Circle is rapidly advancing in the stablecoin race

TechFlow Selected TechFlow Selected

Circle is rapidly advancing in the stablecoin race

Circle is actively expanding across multiple areas including payment networks, banking license applications, and institutional partnerships, while gradually closing the gap with market leader Tether.

Authors: Prathik Desai, Nameet Potnis, Thejaswini M A

Translation: Block unicorn

Introduction

Despite market turmoil caused by former U.S. President Donald Trump’s tariff policies temporarily halting Circle’s上市 plans, the company is now advancing at lightning speed toward its anticipated IPO.

Circle is aggressively expanding across multiple fronts—payment networks, bank charter applications, institutional partnerships—and steadily closing the gap with market leader Tether. Data shows that USDC’s issuer has reduced its market share deficit against Tether from 50 percentage points to just 35.

In today's article, we’ll explore:

-

How USDC is accelerating growth and narrowing the gap with Tether

-

How Circle’s new payment network aims to replace outdated cross-border systems

-

Why Circle and other crypto firms are suddenly racing to apply for bank charters

-

How traditional banks are preparing their counteroffensive against stablecoins

First, let’s examine why the stablecoin race matters beyond the crypto bubble.

The $2 Trillion Stablecoin Race

The competition in the stablecoin space is intensifying. With regulatory clarity emerging, traditional financial giants are preparing to enter—potentially disrupting the current duopoly held by Tether and Circle.

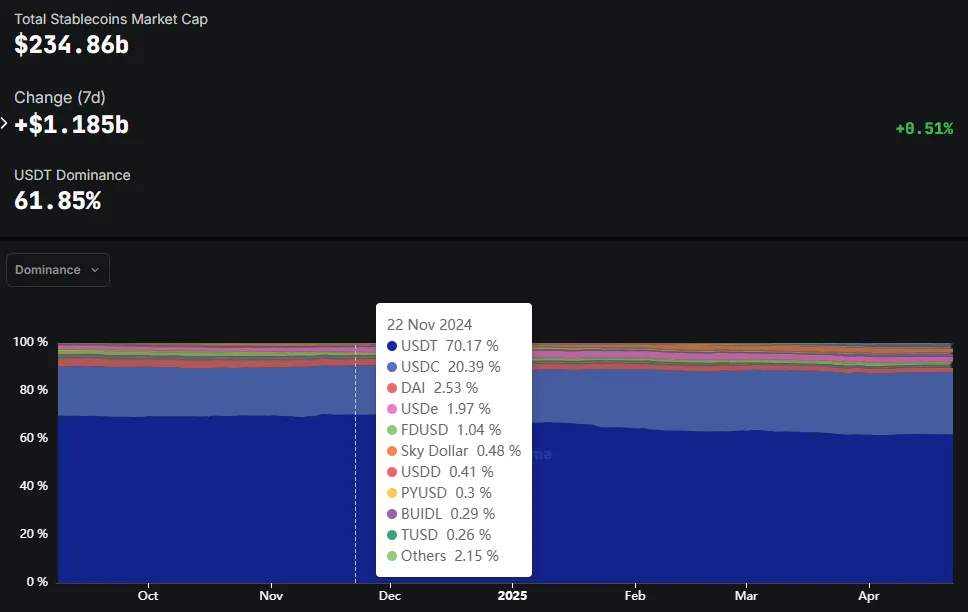

Over the past five months, the combined market share of the two leading stablecoins has declined by 4 percentage points.

"We’re going to see banks issuing stablecoins because they qualify under MiCA," Ran Goldi, Senior Vice President of Payments at Fireblocks, told Coindesk. "By the end of this year, you might see over 50 new stablecoins."

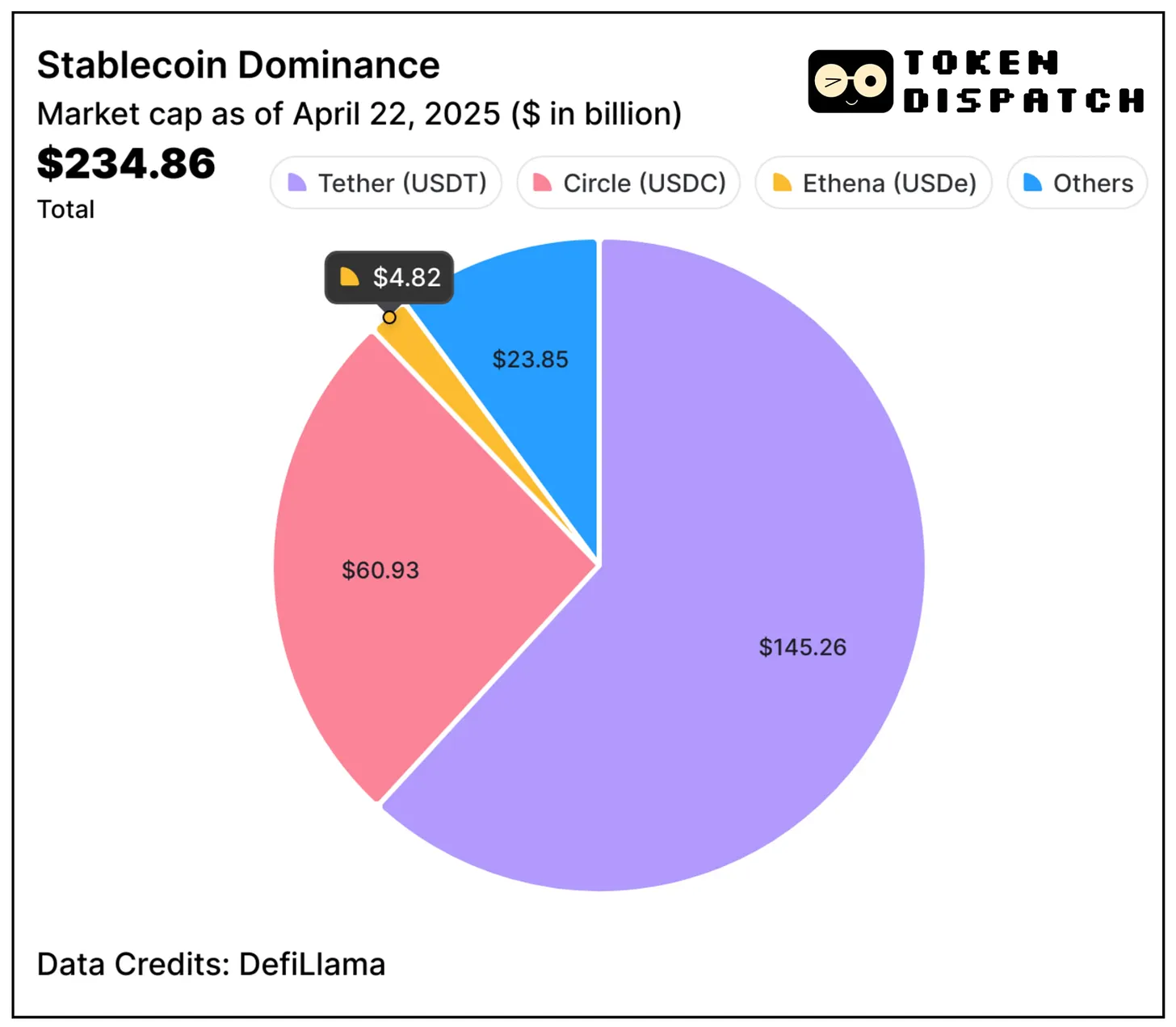

A report from Standard Chartered forecasts that the stablecoin market could surge to a staggering $2 trillion by the end of 2028—nearly ten times the current total supply of $235 billion.

Dozens of banks are privately drafting strategic plans for stablecoin initiatives, with most expected to finalize their strategies by the end of this quarter. "It will be interesting to see whether banks build in-house, use platforms like BNY Mellon that serve banks, or work with providers like Fireblocks," Goldi noted.

This looming competitive threat explains Circle’s urgency across multiple fronts. As traditional financial institutions prepare to enter, the window to solidify market position is rapidly closing.

The Stablecoin Race Heats Up

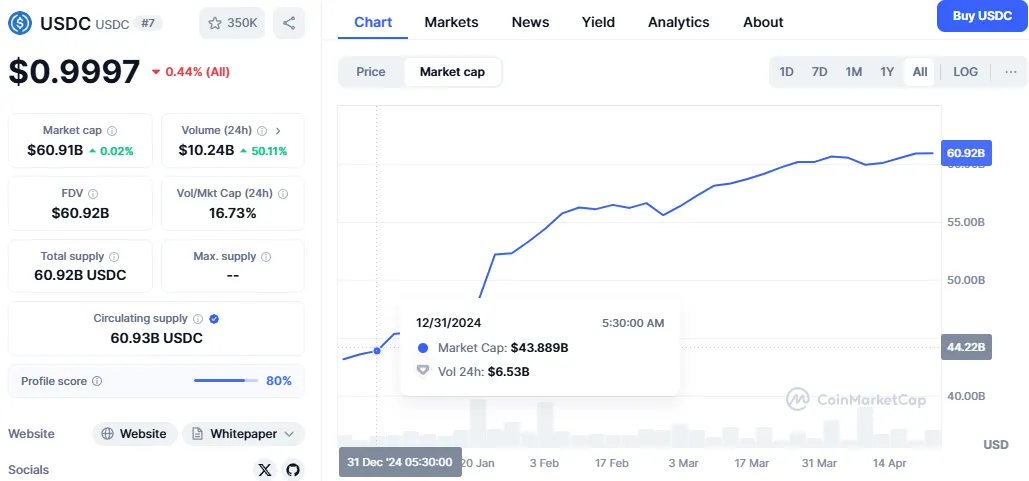

Circle’s intent and rapid execution are clear: as of April 19, USDC’s market cap surged past $60 billion, up $17 billion—or about 40%—from $44 billion at the start of the year.

In contrast, Tether’s USDT saw only an 8% increase in market cap during the same period. While Tether maintains dominance with a market cap nearly 2.5 times larger than USDC’s, the growth gap is rapidly narrowing.

USDT’s market share has dropped nearly 10 percentage points over the past five months to 61.85%, while Circle’s has risen by approximately 6 points.

Data indicates a widening preference gap between the two stablecoins. Regulated entities and DeFi protocols increasingly favor USDC due to Circle’s clear and transparent regulatory framework.

This advantage is most evident in Europe. USDC has obtained licensing under MiCA, enabling it to operate across all 27 EU countries—a region with a combined population of 450 million. USDT does not have this approval.

Regulators aren’t the only challenge to Tether’s continued dominance.

Coinbase CEO Brian Armstrong recently stated the exchange’s new “audacious goal” is to dethrone Tether’s USDT and become the world’s “number one dollar stablecoin.”

Other exchanges, including Kraken and Crypto.com, have also delisted USDT in European markets.

Breaking the Bank Rails

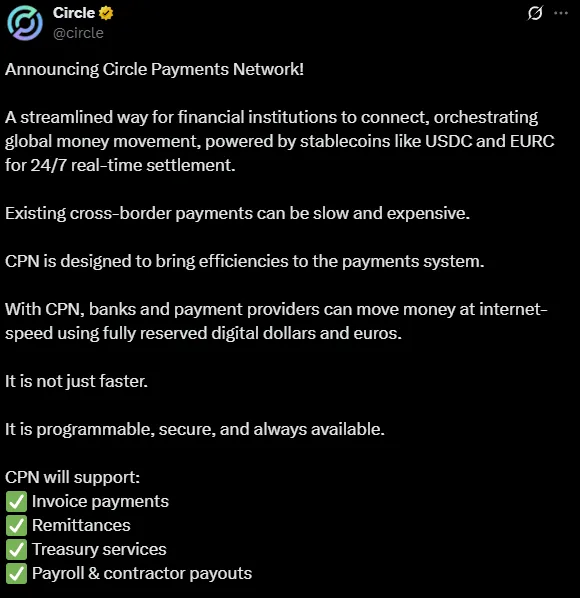

Tuesday marked Circle’s launch of a product designed to reduce the cost and delay of cross-border fund transfers. The Circle Payment Network (CPN) aims to use stablecoins as bridges to dismantle the outdated infrastructure of global finance.

"We're not just building a stablecoin—we're building modern infrastructure for global payments," Circle posted on X.

International bank settlements are notoriously slow, expensive, and constrained by legacy systems that often shut down overnight and on weekends. Circle’s alternative promises instant, 24/7 transfers using fully reserved digital dollars (USDC) and euros (EURC).

Circle has onboarded more than 20 design partners, including dLocal, WorldRemit, BVNK, Yellow Card, and Coins.ph.

This partner lineup signals a clear focus on institutions serving emerging markets and high-volume remittance corridors—areas where traditional banking performs particularly poorly.

Circle’s network initiative rests on a simple yet fundamental premise: transforming a stablecoin issuer into a key financial infrastructure provider capable of moving these assets at scale.

"Circle is launching a payment network initially targeting remittances but ultimately aiming to compete with Mastercard and Visa," said a source familiar with the matter.

Bank Moves

Alongside its payment network launch, Circle is preparing to clear a major regulatory hurdle by applying for a U.S. bank charter or license, according to The Wall Street Journal.

But Circle isn’t alone. BitGo—the custodian behind the Trump family’s USD1 stablecoin—as well as Coinbase and Paxos, are pursuing similar paths. The timing coincides with evolving U.S. stablecoin regulations that may soon require issuers to obtain licenses.

Why pursue a bank charter now?

A bank charter would allow Circle to operate like a traditional bank, potentially including accepting deposits and issuing loans.

But it comes at a steep cost. Anchorage Digital reportedly spent millions of dollars complying with regulatory requirements after securing a federal charter.

Yet the payoff could be immense: access to a Federal Reserve master account—the so-called “holy grail” that crypto-native banks like Custodia have long sought but failed to achieve. Such access would give Circle the closest possible link to the U.S. monetary supply available to financial institutions.

Our Take

Circle’s multi-pronged strategy reveals ambitions far beyond mere pre-IPO positioning—it represents a deep effort to bridge the gap between traditional finance and crypto, a leap no other stablecoin issuer has successfully made.

Circle’s institution-grade payment network, bank charter aspirations, and USDC’s regulated status collectively form an unprecedented moat against both Tether and incoming traditional financial competitors. By establishing strong foundations across diverse domains, Circle is creating significant differentiation from rivals.

Notably, Circle’s focus on emerging markets and remittance corridors stands out. While competitors battle for dominance in mature Western markets, Circle is quietly building infrastructure in regions where financial inclusion remains out of reach.

Its partner list—dLocal (Latin America), WorldRemit (Africa and Asia remittances), Yellow Card (Africa), Coins.ph (Philippines)—reads like a roadmap to the next generation of remittance markets.

Compared to Tether, MiCA licensing may be Circle’s most underrated asset. Gaining regulatory access to 450 million European users is undoubtedly a winner-takes-all opportunity.

Circle’s strategy reflects an understanding of a fundamental truth: victory in the stablecoin wars depends not only on market share but also on infrastructure, regulatory positioning, and institutional integration.

Circle knows it can’t surpass Tether’s market cap in the short term—so instead, it’s building an entirely different arena where Tether, despite its size, cannot effectively compete.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News