Decoding the RWA Market: Market Size Surges 48% in First Half, ZKsync "Fights Back" to Become Second-Largest Public Chain

TechFlow Selected TechFlow Selected

Decoding the RWA Market: Market Size Surges 48% in First Half, ZKsync "Fights Back" to Become Second-Largest Public Chain

From a data perspective, the growth of the RWA market appears substantial.

Author: Frank, PANews

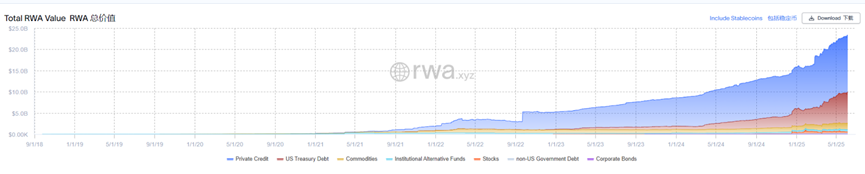

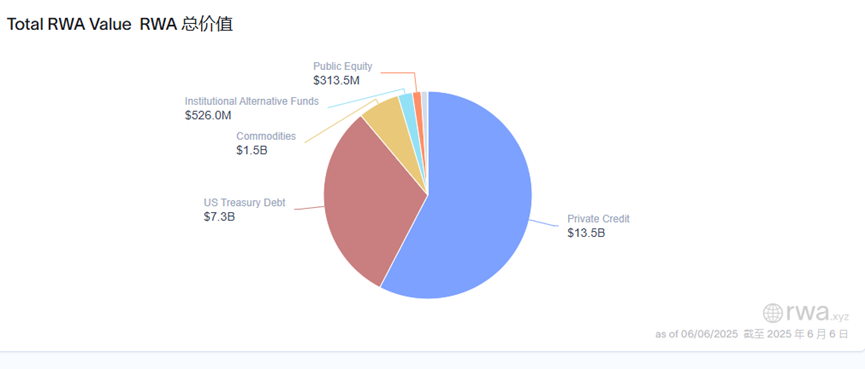

In the first half of 2025, a relatively low-key sector in the cryptocurrency world—real-world asset (RWA) tokenization—witnessed remarkable explosive growth. As of June 6, the global RWA market capitalization had surged to $23.39 billion (excluding stablecoins), up 48.9% from $15.7 billion at the beginning of the year. Behind this surge, private credit (approximately 58%) and U.S. Treasuries (about 31.2%) have emerged as the dominant dual engines, collectively accounting for nearly 90% of the market.

However, beneath these impressive figures lie deeper issues such as high concentration of asset types, limited liquidity, questionable transparency, and weak integration with native crypto ecosystems. RWA still has a long way to go before becoming a true "mainstream" sector.

Private Credit + U.S. Treasuries Account for 90% of Market

Private credit has become the most popular asset type within the RWA market, reaching a total scale of $13.5 billion, or about 57.7% of the total.

Figure leads with $10.19 billion in outstanding loans. Figure is a blockchain-based financial technology platform primarily offering home equity lines of credit (HELOC), allowing users to borrow up to 85% of their home’s value. According to its official data, HELOC has become the largest non-bank home equity line of credit in the U.S., having issued over $15 billion in credit facilities.

Unlike most RWAs that are typically issued on public blockchains, Figure uses Provenance Blockchain—a public yet permissioned Layer 1 chain. This design, similar to a consortium chain, allows better management of RWA assets but restricts their broader circulation in the market. Although Figure's on-chain RWA issuance exceeds $10 billion, these assets have minimal interaction with the broader crypto market. They are essentially tokenized mortgage notes without tradable or transferable features. As of now, this segment lacks transactional liquidity. By conventional definitions of RWA, Figure's offerings represent an atypical form of RWA.

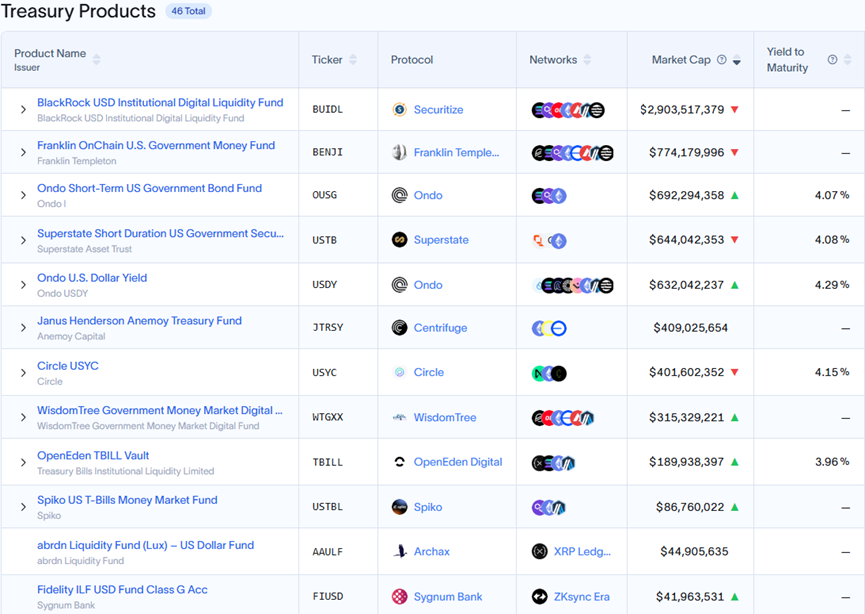

U.S. Treasuries rank second among RWA asset classes. These RWAs operate by converting traditional dollar-denominated assets—such as U.S. government bonds, cash, and repurchase agreements—into digital tokens via blockchain technology. In this category, BlackRock’s BUIDL leads with approximately $2.9 billion in total issuance.

The BUIDL fund was initially launched on Ethereum and has since expanded to multiple blockchain networks including Solana, Aptos, Arbitrum, Avalanche, Optimism, and Polygon. However, the vast majority—around 93%—of BUIDL assets remain issued on Ethereum.

Compared to traditional U.S. Treasury purchases, this type of RWA offers greater flexibility and 24/7 liquidity, whereas conventional treasury transactions may take days to settle. Currently, BUIDL is only available to qualified investors with a minimum investment threshold of $5 million, and there are only 75 holders. Additionally, BUIDL has introduced a DeFi-compatible version called sBUIDL—an ERC-20 token representing a 1:1 claim on the BUIDL fund. sBUIDL can interact with DeFi protocols such as Euler.

Beyond private credit and U.S. Treasuries, commodities rank third among RWA asset classes, primarily consisting of tokenized gold issued by institutions like Paxos and Tether, with a current total market cap of approximately $1.51 billion.

ZKsync and Stellar Emerge as Dark Horses in RWA Blockchains

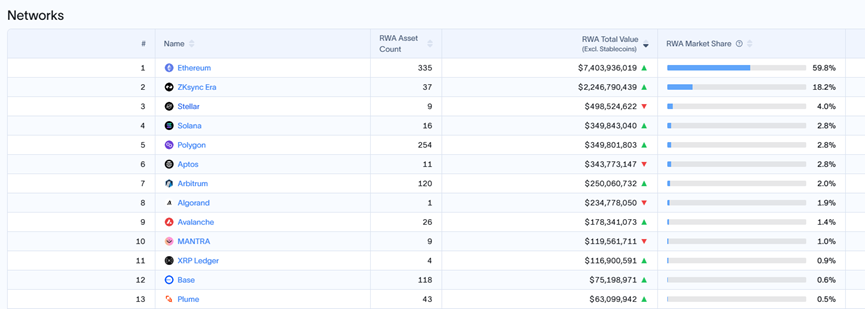

When comparing blockchains, Ethereum remains the most favored network for RWA assets, hosting $7.4 billion in market value—representing 55% of all assets issued on public chains (note: this percentage is calculated against ~$12.55 billion in total public chain-issued assets; Figure’s assets on its own chain are excluded).

Of Ethereum's holdings, $2.7 billion comes from BUIDL, making up 36.48%, while the rest consists largely of tokenized gold such as PAXG and XAUT.

More surprisingly, ZKsync ranks second in RWA blockchain adoption with $2.25 billion in asset issuance. This achievement is primarily attributed to Tradable, an asset management firm integrating Web3 technologies. Tradable enables institutions to launch investment opportunities on its platform, specifying details such as use cases and terms. Investors can then choose from offerings such as senior secured loans in fintech ($110 million raised, 15% return) or term loans to top-tier law firms ($57 million raised, 15.5% return). According to Tradable’s official data, 34 assets have been listed so far, with an average APY of 10%. However, the company appears inactive in marketing and operations—having only retweeted two posts on Twitter and never published original content, with its news page last updated in 2023.

Furthermore, PANews’ review of Tradable’s smart contracts reveals they are not open-sourced, do not involve interactions with crypto assets, and all show zero token balances. Thus, the actual on-chain amount of Tradable’s RWA assets remains questionable.

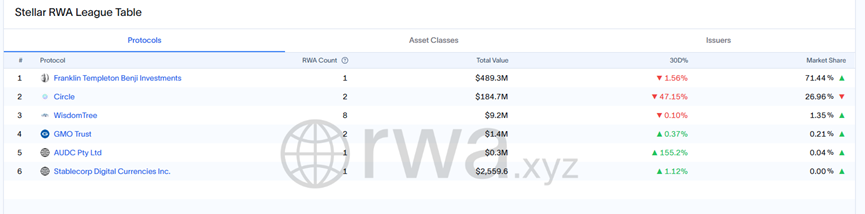

Additionally, Stellar ranks third in the RWA landscape—an unexpected result. The network currently hosts approximately $498 million in RWA assets, driven overwhelmingly by BENJI, a fund issued by Franklin Templeton worth around $489 million. BENJI is a money market fund backed by U.S. Treasuries, with a total issuance of about $770 million—63% of which is deployed on the Stellar chain.

Stellar, a veteran blockchain launched in 2014, had gradually faded from mainstream attention in recent years. In 2024, it launched the Soroban smart contract platform and introduced a $100 million adoption fund to incentivize development. Over the past year, it has also strengthened partnerships with institutions such as Franklin Templeton, Paxos, and Circle. These moves enabled Stellar to surpass popular chains like Solana and become the third-largest RWA-issuance blockchain. However, its RWA ecosystem remains heavily reliant on Franklin Templeton’s BENJI, indicating a relatively narrow and concentrated base.

Solana ranks fourth in RWA issuance with approximately $349 million. While the volume is modest, it has grown rapidly—up 101% since January 2025. Its RWA distribution is also dominated by U.S. Treasury-backed tokens.

Behind the Numbers: Hidden Challenges in the RWA Market

On the surface, the RWA market shows promising growth. Yet, several underlying challenges persist.

First, asset types remain heavily concentrated in private credit and U.S. Treasuries. Leading private credit projects like Figure and Tradable lack transparency. Moreover, Figure’s RWA assets exist merely as on-chain records without actual trading functionality. From this perspective, these assets fail to fully leverage blockchain’s potential to enhance liquidity and transparency for traditional finance.

Second, in the Treasury space, many RWA products resemble stablecoin issuance models. Interest-bearing stablecoins backed by U.S. Treasuries already deliver similar yields, creating direct competition for Treasury-centric RWA products.

Third, the market remains overly centralized in asset composition. Despite years of development, nearly 90% of RWA issuance still revolves around just two categories: Treasury bonds and private credit. Other asset classes such as commodities, equities, and funds remain underdeveloped due to hurdles related to physical custody, regulatory compliance, and operational costs.

As of now, the total RWA market size stands at $23.3 billion—far smaller than the stablecoin market (~$2.36 trillion) and even less than the market cap of some newly launched blockchain tokens. This pales in comparison to the widely anticipated multi-trillion-dollar potential of RWA. In terms of operation, today’s RWA landscape is almost exclusively dominated by institutions and large players, operating quite differently from traditional crypto markets. For retail investors, participation in RWA remains difficult. It will take considerable time before RWA becomes accessible to everyday users.

Overall, the first half of 2025 has indeed delivered strong growth for the RWA market, with near 50% expansion in market value and a clear duopoly forming between private credit and U.S. Treasuries. The potential of RWA is undeniable. However, overcoming current bottlenecks—achieving breakthroughs in transparency, liquidity, and integration with the broader crypto ecosystem—will determine whether RWA is a fleeting trend or the dawn of a new era in finance.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News