Beware of Ponzi schemes exploiting the "RWA" concept

TechFlow Selected TechFlow Selected

Beware of Ponzi schemes exploiting the "RWA" concept

True RWA refers to compliant financial products, which currently are only available overseas; ordinary retail investors within the country cannot purchase them.

By: Manqin

RWA Has Been Ruined, the Ponzi Scheme Quintet Is Live

This lawyer has been watching video accounts lately—my eyes are nearly blind. Dozens of accounts hype “RWA tokens” every day. Click in and what do you see? Well well, none of them are legitimate RWA at all—they’ve simply named their own worthless coin “RWA” and started piggybacking on the concept like crazy. Phrases like “empowering the real economy,” “blending virtual with reality,” and “the future of blockchain” roll off the tongue, leaving people dizzy and confused. Even more absurd is that these video accounts follow the exact visual template of a Ponzi scheme:

1. Whiteboard: A slickly dressed “instructor” uses a marker to scribble on a whiteboard, calculating returns and drawing organizational charts as if it were all real.

2. Red banners: The backdrop features large red banners with white text proclaiming events like “Web3 Wealth Summit” or “RWA Global Ecosystem Conference,” looking as festive as Chinese New Year.

3. Display boards: Walls covered in “project introductions” and “global expansion plans,” filled with English jargon and technical terms, plastered on every available surface.

4. Money counters + cash: On-site currency detectors and stacks of red banknotes are displayed prominently, hinting that “you can earn this much if you invest.”

5. Rows of elderly men and women sit below, their eyes shining with “hope for sudden wealth.” Can you even recognize this scene anymore? My years of legal experience tell me—if this isn’t a Ponzi scheme, I’ll eat my keyboard!

Below are some audience-submitted photos from these video accounts—take a look:

(Images above sourced from WeChat video accounts; feel free to self-identify)

Pretending to Be “Web3 Evangelists” While Cutting韭菜

The names of these accounts grow increasingly intimidating—“Web3 Evangelist,” “RWA Evangelist,” “Blockchain Wealth Mentor”—these terms are being so abused they’re turning into insults. They love calling themselves “industry pioneers” and boasting about having “deep expertise in blockchain for ten years,” but when you check, blockchain wasn’t even popular a decade ago—what exactly were you deepening back then? Deepening your P2P scam?

Even more ridiculous: their video account bios all claim “guiding everyone into Web3” and “RWA is the future trend.” But open any video and it’s pure brainwashing:

First, they bombard you with incomprehensible jargon—“staking,” “compound interest,” “smart contracts,” “algorithmic supply-demand balance”—and by the end, all grandma and grandpa remember is: “invest and get rich quick.”

Then they pitch a “once-in-a-lifetime opportunity,” telling you “RWA is the ultimate form of blockchain—miss it and regret forever.”

Finally, they add “limited-time offers,” like “invest 10,000, get 5,000 tokens free” or “30% commission for recruiting others”—straight-up pyramid scheme vibes.

Dude, does life really have such good deals? Real RWA is serious financial product involving asset securitization and regulatory compliance—do you seriously think they’d be shouting about it offline? These so-called “evangelists” don’t understand RWA at all. Their “ecosystem” is just a Ponzi scheme targeting seniors’ pensions.

Why Target Seniors? Because Young People Aren’t Easy to Fool

Have you noticed that the audiences at these Ponzi scheme events are almost exclusively seniors? Why? Because they can’t fool young people! Today’s post-95s and post-00s are fluent in Web3, trading meme coins like pros. They can check a contract address and do basic research to spot a scam coin instantly. Try giving them offline lectures, asking for cash deposits, or pushing referral commissions? Sorry, they’re already out on-chain farming airdrops.

Seniors are different. They’re clueless about blockchain and Web3. Hearing high-sounding terms like “RWA” and “Web3,” their brains register only one thing: “can make big money.” They don’t know how to read whitepapers or analyze on-chain data. When an instructor draws a pie, they believe it. And these schemes are masters at emotional manipulation—phrases like “investing in RWA is building wealth for your descendants” or “not investing means falling behind the times” stir up emotions fast. One surge of excitement, and out come their retirement savings.

Let me say this fairly: seniors aren’t stupid—they just trust “experts” too much. Unfortunately, these “experts” are either ignorant or malicious, exploiting information asymmetry to fleece the elderly. Don’t they feel any guilt?

The Ponzi Playbook: Three Moves + Pyramid Scheme Smell

The套路 of these fake RWA schemes boils down to three classic moves:

Hype: First, blow RWA up as “the ultimate blockchain opportunity,” drown you in fancy jargon until you’re dazed, then declare “this is your last chance to join.”

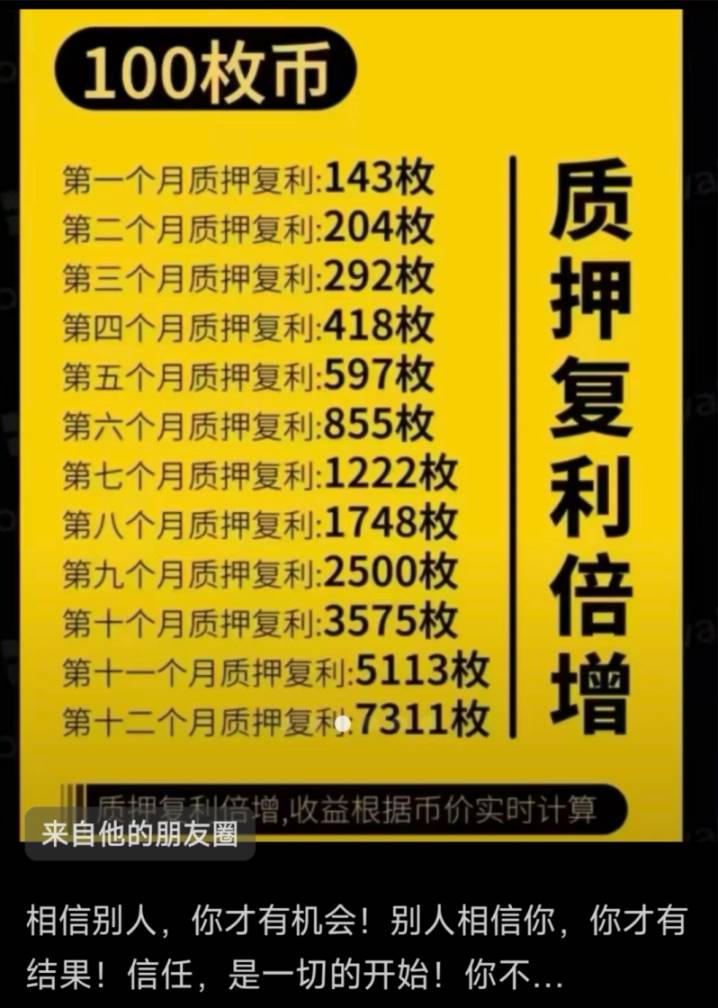

Promises: Calculate insane returns—“50% annual yield,” “double your money in six months”—and show “success stories” that are either Photoshopped or faked backend data.

Pressure: Limited-time offers, referral rewards, team dividends—naked pyramid tactics that force you to pay now and recruit friends and family to “get rich together.”

Worse still, they love “offline experiences.” Rent a hotel conference room, set up money counters and cash stacks, hire actors to shout “I invested 100,000 and already made 500,000!” Seniors see this, blood rushes to their heads, and they hand over cash immediately. Bro, this isn’t investing—it’s jumping into a pit!

Their so-called “RWA tokens” have zero underlying assets. Real RWA, like those issued in Hong Kong, has financial products in the middle layer and valuable, income-generating assets at the base, with clear cash flows and regulatory backing. Your token doesn’t even specify which real-world project it funds—how exactly does it empower the real economy? With your mouth?

How “Criminal” Are These Schemes? Let’s Calculate the Jail Time

As a justice-driven lawyer, I despise these brazen Ponzi schemes most of all. Don’t think wearing an “RWA” disguise makes you untouchable. In China, issuing or promoting virtual currencies—especially running Ponzi schemes—crosses legal red lines. Let’s break down what crimes these people might face and how many years they could serve:

1. Crime of Illegally Absorbing Public Deposits

Don’t think renting a ballroom in a five-star hotel and hiring actors in suits lets you rebrand illegal fundraising as “financial innovation.” According to Supreme Court judicial interpretations, meeting these four criteria constitutes illegal absorption of public deposits:

-

Illegality: Not approved by financial regulators

-

Publicity: Promoted publicly via media, roadshows, etc.

-

Profit inducement: Promising principal protection and returns

-

Social nature: Raising funds from unspecified individuals

Those “RWA evangelists” flooding video feeds—aren’t they all shouting on camera about “principal guaranteed,” “passive income,” and “dynamic rewards”? Some even hold rallies in community centers demonstrating how to exchange RMB for USDT. They might as well tattoo the “four characteristics” on their foreheads and dance in the streets.

Under current sentencing standards, individuals who illegally absorb over 1 million yuan or target more than 150 people face three to ten years in prison. Those organizing “100-city linkups” and “10,000-person summits” might just wear out the prison floor.

2. Crime of Fundraising Fraud

If illegally absorbing public deposits is “blindly charging ahead,” fundraising fraud is “charging ahead with a knife”—the key difference being “intent to illegally possess.” Here are three ways to spot it:

-

Check fund flow: Did the money go to personal or corporate accounts? Was it spent lavishly or transferred away?

-

Verify project authenticity: Are there verifiable underlying assets—like real estate, equity, or supply chain documents?

-

Review team background: Does the founder dare show their face? Use their real name? Publish business license and financial licenses?

For these “RWA Ponzi schemes,” the whitepaper is sloppier than a primary school essay, team bios are full of titles like “blockchain expert” and “Wall Street returnee elite,” yet not a single real photo is shown. Even more laughable: their so-called “real economy empowerment” is just staged photos in a rented co-working space. How is this different from eZubao renting the Diaoyutai State Guesthouse for its launch event?

Under China’s Criminal Law, fundraising fraud involving particularly large amounts (over 5 million yuan) can carry a life sentence. Those who trick seniors into betting their life savings deserve to taste the bitterness of “tears behind bars.”

3. Crime of Organizing or Leading Pyramid Sales Activities

Modern Ponzi schemes have gotten smarter—abandoning “three-tier distribution” for “community consensus”—but the core remains unchanged. If it meets these three traits, it’s just a pyramid scheme in disguise:

-

Entry fee: Must buy coins or stake to participate

-

Recruitment: Must refer others to unlock higher returns

-

Team-based compensation: Earnings directly tied to downline performance

I once saw the incentive structure of an “RWA ecosystem”—impressive in all the wrong ways: 1% daily passive income, 30% direct referral bonus, 10% indirect referral rewards—the compounding model beats even Ponzi’s original scheme. Even better, they run “city node” and “super node” ranking contests, elevating pyramid structures to new blockchain heights.

According to judicial interpretations, if a scheme involves 30+ participants across three or more tiers, criminal prosecution begins. Those team leaders spamming “good news” in WeChat groups might soon be reciting the Anti-Pyramid Scheme Handbook backward.

Last warning: Uncle, give it up! Don’t think hiding behind video accounts keeps you safe. On-chain data, fund trails, promotional records—police can trace everything down to your underwear. You really think the Criminal Code is decoration? Prison meals aren’t as tasty as your promised “50% annual returns”!

Conclusion

Seniors, protect your retirement savings

At this point, I must speak up for seniors: stop embracing “RWA”! These Ponzi “RWA tokens” have nothing to do with real RWA. True RWA consists of compliant financial products, currently only available overseas. Domestic retail investors can’t even buy them. The “RWA” you see on video accounts and offline seminars? It’s just a worthless coin. Your investment will almost certainly vanish.

Seniors, investing isn’t gambling, and blockchain isn’t magic. For financial planning, go to a bank and buy government bonds or funds—safe and steady. Don’t believe lies about “50% annual returns” or “doubling in half a year.” There’s no free lunch—only traps. Protect your retirement savings. Don’t let “Web3 evangelists” steal your life’s work.

To the project teams: Watch your step

Finally, a word to those project teams piggybacking on RWA for Ponzi schemes: Watch your step! Don’t think wearing an “RWA” mask gives you free rein. Every post on video accounts, every message in WeChat groups, every offline seminar—you’re creating evidence. Every token you issue leaves a clear trail on-chain. The police aren’t coming for you yet because the time hasn’t come. When it does, you won’t have time to cry.

Last but not least, we remind all investors—especially older friends—to beware of Ponzi scams disguised under the RWA banner. Always verify a project’s authenticity and legality before investing. Avoid blindly following trends. We also urge regulators to strengthen crackdowns on such fraud to safeguard financial stability and investor rights.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News