The Death of Decentralization and the Concentration of Power: U.S. Capital Is About to Complete the Handover of Control in the Crypto Utopia

TechFlow Selected TechFlow Selected

The Death of Decentralization and the Concentration of Power: U.S. Capital Is About to Complete the Handover of Control in the Crypto Utopia

All medicine has side effects—ETFs, flooded with continuous inflows, are merely pain-relieving capsules that cannot cure the root cause.

Author: YBB Capital Researcher Ac-Core

TL;DR

● In the long term, Bitcoin ETFs are not beneficial. There is a huge gap between Hong Kong's Bitcoin ETF trading volume and that of U.S. Bitcoin ETFs, making it undeniable that American capital is gradually taking control of the crypto market. Bitcoin ETFs have split the market into two distinct parts: the "white" segment operates under centralized financial regulation with only speculative trading as its sole financial attribute, while the "black" segment retains native blockchain vitality and more trading opportunities but faces regulatory pressure due to being considered "illegitimate";

● MicroStrategy has achieved efficient arbitrage among stocks, bonds, and Bitcoin through capital structure design, tightly linking its stock price fluctuations with Bitcoin prices, thereby realizing lower-risk returns over the long term. However, MicroStrategy is essentially issuing infinite debt on its assets, using unlimited leverage to inflate its value—this model relies on a sustained Bitcoin bull market to maintain its valuation. Therefore, Citron’s short position against MicroStrategy offers a higher reward ratio than directly shorting Bitcoin, yet MicroStrategy is betting decisively that Bitcoin’s future price trajectory will be a steady, low-volatility upward trend;

● Trump's pro-crypto policies will not undermine the dollar's status as the world's reserve currency but instead strengthen the U.S. dollar's pricing power in the crypto market. With one hand, Trump clings firmly to the dominance of the U.S. dollar, and with the other, he holds onto Bitcoin—the strongest weapon against national fiat devaluation—simultaneously reinforcing both positions and hedging risks.

I. American Capital Gradually Taking Control of the Crypto Market

1.1 U.S. vs. Hong Kong ETF Data

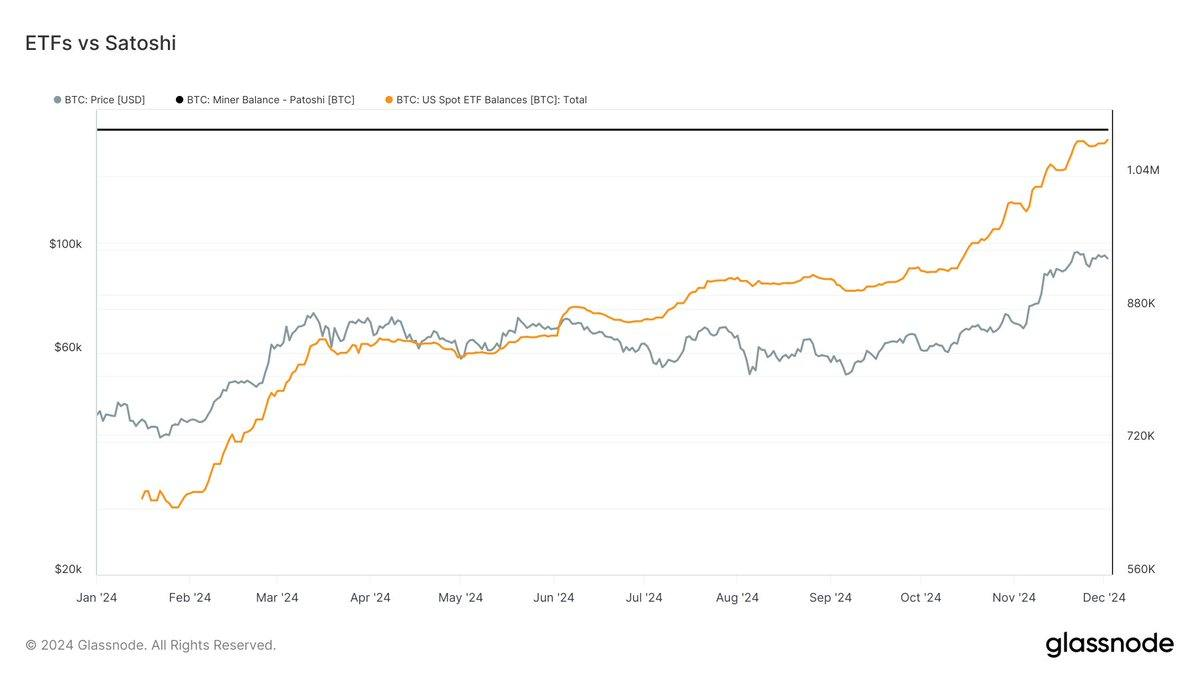

According to Glassnode data from December 3, 2024, U.S. spot Bitcoin ETF holdings were only 13,000 BTC away from surpassing Satoshi Nakamoto’s estimated holdings, standing at 1,083,000 BTC compared to 1,096,000 BTC respectively. The total net asset value of U.S. spot Bitcoin ETFs reached $103.91 billion, accounting for 5.49% of Bitcoin’s total market cap. Meanwhile, according to Aastocks on December 3, Hong Kong Exchange data showed that the combined trading volume of Hong Kong's three spot Bitcoin ETFs in November was approximately HK$1.2 billion.

Source: Glassnode

American capital is deeply engaging in and influencing the global crypto market—even leading the industry’s development. ETFs have transformed Bitcoin from an alternative asset into a mainstream one, but they’ve also weakened Bitcoin’s decentralization. While ETFs bring massive inflows of traditional capital, they also place Bitcoin’s pricing power firmly in the hands of Wall Street.

1.2 The “Black and White Divide” Created by Bitcoin ETFs

Classifying Bitcoin as a commodity means it must follow tax rules applicable to other commodities like stocks and bonds. However, the impact of launching a Bitcoin ETF differs significantly from launching ETFs for other commodities such as gold, silver, or crude oil. Currently approved Bitcoin ETFs differ fundamentally from broader market recognition of Bitcoin itself:

● The path to commoditization resembles a custodian (left hand) holding physical assets (like copper warehouses or bank gold vaults), who uses a central intermediary for custody and authorizes institutions to handle transfers and recordkeeping. On the right hand, after shares are issued (e.g., fund shares), shareholders buy and trade these shares with capital.

However, in this process, the front end (design, development, sales, and after-sales services) involves physical delivery, spot settlement, or cash settlement. Currently, the U.S. SEC-approved Bitcoin ETFs use cash settlement in the subscription and redemption phase—this is precisely what Cathie Wood has long contested, advocating instead for physical delivery, which remains practically unachievable.

This is because the cash custodians in the U.S. operate within the traditional centralized financial framework, conducting all subscription and redemption transactions centrally. Thus, the first half of the Bitcoin ETF mechanism is fully centralized.

● At the back end of Bitcoin ETFs, the centralized regulatory framework struggles to accommodate true decentralization. To recognize Bitcoin legally, regulators require it to fit within the existing centralized financial system as a commodity—but they refuse to acknowledge Bitcoin’s potential to replace fiat currencies or its untraceable, decentralized nature. Hence, Bitcoin can only undergo financial product derivatives such as futures, options, and ETFs when it fully complies with regulations.

Therefore, the creation of Bitcoin ETFs signifies a complete failure of the ETF-linked portion of Bitcoin to serve as an anti-fiat instrument. The decentralized essence of this segment becomes meaningless. The front end must rely entirely on regulated custodians like Coinbase, ensuring every transaction in the chain is legal, transparent, and traceable.

The emergence of ETFs creates a clear black-and-white divide in Bitcoin:

The current white segment: Operating under centralized regulatory frameworks, it enables broad financial product innovation aimed at reducing market volatility. As legitimate participants expand, Bitcoin’s speculative and volatile characteristics gradually diminish. After ETF approval, the white segment loses key demand drivers such as Bitcoin’s decentralization and anonymity, retaining only a single financial attribute—speculative tradability. Within the legalized regulatory framework, users must pay higher taxes, eliminating Bitcoin’s original functions of asset transfer and tax avoidance. Endorsement thus shifts from decentralized chains to centralized governments.

The former black segment: The primary reason for extreme volatility in crypto markets lies in their opacity and anonymity, which make them prone to manipulation. Yet, this black segment remains more open and vibrant with native blockchain values, offering greater trading opportunities. However, with the rise of the white segment, any part unwilling to transition into legitimacy will remain marginalized under centralized regulation and lose pricing power—akin to paying fines to the SEC.

II. Trump’s Pro-Crypto Cabinet Picks

2.1 Cabinet Nominees

Following Donald Trump’s victory in the 2024 U.S. presidential election, his administration is expected to adopt a more open stance toward cryptocurrencies compared to the restrictive policies of the Biden-era SEC, Federal Reserve, and FDIC. According to Chaos Labs data, the following are key nominations in Trump’s new cabinet:

Source: @chaos_labs

Howard Lutnick (Transition Team Leader & Secretary of Commerce nominee): As CEO of Cantor Fitzgerald, Lutnick publicly supports cryptocurrencies. His company actively explores blockchain and digital assets, including strategic investments in Tether.

Scott Bessent (Treasury Secretary nominee): A veteran hedge fund manager, Bessent supports crypto, viewing it as a symbol of freedom and a long-term fixture. He is notably more favorable toward crypto than previous Treasury candidates like Paulson.

Tulsi Gabbard (Director of National Intelligence nominee): Gabbard champions privacy and decentralization, supports Bitcoin, and invested in Ethereum and Litecoin back in 2017.

Robert F. Kennedy Jr. (Secretary of Health and Human Services nominee): Kennedy openly backs Bitcoin as a hedge against fiat depreciation and could become a strong ally for the crypto industry.

Pam Bondi (Attorney General nominee): Bondi has not made clear statements on crypto; her policy direction remains uncertain.

Michael Waltz (National Security Advisor nominee): Waltz actively supports cryptocurrencies, emphasizing their role in enhancing economic competitiveness and technological independence.

Brendan Carr (FCC Chairman nominee): Known for opposing censorship and supporting tech innovation, Carr may provide critical infrastructure support for the crypto sector.

Hester Peirce & Mark Uyeda (Potential SEC Chair candidates): Peirce is a staunch crypto advocate calling for clearer regulation. Uyeda criticizes the SEC’s aggressive stance on crypto and advocates for defined regulatory rules.

2.2 Pro-Crypto Policies as a Hedge Against Eroding Trust in the Dollar’s Global Reserve Status

Could the White House’s promotion of Bitcoin undermine confidence in the U.S. dollar as the global reserve currency and weaken its position? U.S. scholar Vitaliy Katsenelson argues that amid growing market unease about the dollar, promoting Bitcoin might further erode trust in the dollar’s reserve status. Regarding current fiscal challenges, he notes: “What will truly keep America great isn’t Bitcoin—it’s controlling debt and deficits.”

Trump’s approach may actually serve as a risk hedge for the U.S. government against a potential loss of dollar dominance. In the context of economic globalization, every nation seeks international circulation, reserve, and settlement status for its own currency. However, the trilemma of monetary sovereignty, free capital flow, and fixed exchange rates persists. Bitcoin’s key value lies in offering a novel solution to institutional contradictions and economic sanctions in a globalized economy.

Source: @realDonaldTrump

On December 1, 2024, Trump posted on X (formerly Twitter) stating that the BRICS nations’ attempt to move away from the dollar is over. He demanded these countries commit not to create a new BRICS currency or support any alternative to the dollar, warning that failure to comply would result in 100% tariffs and exclusion from the U.S. market.

Today’s Trump appears to be gripping the dollar’s hegemony with one hand while refusing to let go of Bitcoin—the strongest weapon against national fiat distrust—with the other, simultaneously reinforcing both the dollar’s global settlement dominance and the crypto market’s pricing authority.

III. The Battle Between MicroStrategy and Citron Capital

During U.S. trading hours on November 21, well-known short-seller Citron Research announced plans to short MicroStrategy (MSTR), labeled as a “Bitcoin-heavy stock,” causing MSTR’s share price to plunge sharply, dropping over 21% from intraday highs.

The next day, MicroStrategy Executive Chairman Michael Saylor responded in a CNBC interview, stating that the company profits not only from Bitcoin’s volatility but also leverages ATM (At-The-Market) mechanisms to increase Bitcoin investment. Thus, as long as Bitcoin continues rising, the company remains profitable.

Source: @CitronResearch

In summary, the premium in MicroStrategy (MSTR) stock, its profit strategy via the ATM mechanism, its leveraged Bitcoin investment operations, and short-sellers’ perspectives can be summarized as follows:

1. Source of Stock Premium:

MSTR’s premium largely stems from the ATM mechanism. Citron Research believes MSTR stock has become a substitute investment vehicle for Bitcoin, arguing that its stock price carries an unjustified premium relative to Bitcoin, justifying their short position. However, Michael Saylor refutes this, asserting that short-sellers overlook MSTR’s core profitability model.

2. MicroStrategy’s Leveraged Operations:

Leverage and Bitcoin Investment: Saylor explains that MSTR uses debt financing to lever up its Bitcoin investments, profiting from Bitcoin’s volatility. The company employs the ATM mechanism for flexible fundraising, avoiding discount issuance typical in traditional financing, while leveraging high trading volumes to execute large-scale stock sales and capture arbitrage opportunities from stock premiums.

3. Advantages of the ATM Mechanism:

The ATM model allows MSTR to raise capital flexibly, shifting debt volatility, risks, and performance onto common equity. Through this structure, the company achieves returns far exceeding borrowing costs and even Bitcoin’s price gains. For instance, Saylor notes that investing in Bitcoin with 6% interest funding yields an effective return of about 80% if Bitcoin rises 30%.

4. Specific Profit Case:

By issuing $3 billion in convertible bonds, the company expects to generate $125 in earnings per share over ten years. If Bitcoin prices continue rising, Saylor forecasts substantial long-term gains. For example, two weeks prior, MSTR raised $4.6 billion via the ATM mechanism at a 70% premium, acquiring $3 billion worth of Bitcoin within five days—equivalent to $12.50 per share—with projected long-term profits reaching $33.6 billion.

5. Risk of Bitcoin Price Decline:

Saylor emphasizes that buying MSTR stock means investors accept the risk of Bitcoin price drops. High returns require accepting corresponding risks. He projects Bitcoin will rise 29% annually, while MSTR’s stock will grow 60% per year.

6. MSTR’s Market Performance:

Year-to-date, MSTR’s stock has surged 516%, outperforming Bitcoin’s 132% gain and even Nvidia’s 195% rise as an AI leader. Saylor claims MSTR has become one of the fastest-growing and most profitable companies in the U.S.

Regarding Citron’s short position, MSTR’s CEO stated that Citron fails to understand the source of MSTR’s premium over Bitcoin:

“If we invest in Bitcoin using funds borrowed at 6% interest, and Bitcoin rises 30%, our actual gain is effectively 80%—a function combining stock premium, conversion premium, and Bitcoin appreciation.”

“We issued $3 billion in convertible bonds. At an 80% Bitcoin spread, this investment will generate $125 in earnings per share over ten years.”

This implies that as long as Bitcoin keeps rising, the company continues to profit:

“Two weeks ago, we executed a $4.6 billion ATM offering, trading at a 70% spread, meaning we earned $3 billion in Bitcoin within five days—about $12.50 per share. Over ten years, this translates to $33.6 billion, or roughly $150 per share.”

In conclusion, MicroStrategy’s business model leverages structured capital design to achieve efficient arbitrage across stocks, bonds, and Bitcoin, tightly coupling its stock price to Bitcoin’s movements to ensure low-risk profitability over long cycles. Yet, MicroStrategy’s core operation involves infinite debt issuance and infinite leverage to inflate its own value—a model dependent on a prolonged Bitcoin bull market. Undoubtedly, Citron’s short bet on MicroStrategy offers a much higher payoff ratio than shorting Bitcoin directly, which suggests that MicroStrategy is confidently betting on a future of slow, stable, low-volatility Bitcoin price increases.

IV. Conclusion

Source: Tradesanta

The United States is continuously strengthening its control over the crypto industry, and market opportunities are increasingly shifting toward centralization. The utopian vision of decentralized crypto is gradually compromising with centralized systems, effectively “handing over” power. Every medicine has side effects—ETFs bringing in endless capital are merely pain-relieving capsules that cannot cure the underlying disease.

In the long run, Bitcoin’s approval via ETFs is not a positive development. The massive disparity between Hong Kong’s and the U.S.’s Bitcoin ETF trading volumes clearly shows that, based on capital scale, American capital is progressively dominating the crypto market. Despite China’s absolute leadership in mining, it still lags behind in capital markets and policy guidance. Perhaps the long-term impact of Bitcoin ETFs will accelerate the normalization of crypto asset trading—this marks both a beginning and an end.

References: Fu Peng: Discussing the SEC and Bitcoin ETF – The Clear Divide of Centralization

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News