Is this company the real stablecoin unicorn?

TechFlow Selected TechFlow Selected

Is this company the real stablecoin unicorn?

$260 million in cash will be used by Ethena Foundation's subsidiary to purchase ENA on the open market.

By Alex Liu, Foresight News

On the evening of July 21, Ethena's native token ENA briefly surged 20% to reach 0.59 USDT, hitting a six-month high, after news spread that a treasury company planned to purchase $260 million worth of ENA tokens, sparking widespread market discussion. This article will detail the event and ENA’s recent performance, analyze its potential impact on the Ethena project and the broader market, and assess the current state of the project.

StablecoinX Completes Funding and Pursues Nasdaq Listing

On the evening of July 21, Ethena announced that its subsidiary StablecoinX has entered into a merger agreement with TLGY Acquisition Corp, aiming to go public via a SPAC deal and raise approximately $360 million. The Ethena Foundation will subscribe for $60 million, while other institutional investors include Dragonfly, Pantera Capital, Galaxy Digital, Wintermute, Polychain, and Haun Ventures.

The funding is being conducted through a PIPE (private investment in public equity) offering, consisting of $260 million in cash and $100 million in discounted, locked ENA tokens. According to the announcement, these funds will be used to establish a long-term ENA treasury reserve. The new company, StablecoinX, plans to invest approximately $5 million daily into buying ENA tokens on the open market, aiming to accumulate around $260 million worth of ENA within six weeks—accounting for roughly 8% of the current circulating supply.

In addition to investing in ENA, StablecoinX also plans to operate technical infrastructure related to the Ethena ecosystem, such as running validator nodes and staking services. Upon completion of the financing, StablecoinX will list on Nasdaq under the ticker symbol "USDE", while the Ethena Foundation will retain majority voting rights.

The Ethena team emphasized that these tokens will be permanently locked and held long-term, with the Ethena Foundation retaining veto power over any sale. The goal is to support the ecosystem through continuous accumulation and increase the per-share ENA holdings.

Review of ENA’s Recent Price Performance

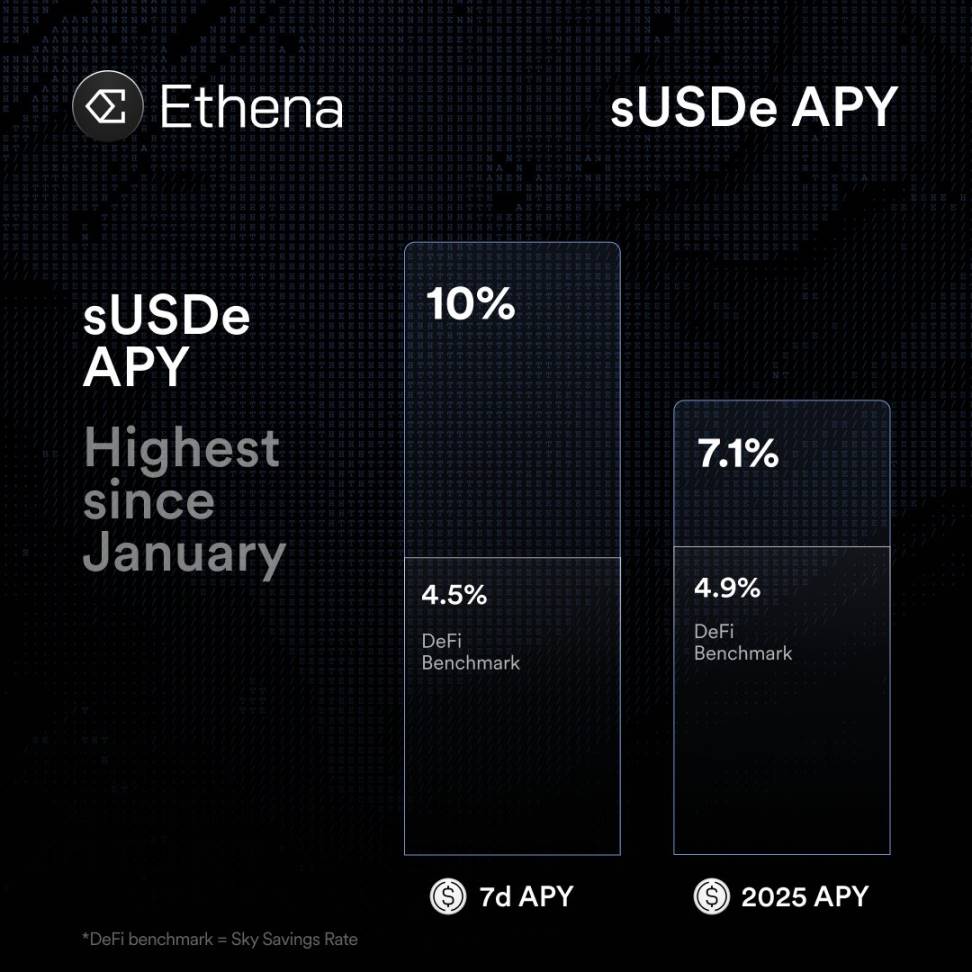

Prior to the StablecoinX announcement, ENA had already begun a rapid price rise. On July 20 (Sunday), broad market gains lifted funding rates, with major assets like ETH and SOL rising. Ethena, which had previously been sluggish, saw renewed capital inflows. That day, ENA surged by as much as 20%, breaking above the 0.5 USDT level—the highest since February this year. Meanwhile, Ethena’s “synthetic dollar” stablecoin USDe attracted about $750 million in net inflows, pushing its supply close to a record high of nearly 6.1 billion. During this rally, Ethena’s yield-generating strategy became profitable again, driving the annualized sUSDe interest rate to 10%, significantly surpassing traditional money market funds.

Potential Impacts on the Ethena Project

The preparation and listing plan for StablecoinX carries significant implications for the Ethena project itself.

First, this represents another attempt by a DeFi project to engage with traditional capital markets, similar to Circle’s (USDC) listing or Ripple’s issuance of tradable products, reflecting strong institutional interest in the stablecoin sector. By presenting its “growth story” through a public company structure, Ethena offers exposure to traditional stock market investors—an industry signal of integration with traditional finance (TradFi). As Ethena’s founder stated, the transaction provides stock market investors with a pure-play investment vehicle focused on the theme of “digital dollars.”

Second, from a supply-demand perspective, StablecoinX’s plan to aggressively buy and permanently lock ENA introduces a powerful new buyer into the ecosystem. A sustained daily purchase of $5 million over several weeks, along with total procurement power of $360 million combining cash and locked tokens, will substantially increase demand for ENA. This model, akin to a “Bitcoin treasury” approach (inspired by companies holding BTC), could provide long-term value support for ENA.

Some argue that such a stable capital allocation strategy can generate real user-level demand and potentially lift the long-term floor value of the token. However, others note that this capital flow does not directly alter Ethena’s underlying economic model: Ethena’s core mechanism remains users minting USDe by collateralizing crypto assets and executing hedging strategies to generate yield. The StablecoinX buyback plan increases market demand but does not change the operational logic of the Ethena protocol, so whether the project’s “fundamentals” have truly changed remains to be seen. In the long run, this adds a consistent capital player bullish on ENA, but if the underlying arbitrage model falters (e.g., funding rates decline), the project’s return capacity will still need to be tested.

Third, the macro regulatory environment is also shifting. Recently, the U.S. passed several stablecoin regulations including the GENIUS Act, which mandates full asset backing (cash or Treasuries) for stablecoins, strengthens oversight, and prohibits dividend-like yield-bearing stablecoins—indicating growing scrutiny from both U.S. regulators and traditional financial institutions.

For Ethena, its USDe falls under “crypto-collateralized synthetic dollars,” which may face compliance pressure under the new regulatory framework. If Ethena were to fully comply with U.S. stablecoin laws, it might need to adjust its hedging strategies. Nevertheless, Ethena’s current stance is that USDe is not a payment-oriented stablecoin but rather a synthetic asset tool, and therefore should not fall directly under the jurisdiction of the new law. Overall, StablecoinX’s listing and fundraising occur against a backdrop of increasingly clear regulatory boundaries, potentially introducing more compliance considerations for Ethena while simultaneously boosting its visibility and legitimacy in mature markets.

Assessment of Ethena’s Current Status

Overall, Ethena is currently in a phase of rapid development. First, the recovery in funding rates has genuinely enhanced USDe’s appeal. Recently, Ethena’s stablecoin strategy—hedged using BTC, ETH, and SOL—has delivered nearly 10% annualized returns to users, far exceeding traditional dollar funds. This has drawn substantial capital inflows, with last week’s net mints totaling around $750 million, bringing USDe supply near all-time highs.

Second, regulatory and policy developments warrant attention. The U.S. has enacted the GENIUS stablecoin bill, placing stablecoin issuers under Federal Reserve oversight and requiring 100% asset backing. This has profound implications for mainstream stablecoins like USDC and USDT. Ethena’s USDe, as a crypto-collateralized stablecoin, may need adjustments or exemptions under the new law’s definitions.

As noted earlier, Ethena is engaging with regulators to assert the synthetic nature of its dollar product and avoid direct regulation. However, if Ethena aims to offer USDe to U.S. investors in the future, it may be required to add fiat or Treasury-backed reserves. In short, regulatory uncertainty poses challenges, particularly regarding compliance pressures on its high-yield model.

Finally, the project has made progress integrating with traditional assets. For example, Ethena launched USDtb—a stablecoin backed by fiat or existing institutional assets—and allocated part of its capital to a dollar fund managed by BlackRock. These moves enhance product compliance and institutional credibility. Additionally, Ethena’s recent integration with Telegram Wallet and launch of lending strategies add stickiness to its ecosystem. Despite these advances, Ethena remains a relatively young DeFi protocol and must still overcome multiple hurdles—including regulation, competition, and market volatility—to achieve sustainable long-term growth.

In summary, StablecoinX’s successful fundraising and launch of the ENA treasury plan have brought positive momentum to the Ethena project: pushing up the token price in the short term and creating appreciation expectations for holders. In the long run, this marks Ethena’s effort to connect its digital dollar vision with traditional capital markets, opening new avenues for fundraising and distribution. However, this move does not fundamentally alter Ethena’s asset or yield model, as its stablecoin operations continue to rely on crypto-collateralized hedging mechanisms.

Therefore, whether the project’s fundamentals have been “transformed” remains uncertain: the cash inflow and public market backing brought by StablecoinX are undoubtedly bullish, but Ethena must still prove the sustainability of its high-yield model and adaptability to evolving regulations—both of which require time and further observation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News