Crossing the chasm, "crypto-related" enterprises will replace "crypto-native" projects in going mainstream

TechFlow Selected TechFlow Selected

Crossing the chasm, "crypto-related" enterprises will replace "crypto-native" projects in going mainstream

As the crypto industry gradually matures and develops steadily, successful founders of crypto-related projects will also emerge.

Author: Richard Chen

Translation: Tim, PANews

It's 2025, and cryptocurrency is going mainstream. The GENIUS Act has officially been signed into law, giving us a clear regulatory framework for stablecoins at last. Traditional financial institutions are embracing crypto en masse. Crypto has won!

As crypto crosses the chasm, this shift carries profound implications for early-stage VCs: we're now seeing crypto-related projects gradually surpassing crypto-native ones. "Crypto-native" refers to projects built by crypto experts for the internal crypto ecosystem, while "crypto-related" refers to applications of crypto technology by mainstream industries. This is the first time in my career I've witnessed such a transition, and this article aims to deeply explore the core differences between building crypto-native versus crypto-related projects.

Building for Crypto-Native

The most successful crypto products to date have almost all been built for crypto-native users: Hyperliquid, Uniswap, Ethena, Aave, and others. Like any niche cultural movement, crypto technology is so far ahead of its time that average users outside the space struggle to "get it," let alone become passionate daily active users. Only those crypto-native players on the front lines possess the risk tolerance and dedication needed to test every new product and survive through hacks, rug pulls, and other dangers.

Traditional Silicon Valley VCs once rejected crypto-native projects, arguing their total addressable market was too small—a fair point, given how early the space was. On-chain applications were few, and the term "DeFi" wasn't even coined until October 2018 in a group chat in San Francisco. But you had to bet on faith, hoping macro tailwinds would eventually propel the crypto-native market to scale. And indeed, fueled by the liquidity mining frenzy of DeFi Summer 2020 and zero interest rates in 2021, the crypto-native market expanded exponentially. Suddenly, every Silicon Valley VC rushed into crypto, asking me for advice to catch up on four years of missed learning.

Even today, the total serviceable market size of crypto-native users remains limited compared to traditional non-crypto markets. I estimate the number of Twitter users in crypto is at most in the tens of thousands. Therefore, to achieve nine-figure annual recurring revenue (ARR), average revenue per user (ARPU) must remain extremely high. This leads to a critical conclusion:

Crypto-native projects are built entirely for experts.

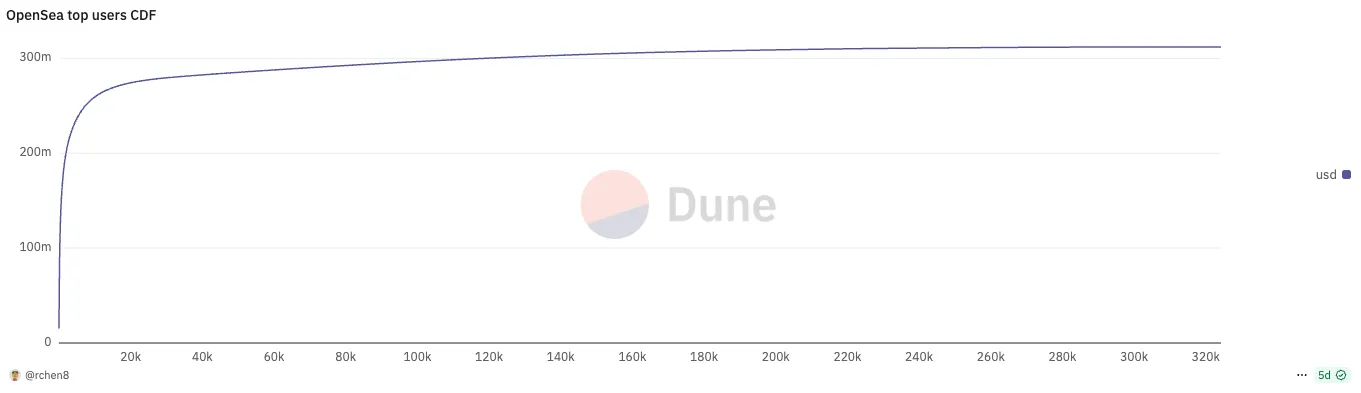

Every successful crypto-native product follows an extreme power-law distribution in user behavior. Last month, the top 737 users on OpenSea—just 0.2% of users—accounted for half of the platform’s total trading volume. Similarly, the top 196 users on Polymarket—only 0.06%—generated 50% of the platform’s volume!

As a founder of a crypto project, what should keep you awake at night is not chasing user growth, but retaining your top-tier core users—an idea starkly opposed to Silicon Valley’s traditional obsession with daily active users (DAU).

User retention in crypto has always been challenging. Top users are often purely incentive-driven and easily poached. This allows new competitors to steal just a few key users and suddenly emerge, eroding your market share—just like the battles between Blur and OpenSea, Axiom and Photon, or LetsBonk and Pump.fun.

In short, compared to Web2, crypto projects have much shallower moats. With all code open-source and projects easy to fork, native crypto projects are often short-lived, rarely surviving beyond one market cycle—and sometimes only lasting months. Founders who get rich post-TGE often choose to retire early, turning to angel investing as a side hobby.

The only way to retain core users is continuous product innovation and staying one step ahead of competitors. Uniswap has endured seven years of fierce competition largely because it consistently delivers breakthrough innovations—from V3 concentrated liquidity and UniswapX to Unichain and V4 hooks—meeting the evolving needs of its core users. This is especially impressive given that decentralized exchanges are arguably the most brutally competitive sector of all.

Building for Crypto-Related

There have been many attempts to apply blockchain technology to broader real-world markets—such as supply chain management or interbank payments—but they failed due to premature timing. Fortune 500 companies experimented with blockchain in innovation labs but never seriously scaled it into production. Remember the buzzwords? "Blockchain, not Bitcoin," "distributed ledger technology," and so on.

Now we’re seeing a complete shift in attitude from major traditional institutions. Banks and corporations are launching their own stablecoins, and regulatory clarity during the Trump administration opened the door for crypto’s mainstream adoption. Crypto is no longer an unregulated financial frontier.

In my career, this is the first time I’m seeing more crypto-related projects emerging than crypto-native ones. And there’s good reason: the biggest success stories over the next few years are likely to be crypto-related rather than crypto-native. IPOs are scaling into hundreds of billions in size, while TGEs are typically capped at several billion to tens of billions. Examples of crypto-related projects include:

-

Fintech companies using stablecoins for cross-border payments

-

Robotics companies using DePIN incentives for data collection

-

Consumer companies using zkTLS to authenticate private data

The common pattern here is: crypto is just a feature, not the product itself.

For industries heavily relying on crypto technology, expert users still matter—but the extreme concentration is less pronounced. When crypto is merely a feature, success rarely hinges on the crypto tech itself, but more on whether founders possess deep domain expertise and understand core industry dynamics. This is evident in fintech.

The essence of fintech lies in user acquisition with strong unit economics (customer acquisition cost vs. lifetime value). Today’s emerging crypto fintech startups live in fear that established non-crypto fintech giants—with larger user bases—could simply add crypto as a module and crush them, or drive up customer acquisition costs to uncompetitive levels. Unlike pure crypto projects, these startups can’t rely on launching hyped tokens to sustain operations.

Ironically, crypto payments has long been an ignored space—I said so in my 2023 Permissionless talk! But the golden era for founding crypto fintech companies was before 2023, when pioneers could build distribution networks early. Now, as Stripe acquires Bridge, native crypto founders are shifting from DeFi into payments—but they’ll ultimately be outcompeted by former Revolut employees who truly understand fintech mechanics.

What does "crypto-related" mean for crypto VCs? The key is to avoid reverse selection—don’t become a fallback option for founders rejected by domain-specific VCs. Much reverse selection comes from backing native crypto founders who recently pivoted into "crypto-related" spaces. A harsh truth: generally, crypto founders are Web2 losers (though the top 10% are exceptional).

Crypto venture firms have historically found value in overlooked founders outside Silicon Valley’s networks—those without elite pedigrees (like Stanford or Stripe experience) or polished pitch skills, but who deeply understand crypto-native culture and know how to rally passionate online communities. When Hayden Adams was laid off from Siemens as a mechanical engineer, he built Uniswap just to learn Vyper; Stani Kulechov started building Aave (originally ETHLend) while finishing his law degree in Finland.

Successful founders of crypto-related projects will contrast sharply with those of crypto-native projects. They won’t be wild west financial cowboys who master speculator psychology and build personal cults around their token ecosystems. Instead, they’ll be more mature, business-savvy founders, typically from the relevant domain, with unique go-to-market strategies for user reach. As the crypto industry matures steadily, a new generation of successful founders will rise.

Finally

1. The Telegram ICO in early 2018 vividly illustrated the mental gap between Silicon Valley VCs and crypto-native investors. Firms like Kleiner Perkins, Benchmark, Sequoia, Lightspeed, and Redpoint invested, believing Telegram had the user base and distribution to become a dominant app platform. Nearly all crypto-native VCs passed.

2. My contrarian take on crypto: consumer apps aren’t scarce. In fact, most consumer projects can’t attract VC funding because their revenue models are unstable. These founders shouldn’t seek venture capital—they should bootstrap profitability and cash in quickly during the current consumer wave. They must seize the narrow window of a few months before trends shift to accumulate initial capital.

3. Brazil’s Nubank gained an unfair advantage by pioneering the "fintech" category before the concept was widespread. Crucially, it initially competed only against traditional Brazilian banking giants, not against other emerging fintech startups. With public patience exhausted toward legacy banks, users flocked to Nubank immediately upon launch, giving the company the rare combination of near-zero customer acquisition cost and perfect product-market fit.

4. If you’re building a stablecoin digital bank for emerging markets, why stay in San Francisco or New York? You need to go local and talk to users directly. Surprisingly, this has become the primary filter for spotting viable startups.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News