economy: one where money moves instantly, settles automatically, and remains stable throughout development. Just as the early internet reshaped communication and commerce, stablecoins are doing the same to money itself. This transformation is not about printing more money, but about using existing resources more efficiently.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News