The More Powerful AI Becomes, the More Valuable McDonald’s Becomes

TechFlow Selected TechFlow Selected

The More Powerful AI Becomes, the More Valuable McDonald’s Becomes

The world’s smartest money is buying the world’s dumbest companies.

Author: David, TechFlow

At the start of 2026, AI sent shockwaves through capital markets.

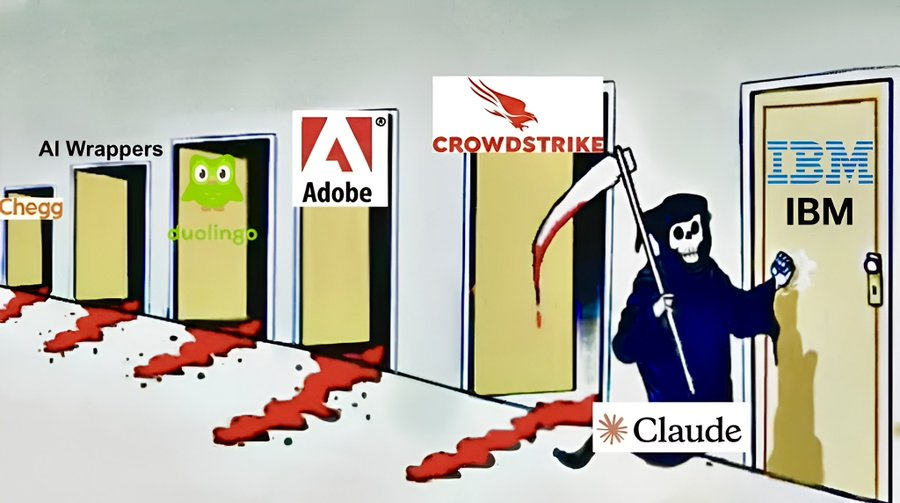

It’s not that AI doesn’t work—it works too well. So well that every new product launch triggers a stock collapse in an entire industry.

For instance, throughout February, Anthropic—the parent company of Claude—rolled out four major AI product updates. When AI began automating enterprise workflows, SaaS software stocks collapsed; when AI started automatically scanning code for vulnerabilities, cybersecurity stocks plummeted; when AI helped banks rewrite decades-old legacy code, IBM plunged 13% in a single day—erasing $31 billion in market value, the largest one-day loss since the 2000 dot-com bubble.

Within one month, multiple industries were individually targeted.

Panic is contagious.

Duolingo, the online education platform, peaked at $544 per share in May last year—but by late February this year, its share price had fallen below $85, losing over 80% of its value. The iShares U.S. Software ETF has declined 22% year-to-date and is down 30% from its all-time high...

A trader told Bloomberg that software stocks have been under relentless selling pressure—just a media headline declaring “AI Will Disrupt XX” can trigger a mini flash crash.

Money is fleeing these companies—but it must go somewhere.

Investing along the AI chain is one option—buying NVIDIA, computing power, infrastructure… But this path is already overcrowded—and growing increasingly expensive.

Some investors are now asking another question: Are there companies so fundamentally resilient that no matter how far AI evolves, they remain unkillable?

HALO Fires the First Shot Against AI Anxiety

In early February, a man named Josh Brown published an article on his blog.

Brown is CEO of a U.S. asset management firm and a frequent guest on CNBC—essentially a financial influencer. In his article, he coined a term:

HALO.

Heavy Assets, Low Obsolescence—i.e., heavy assets, low obsolescence risk.

The idea is simple: invest in companies that AI simply cannot displace, no matter how advanced it becomes.

He also provided a straightforward identification method: the sole litmus test for HALO stocks is, “Can you replicate this company’s product by typing a few words into a prompt box? If not, it qualifies as a HALO stock.”

He gave an example.

Delta Air Lines and Expedia both operate in the travel sector. This year, Delta rose 8.3%, while Expedia fell 6%. What’s the difference?

AI can help you find the cheapest flight—but you still need to board the plane. Delta owns aircraft; Expedia only offers a search box.

He added that this is the simplest investment logic he’s ever encountered.

For the past 15 years, Wall Street has favored light-asset models. Software companies require no factories or inventory; code replication costs virtually nothing, and profit margins are astonishingly high. Now, however, AI has arrived—and AI excels precisely at replacing businesses whose profits rely on code and information asymmetry.

Fortunes shift: “Heavy” is back in vogue.

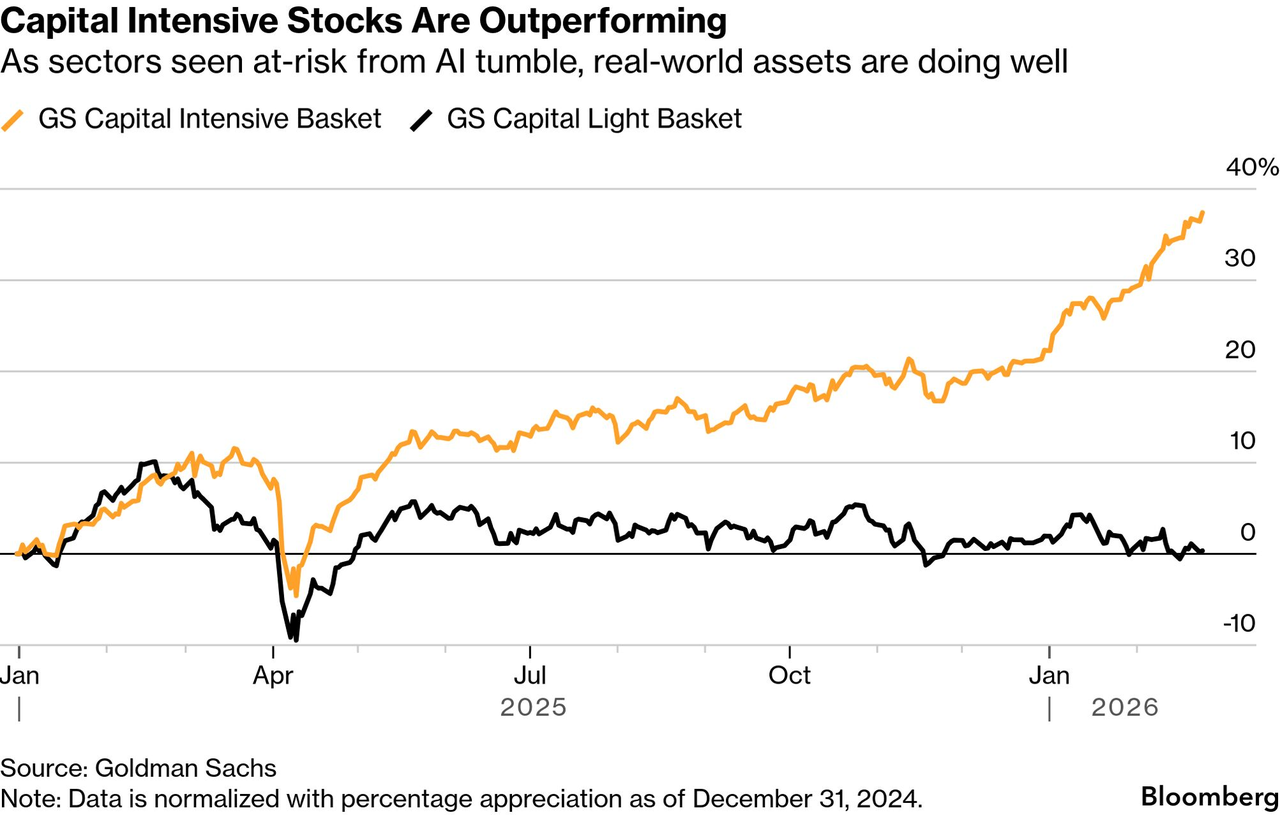

Within weeks of HALO’s emergence, Goldman Sachs issued an official research report titled “The HALO Effect.” Its data shows that Goldman’s “heavy-asset” stock portfolio has outperformed its “light-asset” portfolio by 35% since the start of 2025.

Soon after, Morgan Stanley’s trading desk began recommending HALO-aligned stocks to clients; Barclays and Bank of America incorporated the term into their research notes. Axios, The Wall Street Journal, and CNBC all ran concentrated coverage...

A term casually invented by a blogger became Wall Street’s biggest trading theme of 2026.

What does this signify? Not that Brown is exceptionally brilliant—but rather, that investors are genuinely panicked. So panicked, they need a label to reassure themselves:

Don’t worry—while AI is disrupting many things, a category of companies remains safe.

The World Is a Massive Heavy-Asset System

Do you think HALO is merely a narrative? Capital markets have already begun voting with their money.

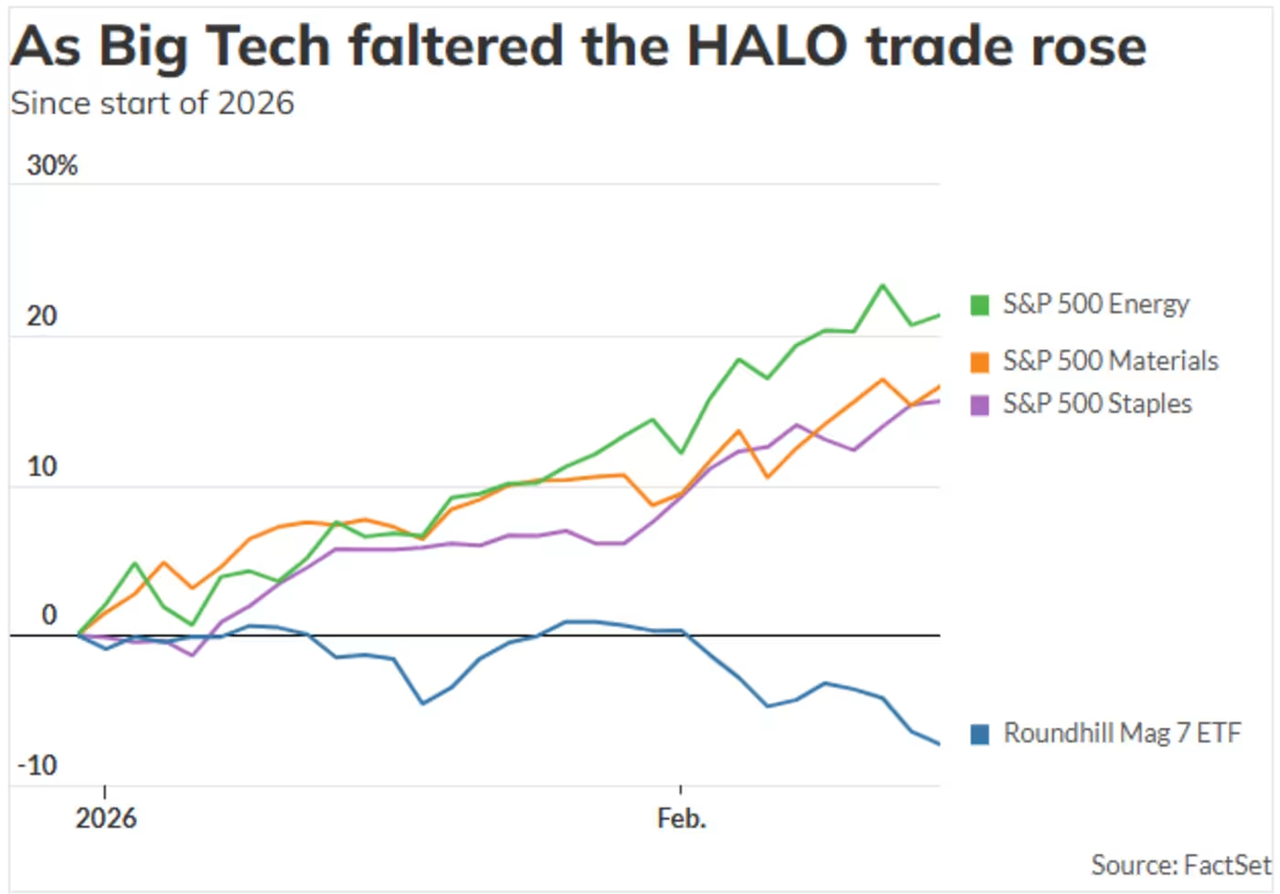

From the start of 2026 through late February, the S&P 500 Energy sector rose over 23%, Materials climbed 16%, Consumer Staples gained 15%, and Industrials rose 13%.

Meanwhile, the Information Technology sector fell nearly 4%, and Financials dropped nearly 5%.

At the same time, the U.S. tech “Magnificent Seven”—Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla—collectively stalled. Only two posted gains year-to-date.

Investors’ concern is whether these firms—spending hundreds of billions annually building compute infrastructure—will ever recoup their investments.

So which specific companies are rising?

McDonald’s, Walmart, ExxonMobil—burger sellers, supermarket operators, oil refiners. AI can write poetry, program software, and even argue legal cases—but it cannot fry french fries or drill for oil.

Anheuser-Busch’s beer stock has risen 48% year-to-date—after all, you can’t drink AI.

Thus, HALO represents a fundamental reversal in capital markets’ valuation logic amid AI anxiety. The last such reversal occurred in 2000.

Back then, investors fled technology stocks en masse, rushing into “boring” sectors like energy, industrials, and consumer staples. The Nasdaq fell nearly 80% between 2000 and 2002, while the S&P Energy sector rose nearly 30% over the same period.

But there’s a crucial distinction. The dot-com bubble burst because the internet wasn’t profitable—the story ran out of steam. This time, the situation is different:

AI is simply too capable—so capable it inspires fear.

Panicked reactions to AI’s technical failure would be unsurprising—but panic triggered by AI’s success is unprecedented in capital markets history.This has almost no historical precedent.

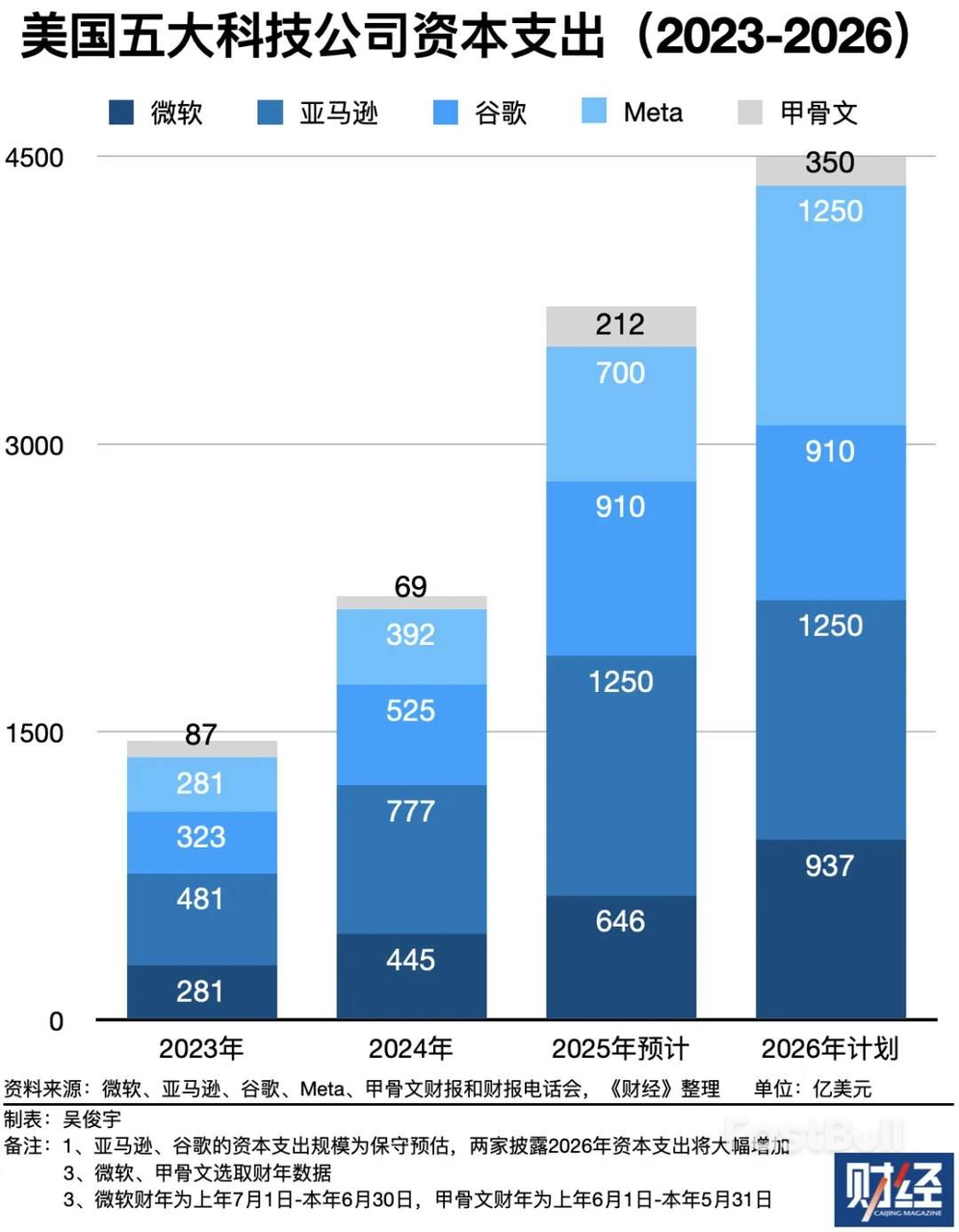

More ironically, AI companies themselves are becoming heavier.

Goldman Sachs specifically noted in its report that the firms most devoted to light-asset models over the past several years are now historically the largest capital spenders.

The five major tech giants are projected to spend $1.5 trillion in capital expenditures from 2023 to 2026—with over $450 billion alone in 2026, exceeding their total historical pre-AI-era spending combined.

Source: Caijing

Where is this money going? Data centers, chips, cables, cooling systems, and power-generation facilities—all physically heavy, expensive real-world assets.

So you get a surreal picture:

AI shatters others’ light-asset models—then transforms itself into a heavy-asset business.

Companies claiming to disrupt the old world ultimately discover they need exactly the same things the old world relied on: factories, electricity, pipelines…

Wall Street spent 15 years chasing “light”—only to realize even AI itself cannot escape “heavy.”

America Hides in McDonald’s; China Orders via Qwen

Meanwhile, across the Pacific, we’ve delivered a completely opposite answer.

In late February, Bloomberg published a report titled roughly: “China’s Market Resists Global AI Panic Trading.” One line in the article struck me as particularly incisive:

U.S. markets focus on what AI will take away; Chinese markets focus on what AI can enable.

Same technology—two diametrically opposed sentiments.

While U.S. investors coin the term HALO and flee to McDonald’s and Walmart, Chinese investors rush to buy AI application stocks.

JPMorgan assigned “Buy” ratings to MiniMax and Zhipu AI in February; Goldman Sachs simultaneously initiated “Buy” recommendations for Biren Technology and Muxi Integrated Circuits; Bank of America analysts stated that AI Agents and their commercialization may be China’s biggest investment theme in 2026.

No one worries Tencent or Alibaba will be killed by AI—investors instead ask whether they can leverage AI to earn more.

Goldman Sachs’ January report identified Tencent as China’s largest beneficiary of AI adoption across internet services—its gaming, advertising, fintech, and cloud businesses are all being accelerated by AI.

Why do the two sides react so differently to the same wave?

U.S. tech stocks have soared to such lofty valuations over the past decade that even minor AI-driven margin pressure makes them unsustainable. Meanwhile, Chinese tech stocks have just emerged from a two- to three-year trough—already cheap, AI represents upside, not threat.

Yet stock prices alone don’t explain everything—the deeper difference lies in the soil.

Just as the HALO narrative surged across U.S. equities, China celebrated its most AI-saturated Spring Festival in history:

VolcEngine became the exclusive AI cloud partner of CCTV’s Spring Festival Gala; Doubao secured an exclusive partnership with CCTV’s Gala; Qwen sponsored the galas of Dragon TV, Zhejiang TV, Jiangsu TV, and Henan TV; Tencent Yuanbao distributed RMB 1 billion in red envelopes; Baidu Wenxin distributed RMB 500 million. Alibaba went further—launching a RMB 3 billion “Spring Festival Hospitality Plan,” where Qwen helps users order milk tea, delivering 1 million orders within three hours…

Source: Sina News | Tushishi

The four major tech firms collectively spent over RMB 4.5 billion on Spring Festival AI marketing.

Ten years ago, WeChat and Alipay competed for red envelopes during the Gala. Today, Doubao and Qwen have taken their place.AI companies aren’t treating the Gala as an ad slot—they’re using it as a public education platform to introduce AI to mass consumers.

The same fire: disaster on dry timber, warmth on damp wood.

Amid the same AI wave, U.S. capital flees companies vulnerable to AI disruption and pours into “AI-proof” firms; Chinese capital chases companies adept at leveraging AI.

One side races forward; the other retreats. In my view, the retreating side may already be overpriced.

The current situation is that AI’s capabilities are fairly priced—but its disruptive potential is overpriced. Money flooding into HALO stocks reflects anticipation of who AI will eliminate—and preemptive flight.

Investors flee to McDonald’s, Anheuser-Busch, and Walmart—solid companies, certainly. But how much of their 2026 gains reflect actual earnings versus fear-driven premiums?

Wall Street’s pendulum has always swung excessively. In 2000, everything .com was deemed valuable; in 2002, everything .com was dismissed as a scam. Now, even beer and tractors are seen as AI-proof.

Once this consensus becomes sufficiently crowded, the next excessive swing won’t be far off.

As for my own view:

AI is indeed growing stronger—this is indisputable. Yet the gap between “growing stronger” and “killing an entire industry” is far wider than most assume.

Every technological revolution follows the same script: first panic, then overreaction, and finally realization that the supposedly doomed sectors never truly died—instead, they became cheaper due to panic.

The internet didn’t kill Walmart—Walmart embraced e-commerce. Mobile payments didn’t kill banks—banks launched apps.

What AI will truly kill are companies that never should have existed in the first place—those lacking product moats, relying solely on funding for growth, surviving purely on information asymmetry.

These companies don’t need AI to eliminate them—economic cycles will.

So perhaps the real question isn’t “Will AI disrupt the world?” Instead, each of us should ask: Does the company I’m investing in possess the ability to wield AI as its weapon—not its obituary?

Those who can answer that question need no HALO.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News