The role of stablecoins in Africa's digital economy

TechFlow Selected TechFlow Selected

The role of stablecoins in Africa's digital economy

Financial inclusion is one of the biggest opportunities in Africa's digital industry.

Author: WSPN

1. Introduction

1.1 Africa's Digital Economy

As the global digital economy rapidly expands, Africa stands at a pivotal moment—poised to leverage digital transformation for economic development and sustainable growth. Covering over 30 million square kilometers, Africa had a population exceeding 1.4 billion in 2022, rich in natural resources. According to the World Bank, Africa’s GDP reached approximately $2.98 trillion in 2022, growing at an annual rate of more than 3%. A report by Endeavor estimates that Africa’s digital economy was valued at around $115 billion in 2022, accounting for 3.86% of GDP, and is projected to reach $712 billion by 2050. In comparison, Asia’s digital economy accounted for over 30% of its GDP in 2022. This highlights the immense potential of Africa’s digital economy.

The digital economy spans industries such as digital finance, e-commerce, and digital education. Digital finance integrates traditional financial services with digital technologies. Up to 66% of Africa’s population remains unbanked—individuals and businesses across African nations face persistent challenges in accessing payments, loans, savings, and insurance. However, the number of fintech startups in Africa has surged in recent years. Statistics show that African fintech companies raised nearly $200 million in funding in 2017; the top 10 African fintech firms raised close to $300 million in the first ten months of 2018; and in 2019, investments exceeding $5 million per deal totaled over $580 million. The most prominent sectors in African digital finance include mobile payments (digital wallets), online lending, and international remittances. Financial inclusion represents one of the greatest opportunities in Africa’s digital sector, centered on using digital technology to expand access to financial services at scale.

Distribution of major African Fintech enterprises (Source: Digital Africa Observatory, briterbridges)

According to Statista, Africa’s mobile payment transaction volume will surpass $195 billion in 2024—more than double the 2020 level—with double-digit compound annual growth. By 2028, this figure is expected to grow further to $314.8 billion. Over the past two years, many African countries have seen record highs in electronic payment volumes. Data from Nigeria’s central bank shows that mobile money transactions doubled in 2020, reaching about 800 million. South African data indicates that online commerce grew by approximately 40% between 2020 and 2021. Digital payments are becoming an increasingly dominant method across the continent. In 2023, 17% of African consumers used digital payment services daily, while 48% used them weekly.

Africa’s digital payment market size (Source: Statista)

Mobile money is currently the primary and fastest-growing form of digital payment in Africa. According to GSMA’s “The State of the Industry Report on Mobile Money,” Africa had 856 million registered mobile money accounts in 2023, representing 49% of global registrations. New registrations reached 136 million, accounting for over 70% of global growth—making Africa the main driver of global mobile money expansion. Currently, Africa hosts about 169 mobile money services, including M-PESA, Airtel Money, Orange Money, MTN Mobile Money, Ecocash, and Tigo Pesa. These platforms allow users to save, send, and receive money via mobile phones, offering a convenient alternative to traditional banking, especially in areas with limited banking infrastructure. Beyond improving financial inclusion and access to other digital services, the adoption and use of mobile money also contribute significantly to macroeconomic growth. Mobile money contributed over $150 billion to sub-Saharan Africa’s GDP, equivalent to a 3.7% contribution rate, and up to 5.9% in East Africa.

Contribution of mobile money to GDP across regions (Source: GSMA)

Digital commerce, also known as e-commerce, faces challenges in Africa due to underdeveloped infrastructure, late start, and incomplete systems. However, the continent’s large population base, high proportion of youth, and significant room for improvement have attracted investors globally. According to Statista, Africa’s e-commerce market generated $49.02 billion in online retail revenue in 2023, with an annual growth rate nearing 14%. By 2027, the user base could surge to 600 million, achieving a penetration rate of 44.3%. This expansion brings multiple benefits, including economic growth, job creation, and improved access to goods and services in rural and remote areas.

Africa’s e-commerce industry is redefining traditional supply chains and business models. For example, Kenya’s Twiga Foods sources directly from farmers and efficiently delivers products to urban retailers, streamlining the agricultural value chain. Egypt’s MaxAB connects food and grocery retailers with suppliers in underserved areas. These innovations add diversity to Africa’s e-commerce landscape. Meanwhile, the Pan-African Payment and Settlement System (PAPSS) facilitates cross-border transactions within Africa without relying on correspondent banks outside the continent. With over ten countries and commercial banks adopting PAPSS, it has significantly boosted e-commerce growth.

Additionally, the digital economy plays a vital role in traditional sectors such as logistics, agriculture, education, energy, and transportation. While driving technological advancement, it also enhances inclusivity and innovation. For instance, Lagos-based Kobo360 in Nigeria and Nairobi-based Lori Systems in Kenya apply digital tools to traditional road freight markets, improving efficiency and reliability while reducing truck idle rates. Most drivers saw income increases of over 50% after partnering with these platforms. Historically, Africa’s education sector has been constrained by teacher shortages, tuition costs, gender disparities, safety concerns, long distances to schools, and low smartphone penetration. To address this, Kenyan edtech company Eneza Education provides services via USSD and SMS for feature phone users. Its website reports 4.9 million users, over 1 million daily messages sent, more than 10 million student quiz attempts, and over 1 million questions asked cumulatively.

1.2 Stablecoins

1.2.1 Africa’s Stablecoin Market

Adoption of cryptocurrency in Africa is experiencing rapid growth. According to Chainalysis, Nigeria ranks second globally in overall crypto adoption index, just behind India and ahead of Western nations like the United States. Stablecoins dominate crypto usage. From July 2022 to June 2023, cryptocurrency transfers in sub-Saharan Africa reached $117.1 billion, with stablecoins accounting for over 50% of all asset categories—significantly higher than BTC or ETH.

Monthly cryptocurrency transaction volume in sub-Saharan Africa by asset type, 2023 (Source: Chainalysis)

Taking Nigeria—the largest crypto economy in Africa—as an example, in 2022, the Central Bank of Nigeria announced plans to redesign the national currency (Naira) and issue new banknotes to combat inflation and gain greater control over cash circulation. Unfortunately, the resulting cash shortage placed severe strain on the country’s unbanked population early in 2023. Uncertain economic conditions encouraged more citizens to seek financial alternatives—increasing their holdings in cryptocurrencies, primarily stablecoins.

Cryptocurrency transaction volume in Nigeria (Source: Chainalysis)

1.2.2 Applications of Stablecoins in Africa

Remittances

Over the past decades, inflows into Africa have steadily increased, yet Africans still face high remittance costs. According to the United Nations Development Programme (UNDP), sending $200 to Africa cost 7.8% in Q2 2022—far above the global average of 4%–6.4%. Using cryptocurrency for remittances can drastically reduce costs (as low as one-twentieth of traditional methods). For example, Nigeria’s SureRemit charges only 0%–2% for remittance services. Additionally, using stablecoins avoids losses from price volatility. Major African exchanges such as Paxful, BuyCoins, Luno, and Quidax have seen substantial demand for stablecoin transactions driven by remittance needs.

Remittance costs (Source: UNDP)

Cross-Border Trade

Using stablecoins for cross-border trade offers lower fees and faster settlement times. In traditional trade, banks play a key role. However, most African trade is conducted by SMEs, and increasing regulatory scrutiny, risk management, KYC requirements, and exchange rate risks have led to declining bank support for cross-border activities. Moreover, underdeveloped financial infrastructure means African trade heavily relies on international banks, limiting trade expansion. Stablecoins combined with blockchain smart contracts offer effective solutions to these issues.

Financial Inclusion

According to UNDP, as of 2021, about 60% of adults aged 15 and above in sub-Saharan Africa were unbanked (compared to a global average of 26%), with women less likely to have accounts than men by 12 percentage points. In terms of financial infrastructure density, Africa averages only 4.5 commercial banks per 100,000 people (global average: 10.8).

Many crypto service providers integrate various industry resources to offer broader services to those lacking basic financial access. For example, Nigeria’s SureRemit allows users not only to transfer money but also to purchase goods, pay tuition, settle utility bills, and make donations through its network of over 1,000 merchant partners, leveraging blockchain-based payments to address challenges faced by the unbanked.

Statistical evidence further shows that as mobile phone usage rises across Africa, there is a clear negative correlation between the proportion of adults with mobile money accounts and those who have never had any financial account. Countries with higher mobile money adoption demonstrate greater financial inclusion.

Cryptocurrency enhancing financial inclusion (Source: UNDP)

Value Preservation and Inflation Hedging

Many African countries suffer from persistently high inflation (double-digit annual rates), far exceeding global averages, leading to continuous depreciation of local currencies. The situation worsened after the pandemic: in 2021, supply chain crises and resource scarcity caused inflation in sub-Saharan Africa to rise by 3%. Holding dollar-pegged stablecoins as reserves effectively addresses this issue. Many major centralized exchanges now offer stablecoin savings products tailored for African users.

Inflation rates in selected sub-Saharan African countries (Source: UNDP)

1.2.3 Major Stablecoins in Africa

The primary stablecoins used in Africa include:

-

Tether (USDT): The largest stablecoin by market capitalization (over $110 billion), and the most widely used stablecoin in Africa and globally. Christopher Maurice, founder of Yellow Card—one of Africa’s leading crypto exchanges—stated that USDT on the Tron network is among the most popular cryptocurrencies among African users. Many Africans prefer using dollar-pegged stablecoins like USDT on low-cost networks such as Tron to hedge against domestic inflation.

-

USD Coin (USDC): The second-largest USD-pegged stablecoin by market cap, issued by Circle. Like USDT, USDC is actively expanding into African markets. In January 2024, Coinbase partnered with Yellow Card to extend its product availability to 20 additional African countries, focusing on increasing USDC adoption. This move enables millions of users to access USDC and conduct fast, reliable, and cheaper transactions on the decentralized, open L2 Base network via Coinbase and Yellow Card products.

-

WSPN USD (WUSD): A USD-pegged stablecoin issued by WSPN, a stablecoin infrastructure company, aiming to provide users with secure, efficient, and transparent payment solutions through a global compliance framework and a new payment ecosystem. In July 2024, WSPN formed a strategic partnership with CanzaFinance, a pioneering African fintech firm. Integrating WUSD into CanzaFinance’s ecosystem enables seamless financial transactions—including remittances, payments, and savings—and smooth conversion between WUSD and African fiat currencies, accelerating the real-world application of real-world assets (RWA) and decentralized finance (DeFi) solutions in emerging markets like Africa.

-

PayPal USD (PYUSD): A USD-pegged stablecoin issued by PayPal, the world’s largest third-party payment platform.

-

Celo USD (CUSD): A USD-pegged stablecoin issued by Celo. Unlike the above three, CUSD is primarily backed by cryptocurrencies including BTC, ETH, and Celo. In 2023, Celo partnered with Opera to launch MiniPay, a stablecoin wallet first rolled out in Nigeria. Integrated with Opera Mini, the mobile browser, MiniPay aims to help African mobile internet users access Web3 products. OPAY, Opera’s mobile payment arm, is now one of Africa’s leading mobile payment providers, with over 35 million registered users.

1.2.4 Regional Differences

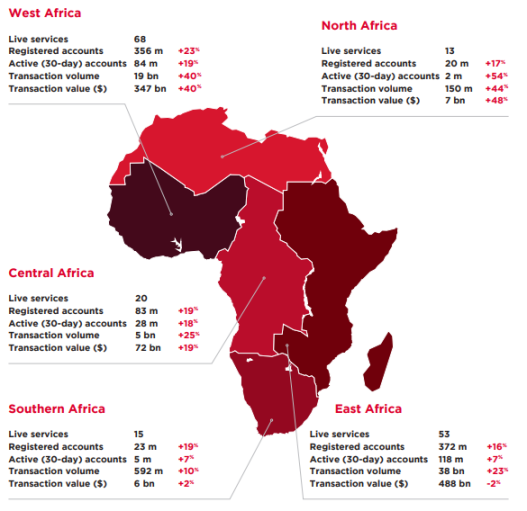

Africa’s digital economy exhibits significant regional disparities. In 2023, Africa had 856 million mobile money accounts with transaction volumes reaching $919 billion. East and West Africa lead in mobile money development, collectively accounting for 85% of active accounts and 90.8% of transaction volume. In terms of active accounts, East Africa had an early advantage, while West Africa experienced the fastest growth over the past decade.

Overview of Africa’s mobile money in 2023 (Source: GSMA)

Regional share of active mobile money accounts in Africa, 2013–2023 (Source: GSMA)

West Africa: Nigeria, Ghana, and Senegal are among the fastest-growing crypto economies. A 2020 Statista survey found that 32% of Nigerians have held or used cryptocurrency—the highest rate globally. Nigeria also received the most cryptocurrency in Africa in 2023 (over $56 billion). On one hand, local currencies like the Naira and Ghanaian Cedi have depreciated significantly amid high inflation, prompting citizens to seek safer, dollar-pegged stablecoins. On the other hand, Nigeria is Africa’s largest country by population and economy, accounting for 38% of remittance flows in sub-Saharan Africa in 2023, creating massive demand for remittances and payments.

East Africa: Kenya, Tanzania, and Mauritius are also active crypto economies. M-Pesa has become Kenya’s largest mobile payment platform, enabling ordinary people to perform cross-border payments, short-term loans, salary collection, bill payments, and wealth management via mobile phones and networks—greatly improving financial access for underserved populations and indirectly boosting Kenya’s overall economic and social well-being.

Southern Africa: South Africa has seen rapid growth in its crypto sector. Beyond offering cheaper and faster remittance options, South Africa’s relatively robust financial infrastructure—where over 80% of the population has bank accounts—and higher financial literacy mean that crypto and stablecoin adoption is primarily investment-driven. A study by Kucoin shows that approximately 22% of South African adults (7.6 million people) are crypto investors, with many preferring digital assets as their preferred savings vehicle for stable returns.

1.2.5 Growth Outlook

The rapid growth of e-commerce, widespread adoption of digital services, revolutionary advances in mobile payments, and uneven development across African nations will all drive stablecoins to play a critical role in Africa’s future digital economy and financial system.

In recent years, Africa’s e-commerce market has grown at an astonishing pace, projected to reach $939.8 billion by 2030. Local platforms such as Jumia (the first African tech company listed on the NYSE) and Konga are rising, while global giants like Amazon are actively entering the market. This growth is fueled by Africa’s demographic dividend—Africa is one of the fastest-growing regions globally, with a current population exceeding 1.2 billion and projected to reach 2.5 billion by 2050. This large and youthful population base provides enormous consumption potential. Increasing internet penetration and shifting consumer habits toward online shopping lay a solid foundation for e-commerce. Furthermore, governments and private enterprises have invested heavily in internet infrastructure, expanding fiber-optic and mobile network coverage. Smartphone adoption is also rising rapidly—Africa is expected to have 675 million smartphone users by 2025, providing essential technical support for e-commerce platforms. The success of mobile payment platforms like Kenya’s M-Pesa has promoted cashless transactions. As payment systems improve, online shopping becomes more convenient and secure, further accelerating e-commerce growth.

Currently, Africa has 1.22 billion mobile network users, of which 676 million are smartphone users (55.32%). Key mobile payment platforms include M-PESA, Airtel Money, Orange Money, and MTN Mobile Money, which are widely adopted and provide accessible financial services to the unbanked. By 2028, the value of Africa’s digital payment market is expected to grow to $314.8 billion.

Other digital services such as online education and telemedicine are also in rapid development. According to Expert Market Research, Africa’s e-learning market is projected to reach $20.35 billion by 2028, with a compound annual growth rate of 39.2% from 2023 to 2028—driven by rising demand for online learning solutions, increased mobile device usage, and government initiatives promoting digital education. Africa’s healthcare market is expected to grow at an average annual rate of 8.3%, reaching $259 billion by 2025. The rise of digital health—mobile health apps, telemedicine, and electronic health records—offers new ways to improve healthcare accessibility and quality.

Beyond the momentum of the digital economy, Africa faces persistent challenges such as high inflation, currency volatility, low banking penetration, and weak financial infrastructure. Stablecoins offer a relatively stable medium of exchange, helping individuals and businesses manage these economic pressures.

2. How Stablecoins Empower Africa’s Digital Economy

Stablecoins are designed to maintain stable value. The most widely circulated ones—such as USDT and USDC—are pegged to the U.S. dollar. As the world’s primary trade currency, the dollar maintains relative stability against most national currencies. Thus, using dollar-pegged stablecoins helps mitigate exchange rate risks in African countries where local currencies often depreciate long-term due to monetary instability and high inflation.

In traditional cross-border trade, banks provide crucial services such as payment settlement, trade financing, risk management, and foreign exchange. SMEs dominate economic activity and cross-border trade in Africa, making trade financing essential for importers and exporters. Bank-mediated trade finance accounted for an average of 40% of total African trade over the past decade. However, stricter KYC, anti-money laundering, and risk-based capital regulations have led to a steady decline in bank-supported trade finance, disproportionately affecting micro, small, and medium enterprises (MSMEs). Other factors—liquidity constraints, currency risk, credit risk, time delays, and high transaction costs—further exacerbate trade financing challenges in Africa. Stablecoins can significantly alleviate these issues by enabling near-instant payments via blockchain technology, accelerating fund flows across supply chains, buyers, shippers, and sellers. SMEs engaged in cross-border trade can access funds faster from banks and financial institutions, ensuring liquidity. Stablecoins like USDT and USDC are already being used in international trade by African SMEs. Moreover, decentralized finance (DeFi) built on stablecoins now offers mature financial products such as lending and deposits. This underutilized trade finance potential could enable greater SME participation in intra-African and sub-regional trade (e.g., ECOWAS, SADC, IGAD).

Integrating stablecoins with existing mobile payment platforms can enhance transaction efficiency and reduce costs. The low cost and speed of stablecoin transactions are highly attractive to users. They also promote financial inclusion by giving the unbanked access to a broad range of financial services through stablecoins and DeFi ecosystems.

The low-cost, fast nature of stablecoin transactions can further improve various aspects of digital services, enhancing convenience and attracting more users. In micropayments, stablecoins significantly reduce transaction costs, making small-value transactions economically viable—especially important in Africa, where traditional payment methods are expensive. Fast settlement enables instant or near-instant payments, crucial for seamless micropayment experiences. In subscription models, stablecoins simplify recurring payments—users set up automatic payments once, eliminating repeated manual input. This is particularly useful for African users accustomed to mobile devices. Additionally, stablecoins’ price stability reduces the risk of failed payments due to currency fluctuations, ensuring uninterrupted service delivery. Stablecoins can also be used across digital services such as in-game purchases, online education, and health services, offering smooth payment experiences. This encourages African developers and service providers to explore new business models, such as micropayment-based monetization, and supports regional economic integration, trade, and investment.

3. Challenges Facing Stablecoin Adoption

Despite strong potential, stablecoin adoption in Africa faces challenges related to government regulation, compliance, infrastructure, public perception, and trust.

Regulation and Compliance:

Most African countries are still exploring cryptocurrency regulation, lacking clear legal definitions and frameworks. Authorities are concerned about financial stability—particularly the relationship between non-local-currency-pegged stablecoins and fiat currencies. For example, Nigeria’s central bank fears widespread stablecoin adoption could undermine monetary policy control, trigger capital flight, and further devalue the Naira. Some stablecoins are pegged to dollars or other foreign assets; if reserve assets are poorly managed, they could spark financial panic and systemic instability—especially if stablecoins are widely used for transactions or savings. Additionally, the anonymity associated with certain cryptocurrencies may facilitate criminal activities such as money laundering or illicit financing, threatening financial security. Clearly defined regulatory frameworks and legal safeguards are therefore essential for stablecoin development.

Current status of cryptocurrency regulation in sub-Saharan Africa (Source: UNDP)

Limited Infrastructure:

Mobile networks (4G/5G) and internet connectivity are foundational to the digital economy. Currently, Africa’s 4G coverage stands at only 50%, far below the global average. Some areas still rely on 2G networks. Internet penetration across Africa is only about 30%, compared to much higher rates in developed nations like South Africa—this limits the development of both the digital economy and stablecoin ecosystems.

Global mobile network coverage (Source: International Telecommunication Union)

Internet users as percentage of population (Source: World Bank)

Social Concerns and Education:

The anonymity linked to crypto transactions often raises concerns about crime. Social engineering scams, phishing attacks, and fraudulent investment schemes targeting stablecoins can severely impact inexperienced users—especially those in rural areas or with limited tech exposure. Lack of awareness hinders mass adoption and makes people vulnerable to fraud or misinformation. Understanding how stablecoins work, their risks and benefits, and how to use them securely requires a certain level of financial literacy. Governments and relevant institutions must increase public awareness and deliver targeted financial education. Even fiat-pegged stablecoins may experience minor price fluctuations, which could concern potential users—especially those unfamiliar with crypto markets or with limited financial resources.

4. Case Studies

OnAfriq (MFS Africa)

OnAfriq (formerly MFS Africa) is Africa’s largest cross-border payment platform, founded in 2009, dedicated to advancing Africa’s digital economy through digital payment solutions and financial services. Operating in major economies such as Nigeria, South Africa, and Ghana, OnAfriq’s core offerings include digital wallets, cross-border payment solutions, stablecoin services, and fintech products.

As of 2024, OnAfriq serves over 500 million users across more than 40 African countries. Individual users leverage OnAfriq for daily transactions, international remittances, and micropayments, while businesses use its cross-border solutions and merchant payment services—especially for transactions with overseas suppliers and customers. OnAfriq supports multiple stablecoins, including USDC, USDT, DAI, and EURC, and has launched AfriqCoin, a dollar-pegged stablecoin specifically for cross-border payments, with fees as low as 0.5%–1%.

OnAfriq collaborates with international financial institutions and local banks such as Visa, Mastercard, Ecobank, and Stanbic Bank, and partners with Circle, a leading stablecoin provider, to expand its footprint in Africa using USDC’s stability and wide acceptance. The platform supports USDC for payments, transfers, storage, and offers DeFi products such as high-yield deposits, lending, and asset management.

OnAfriq has significantly enhanced financial inclusion in Africa, with over 500 million digital wallet users—most previously unbanked. It has provided financial education and training to over 1 million people, improving financial literacy. Its digital payment and stablecoin solutions (like AfriqCoin) have improved cross-border payment efficiency, reduced costs, and accelerated regional and international trade, cutting processing times to just 2 minutes. OnAfriq also provides payment gateway services for local e-commerce platforms and merchants, supporting online transactions and digital marketplace development. Going forward, OnAfriq plans to launch innovative products such as digital insurance and decentralized finance loans, continuing to drive Africa’s digital transformation.

AZA Finance

AZA Finance, established in 2013, is a leading fintech company in Africa specializing in cross-border payments and foreign exchange solutions. Through its innovative technology platform, AZA Finance optimizes cross-border payment processes and enhances liquidity between Africa and the rest of the world. As of 2024, AZA Finance has processed over 15 million transactions worth $9 billion, serving more than 1.5 million users across 183 countries.

AZA Finance’s cross-border payment solutions support the implementation of the African Continental Free Trade Area (AfCFTA). By simplifying payment procedures and lowering transaction costs, AZA Finance strengthens trade among AfCFTA member states, promoting regional economic integration.

AZA Finance supports USDC and USDT on its platform. In 2023, stablecoin transaction volume accounted for 30% of total volume on AZA Finance, reflecting strong market demand and acceptance.

WSPN

WSPN (Worldwide Stablecoin Payment Network) is a global digital payment company committed to advancing future digital payments and financial inclusion through cutting-edge distributed ledger technology (DLT). The company raised $30 million in seed funding from renowned investors including Foresight Venture and Folius Ventures.

In the global digital payments landscape, WSPN successfully entered the African market through a partnership with StableWallet, an innovative AA wallet. This collaboration laid a solid foundation for WSPN’s market penetration and financial inclusion goals in Africa, marking a key milestone in its global strategy.

Through diverse promotional campaigns, WSPN and StableWallet attracted a large number of new users to register and use WUSD. These users not only experienced the convenience of WSPN’s stablecoin payments but also received generous WUSD rewards.

Moreover, WSPN continues to enhance user experience and promote WUSD adoption in Africa through collaborations with other projects and innovative approaches such as building Telegram miniapp communities. Account-abstraction wallets make WSPN’s WUSD easier to use and enable seamless cross-chain payment experiences.

This partnership has enabled WSPN to achieve success in Africa—not only in rapid user growth but also in advancing financial inclusion through stablecoin technology. Moving forward, WSPN will continue collaborating with global partners to innovate digital payments in Africa and worldwide, building a more transparent, efficient, and user-friendly digital payment ecosystem.

Future Outlook

The success stories of OnAfriq, AZA Finance, and WSPN demonstrate how stablecoins can improve financial services and drive economic development in Africa. For other industries and tech companies in Africa, key entry points include:

1. Strengthen Financial Infrastructure

Develop local blockchain infrastructure to enhance transaction capacity and security, supporting larger volumes of stablecoin transactions. Promote interoperability among financial institutions and strengthen collaboration between banks and non-bank financial entities to build broader payment networks. Encourage public adoption of digital wallets for storing and transferring stablecoins, and further introduce DeFi and other on-chain financial infrastructure to improve usability.

2. Advance Policy and Regulatory Frameworks

For example, AZA Finance strictly complies with international and local financial regulations while supporting stablecoin payments, ensuring compliant operations. Governments should be encouraged to establish clear rules for stablecoin use and trading, creating legal space for operation while preventing illegal activities. Regional cooperation should be promoted to develop common regulatory standards, facilitating the legalization and standardization of cross-border stablecoin payments.

3. Enhance Public and Corporate Awareness and Acceptance of Stablecoins

OnAfriq has raised public awareness and acceptance through extensive user education and outreach. Online and offline educational programs, media campaigns, and financial literacy initiatives can help the public understand the advantages and usage of stablecoins. Collaborate with local businesses to encourage them to accept stablecoins as a payment method, increasing their use in commercial transactions. Promote stablecoin usage in everyday activities—such as paying bills, purchasing goods, and accessing services—to boost public familiarity and adoption.

4. Strengthen Partnerships and Build Strong Collaborative Relationships

OnAfriq’s partnership with Circle, a global stablecoin issuer, strengthened its competitiveness in the global payments market. Collaborating with stablecoin issuers like Circle and Tether can expand available options and use cases. Partnering with blockchain and fintech companies can enhance technical capabilities and optimize payment and transaction systems. Building relationships with international financial institutions can promote stablecoin adoption and expand the global payment network.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News