Market in Downturn: Re-evaluating Hyperliquid's Fundamentals and Valuation

TechFlow Selected TechFlow Selected

Market in Downturn: Re-evaluating Hyperliquid's Fundamentals and Valuation

Hyperliquid is expected to become the leading trading and liquidity hub for all on-chain activities.

Author: Vikram Singh

Translation: TechFlow

We are experiencing shocks in both stock and crypto markets due to challenging macroeconomic conditions. In this context, I believe it's essential to step back and refocus on fundamentals. Price declines cleanse the market of speculators while creating entry opportunities for new "first-principles" investors. Assets like HYPE, in particular, have a large portion of holders who are perpetual contract traders (related to the nature of its airdrop distribution). As a result, during market downturns, these perpetual traders may be forced to liquidate their HYPE positions due to margin calls, triggering broad-based selling pressure across the market. However, from another perspective, volatile markets typically generate higher trading volumes, leading to increased fee revenue—making HYPE more attractive to fundamental investors.

Here’s what we’ll explore:

-

Why I’m excited about Hyperliquid today?

-

Hyperliquid from a long-term perspective

-

Potential headwinds

-

HYPE comparative valuation model

Why I'm Excited About Hyperliquid Today?

I believe an efficient on-chain order book can significantly improve existing trading paradigms. Markets should be gathering places for investors under equal conditions, but today’s markets fundamentally favor institutions and high-frequency trading (HFT) firms. On-chain order books change that dynamic, and Hyperliquid is the tool enabling this transformation.

In traditional finance, HFT firms spend millions just to move their servers closer to exchange data centers, while ordinary users must spend thousands setting up and maintaining their own infrastructure. Similarly, centralized crypto exchanges create unfair playing fields through internal market-making agreements and privileged server hosting. By providing access to order flow via an on-chain order book, Hyperliquid allows anyone to build their own “Citadel” or “Jane Street” at nearly zero cost. Additionally, Hyperliquid’s powerful and user-friendly SDK offers non-native crypto users an accessible way to experiment with trading strategies.

While average users may not outperform Wintermute in market making, at least they now have a fair chance—something current systems don’t even allow. Users can also leverage Hyperliquid’s native market-making treasury, HLP, earning approximately 10%-20% annual percentage yield (APY) in USD.

Through these mechanisms, Hyperliquid creates a fairer market. The following upcoming features particularly excite me:

-

Non-custodial BTC/SOL/ETH and related applications

Users need an on-chain platform to trade and collateralize BTC. Through @hyperunit, Hyperliquid provides a seamless way to bridge BTC onto its on-chain platform. With low-latency settlement support for spot and perpetual contracts, I anticipate use cases such as on-chain spot-futures arbitrage, spot hedging, and real-time options position settlement.

-

Stocks and other real-world assets (RWAs) + Hyperliquid backend / traditional finance frontend

The Unit team is developing solutions to bring stocks and RWAs onto the Hyperliquid order book. I’m not only excited about the demand for this on-chain, but also about Hyperliquid serving as blockchain and liquidity infrastructure that brings previously inaccessible financial opportunities to emerging markets (EMs). For example, users outside the U.S. might gain seamless access to Apple (AAPL) stock via Hyperliquid’s order book backend without needing to interact directly with blockchain complexity.

-

BTC and HYPE as collateral

Currently, Hyperliquid only accepts USDC as collateral for perpetual contracts. Allowing BTC and HYPE as collateral would reduce sell pressure caused by margin calls and increase capital efficiency.

-

Native USDC support

Currently, Hyperliquid supports Arbitrum-bridged USDC, but because it’s locked within smart contracts, this version cannot be directly redeemed into dollars and must be bridged back to Arbitrum. Moreover, bridged USDC isn't compatible with the CCTP protocol. Deploying native USDC would unlock greater capital efficiency. For more insights on native USDC or other native stablecoins on Hyperliquid, read the thread by @0xBroz here.

-

Lending market launch

The introduction of a lending market will boost activity, as HYPE airdrop recipients could borrow against their HYPE holdings and participate more actively in the ecosystem. I look forward to seeing multiple lending protocols, including @felixprotocol, go live.

-

Direct deposits and withdrawals

Solutions like @HanaNetwork will enable users to deposit and withdraw directly using Apple Pay, PayPal, Wise, and debit cards. Lowering onboarding barriers will drive more market participation.

-

Bringing non-crypto users onchain

Hyperliquid was the first crypto app many of my non-crypto friends used. Most were drawn in through trading competitions hosted by @pvp_dot_trade, and even after the points program ended, they remain loyal users.

Long-Term View: Hyperliquid’s Future Potential

Given the above factors, I believe Hyperliquid has the potential to become a strong magnet for liquidity. As we've repeatedly seen in crypto, liquidity attracts more liquidity. Therefore, I expect Hyperliquid to emerge as the leading trading and liquidity hub for all on-chain activities.

As discussed earlier, the introduction of native non-custodial BTC will unlock new opportunities where efficient central limit order books (CLOBs) meet BTC liquidity—including deeper CLOB liquidity, EVM-based automated market makers (AMMs), and lending pools. We may also see spot ETH/SOL and other altcoins migrate to Hyperliquid, capturing market share from DEXs on other chains and potentially draining liquidity from their order books and pools.

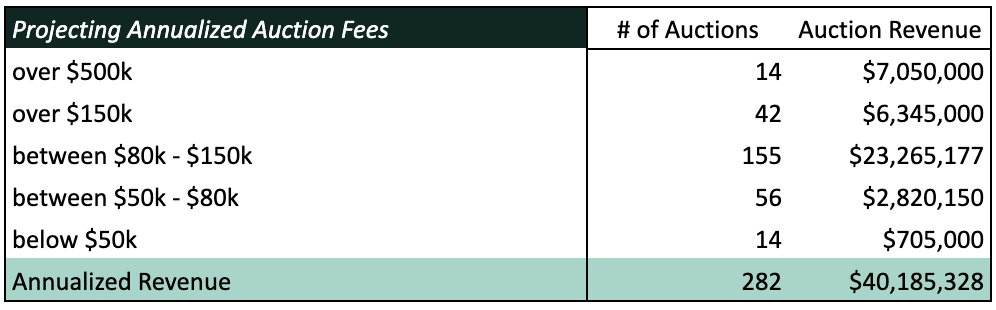

I believe Hyperliquid will begin competing with centralized exchanges (CEXs) in **token listings**. This has already been demonstrated by projects like Swell and Plume purchasing ticker symbols on Hyperliquid. Since ticker auctions occur every 31 hours, there are roughly 282 auctions per year at most. As Hyperliquid becomes the de facto on-chain trading venue, “tickerspace” will grow increasingly valuable—though likely still cheaper than paying Binance 5% of a token supply. If Hyperliquid succeeds as a liquidity center, I estimate the average ticker auction price could reach around $500,000.

As previously mentioned, combining Hyperliquid’s backend with retail-focused frontends could bring unprecedented financial access to non-U.S. markets and unlock liquidity from user segments currently untouched by the crypto industry.

Potential Headwinds

-

Regulatory pressure

Hyperliquid hasn’t aligned itself with U.S. political circles (MAGA), unlike other chains that have gained favor by courting Washington politicians—a trend clearly illustrated by World Liberty Finance’s token purchases. Additionally, many VCs have invested in competing chains and DEXs, and since Hyperliquid is siphoning liquidity and attention from those platforms, these investors have criticized Hyperliquid’s regulatory legitimacy since its inception. Lacking strong support in the U.S., Hyperliquid may face regulatory scrutiny.

-

EVM deployment quality

The EVM testnet launch quality has lagged behind HyperCore, suffering from low gas limits, occasional block time delays, and lack of native USDC. These issues slow down application deployment. If EVM apps fail to deliver novel functionality or if total value locked (TVL) and trading volume remain low, attention and TVL could shift to other L1s/L2s like Monad or MegaETH. That said, based on conversations with developers, the Hyperliquid team is actively collaborating with dApps, gathering feedback, and iterating quickly.

-

Validator network transparency

Although Hyperliquid is transitioning toward a permissionless validator system, the specific operations validators perform are still obscured by opaque binary code. To become a secure liquidity hub through genuine decentralization, Hyperliquid needs to gradually increase transparency around validator actions.

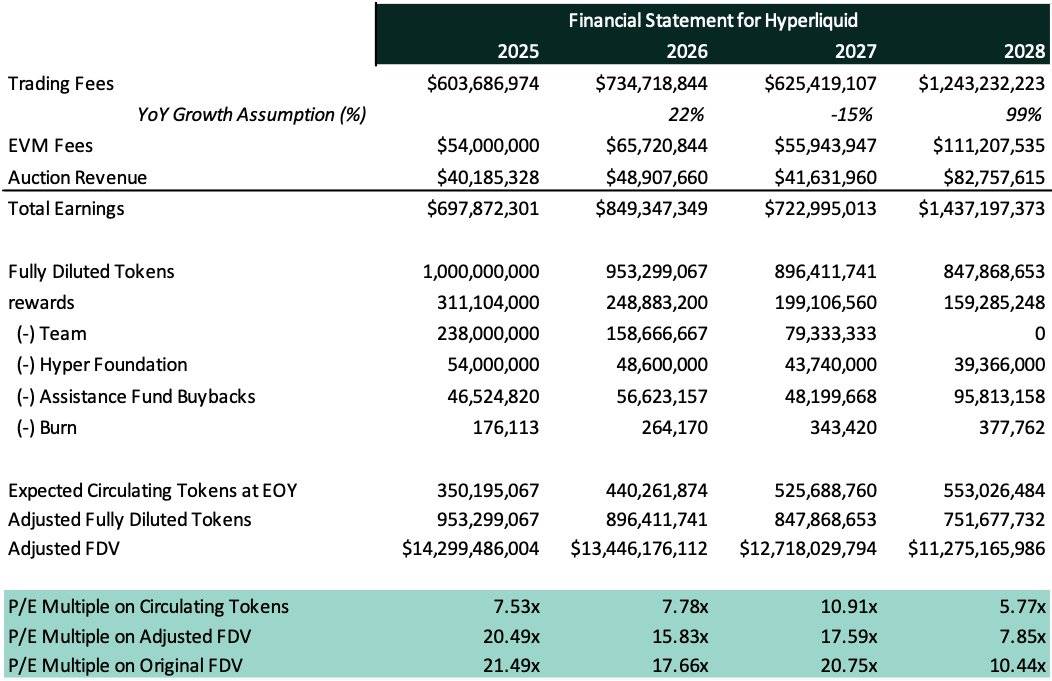

HYPE Comparative Valuation Model

Below is a simple price-to-earnings (P/E) analysis of Hyperliquid’s native token HYPE over the next four years.

I believe it's important to contextualize the impact of Assistance Fund buybacks. Inspired by analysis from @Keisan_Crypto, we introduce the concept of “Adjusted Fully Diluted Valuation” (Adjusted FDV), calculated as:

Adjusted FDV = Price × Adjusted Fully Diluted Supply.

We define next year’s adjusted fully diluted supply as:

Last year’s fully diluted supply – Assistance Fund buybacks – Burns.

For those unfamiliar: fees collected by Hyperliquid go into the Assistance Fund, which buys back HYPE from the open market, reducing supply. In this analysis, we assume repurchased HYPE tokens will never re-enter circulation—functionally equivalent to burning.

Hyperliquid’s revenue streams fall into three main categories: trading fees, EVM fees, and auction fees.

Note: The following calculations assume a HYPE price of $15.

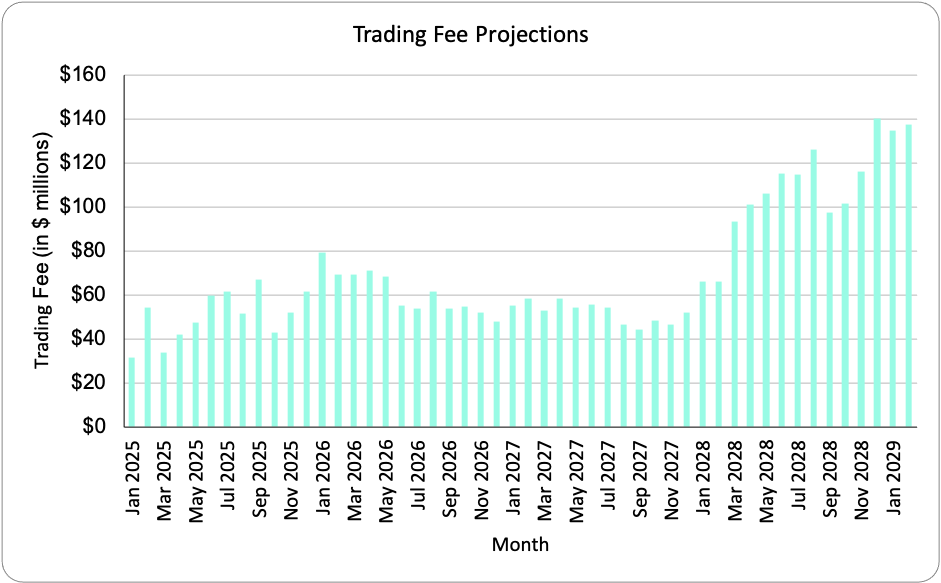

Trading fees are charged when users open or close perpetual (“Perps”) positions. To forecast annual trading fee revenue, I first gathered weekly revenue data from December 23, 2023, to March 10, 2024. Then, I annualized the 4-week rolling average weekly income and performed eight such annualizations to arrive at a balanced estimate of trading fees.

Thus, I estimate Hyperliquid’s trading fee revenue in 2025 will be approximately $600 million.

However, while this method provides a reasonable benchmark for 2025, projecting year-over-year growth from 2025 to 2028 is difficult using this approach alone. Instead, we turn to smoothed historical data on CEX perpetual trading volumes and assume Hyperliquid captures a certain percentage share of total CEX volume. This better reflects the cyclical nature of crypto trading volumes. We further assume Hyperliquid’s market share falls within a defined range each year. Assuming a fixed 5% share in any given year could introduce significant error, so we model 2025 market share between 3%–6%, randomized via the formula: 3% + [(6%–3%) × RAND()]. This range-based randomization yields a more realistic monthly volume capture. Assuming an average trading fee rate of 0.025% of volume, we conclude Hyperliquid will earn ~$600 million in trading fees in 2025. Notably, this aligns closely with our earlier 4-week rolling average estimate, reinforcing our analysis.

Extending this volume capture analysis, we assume Hyperliquid’s market share grows gradually over time. Thus, we project market share ranges of 3%–6% in 2025, 6%–8% in 2026, 8%–10% in 2027, and 10%–12% in 2028. Our findings are summarized below.

We treat EVM fees as a function of annual revenues from other Layer 2 networks like Base. Given HypeEVM’s early stage and naturally lower gas costs, I expect HypeEVM to capture 50% of Base’s annual revenue in 2024. Hence, I estimate Hyperliquid will earn ~$54 million in EVM fees in 2025.

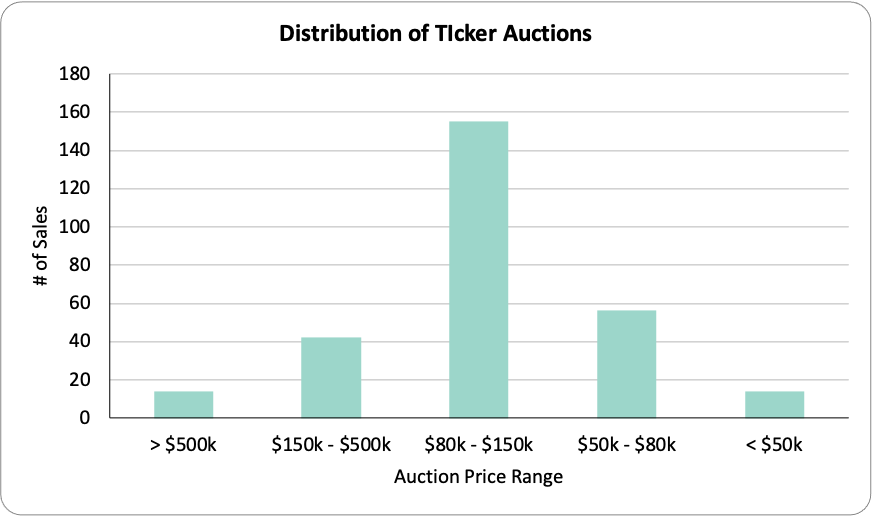

Finally, Hyperliquid holds auctions for ticker symbols in its spot markets. To estimate auction-derived revenue, we analyze the distribution of historical ticker prices. Based on historical data and our prior theory on tickerspace, a normal distribution adequately maps one year of auction pricing. The charts below illustrate the price distribution and revenue contribution across price tiers. Accordingly, I estimate Hyperliquid will earn ~$40 million in auction fees in 2025.

In aggregate, Hyperliquid’s total revenue in 2025 is projected to be approximately $700 million. Since most of these fees are expected to flow into the Assistance Fund for HYPE buybacks, this implies ~$700 million in buying pressure for HYPE in 2025.

Assuming Assistance Fund-held HYPE is effectively burned (never re-entering circulation), plus 176,113 HYPE tokens expected to be burned from HyperCore trading fees, approximately 46 million HYPE tokens will be removed from circulation in 2025.

Therefore, with rising revenues and shrinking supply, HYPE’s price-to-earnings (P/E) ratio will decline over the coming years, making it a more valuable asset over time. Furthermore, this regular removal of HYPE from circulation helps absorb selling pressure from future unlocks of tokens held by the Hyper Foundation, team, and community reward programs.

We assume EVM and auction fee growth rates broadly track trading fee growth. This allows us to compile the final financial projection table as shown below:

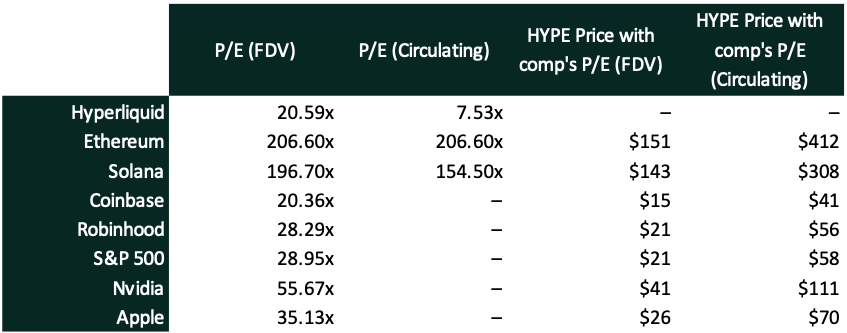

Lastly, we compare HYPE’s P/E ratio—based on both fully diluted valuation (FDV P/E) and market cap (Market Cap P/E)—against the following assets: crypto competitors such as Solana and Ethereum; relevant equity assets like Coinbase and Robinhood; and traditional financial assets including Apple, Nvidia, and the S&P 500 Index.

PS: A Quick Thought on the Hyperliquid Community

I’ve written extensively on Twitter about the Hyperliquid community, so I won’t elaborate too much here to stay focused. But I’d like to share an excerpt from an earlier tweet that captures my sentiment well:

“Whether I make money or lose money, I’ve made new friends. Hyperliquid is the first crypto app where I’ve experienced this—and to me, that’s a critical feature.”

If you’re interested in my broader thoughts on the Hyperliquid community, check out Vikram Singh for more.

Also, regarding community building, credit must go to @HypioHL, who’ve done an outstanding job fostering a strong community around NFTs (I never thought I’d say that about NFTs).

Final Note

Zoom out, sit back, relax, and enjoy the ride (but don’t sell your HYPE due to forced liquidations).

Special thanks to @Keisan_Crypto for inspiring the valuation framework, and to @0xBroze, @rpal_, and @0xDuckworth for suggestions and proofreading!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News