Plasma in one hand, Stable in the other—will the stablecoin king squeeze Tron?

TechFlow Selected TechFlow Selected

Plasma in one hand, Stable in the other—will the stablecoin king squeeze Tron?

In the year of stablecoins, Tether, the largest stablecoin, seems to be building its own Tron.

By Jaleel, BlockBeats

Tether has long become a giant in the stablecoin industry thanks to USDT’s global circulation. Just from treasury bond interest alone, it earns $13 billion annually—making it one of the most profitable fintech companies in the world. However, while reviewing its business model, Tether realized that although it captures significant profits from issuing and managing USDT, it does not directly benefit from the "on-chain economic revenue" generated by its own token.

Ethereum collects gas fees daily, with USDT transactions accounting for nearly $100,000—over 6% of total Ethereum transaction costs. But this is only part of the story. The real stage where USDT value accrual reaches its peak is on Tron. According to the latest on-chain data, USDT transactions and gas consumption on Tron now exceed 98% of the entire public chain's volume. In other words, Tron’s trading activity is almost entirely fueled by USDT.

Each on-chain USDT transfer typically costs users between $0.3 and $8 in fees. To put it more clearly: Tron currently generates over $2.1 million in daily on-chain revenue, amounting to an annualized income of $770 million. The vast majority of this comes from high-frequency USDT transfer fees. With 2.46 million on-chain transactions within 24 hours across the Tron network, the average fee per transaction stands at approximately $0.85—closely matching the typical cost of transferring USDT on-chain. Currently, Tron’s market cap exceeds $25 billion, and its consistent on-chain income ranks among the highest across all major blockchains.

Data source: DefiLama

For Tether, this represents a classic case of “value capture imbalance.” While USDT issuance and branding bring massive user traffic and stable industrial-level demand, the infrastructure—not Tether itself—collects all the transaction fees and ecosystem benefits. This not only weakens Tether’s strategic influence in future on-chain payment and settlement networks but also leaves it vulnerable to emerging threats such as Tron launching its own stablecoin or user traffic being diverted elsewhere.

If Tether remains content being just a “super minting factory” for stablecoins without gaining control over underlying infrastructure, its long-term value ceiling will be severely limited.

This is precisely why Tether is fully investing in building its own stablecoin-centric blockchain ecosystem. Through a dedicated chain model, Tether can reclaim the enormous transaction fees and ecosystem rewards that previously flowed to Ethereum, Tron, and other public chains. More importantly, it can build its own closed-loop on-chain system for B2B payments, compliant settlements, and industrial coordination.

Even more critically, Tron itself is now trying to reduce its reliance on USDT.

Recently, Tron launched USD1, a new stablecoin backed by the Trump family. Tron founder Justin Sun serves as an advisor to the Trump family’s DeFi project and was the top contributor to the TRUMP token—indicating a complex and close relationship that suggests Tron may gradually reduce its dependence on USDT issuance and usage in the coming years.

Additionally, from a cost perspective, Tron’s advantage as a stablecoin settlement network is fading. Without purchasing and burning TRX, current transaction fees on Tron have surpassed even Bitcoin’s traditionally expensive network—and are higher than those on Ethereum, Arbitrum, and BNB Chain.

This trend isn’t favorable for USDT, especially when compared to Base network transfers of USDC, which cost just $0.000409. Circle even introduced Circle Paymaster, allowing users to pay gas fees in USDC on Arbitrum and Base.

These trends and competitive pressures force Tether to swiftly adjust its business strategy.

Plasma: The Source of Tron’s Anxiety

Tether’s first move came quietly at the end of 2024, when it began supporting a new chain called Plasma.

At first, there were only a few announcements and funding rounds—Bitfinex (Tether’s parent company), Peter Thiel’s Founders Fund, Framework, and others injected $24 million, followed by an additional $3.5 million from external investors. Within two months, Plasma’s valuation soared to $500 million.

Plasma uses Bitcoin’s mainnet as its final settlement layer, inheriting UTXO security, while maintaining full EVM compatibility at the execution layer. Most importantly, all on-chain transactions can be paid directly in USDT, and USDT transfers are completely free.

Thanks to this simple yet powerful selling point—"zero gas fees"—when the official team recently opened governance token XPL allocations for liquidity deposits, the initial $500 million quota was snapped up in minutes. An additional $500 million deposit cap sold out within 30 minutes. Some whales even paid $100,000 in Ethereum gas fees just to secure early access. This shows strong market appetite for a fee-free stablecoin chain.

Beyond technical architecture, Plasma has quietly introduced two key advantages. The first is “native privacy.” On-chain transfers are public by default, but users can enable shielded mode with a single wallet toggle to hide addresses and amounts. For audits or compliance needs, selective disclosure remains possible. The second is “Bitcoin liquidity.” Plasma promises to seamlessly integrate native BTC via permissionless bridges. Combined with Tether’s deep USD pools, low-slippage swaps and BTC-collateralized stablecoin loans can happen within the same environment.

All of this aligns perfectly with Tether’s year-long accumulation of Bitcoin. The Plasma team and Bitfinex partners have long been staunch supporters of Bitcoin.

Onstage at the center of the 2025 Bitcoin Conference, Tether CEO Paolo Ardoino stood before an image of Sun Wukong and declared, “Bitcoin is my Monkey King. He is our friend.”

In spring 2025, Tether announced it would become the largest shareholder in Twenty One Capital, a Nasdaq-listed firm formed through mergers and acquisitions—a company similar to MicroStrategy focused on Bitcoin treasury management.

Tether spent $458.7 million acquiring more BTC and transferred 37,000 bitcoins into a new address to support Twenty One Capital. Together, Tether and Twenty One Capital now hold approximately 137,000 BTC—ranking third among publicly traded companies holding Bitcoin, behind only MicroStrategy and mining firm MARA Holdings.

Data source: https://bitbo.io/

Previously, outsiders questioned why Tether would convert stablecoin profits into “digital gold.” Now the answer is clear: USDT acts as the clearing currency, BTC serves as reserve assets, and both converge within Plasma. This aims to consolidate the $150 billion worth of USDT scattered across more than a dozen networks onto a unified settlement layer, enabling transfers, exchanges, and redemptions to occur entirely within Tether’s own domain.

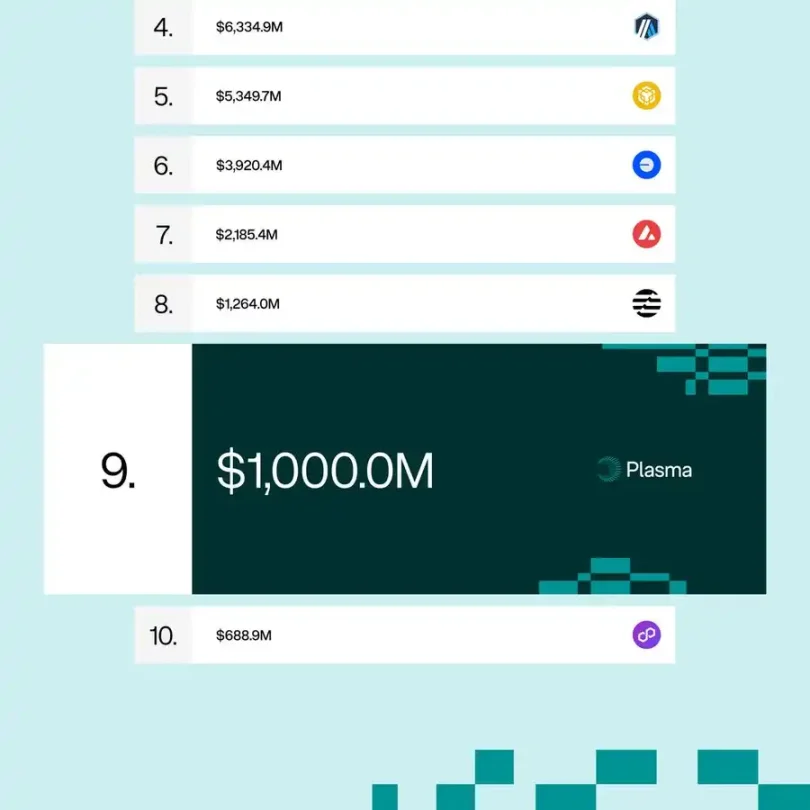

At mainnet testnet launch, Plasma ranked as the ninth-largest blockchain globally by stablecoin liquidity, valued at $1 billion.

In the past, Tether had to follow Ethereum and Tron’s rules—if they raised fees or changed protocols, USDT could only comply passively. Infrastructure supporting USDT (settlement, execution, bridging) was largely outside Tether’s control. Now, with Plasma integrating issuance, circulation, and redemption into its own ecosystem, Tether gains greater pricing power and influence—naturally taking control of the network’s revenue gate.

How Much Can Plasma Earn Tether Annually?

Although Plasma offers zero-fee USDT transfers, that doesn't mean it lacks revenue.

Plasma doesn’t subsidize “free transfers” with corporate funds. Instead, it splits transactions into two billing models based on complexity and priority—similar to saying “children under 1.2 meters tall ride free.”

Simple USDT transfers occupy minimal block space—like “children under 1.2 meters”—and nodes include them in blocks at no charge. To prevent spam attacks, Plasma sets a base throughput limit. Additionally, to deter abuse, users must leave a small on-chain deposit acting as collateral: if usage thresholds are breached, the deposit is automatically forfeited. This preserves the “free” experience while filtering out junk traffic.

More complex operations—such as multi-contract calls, batch settlements, or institutional-grade instant clearing—are identified by the system and require payment. Plasma nodes earn primarily from these advanced transactions. Additional micro-fees from cross-chain bridging and custody services provide further self-sustaining income. Because simple transfers are no longer charged, pricing for premium services becomes more flexible: current estimates show thousands of free payments per second consume minimal resources, allowing nodes to cover costs and generate surplus from a small number of high-end transactions.

This mechanism is supported by Plasma’s “two-layer framework.” The base layer periodically anchors block states back to Bitcoin, outsourcing security to BTC’s proof-of-work. The upper layer maintains full EVM compatibility, enabling developers to port Ethereum contracts directly. By removing traditional gas calculations, execution efficiency improves significantly. Messari noted in a review report that Plasma’s optimized consensus can stably process thousands of payments per second on a single-core CPU during stress tests, with node rewards funded solely by complex transactions.

So how does Plasma make money? The answer is now evident.

First, enterprise “dedicated lanes”: cross-border remittance firms or game publishers seeking sub-millisecond transaction speeds must enter a paid tier, paying a fixed monthly USDT fee for guaranteed bandwidth.

Second, smart contract and batch clearing: DeFi protocols using complex logic still pay gas, priced in USDT instead of ETH.

Third, bridging and custody: moving assets onto or off Plasma incurs a minor exit tax. These funds go into the Plasma treasury and are distributed to validators and the foundation according to predefined rules.

Fourth, governance token XPL inflation: validators stake XPL to earn block rewards; the Plasma treasury retains a portion to auction over time, continuously subsidizing peer-to-peer 0-gas USDT payments.

Combined, these four streams can cover the operational costs of free transfers—and even generate a new revenue stream for Tether.

If Plasma successfully captures most of the USDT traffic currently on Tron and Ethereum, its direct earnings would reclaim much of the on-chain fees previously siphoned off by those chains—generating roughly $1–2 billion annually. Adding enterprise services and cross-chain fees, total incremental revenue could reach $1.2–3 billion.

However, due to free basic USDT transfers, a conservative estimate places Plasma’s annual contribution to Tether at around $1 billion.

Moreover, Plasma may yield hidden benefits and ecosystem spillovers: attracting large new liquidity providers and projects, charging certain “taxes”; offering SDKs and enterprise node access, collecting commercial fees from dApps, etc.

Comparing this new revenue stream to Tether’s existing books makes the impact clearer: in 2024, Tether earned about $13 billion, with $7 billion from treasury bonds, $45 million from 0.1% issuance/redeem fees, and nearly $6 billion from investments in Bitcoin, gold, and early-stage ventures. This means Plasma could potentially boost Tether’s annual profit by 15%–20%.

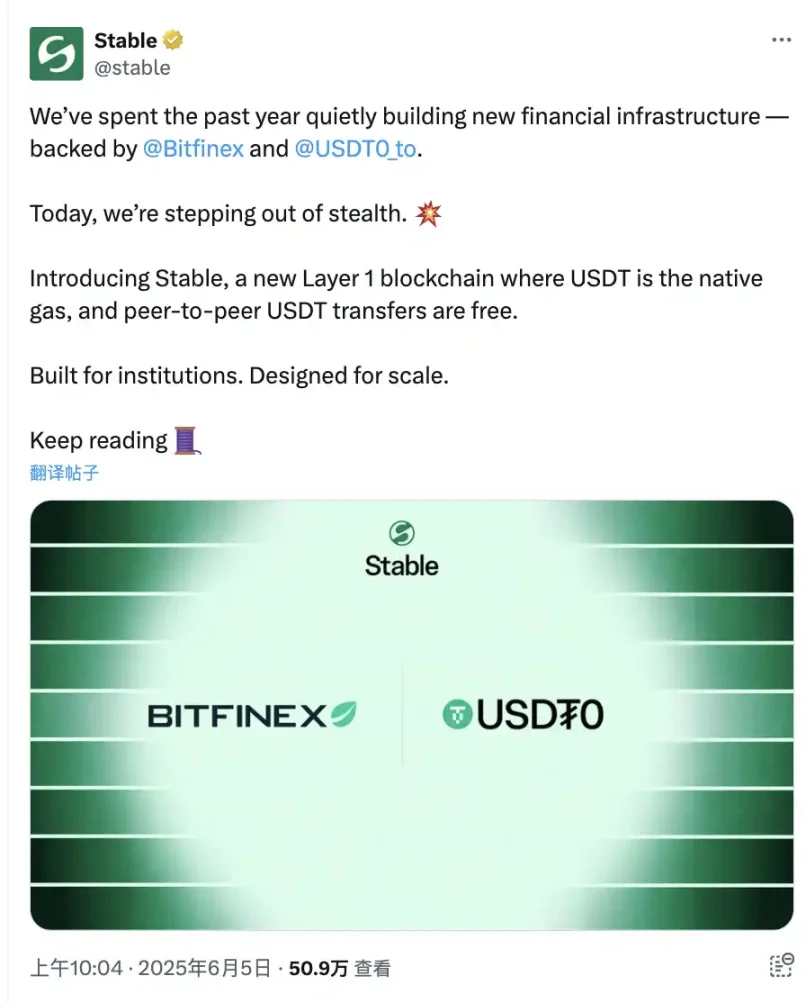

Stable: A USDT L1 Chain Tailored for Institutions

After bringing major liquidity holders and developer ecosystems into the fold via Plasma, Tether didn’t stop there. This month, a new L1 chain named Stable was officially announced—backed by Bitfinex and the unified liquidity protocol USDT0—with Tether CEO Paolo Ardoino serving as project advisor.

Unlike Plasma, which operates as a Bitcoin L2, Stable is an independent L1. While it also uses USDT as gas and enables free point-to-point USDT transfers, it targets a very different audience: global financial institutions, enterprise settlements, bulk clearing, on-chain corporate finance, B2B cross-border payments—not retail or small-scale use cases.

Stable’s internal testnet is already live. The team is guiding early builders to explore SDKs for wallets, applications, and custodial integrations—including fast fiat onboarding, dollar-denominated smart contracts, and gas-free wallets—so users may not even realize they’re interacting with a blockchain.

The rationale behind Stable lies in Tether’s recent flurry of commodity investments. This spring, Tether acquired a 70% stake in Adecoagro, a Latin American agribusiness and renewable energy giant, then announced USDT would directly settle South American grain, ethanol, and even crude oil trades. On June 5, Tether strategically invested in Shiga Digital, an African blockchain financial platform providing virtual accounts, OTC trading, treasury management, and FX services to African enterprises. Most recently, on June 12, Tether acquired approximately 31.9% (78,421,780 shares) of Canadian-listed gold miner Elemental and signed an option agreement with AlphaStream Limited to purchase an additional 34,444,580 shares after October 29, 2025.

Traditional commodity trading has long relied on bank wire transfers and letters of credit. A single cargo shipment might tie up tens of millions of dollars, with funds stuck in banking systems for days during clearance. Converting such sums into on-chain USDT allows counterparties to release funds nearly instantly. Stable’s enterprise channel provides exactly this kind of “dedicated express lane” for high-value, compliant, low-latency dollar flows. Clearing houses and custodians can use the USDT0 bridging protocol to move stablecoins in and out regardless of the underlying chain.

For large commodity traders who manage physical assets and require regulatory compliance, slightly higher channel fees are acceptable if settlement speed vastly outperforms traditional wires. For Tether, this type of traffic is far more stable and profitable than retail transfers. Crucially, once Stable integrates “USDT + physical assets” onto a single ledger, Tether can embed its captured on-chain dollar flows directly into grains, energy, and entire supply chains. As Paolo Ardoino previously stated in an interview, the biggest growth area for USDT over the next five years won’t be crypto trading—but commodity trade.

The two chains have clear roles: Plasma optimizes on-chain user experience, using zero gas to turn small transactions into massive volume; Stable focuses on institutional compliance, turning large volumes into sustainable high-margin revenue via dedicated clearing. Their shared goal is singular—to ensure USDT is no longer constrained by any public chain’s fee structure or taxed by a single ecosystem. From daily remittances to shipments of soybeans, every dollar flow should ultimately return to ledgers controlled by Tether. This is the ultimate objective of Tether’s “sovereignty counteroffensive.”

A New U.S.-Exclusive Stablecoin for Tether?

“Americans want checking accounts—for daily spending—while overseas users treat USDT as savings,” said Tether CEO Paolo Ardoino recently, hinting at Tether’s next strategic move: a localized U.S. payment-focused stablecoin.

Prior to this, Paolo revealed that Tether might establish a new U.S.-based entity to issue a stablecoin tailored specifically for domestic payment scenarios, while retaining existing USDT for international markets and developing regions. When asked whether Tether plans to build a payment network akin to Square that supports stablecoin payments, Paolo responded: “I can’t disclose all the details yet, but you're thinking in the right direction.”

This ambition inevitably involves a pivotal player—U.S. banks.

Last week, Paolo reshared news on X about the first U.S. bank openly expressing willingness to issue stablecoins, adding the cryptic phrase “Select your player.” Industry insiders immediately speculated that Tether is likely partnering with this bank.

What many don’t know is that Tether has a heavyweight ally on Wall Street: Howard Lutnick, former Commerce Secretary under Trump and billionaire head of Cantor Fitzgerald, which currently manages billions in Tether’s treasury holdings and serves as USDT’s most influential advocate in traditional capital markets. Once a U.S.-focused stablecoin launches, Cantor’s clearing network and market-making desks will naturally serve as ideal liquidity backstops.

Of course, Tether’s perceived “gray-area” associations remain under intense scrutiny by U.S. regulators. A Treasury report highlighted Mexican drug cartels’ preference for USDT, and some lawmakers have labeled it a negative example in crypto. In response, Tether relocated its registration to El Salvador—a Bitcoin-friendly jurisdiction—and made highly visible purchases of hundreds of billions in U.S. Treasuries, positioning itself as “America’s creditor” to mitigate policy risks.

Thus, Plasma has already drawn retail users, zero-fee payments, and on-chain developers firmly into Tether’s orbit; Stable is moving shipments of soybeans, crude oil, and cross-border salaries into millisecond-dollar settlements; and the upcoming “U.S. payment coin” aims to dismantle the last stronghold of bank wire transfers. Three distinct networks, clearly divided in function, yet all channeling revenue through a single gatekeeper—Tether itself.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News