What Airwallex's founders got wrong about stablecoins

TechFlow Selected TechFlow Selected

What Airwallex's founders got wrong about stablecoins

Watch the格局being reshuffled—don't tie your own hands at the starting line.

Bottom line first: In the G10 golden corridor of dollar-euro transactions, Airwallex’s “instant settlement + 0.01% fee” offering is nearly flawless. But the financial world isn’t just one highway. Stripe's acquisition of Bridge, Visa integrating stablecoin settlements into its network, and Circle’s explosive NYSE IPO—all paint a much bigger picture: Whoever unlocks the "last mile" of money movement will have the chance to redefine the next-generation payment infrastructure.

1. The "0.01% + instant" halo only covers 15% of the battlefield

Jack Zhang recently posted a series of long threads on X, making three core arguments:

Pricing—Airwallex has slashed USD→EUR fees down to 0.01%;

Speed—Funds settle in real time; even on-chain transfers aren't necessarily faster;

Real-world adoption—Stablecoin on/off ramps remain expensive and bogged down by regulation, with no breakthrough use cases in 15 years.

If we limit the stage to London ↔ New York ↔ Frankfurt, he’s not exaggerating. The problem? 85% of global cross-border flows don’t travel along this G10 superhighway.

-

To a freelancer in Argentina, banks still mean at least 3-day waits and 3% fees;

-

A merchant in Kenya shipping goods to Nigeria must navigate two layers of correspondent banking “mountain roads”;

-

A Turkish importer trying to pay a deposit Friday night faces idle weekends as banks shut down.

In these overlooked corners ignored by “mainstream” finance, stablecoins have tripled in volume over the past six months—growing like wildfire.

2. Three curves explain why stablecoins are winning now

1. The Latin America Curve: Dollar scarcity fuels on-chain dollars

In 2021, stablecoins in Latin America totaled just $20 billion. By 2024, that surged to $68 billion, reaching $75 billion in the first half of this year. Hyperinflation, dollar shortages, and weekend banking blackouts have collectively pushed capital onto blockchains—not to save 0.01%, but because people need funds now.

2. The Big Tech Bet Curve: Keep money inside your ecosystem

Shortly after Stripe acquired Bridge for $1.1 billion, Visa rolled out the same rails across Ecuador, Peru, and Colombia. These companies aren’t chasing FX spreads—they’re betting on the expansion premium of keeping money within their own networks. Once funds no longer need to land in banks, payment providers can evolve into custodians, wealth platforms, and credit gateways—all in one.

3. The Wall Street Valuation Curve: Circle prints money via interest arbitrage

Last year, Circle earned $780 million purely from interest on USDC reserves. Its stock more than doubled in the first three days post-IPO. Wall Street is pricing in the “on-chain dollar + Treasury yield spread” cash machine—and more importantly, evidence that network effects have already materialized: Every new business accepting USDC reduces off-ramp demand and silences fee debates.

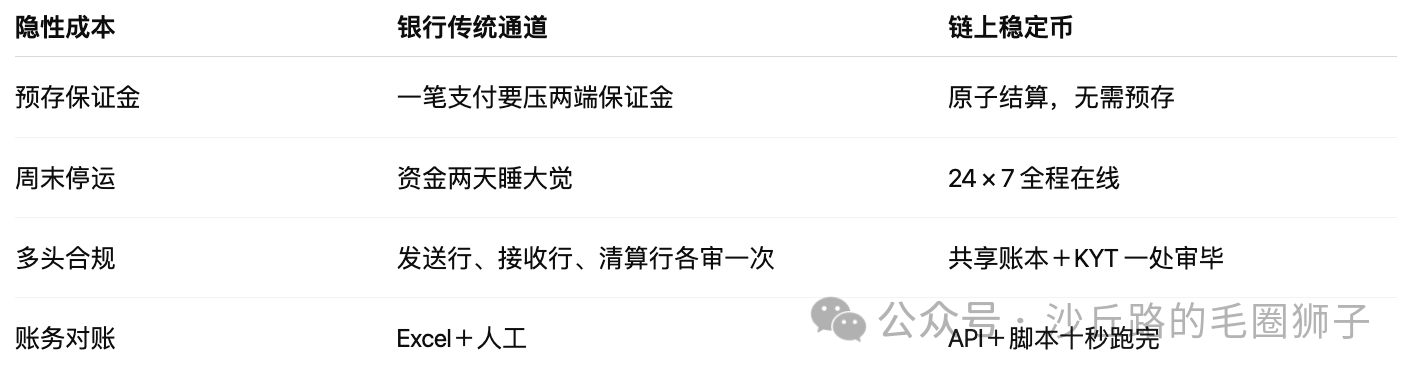

3. Beyond “cheap” and “fast”: The hidden costs nobody talks about

Many obsess over fee schedules while ignoring the silent profit-killers lurking beneath balance sheets: T+2 liquidity delays, Nostro account pre-funding, and repeated KYC checks. These are the real black holes draining cross-border margins.

When these frictions are reduced to code logic, a 0.01% fee advantage quickly becomes irrelevant.

4. Three real-world scenarios where stablecoins already beat banks

-

USD→ARS payroll

Banks impose forex controls and weekend shutdowns—transfers wait until Monday. USDC wallets deliver in 5 minutes, with effective all-in fees ≈1%. Employers get reliability; employees accept willingly. -

KES↔NGN small trade payments

No direct clearing link exists between Kenya and Nigeria. On-chain P2P runs 24/7 with fees of 1–2%. -

Weekend global liquidity management

Banks go dark after Friday close, freezing capital. Finance teams can instantly sweep funds on-chain into BUIDL to earn 4% APY, then redeploy for payroll come Monday morning.

These may not seem flashy, but they represent the thickest-margin, bank-abandoned long tail of global finance.

5. How the flywheel accelerates before 2026

-

Bank-backed issuers: Post-MiCA, at least ten European regional banks will follow Société Générale in launching EUR-denominated stablecoins.

-

Super App gateways: Grab, MercadoPago, and others are already testing USDC wallets in gray markets. Once enabled by default, tens of millions of users will instantly enter the on-chain economy.

-

On-chain closed loops emerge: Merchants receive, supply chains pay, employees collect, and savings earn interest—all within one network. Off-ramp fees naturally trend toward zero.

-

Corporate treasury migration: Deloitte predicts that by 2027, 10% of Fortune 500 idle cash will sit in yield-bearing stablecoin accounts—siphoning a massive chunk away from traditional bank current accounts.

At that point, debating 0.01% fees on G10 corridors will be like telecom giants in 2010 cutting long-distance rates by one cent, oblivious to WhatsApp adding a million free-call users daily.

6. The final message from Circle’s IPO

Circle delivered a pristine interest-income ledger and undeniable network momentum, sending a clear signal to markets: "Cheap remittances" are just the opening act—the main event is rewriting the financial foundation.

Airwallex has optimized the G10 corridor to near perfection—that’s championship-level performance in a 15% slice of the world. But the remaining 85% is racing on a different track, under a new scoring system.

The next phase? Money will fly around like emails. And when that happens, who will care whether the postage costs 1 cent or 0.1?

Watch the landscape shift—don’t tie your hands at the starting line.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News