The "first stablecoin IPO" is coming, but hides a "fatal" flaw

TechFlow Selected TechFlow Selected

The "first stablecoin IPO" is coming, but hides a "fatal" flaw

Beneath the glossy surface of Wall Street giants rushing to enter, Circle also faces structural challenges.

By Xu Chao, Wall Street Insights

This Thursday marks the most significant IPO event of the year in the cryptocurrency market.

(Image generated by Doubao AI with prompt: "风口 and crisis")

Circle Internet Group—the issuer of the $60 billion USDC stablecoin—will begin trading on the New York Stock Exchange. The company will issue 32 million Class A shares at a price range of $27–28 per share, raising up to $896 million. Its stock ticker is CRCL. Pricing will be finalized Wednesday evening, with trading commencing the following day.

The IPO has drawn strong enthusiasm from Wall Street. Circle’s target valuation has been raised from an earlier $5.65 billion to $7.2 billion. BlackRock is leading a 10% stake investment, while Ark Investment has expressed interest in investing up to $150 million.

Yet beneath the glittering interest from financial giants, Circle faces structural challenges.

The Seemingly “Perfect” Money Printing Model

Stablecoins have quietly become the backbone of the crypto market, increasingly intertwined with traditional finance. In 2024, stablecoin transaction volume reached $27.6 trillion—nearly 8% higher than the combined volumes of Visa and Mastercard.

The total market capitalization of stablecoins now stands at $248 billion. Circle’s USDC holds 25% market share, second only to Tether’s USDT at 61%, with a market cap of $60 billion. Circle’s EURC leads among euro-backed stablecoins, with a market cap of $224 million.

Circle’s key advantage lies in regulatory compliance.

In the U.S., USDC positions itself as a compliant bridge between the crypto ecosystem and traditional finance. In the EU, the implementation of MiCA—and the resulting delisting of non-compliant stablecoins like USDT from major regulated exchanges—has paved the way for USDC to become the region’s leading stablecoin.

Circle’s business model is simple and attractive: it issues USDC, a dollar-pegged stablecoin, and invests the $60 billion deposited by users into short-term U.S. Treasury bonds to earn risk-free returns.

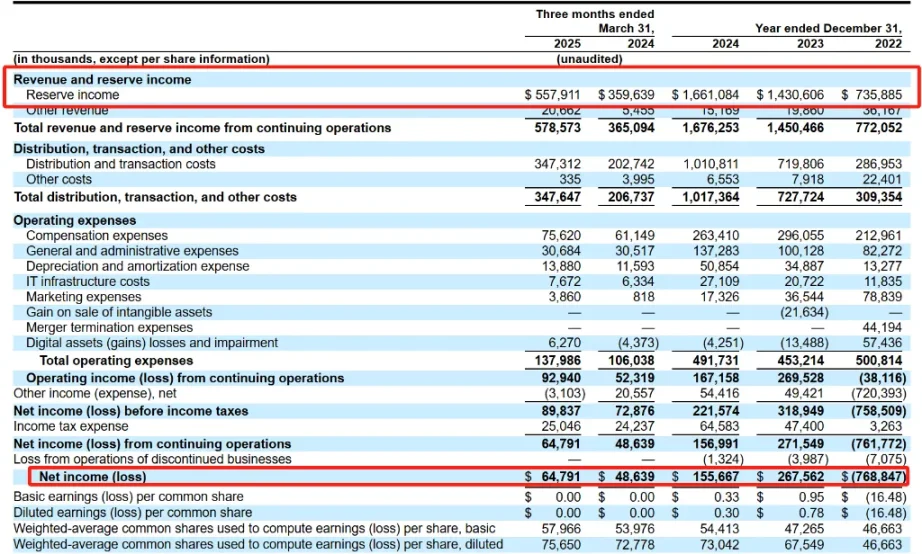

The company primarily invests in U.S. Treasuries (85%, managed by BlackRock’s CircleReserveFund) and cash (10–20%, held at globally systemically important banks). This model is highly profitable, generating approximately $1.6 billion in interest income (“reserve income”) in 2024, accounting for 99% of Circle’s total revenue.

Coinbase “Siphoning” Profits

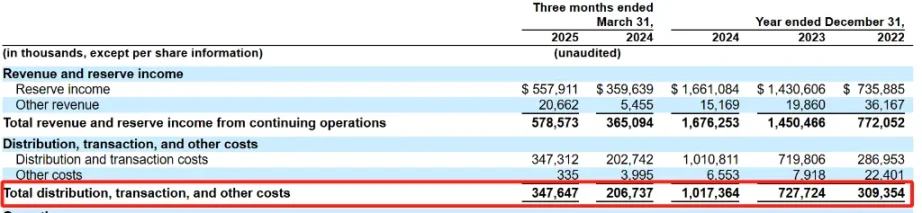

But behind this seemingly “perfect” money-printing machine, Circle’s financials reveal both growth and pressure: in 2024, total revenue and reserve income reached $1.676 billion, up 16% from $1.45 billion in 2023.

However, net profit dropped from $268 million to $156 million, a 42% decline.

The contradiction stems from a surge in “distribution, trading, and other costs,” with Circle’s profit-sharing agreement with Coinbase being the primary factor.

Coinbase and Circle’s partnership dates back to 2018 when they co-founded the Centre Consortium to launch USDC. After the consortium dissolved in 2023, Coinbase received equity in Circle, while Circle gained full control over the USDC ecosystem.

Yet the split did not end the cash flow sharing—the two companies continue to split interest income from the reserves backing USDC. According to Circle’s S-1 filing, the revenue-sharing agreement is as follows:

-

USDC on Coinbase’s platform: Coinbase receives 100% of the reserve yield.

-

USDC on non-Coinbase platforms: Coinbase and Circle each receive 50% of the reserve yield.

As of Q1 2025, about 23% of circulating USDC is held on Coinbase’s platform. This highlights Coinbase’s significant role within the USDC ecosystem and its position as a major custodial platform.

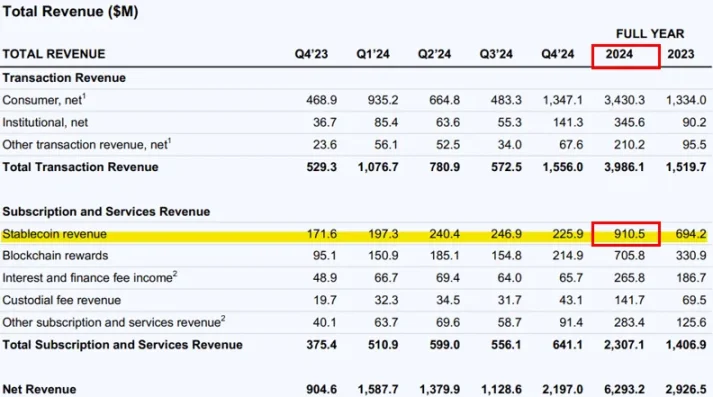

According to data disclosed by Coinbase, the company earned $908 million from USDC-related activities in 2024, accounting for approximately 14.5% of its net income.

Coinbase also retains veto power over Circle’s business partnerships. If Circle wishes to sign new revenue-sharing or distribution agreements with third parties, it must obtain approval from Coinbase.

Some analysts believe these “tight” cooperation terms could lay the groundwork for a potential future acquisition of Circle by Coinbase.

The Hidden “Fatal” Flaw

Beyond high “distribution” costs, Circle’s seemingly bulletproof “money printer” model has serious vulnerabilities.

First, Circle’s revenue is heavily dependent on interest rates. At a 4.75% return rate, $60 billion in USDC would generate roughly $2.85 billion in income—essentially risk-free earnings for Circle.

But when interest rates fall, problems arise. The cost of maintaining these yields (in terms of risk) increases. The temptation to take on excessive risk becomes stronger. Meanwhile, competitive pressures mount as rivals may be willing to sacrifice much of their reserve income to gain market share.

At the same time, Circle’s performance remains tightly linked to the volatile broader crypto market.

In 2022, Circle lost $768.8 million due to the collapses of Terra and FTX. In 2023, after Silicon Valley Bank—the bank partner of Circle—failed, selling pressure on USDC spiked, causing its market cap to halve (coinciding with the timing of the new Coinbase agreement).

Intensifying External Competition

There are no barriers to entry for dollar-backed stablecoins. Providers must be more innovative than competitors to establish their stablecoin as an industry standard.

ARK estimates that by 2030, the stablecoin market could grow from today’s ~$250 billion to $1.4 trillion. This expansion may depend on how much “float income” issuers are willing to share in the form of “incentives” to win or capture market share.

As the regulatory landscape clarifies, Circle may face fiercer competition. Tech giants like Amazon and Google might launch their own stablecoins, while banks such as Bank of America, Citigroup, and JPMorgan Chase are exploring joint stablecoin issuance.

PayPal has already launched its own stablecoin and plans to return most of the reserve yield to users. This race-to-the-bottom trend could compress profit margins across the entire industry.

The Perfect IPO Timing

Despite various internal and external challenges, Circle’s IPO timing couldn’t be better.

Supporters argue that stablecoins are becoming de facto digital dollars—especially amid growing U.S. skepticism toward central bank digital currencies (CBDCs). The potential market for stablecoins spans global remittances, institutional payments, and DeFi integration. Circle’s existing infrastructure and regulatory positioning could give it a first-mover advantage.

As Benjamin Billarant, founder of Balthazar Capital—a fund with significant exposure to crypto-related equities, put it:

“Circle’s IPO timing couldn’t be more perfect. We’ve reached a critical inflection point where stablecoins are gaining mainstream adoption. Once the GENIUS Act passes, it will provide the regulatory clarity needed to unlock their full potential—and Circle, with its compliance-first approach, is uniquely positioned to capitalize on this opportunity.”

In fact, the most comprehensive U.S. stablecoin legislation to date—the bipartisan GENIUS Act—passed the Senate on May 21 and is now under review in the House. This is undoubtedly ideal timing for Circle’s IPO.

The $7.2 billion valuation tells a similar story (Circle’s PE ratio now exceeds that of credit card giant Visa): USDC is just the beginning of tokenization.

While Circle currently depends on demand from the crypto market, stablecoins are poised to become smoother, more efficient payment methods that could go global.

Beyond ordering pizza at home or buying goods overseas, entirely new applications and financial products could be built on this infrastructure. With the Trump administration pushing stablecoins into the mainstream, demand for USDC could expand further, generating additional fee income.

Is the $7.2 billion valuation justified? The market will ultimately decide. But one thing is certain: Circle’s long-term fate hinges on whether it can successfully transition from easy, interest-driven revenue to more challenging, product-driven income.

Selling by Major Shareholders, Buying by Wall Street

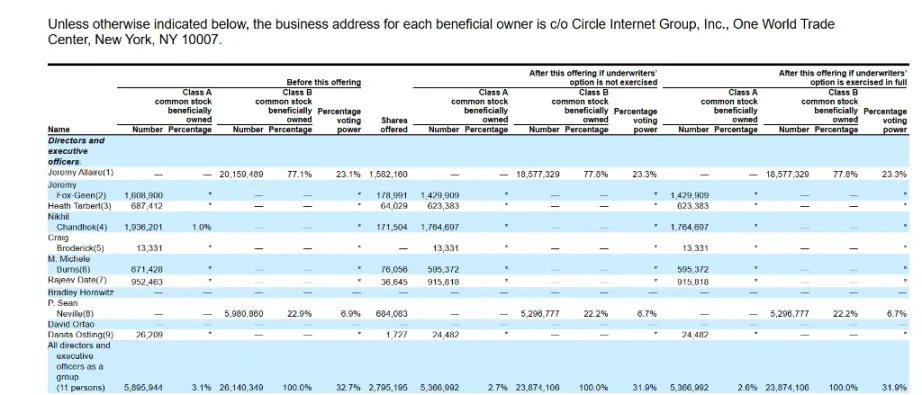

Intriguingly, Circle’s existing shareholders are using this IPO to cash out on a large scale.

According to the prospectus, 60% of the shares being offered come from existing shareholders—far above the typical level for tech IPOs.

Circle CEO Jeremy Allaire will sell 8% of his stake, and several prominent venture capital firms plan to reduce their holdings by around 10%. While insiders will retain substantial ownership, the large-scale exit may send mixed signals to the market.

In tech IPOs, it's extremely rare for existing shareholder sales to exceed newly issued shares by the company.

Meta is one of the few exceptions. During its record-setting 2012 IPO, which raised $16 billion at the time, 57% of the shares sold were from existing shareholders.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News