From Livermore to Crypto Whales: A Century-Spanning Shadow Battle in Trading, Decoding the 300 Million Dollar Order and the Game of Attack and Defense Behind Hyperliquid

TechFlow Selected TechFlow Selected

From Livermore to Crypto Whales: A Century-Spanning Shadow Battle in Trading, Decoding the 300 Million Dollar Order and the Game of Attack and Defense Behind Hyperliquid

This time, the market king once again executed a massive trade successfully, and proactively triggered liquidation amid insufficient market liquidity, pulling off an extreme maneuver that sparked widespread admiration in the market.

Author: Frank, PANews

“Throughout all the days of my life as a stock operator, this day remains the most vivid in my memory. It was the first time my profit exceeded one million dollars. It marked the first successful execution of a trade according to a pre-planned strategy. Everything I had foreseen had now become reality. But beyond all that—my wildest dream had come true.

On this day, I was the king of the market!”

—— *Reminiscences of a Stock Operator*

Over a century ago, legendary stock trader Jesse Livermore described his triumph with these words. A hundred years later, in the crypto markets, a similar scene appears to be repeating itself. Coincidentally, today’s “market king” is also a large-scale operator who succeeded spectacularly—intentionally triggering liquidation amid insufficient market liquidity, pulling off an extreme maneuver that has drawn widespread admiration. The difference? This time, the exchange paid the bill for the whale’s profit.

Century Revisited: The Wall Street Ghost Reborn On-Chain

This whale—who previously invested $6 million at 50x leverage to go long ETH and BTC just before Trump announced plans to include BTC, ETH, SOL, ADA, and XRP in a national crypto reserve, ultimately earning $6.8 million—has been actively trading over the past month with significant gains, culminating in another legendary play worthy of Hyperliquid’s history books.

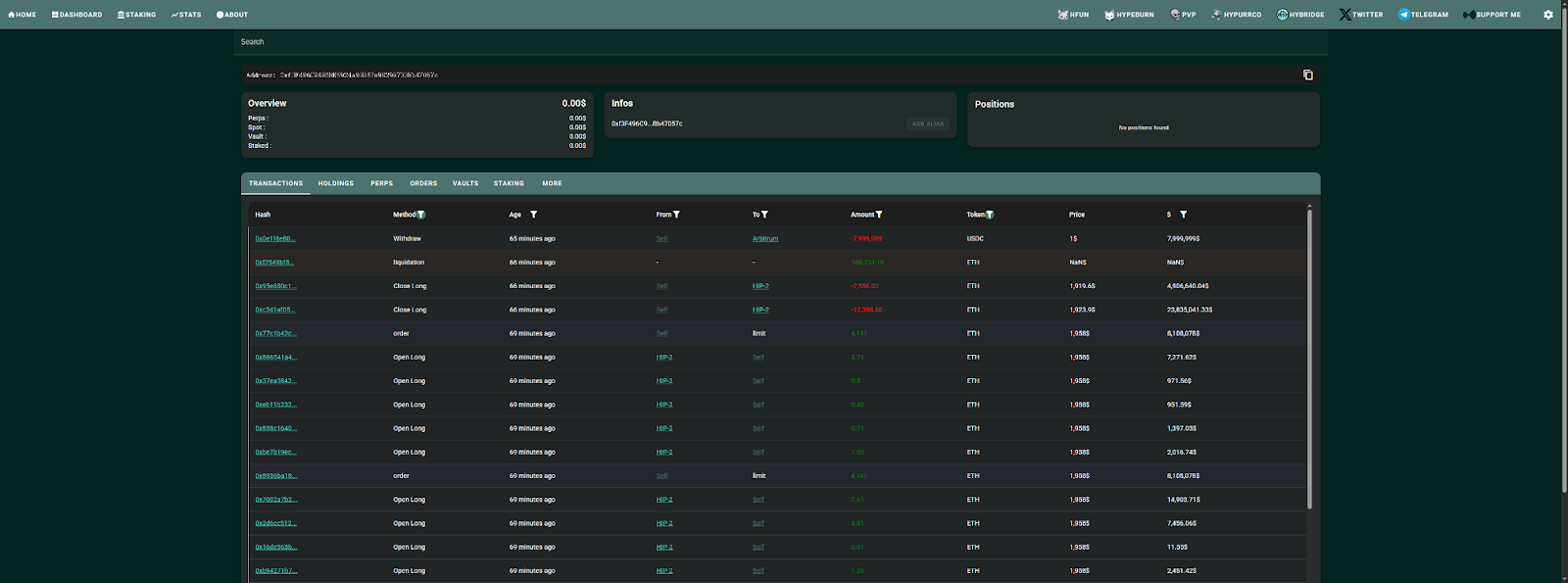

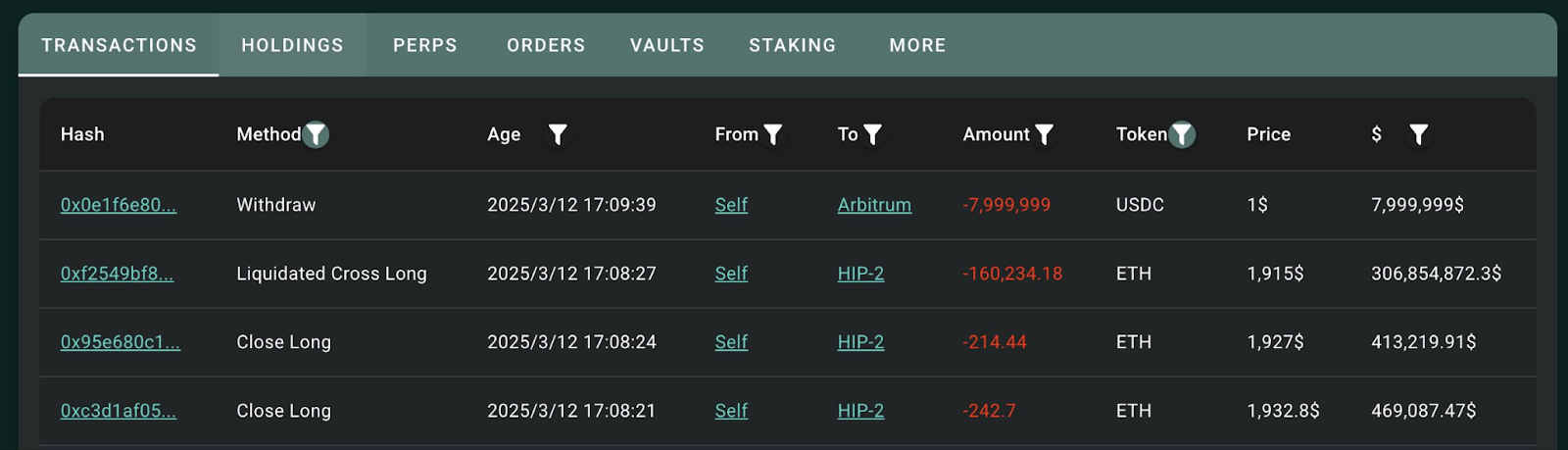

On March 12, the whale opened a 50x leveraged long position of 160,000 ETH, then withdrew $8 million in funds before deliberately getting liquidated, netting approximately $1.8 million in profit—while Hyperliquid itself incurred a $4 million loss.

This scenario may seem logically bizarre, but it fundamentally exploits a "loophole" in Hyperliquid's on-chain trading mechanism.

Let’s review the whale’s sequence of operations:

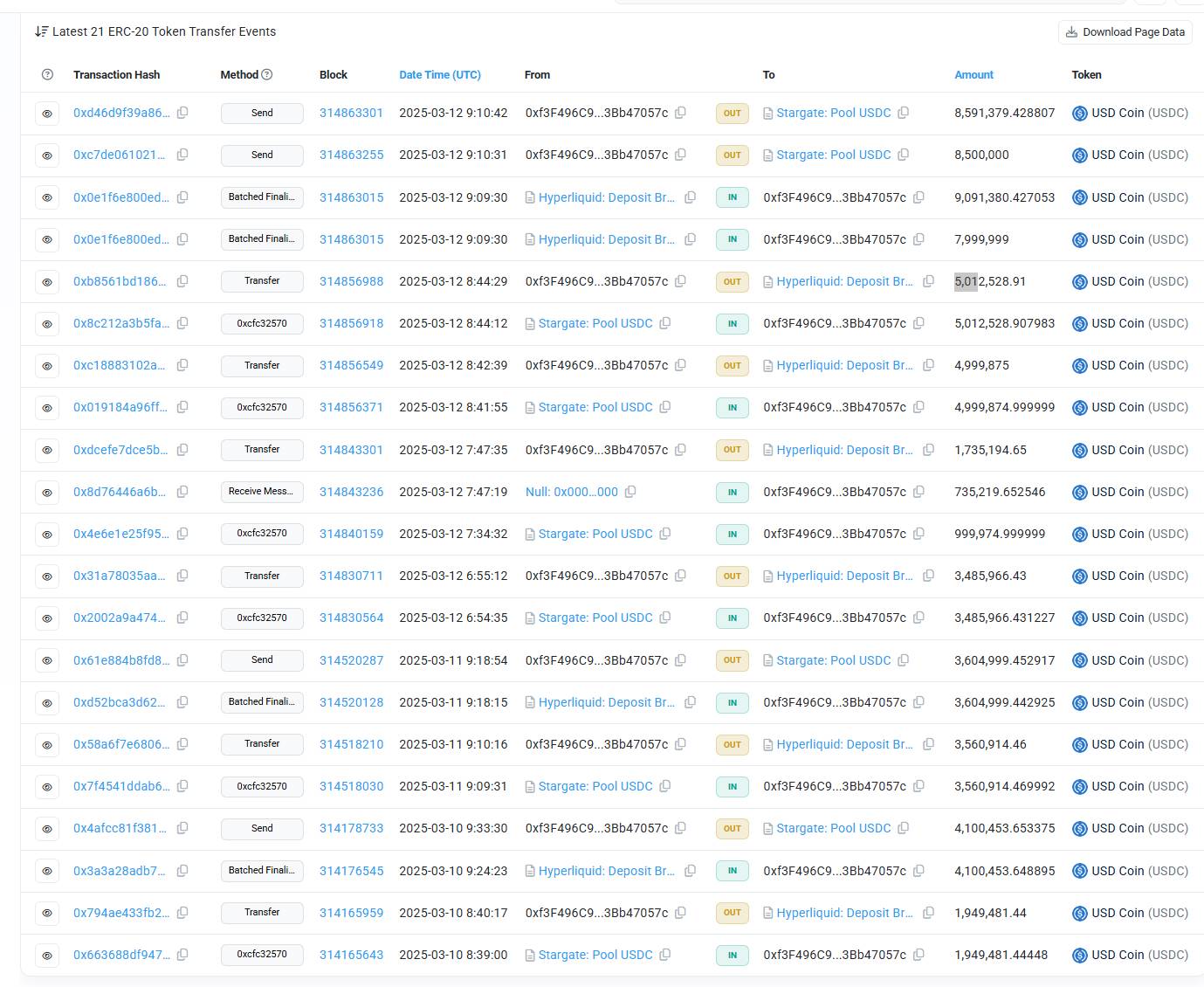

At 6:54 AM on March 12, the address deposited $3.48 million into Hyperliquid via cross-chain bridge, opening a position of 17,000 ETH (worth $31.2 million).

The address then increased its position by adding margin and expanding exposure, growing the holding to 21,790 ETH (worth $40.85 million).

Subsequently, continuous buying pushed the total ETH position up to 170,000 (valued at $343 million), with unrealized profits reaching $8.59 million.

Throughout this process, the whale deployed a total of $15.21 million in margin.

Finally, by partially closing positions and withdrawing margin, the whale reclaimed $17.08 million, securing a profit of $1.87 million.

In the final move, the user withdrew $8 million in funds, leaving around $6.13 million as margin, then waited for forced liquidation.

The Hunt Begins: Precision Calculations Behind the 170,000 ETH Position

Why did the whale choose this route instead of simply taking profits through normal exit?

At this stage, the whale had two options. The first was to close the entire position directly, locking in $8.59 million in unrealized gains. While this would maximize potential returns, such a massive $343 million order could not be absorbed instantly by counterparties on-chain. To execute, the price might need to drop significantly, eroding profits substantially. Moreover, initiating such a large sell order could crash the market, sharply reducing realized gains.

Thus, the whale chose the second path: withdrawing margin and partial profits (i.e., closing part of the position and extracting excess margin) while keeping the remaining margin exactly at the minimum required for 50x leverage. This way, if prices continued rising, the whale could capture even greater profits through staggered exits. If prices dropped sharply, the position would be liquidated within a 2% drawdown. But since $17.08 million had already been withdrawn, a net profit of $1.87 million was already secured. Even upon liquidation, there would be no actual loss.

An operation that appeared wildly risky ended up employing a conservative profit-taking strategy.

Afterward, data released by Hyperliquid showed the exchange lost $4 million that day (including some follower trades that profited). Meanwhile, the whale pocketed over $1.8 million in profit.

In terms of return on investment, the whale committed roughly $15.21 million and earned $1.87 million—a return of about 12.2%. Both in percentage and absolute value, this underperformed compared to earlier trades when the whale capitalized on Trump’s announcement including ADA and SOL in the strategic reserve.

Aftershocks and Lessons: Driving the Evolution of On-Chain Exchanges

From a market perspective, having the exchange absorb the loss is extremely rare. However, such a scenario appears feasible only on Hyperliquid.

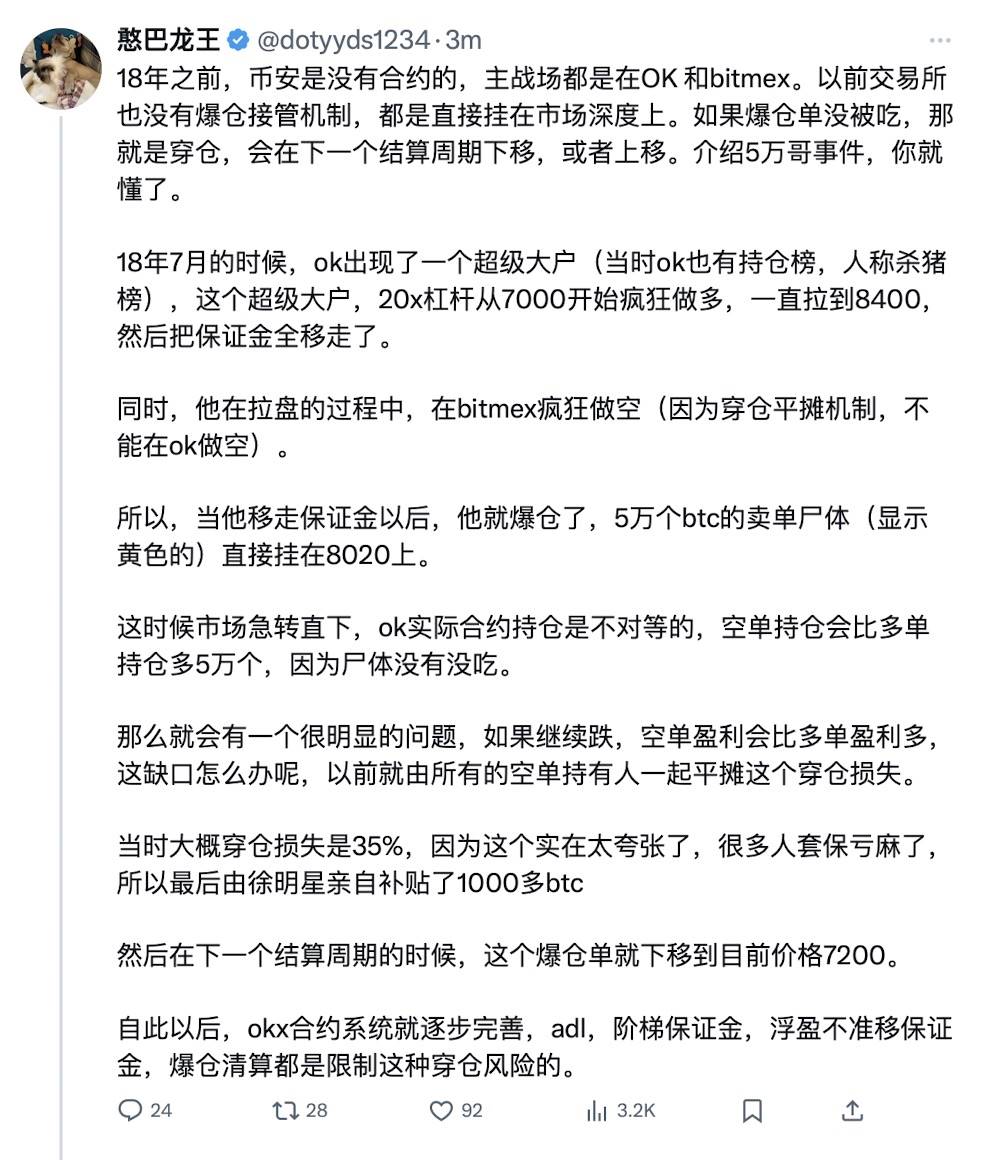

According to a post by KOL Hanba Longwang, a similar incident occurred at OKX in 2018. Using the same method—locking in profits and withdrawing margin until the liquidation price was reached with no available counterparty—the exchange was forced to cover the loss.

Following the OKX incident, centralized exchanges introduced tiered margin systems to ensure users maintain adequate collateral relative to market conditions. This recent event now serves as a lesson for emerging on-chain exchanges like Hyperliquid. By relying entirely on DEX-style trading mechanics, Hyperliquid failed to implement sufficient risk controls on margin requirements.

As a result, when the whale’s position was liquidated, there wasn’t enough market liquidity to absorb the forced sell order—leaving Hyperliquid to step in as the default counterparty. Data from HLP shows the $4 million loss nearly equaled Hyperliquid’s entire monthly profit. As of March 10, Hyperliquid’s HLP pool had accumulated $63.5 million in revenue, meaning the platform still retained nearly $60 million in profit after the incident.

Nevertheless, given the intense social media discussion sparked by this event, there’s concern about copycat behavior. Hyperliquid responded swiftly, announcing it would reduce maximum leverage on BTC to 40x and ETH to 25x to prevent recurrence.

Regarding speculation whether such tactics could fundamentally destabilize Hyperliquid, calculations suggest otherwise: the HLP pool currently holds nearly $60 million. With BTC capped at 40x leverage, the system can withstand up to $2.4 billion in adverse price moves. Very few traders possess the capital to challenge that. For typical orders, normal market counterparties are sufficient to absorb risk.

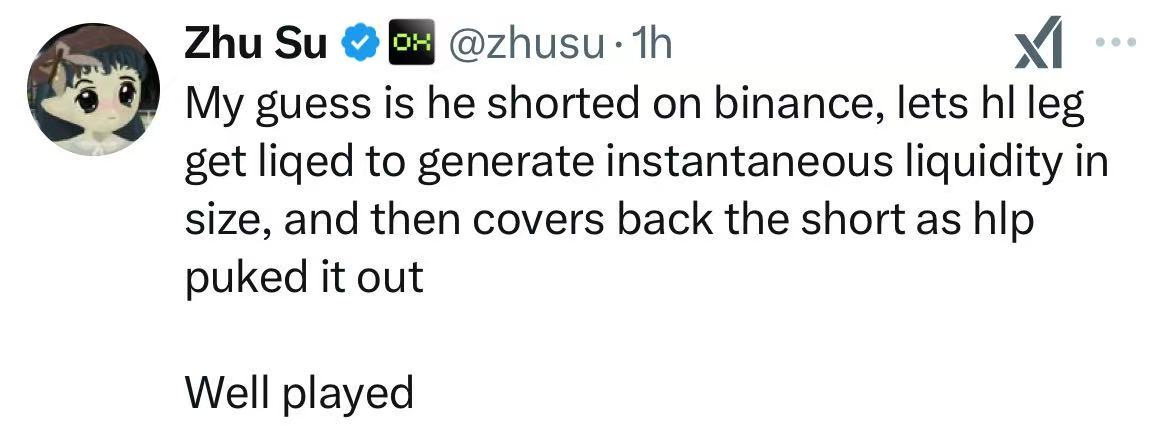

Looking back, it’s likely the whale conducted multiple test runs before executing this final play. Zhu Su, co-founder of Three Arrows Capital, speculated that the reason this address dared take such risks was because it held offsetting short positions on Binance during the same period—an effective hedged position. It was precisely the discovery of Hyperliquid’s differing insolvency handling mechanism compared to centralized exchanges that created the opening for exploitation.

In truth, this tactic isn't some revolutionary innovation. As noted at the outset, over a century ago, Livermore unintentionally achieved something similar. Back then, to sustain market stability, he chose to go long and close positions proactively. Today, exchanges act as backstops, enabling users to effectively "reclaim" profits from the exchange itself. Yet, this loophole will likely be closed permanently—making it improbable for similar platforms to allow such plays again.

For exchanges, this is yet another costly lesson learned. For retail traders, such maneuvers are fleeting anomalies—opportunities born from discovered vulnerabilities, offering profit in isolation but lacking reproducibility. They’re merely entertaining anecdotes in an otherwise dull market landscape.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News