How much does it cost to launch a stablecoin?

TechFlow Selected TechFlow Selected

How much does it cost to launch a stablecoin?

This is not a startup opportunity for the unprepared.

Author:律动

From Wall Street investment banks to tech companies in Silicon Valley, and from Asia's financial giants to payment platforms, an increasing number of enterprises are setting their sights on the same business—issuing stablecoins.

Thanks to economies of scale, the marginal cost for stablecoin issuers approaches zero. To them, it looks like a risk-free arbitrage game. In today’s global interest rate environment, the spread income is incredibly attractive—by simply depositing users’ U.S. dollars into short-term U.S. Treasuries, stablecoin issuers can earn tens of billions of dollars annually from a steady 4–5% interest spread.

Tether and Circle have already proven this model works. As stablecoin regulations roll out across different regions, compliance pathways are becoming clearer, prompting more and more companies to enter the space—even FinTech giants like PayPal and Stripe are moving quickly. Not to mention, stablecoins naturally integrate with payments, cross-border settlements, and Web3 use cases, offering vast potential.

Stablecoins have become a battleground that every global financial firm must fight for.

But here lies the problem: many only see the seemingly risk-free arbitrage logic behind stablecoins, overlooking the fact that this is actually a capital-intensive, high-barrier business.

If a company wants to legally and compliantly issue a stablecoin, how much would it really cost?

This article breaks down the real costs behind issuing a stablecoin, revealing whether this seemingly effortless arbitrage opportunity is truly worth pursuing.

The Real Costs Behind Stablecoin Issuance

To many, issuing a stablecoin simply means launching a token on-chain—a technically low barrier.

However, launching a stablecoin as a compliant entity serving global users involves organizational structures and system requirements far more complex than imagined. It requires heavy asset investment across multiple dimensions—not just financial licenses and audits, but also fund custody, reserve management, system security, and ongoing operations.

In terms of cost and complexity, the overall setup is comparable to running a mid-sized bank or a regulated trading platform.

The first hurdle for stablecoin issuers is building a compliance framework.

They often need to meet regulatory requirements across multiple jurisdictions, securing key licenses such as the U.S. MSB, New York State BitLicense, EU MiCA, and Singapore VASP. These licenses demand rigorous financial disclosures, anti-money laundering (AML) mechanisms, and ongoing monitoring and reporting obligations.

Compared to mid-sized banks with cross-border payment capabilities, stablecoin issuers typically spend tens of millions of dollars annually on compliance and legal fees just to maintain basic cross-border operating eligibility.

Beyond licenses, setting up KYC/AML systems is also mandatory. Issuers usually need to engage established service providers, compliance consultants, and outsourcing teams to continuously operate customer due diligence, on-chain transaction screening, address blacklist management, and related processes.

In today’s increasingly strict regulatory climate, without robust KYC and transaction review capabilities, gaining market access in major jurisdictions is nearly impossible.

Market analysis suggests that HashKey incurred total costs of HK$20–50 million to apply for Hong Kong’s VASP license, required at least two Responsible Officers (ROs), and had to work with one of the Big Three accounting firms—expenses several times higher than in traditional industries.

Besides compliance, reserve management is another major cost in stablecoin issuance, covering fund custody and liquidity arrangements.

On the surface, a stablecoin’s balance sheet appears simple: users deposit U.S. dollars, and the issuer buys equivalent short-term U.S. Treasuries.

Yet once reserves exceed $1 billion—or even $10 billion—the operational costs rise sharply. Just custody fees alone could reach tens of millions per year; Treasury trading, clearing processes, and liquidity management add further expenses and heavily rely on professional teams and institutional partnerships.

More critically, to ensure seamless “instant redemption” user experience, issuers must maintain sufficient off-chain liquidity to handle large-scale redemptions during extreme market conditions.

This configuration closely resembles the risk reserve mechanisms of traditional money market funds or clearing banks—far more complex than simply locking funds via smart contracts.

To support this infrastructure, issuers must also build highly reliable and auditable technical systems covering critical on-chain and off-chain financial processes. These typically include smart contract deployment, multi-chain minting, cross-chain bridge configurations, wallet whitelisting, settlement systems, node operations, security risk controls, and API integrations.

These systems must not only handle massive transaction volumes and fund flow monitoring but also remain upgradeable to adapt to regulatory changes and business expansion.

Unlike the “lightweight deployment” common in typical DeFi projects, stablecoin backend systems effectively serve as a “public settlement layer,” with technology and operational costs consistently reaching millions of dollars annually.

Compliance, reserves, and systems form the three foundational pillars of stablecoin issuance, collectively determining whether a project can achieve long-term sustainability.

At its core, a stablecoin is not merely a technical product, but a financial infrastructure combining trust, compliance frameworks, and payment capabilities.

Only enterprises with genuine cross-border financial licenses, institutional-grade clearing systems, robust on-chain and off-chain technical capabilities, and controlled distribution channels can operate a stablecoin as a platform-level service.

Therefore, before entering this space, companies must first assess whether they possess the full suite of capabilities needed to build a complete stablecoin ecosystem: Can they gain sustained regulatory approval across multiple jurisdictions? Do they own or have trusted custody systems? Can they directly control wallets, exchanges, and other distribution channels to truly enable circulation?

This is not a lightweight startup opportunity, but a grueling battle demanding immense capital, systemic strength, and long-term capabilities.

After Launching a Stablecoin, Then What?

Completing the issuance of a stablecoin is just the beginning.

Regulatory approvals, technical systems, and custody structures are merely entry requirements. The real challenge lies in making it circulate.

A stablecoin’s core competitiveness boils down to one question: will anyone use it? Only when a stablecoin is supported by exchanges, integrated into wallets, adopted by payment gateways and merchants, and ultimately used by end users, does it achieve true circulation. And along this path lie substantial distribution costs.

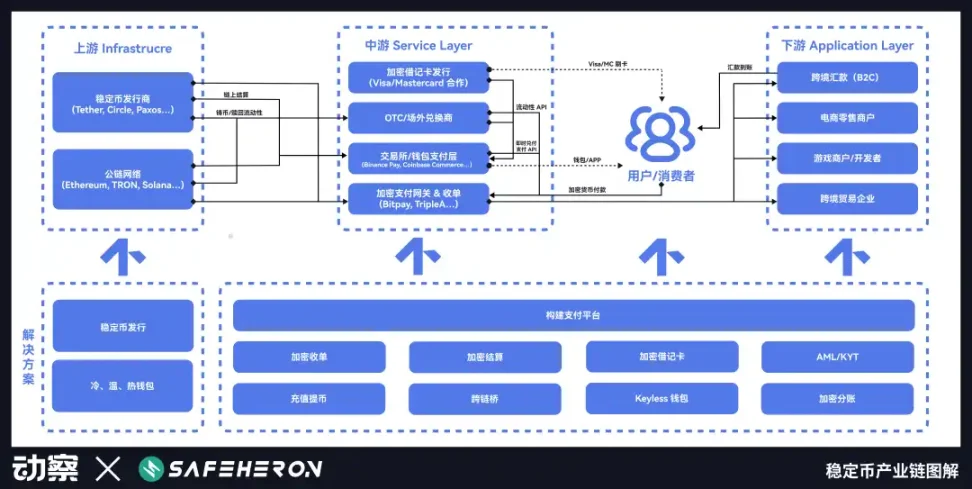

According to the stablecoin industry chain diagram jointly released by Beating and digital asset custody provider Safeheron, stablecoin issuance is only the starting point. To achieve circulation, attention must shift downstream.

Taking USDT, USDC, and PYUSD as examples, we can clearly see three distinct circulation strategies:

· USDT relied on early gray-market scenarios to build an irreplicable network effect, leveraging first-mover advantage to quickly establish market dominance;

· USDC expanded primarily through channel partnerships under a compliance framework, gradually growing via platforms like Coinbase;

While PYUSD, despite being backed by PayPal, still relies on incentive programs to boost TVL and struggles to penetrate real-world usage scenarios.

Different paths, yet all reveal the same truth—competition in stablecoins isn’t about issuance, but circulation. Success hinges on the ability to build a distribution network.

1. USDT’s Irreplicable First-Mover Advantage

USDT was born out of real challenges faced by crypto exchanges at the time.

In 2014, Hong Kong-based cryptocurrency exchange Bitfinex was rapidly expanding globally. Traders wanted to trade in U.S. dollars, but the platform lacked stable USD deposit channels.

Cross-border banking systems were hostile toward cryptocurrency. Moving funds between China, Hong Kong, and Taiwan was difficult, accounts were frequently shut down, and traders constantly faced funding disruptions.

Against this backdrop, Tether emerged. Initially running on Bitcoin’s Omni protocol, its mechanism was simple: users wire U.S. dollars to Tether’s bank account, and Tether issues equivalent USDT on-chain.

This bypassed traditional banking clearance systems, enabling “U.S. dollars” to move borderlessly and 24/7 for the first time.

Bitfinex became Tether’s first major distribution node. More importantly, both were operated by the same group. This deep integration allowed USDT to rapidly gain liquidity and use cases early on. Tether provided Bitfinex with an efficient—though compliance-ambiguous—U.S. dollar channel. Aligned incentives, shared information, mutual benefit.

Technically, Tether wasn't sophisticated—but solving traders' pain points around deposits and withdrawals became the key to capturing user mindshare early.

As capital markets grew volatile in 2015, USDT’s appeal surged. Users from non-dollar regions began seeking dollar alternatives to bypass capital controls, and Tether offered a “digital dollar” solution accessible online without opening accounts or undergoing KYC.

For many users, USDT wasn’t just a tool—it was a hedge.

The 2017 ICO boom marked the moment Tether achieved product-market fit. After Ethereum’s mainnet launch, ERC-20 projects exploded, exchanges shifted to crypto trading pairs, and USDT quickly became the “dollar proxy” in the altcoin market. Traders could freely move between platforms like Binance and Poloniex using USDT, avoiding repeated deposits and withdrawals.

Interestingly, Tether never spent money promoting itself.

Unlike most stablecoins that use subsidies to grow market share early on, Tether never incentivized exchanges or users to adopt its product.

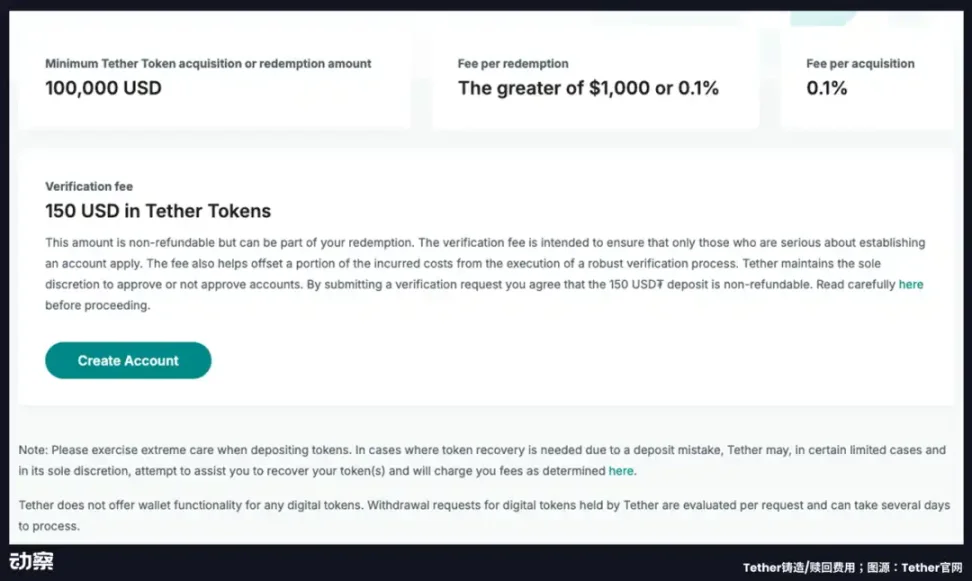

Instead, Tether charges a 0.1% fee on every mint and redemption, with a minimum redemption threshold of $100,000 and an additional $150 verification fee in USDT.

For institutions wanting direct access, this fee structure almost functions as a “reverse promotion” strategy. Rather than selling the product, it sets the standard. The crypto trading network has already formed around USDT—any participant wishing to join must conform to it.

Since 2019, USDT has practically become synonymous with “on-chain dollars.” Despite repeated regulatory investigations, media skepticism, and reserve controversies, USDT’s market share and circulating volume continue to climb.

By 2023, USDT had become the most widely used stablecoin in non-U.S. markets, especially across the Global South. In high-inflation countries like Argentina, Nigeria, Turkey, and Ukraine, USDT is used for salary payments, international remittances, and even as a substitute for local currencies.

Tether’s true moat has never been its code or asset transparency, but the trust pathways and distribution networks it built early within Chinese-speaking crypto communities. Starting from Hong Kong, jumping off from Greater China, this network gradually extended across the entire non-Western world.

This “first-mover-as-standard” advantage means Tether no longer needs to prove who it is—instead, the market must adapt to the circulation system it has already established.

2. Why Circle Depends on Coinbase

Unlike Tether’s organic growth in gray-market environments, USDC was designed from the outset as a standardized, institutional financial product.

In 2018, Circle partnered with Coinbase to launch USDC, aiming to create a “on-chain dollar” system for institutions and mainstream users under a compliant and controlled framework. To ensure governance neutrality and technical collaboration, both parties held 50% stakes in a joint venture called Center, responsible for USDC’s governance, issuance, and operations.

Yet this joint governance model failed to solve a critical question—how would USDC actually achieve circulation?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News