2030 Retrospective on 2025: The Year Wall Street Officially Took Over Bitcoin

TechFlow Selected TechFlow Selected

2030 Retrospective on 2025: The Year Wall Street Officially Took Over Bitcoin

History repeats itself, but this time what's taking the stage isn't retail investors' tears, but the ceaseless sound of institutional treasury transfers on-chain.

By Daii

One day in 2030, when BlackRock's Bitcoin ETF surpasses the S&P 500 index fund in size, Wall Street traders suddenly realize: the thing they once mocked as a "dark web toy" now controls the throat of global capital.

But all this turning point began in 2025—the year Bitcoin surged past $250,000 amid institutional whale accumulation, yet no one could clearly say who owned it anymore. On-chain data revealed over 63% of the circulating supply locked into institutional custody addresses, with exchange liquidity drying up to barely cover three days of trading volume.

The above is fantasy. Let’s return to the present first.

A large amount of capital is continuously flowing out of Bitcoin ETFs, causing Bitcoin to drop below $80,000. This phenomenon can be explained by two main factors: First, policy-wise, U.S. tariffs reignited under Trump; second, from a funding perspective, 56% of short-term holders—hedge funds—have unwound their arbitrage strategies.

However, analysts believe we are currently in the "distribution phase" of the Bitcoin bull market.

The "distribution phase" of a Bitcoin bull market typically refers to the period near the end of the cycle, around price peaks, when large holders ("whales") begin gradually selling off their holdings, transferring Bitcoin from early adopters to newly entering investors. This phase signals the transition from frenzied upward momentum to the top zone and marks a critical juncture between bull and bear markets.

No more suspense—here’s the answer upfront: the current market liquidity structure has changed.

-

OG retail investors and OG whales are becoming sellers;

-

Institutional whales and new retail investors entering via ETFs are becoming the primary buyers.

In the cryptocurrency space, "OG" stands for "Original Gangster" (often interpreted as "Old Guard"), referring specifically to pioneers, early participants, or long-standing core members in the Bitcoin ecosystem.

In short: old money is exiting, new money is entering—and among the new money, institutions dominate.

Below, we will provide a detailed analysis covering market structure, characteristics of the current cycle, evolving roles of institutions versus retail, and the timeline of this market cycle.

1. Classic Market Structure: Whale-to-Retail Distribution at Bull Market End

Drawing on historical cycles, the late stage of a typical Bitcoin bull market features a structural pattern where whales distribute holdings to retail investors—early large holders sell their coins to newer, less experienced market entrants at high prices.

In other words, retail investors often buy at peak prices amid euphoric sentiment, while “smart money” whales take advantage of these highs to gradually offload their positions and lock in profits. This dynamic has repeated itself across previous cycles:

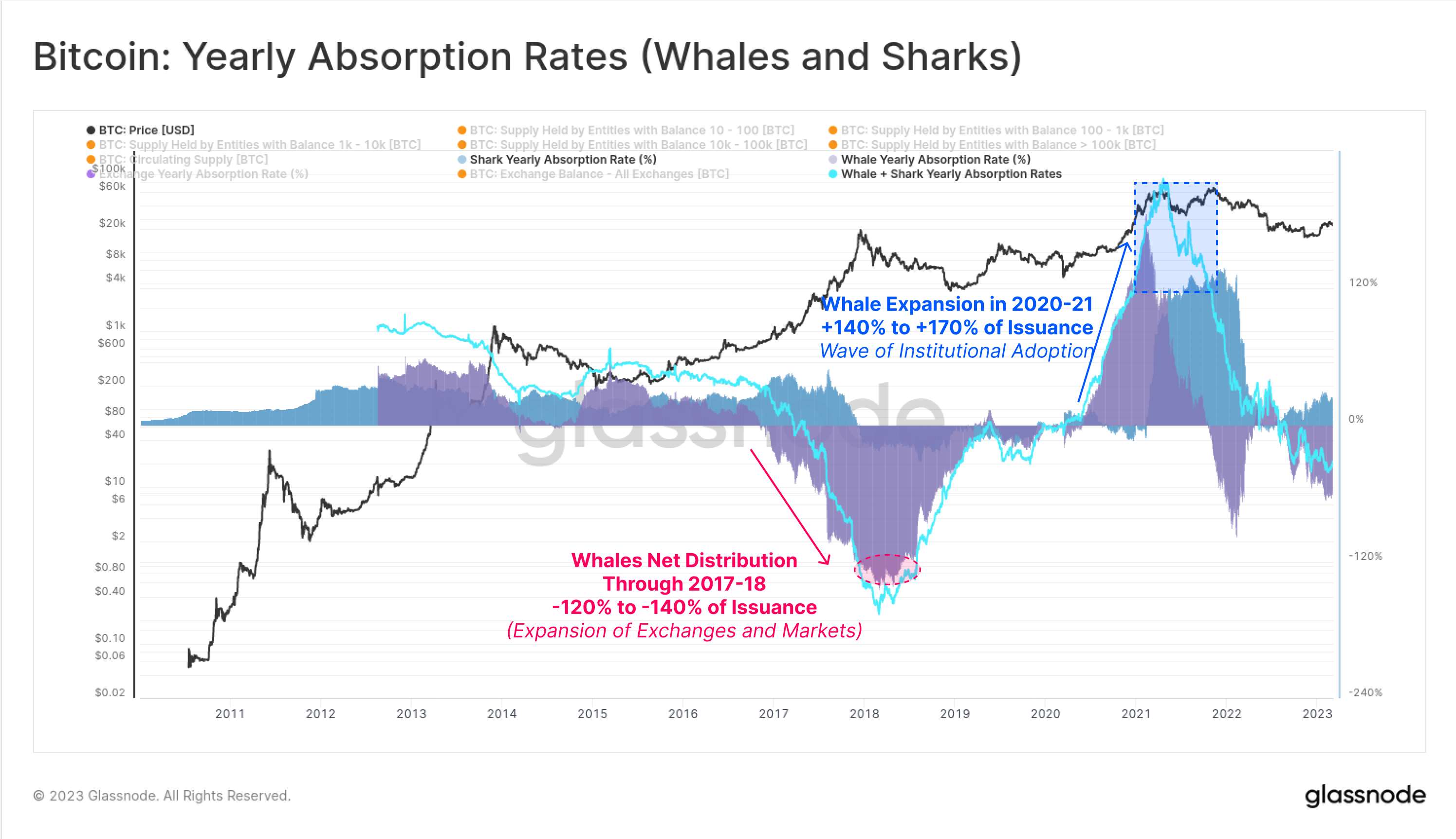

For example, during the peak of the 2017 bull run, net balances held by whales declined, indicating massive coin transfers out of whale wallets. This was driven by a surge of new demand that provided sufficient liquidity for whales to distribute their holdings. See: The Shrimp Supply Sink: Revisiting the Distribution of Bitcoin Supply.

Overall, the classic late-stage bull market structure can be summarized as early large holders gradually selling, increasing market supply, while retail investors, driven by FOMO (fear of missing out), absorb these sales aggressively. This distribution process is often accompanied by signs such as increased Bitcoin inflows into exchanges and movement of old coins on the blockchain—signals that the market is nearing its peak and poised for reversal.

2. Characteristics of This Bull Run: Structural Shifts

The current bull market (2023–2025 cycle) differs from past cycles during its distribution phase, especially in terms of retail and institutional investor behavior.

2.1 Unprecedented Institutional Participation in This Cycle

The launch of spot Bitcoin ETFs and widespread corporate treasury purchases have diversified market participants beyond just retail-driven rallies. The influx of institutional capital brings deeper pools of liquidity and more stable demand, directly reflected in reduced market volatility. Analyses show that drawdowns in this bull market have been significantly smaller than in prior cycles, with corrections rarely exceeding 25%–30%, largely attributed to stabilizing effects from institutional involvement.

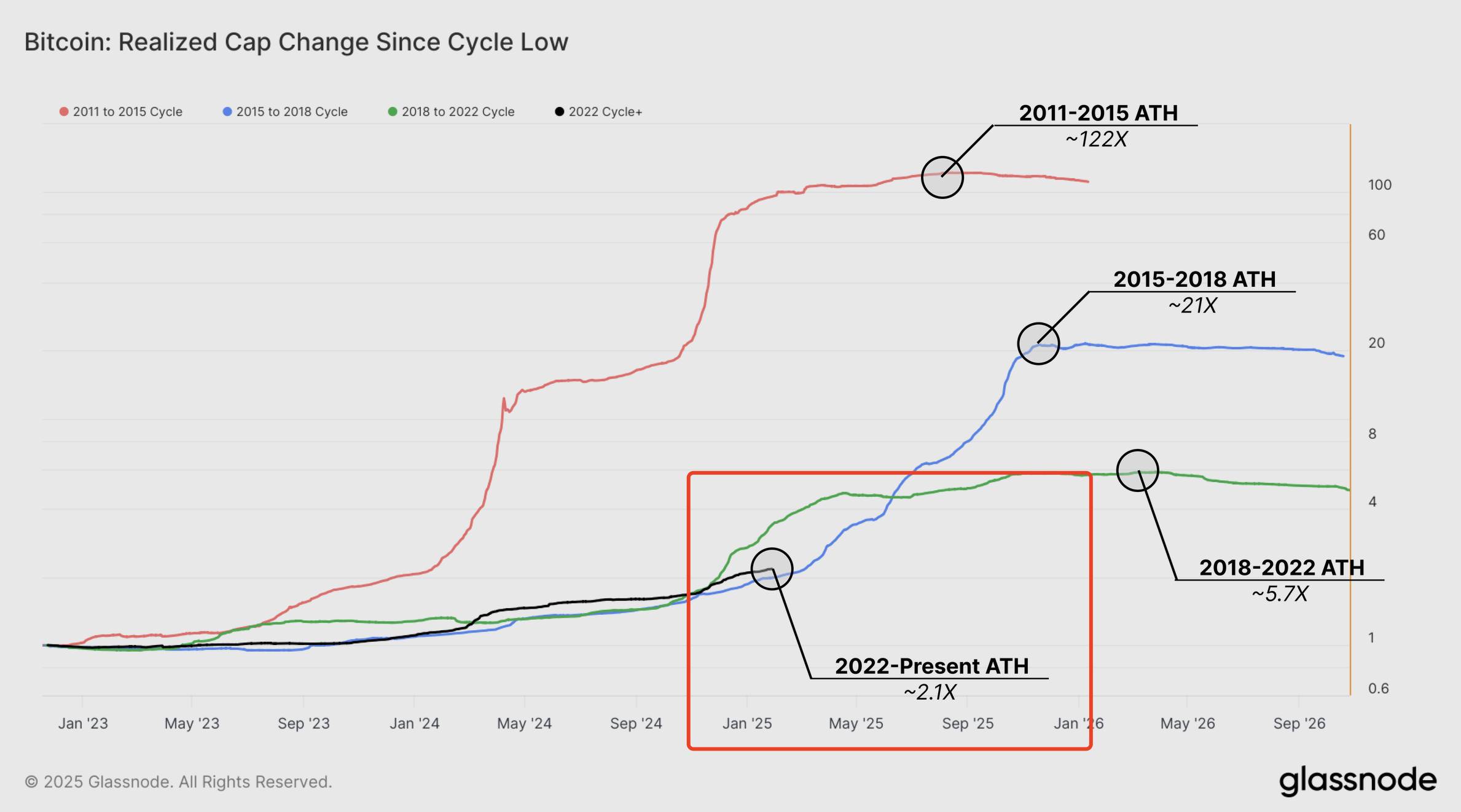

Additionally, increasing market maturity has led to more moderate price appreciation compared to previous cycles. This can also be seen through metrics like Realized Cap growth: this cycle’s Realized Cap expansion represents only a fraction of the previous peak, suggesting full-blown mania has not yet taken hold (see: Thinking Ahead).

Realized Cap is an important metric measuring actual capital inflow into the market. Unlike traditional market cap—which simply multiplies current price by total supply—Realized Cap considers the last transaction price of each individual Bitcoin on-chain. As such, it better reflects the true scale of invested capital.

Naturally, these indicators may also suggest the market is transitioning into a more mature and stable phase of development.

2.2 Retail Investor Behavior Has Become More Rational and Diversified

On one hand, seasoned retail investors (individuals who’ve lived through multiple cycles) are acting more cautiously, locking in profits earlier rather than chasing prices all the way to the top, unlike in previous cycles.

For instance, early 2025 data showed small holders (retail) net transferred approximately 6,000 BTC (~$625 million) into exchanges in January alone, beginning profit-taking early. Meanwhile, whales saw only minor net inflows of about 1,000 BTC, remaining mostly inactive. This divergence suggests many retail investors perceived a temporary top and chose to cash out, while whales (“smart money”) stayed put—clearly anticipating even higher price targets.

On the other hand, enthusiasm among newly entering retail investors continues to build. Indicators like Google Trends show public interest dipped and reset after new price highs, without reaching the kind of fever-pitch, mass-hysteria levels seen at the end of past cycles. This implies the current bull market may not yet have entered its final euphoric stage, leaving room for further upside.

2.3 Institutional Investor Behavior Is a Defining Feature of This Bull Market

The previous 2020–2021 cycle marked the first time significant institutional and corporate participation occurred. Interestingly, during that period, whale holdings actually increased—new institutional “whales” were accumulating heavily, pulling Bitcoin out of retail hands into their own wallets.

This trend continues today: major institutions are buying large amounts of Bitcoin via OTC markets, trusts, or ETFs, meaning traditional whales aren’t necessarily net sellers anymore. This has delayed and softened the onset of the distribution phase. As a result, distribution in this cycle is more gradual and dispersed—not the abrupt handover from whales to naive retail seen before. With greater market depth, new capital is able to absorb sell-side pressure from long-term holders.

A Glassnode report noted that significant wealth is already shifting—or actively shifting—from long-term holders to new investors, signaling market maturation. Long-term holders have realized record profits (up to $2.1 billion in a single day), while new investors possess sufficient demand to absorb these sell-offs. See Bitcoin sees wealth shift from long-term holders to new investors – Glassnode.

Clearly, the interaction between retail and institutional players has created a more resilient market environment in this cycle.

3. Evolving Roles of Institutions and Retail: How OG Holders and Institutions Affect Liquidity

As the participant landscape evolves, so too do the roles of institutions and retail in the distribution phase.

Ki Young Ju, CEO of CryptoQuant, summarized this cycle’s distribution model as: OG retail + legacy whales → new retail (via ETFs, MSTR, etc.) + new whales (institutions).

In other words, early-cycle retail investors and whales are now gradually selling, while the buyers include not only traditional retail but also ordinary investors entering via ETFs and new institutional capital stepping into whale-like roles.

This diversified participation contrasts sharply with the classic linear “whale → retail” distribution model.

-

In this cycle, OG retail (early individual holders) likely possess substantial Bitcoin quantities and are choosing to exit at elevated prices, contributing partial selling pressure and liquidity to the market.

-

Likewise, OG whales (early large holders) are incrementally offloading assets to realize multiples—or even tens of multiples—of their original gains. In contrast, institutional whales are stepping in as dominant buyers, absorbing this supply through custodial accounts and ETF channels, shifting Bitcoin from legacy wallets into institutional custody.

-

Moreover, some traditional retail investors now indirectly hold Bitcoin via ETFs or stocks of companies like MicroStrategy, representing a new form of “retail absorption.”

These role shifts have profound implications for market liquidity and price dynamics.

3.1 More Bitcoin Is Leaving Exchanges

On one hand, selling activity by OG holders leaves clear on-chain footprints: increased movements from dormant wallets, large transfers directed toward exchanges, etc.

For example, in this bull run, certain long-dormant wallets have reactivated, moving coins into exchanges for sale—an observable sign of OG holders distributing their holdings. Ki Young Ju notes that OG activity manifests clearly in on-chain and exchange data, whereas flows of “paper Bitcoin” (such as ETF shares or crypto-related equities) only appear on-chain when settled into custodial wallets. That is, institutional buying often occurs off-exchange or through custodians, with direct on-chain evidence showing up as rising balances in custodian addresses—not direct exchange flows.

The current exchange Bitcoin balance of 2.22 million BTC reflects this very dynamic.

3.2 New Whales and New Retail Are More Resilient

On the other hand, institutional investors, as emerging whales, not only provide strong bid support but also enhance the market’s capacity to absorb sell-offs and deepen overall liquidity.

Unlike past retail-dominated markets prone to panic cascades, institutional capital tends to accumulate on dips and maintain long-term allocations. When corrections occur, this professional capital often steps in to stabilize prices. For instance, analyses attribute the lower volatility in this cycle directly to institutional participation: when retail sells, institutions step in to absorb supply, keeping drawdowns far milder than in previous cycles.

While Bitcoin ETFs have injected massive new capital into the market, some ETF holders—particularly hedge funds—may primarily engage in arbitrage trades, making their capital highly liquid. Recent large outflows from ETFs indicate certain institutional players are conducting short-term arbitrage rather than committing to long-term holding. The recent drop below $80,000 was fueled by hedge fund arbitrage strategy unwinds.

Nevertheless, newly entering retail investors have shown notable resilience, refraining from panic-selling during every correction and instead opting to hold. Bitcoin’s short-term holder metrics reflect stronger downside resistance.

Overall, the interplay between OG retail + OG whales and new institutional whales + new retail has formed a unique supply-demand structure: early holders provide liquidity, while institutions and new buyers absorb it, making the late-stage distribution process smoother and more traceable.

4. Market Cycle Timeline: Historical Patterns and Outlook for This Bull Run

Historically, Bitcoin follows a roughly four-year cycle, encompassing complete phases of bear market, bull market, and transition. This rhythm closely correlates with Bitcoin’s block reward halving events: after each halving, new coin issuance drops sharply, followed by a significant price rally (bull market) within approximately 12–18 months, eventually peaking before entering a bear market correction.

4.1 History

Reviewing key past bull market timelines:

-

The first halving occurred at the end of 2012, followed by a price peak about 13 months later in December 2013;

-

The second halving in 2016 led to a bull market peak around 18 months later in December 2017, approaching $20,000;

-

The third halving in May 2020 was followed by dual peaks in late 2021 (April and November), nearing $70,000;

-

Therefore, the fourth halving in April 2024 could trigger another bull run, most likely peaking between one to one-and-a-half years post-halving—around the second half of 2025—marking the final distribution phase (end of the bull market).

Of course, cycles don’t repeat mechanically. Changes in market conditions and participant structures may affect the duration and peak level of this cycle.

4.2 Optimistic View

Some analysts argue that macroeconomic conditions, regulatory developments, and market maturity will significantly influence this cycle.

For example, Grayscale’s research team stated in a late 2024 report that the market is still in the mid-phase of a new cycle. If fundamentals—such as user adoption and macro trends—remain favorable, the bull market could extend into 2025 or beyond. They emphasize that newly launched spot Bitcoin ETFs have broadened access for capital entry, and clearer U.S. regulatory frameworks ahead (e.g., potential impacts under a new Trump administration) could further boost crypto valuations.

This suggests this bull market could last longer than previous ones, potentially extending beyond traditional timing windows.

Additionally, on-chain data supports the case for a prolonged bull run. As previously mentioned, Realized Cap growth this cycle hasn’t even reached half of the prior peak, indicating full speculative fervor hasn’t erupted. Some analysts therefore predict the final top could far exceed the last cycle, with common forecasts raising expectations to $150,000 or higher.

4.3 Conservative View

Still, others believe the peak will materialize within 2025.

CryptoQuant’s Ki Young Ju expects the final distribution phase—where OG holders and institutions collectively offload to the last wave of incoming capital—to occur within 2025. His view is based on the current early distribution phase and observed inflows of new retail capital, arguing there’s no need to turn bearish prematurely before the final distribution completes.

Combining historical patterns and current indicators, it’s likely this bull market will enter its final stage in the second half of 2025. As prices reach a temporary climax, various holders will accelerate distribution, completing the final transfer of wealth.

Of course, exact timing and peak levels are impossible to predict precisely. But judging by cycle length (~1.5 years post-halving) and market signals (retail frenzy levels, institutional flow trends, etc.), 2025 may prove to be the decisive year.

Conclusion

As Bitcoin transforms from a geek toy into a trillion-dollar strategic asset, this bull market may reveal a harsh truth: the essence of financial revolution isn’t eliminating old money, but reconstructing the DNA of global capital under new rules.

The current “distribution phase” is, in reality, Wall Street’s formal coronation of control over the crypto world. When OG whales hand over their chips to BlackRocks and Fidelity, it’s not the prelude to a crash—it’s the soundtrack of global capital realignment. Bitcoin is evolving from a retail get-rich-quick myth into a “digital strategic reserve” on institutional balance sheets.

The greatest irony? While retail investors are still calculating the “perfect exit code,” Blackstone has already embedded Bitcoin into its 2030 balance sheet template.

The ultimate question of 2025: Is this the cyclical peak, or the birth pangs of a new financial order? The answer lies buried in cold, hard on-chain data—each outgoing transaction from an OG wallet adds another brick to BlackRock’s custody vault; every ETF inflow redefines ownership of “store of value.”

To investors navigating cycles: the greatest risk isn’t missing out, but interpreting the 2025 game with 2017-era logic. When “holding addresses” become “institutional custody accounts,” and “halving narratives” morph into “derivatives of Fed rate decisions,” this generational shift transcends mere bull and bear cycles.

History repeats itself—but this time, what echoes isn’t retail tears, but the ceaseless on-chain transfers into institutional vaults.

This institutionalization trend mirrors the evolution of Web1.0—the internet once ruled by geeks ultimately fell into the hands of FAANG giants (Facebook, Apple, Amazon, Netflix, Google).

History’s cycles are always laced with dark humor.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News