Web3 Startup Survival Guide: Struggling to Secure VC Funding, But Stay Flexible, Resilient, and Courageous in Moving Forward

TechFlow Selected TechFlow Selected

Web3 Startup Survival Guide: Struggling to Secure VC Funding, But Stay Flexible, Resilient, and Courageous in Moving Forward

The two core elements of a seed round: signal and insight.

Author: Ishita Srivastava

Translation: TechFlow

Fundraising isn't easy—whether you're a first-time founder or a seasoned builder, it feels like navigating a storm without a map. This article could easily send you into despair, but today we're staying positive.

Image: Founders navigating the DeFi/VC liquidity pool

In part one, we’ll dive into the fundamentals of angel investing and venture capital in crypto. Understanding what drives their investment decisions is crucial to grasping why they accept or reject deals.

We'll explore their primary goals when selecting investments, how they process deals, and the three key criteria they use to evaluate potential opportunities.

Next, we’ll examine common failure points, drawing from personal experience and insights from repeat founders who’ve navigated this rugged terrain. Ultimately, I hope to equip you with knowledge for a clearer perspective on fundraising and better preparation for its challenges.

Cheer up, friends—we've got this.

Your Angel Investors

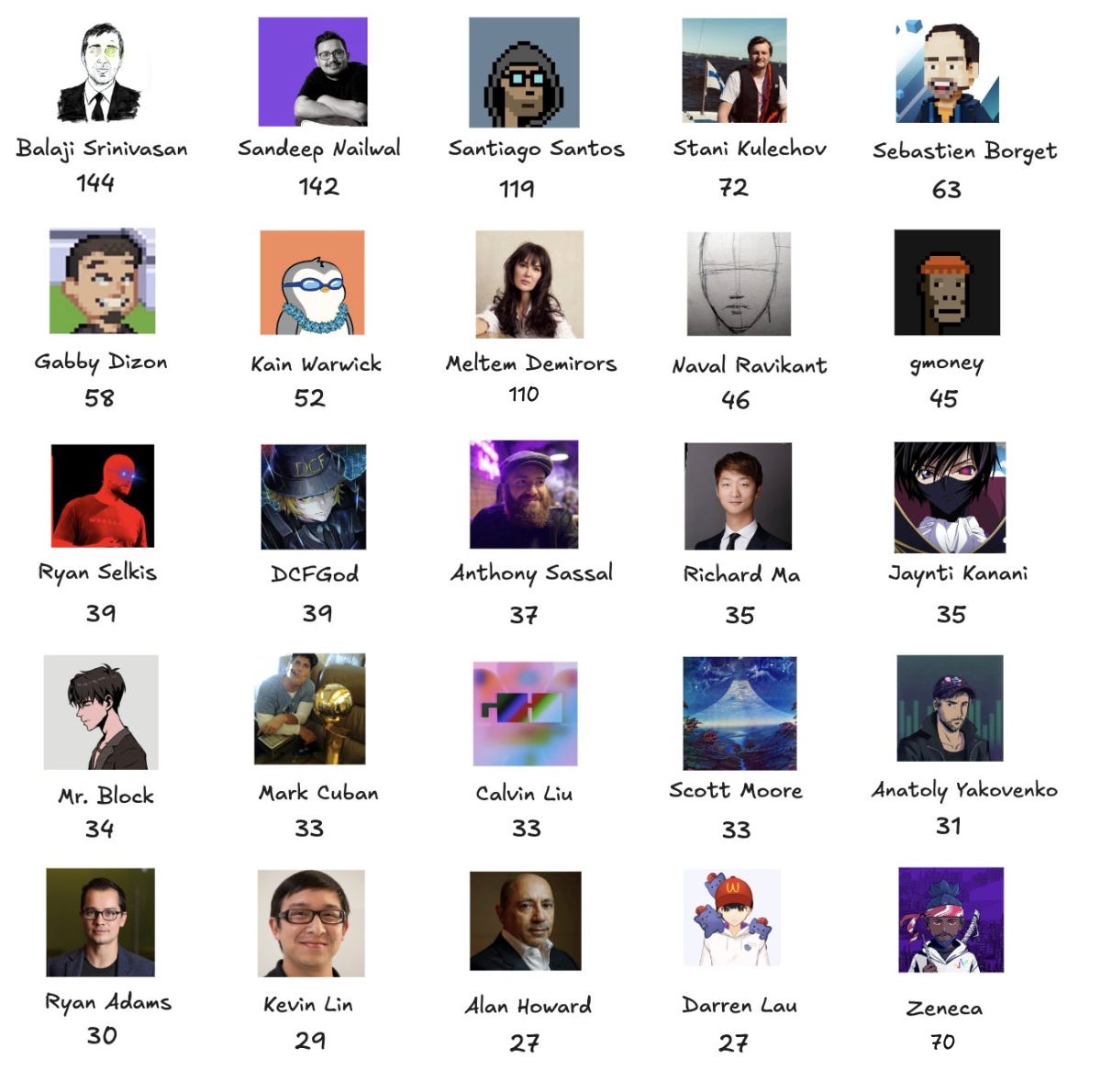

Founders typically raise their first angel round from Twitter friends and Discord communities. During this process, cap table construction is critical. Founders often bring on angels who make noise but offer little real support, disappearing when introductions or meaningful feedback are needed. The harsh truth is: if someone has done over 150 deals in the past year, they’re probably not the reliable signal you need.

Image: Top angel investors ranked by number of deals, source: Rachit

What Drives Angel Investing?

Angel investing is highly network-dependent. Some angels, like Polygon’s founders, back ecosystem projects; others, like GMoney and Zeneca in the NFT space, operate within specific influence circles. Yet ROI remains the primary driver for most angel investors.

A frustrating subset of angels invest purely for signaling—hopping onto hot cap tables hoping to unlock more deal flow. While I don’t hold them in high regard, used strategically, they can still help build connections. This leads us to two core elements of angel rounds: signal and insight.

Signal vs Insight

Signals are industry-specific. In Solana DeFi, having Mert or Anatoly onboard signals success. In gaming, an endorsement from Ellio Trades shows deep domain understanding. But getting support from Avalanche’s ecosystem lead for a ZK project? Probably less useful.

Insight, on the other hand, can compress months of work into weeks—for example, experts like DCF God sharing TVL strategies. At the angel stage, you need both signal and insight, but expect your cap table might be 90% signal and 10% insight.

Cap Table Construction & Due Diligence

Finding the right angels not only boosts credibility but also lays the foundation for riskier, higher-return future rounds.

You’re selling ownership at the best price possible, so you must clearly understand the added value each angel brings and know how to leverage it effectively. Core angels use their networks to help complete your cap table. Most angel rounds are high-risk, high-reward—they might lead you to top-tier funds or simply fall flat. These deals are heavily network-driven, and due diligence (DD) at this stage is usually light—a simple pitch deck often suffices to get started.

The smartest founders keep their round open through Series A, allowing valuable stakeholders to join at steep discounts. VCs typically don’t mind this “backdoor” approach because it increases overall company value.

Once you’ve solidified your early angel cap table, you enter the bigger leagues: venture capital. In the next section, we’ll explore how VC firms operate.

Venture Capital

In this section, we’ll look at things from the investor’s perspective. Who’s driving these investors? What ROI expectations do limited partners (LPs) have for fund performance? How does the VC ecosystem function? We’ll dive into why VCs choose certain investment strategies, typical deal processes, and why ROI remains the dominant force behind most investment decisions.

Limited Partners: The Top of the Liquidity Chain

Image: The big boss

At the top of the liquidity chain are the limited partners (LPs) who provide capital to VC funds. In crypto, these LPs are typically early adopters—investors, operators, and miners who accumulated wealth in prior cycles. After experiencing exponential returns, they now expect fast, outsized returns from venture investments.

Crypto investments are often token-based, involving vesting schedules, liquidity events, and market cycles that move much faster than traditional equity. As a result, expected return timelines are far shorter. Holding capital in slow-moving, long-cycle projects carries high opportunity costs, so LPs demand faster ROI, pushing VCs to invest at a pace matching market volatility and speed.

While pressure from LPs doesn’t directly reach investment teams—due to legal separation—the reality is funds know they must deliver 1000x returns to satisfy LPs if they want to raise Fund-3 or Fund-4.

Image: Venture capitalists raising a new fund

Ultimately, this dynamic makes crypto venture capital unique: capital is impatient, risk is high, and margin for error is slim. VCs know they must outperform competitors and deliver quickly to meet rising LP expectations. However, this is shifting as more mature capital re-enters the space—including pension funds, family offices, and web2 VCs.

Inside the Investor’s Mind

An interesting mix emerges: LP capital combined with analysts and associates, many fresh out of college with little operational experience (myself included). These analysts are expected to process over 360 deals annually across diverse areas—from ZK to modular infrastructure.

Image: A dramatized and simplified view of Q2 2023 crypto venture activity

This toxic dynamic—driven by rampant speculation—has created frothy fundraising environments. Sadly, founders outside traditional success circles—like Ivy League alumni, Singapore VC networks, or London web3 running groups—are hit hardest. They’re often disadvantaged because a) they don’t understand how crypto VCs process deals, and b) have limited access to capital allocators, forcing them to rely solely on the strength of their idea, with almost no room for error.

It’s a brutal reality, but if you’re reading this as an investor, I strongly suggest inviting five non-traditional pitches each month. We can fix this systemic issue—one deal at a time. Now, back to the agenda.

Deal Flow in Motion

For an investment committee (IC) to approve a deal, Monday morning conditions must be perfect: the deal lead needs to have circulated a 20-page investment memo by Thursday of the prior week (with final tweaks Sunday night), and the CIO’s coffee temperature must be just right.

The first discussion point is usually strategic fit. The deal must align with the firm’s investment thesis—infrastructure, gaming, Bitcoin ecosystem, etc. Then, the deal lead presents her case: why this is an interesting problem worth solving, what makes the solution unique, why this team is the right one, and what kind of returns participation could generate.

At its core, the deal lead focuses on ROI and risk.

ROI

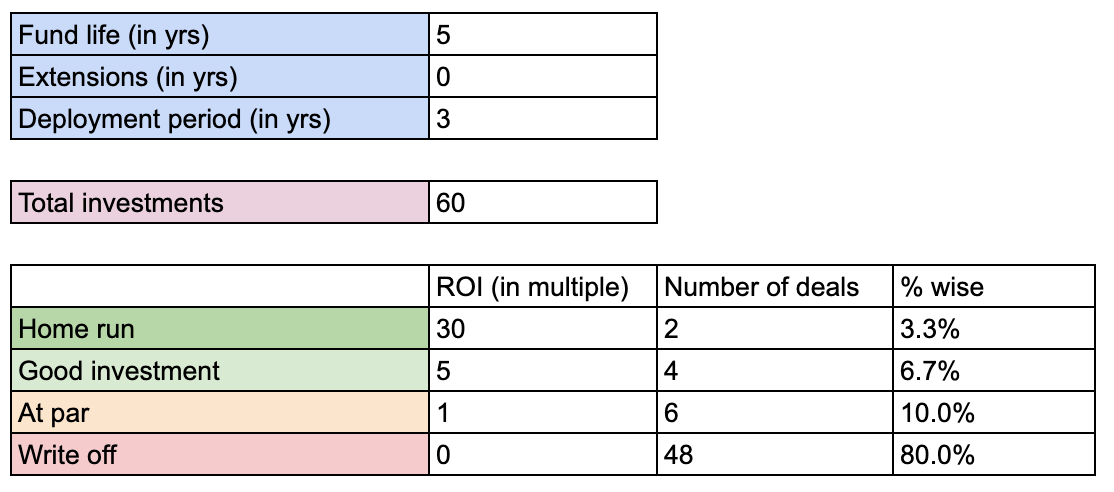

Let’s examine a typical portfolio construction to understand average ROI expectations:

Overly optimistic portfolio construction in crypto VC around 2021

Everyone at a VC firm dreams of landing the home-run deal, while more seasoned investors are willing to swing at 1-in-100 moonshots. A 30x return matters, but even a 5x can be attractive from a portfolio standpoint if the risk is low enough.

To illustrate: entering a deal at a $25M valuation with a potential $250M exit offers better risk-adjusted ROI than joining a hyped $1B seed round where a 10x is unlikely. Though WLD pulled it off.

In this cycle, funds are increasingly cautious about lock-up periods. A project up 60x at TGE but down to 2x at unlock is far from a win. We’re seeing polarization—either you’re raising a $7M seed or scrambling to piece together $1M from tier-three investors, with little middle ground.

Recap

VCs spend roughly 40 seconds per pitch, making it essential to align with their investment framework to survive the fierce competition in crypto venture. Over time, this framework has distilled into single-line views on most sectors:

-

Too many Bitcoin infrastructure projects; large investors aren’t interested;

-

NFTs seen as last cycle’s trend;

-

DeFi? Most infrastructure is already built. Top investors stay flexible, constantly updating their stance by reading and following thought leaders.

Founders who deeply research competitors are hidden gems in the investment market. For founders, the key insight is this: by 2024, the investor you’re pitching likely saw a similar deal—and may have lost money on it. Your job isn’t just to explain why past attempts failed (showing industry understanding), but to demonstrate why you’ll succeed. Whether through execution insight, customer validation, or technical strength, you must redefine the project’s ROI. With every cycle, benchmarks grow more sophisticated.

In my career, I’ve used strict frameworks to evaluate deals, but frankly, (more often than I’d admit) strong deal flow and founder-problem fit heavily influence my decisions.

Rejection Is Always Unpleasant

That’s why investors often give generic responses like “not the right timing” or “doesn’t fit our thesis” when declining. But here are some real reasons I personally pass on deals:

-

Founder-market mismatch: Lack of relevant experience is a red flag. For example, custody businesses require enterprise sales expertise, so the founder’s background must closely match the problem.

-

No competitive edge: Without advantages—better distribution, higher TVL, more users, or stronger tech—it’s hard to gain traction. Pitching the 17th stablecoin is tough when a Stanford cryptography PhD is already building something similar.

-

Low-ROI/high-risk sectors: Some industries simply can’t deliver the returns most funds seek. DAO deals often fall here. Likewise, most funds avoid gaming due to high failure risk.

-

Zero-knowledge issues: Sometimes a great project just doesn’t fit our thesis. For instance, unless led by someone known for deep technical DD, I won’t touch ZK-heavy projects.

-

SAFT > SAFE: Equity requires more DD and offers less flexibility than token raises.

-

Over-pivoters: Founders who frequently shift direction to chase trends often lose investor trust.

-

Distribution bottlenecks: If MetaMask or another giant builds a similar feature, your distribution advantage vanishes overnight. I won’t bet on that.

Of course, not every rejection is correct. Some deals I passed on later performed exceptionally well. My anti-portfolio hurts—when chatting with VC peers, Celestia and Botanix are the most painful misses we share.

Fundraise Like a Winner

Many technically focused founders dread pitching—it feels too salesy. But surviving without this skill is unrealistic. Pitching to investors is a professional competency, and your pitch deck and data room are like quality running shoes. Sure, you can run 5km barefoot, but why would you?

Yes, Make a Pitch Deck

As discussed, investors face overwhelming deal flow. Unless you already have strong relationships, polished sales materials (pitch deck, data room) will help you find lead or anchor investors faster.

Pitch Relentlessly

Another key step: practice pitching as much as possible and gather feedback. You must master your narrative—no awkwardness allowed. The more people you talk to (marketers, BD, engineers—anyone willing to listen), the sharper and stronger your pitch becomes. Demo days and VC events are excellent for testing pitches and getting real-time feedback from diverse audiences.

Further reading: The Art of Feedback

As I mentioned, people hate saying “no”—it’s basic psychology. So investors often give vague rejection reasons. For investors you respect, don’t hesitate to ask for specific feedback. Most may decline, but those confident enough to engage will offer valuable insights, helping you truly understand weaknesses in your thesis.

Warm Intros Rule

The crypto world is small—warm intros matter immensely. Cold DMs are inefficient; I once sent 60 and got only 5 replies. Instead, invest time building genuine relationships on platforms like Twitter and Telegram—where connections count. Similarly, submitting via website forms rarely works—99% of funds I know either have interns review them or worse, no one reads them at all.

Image: The only metaverse that matters is Twitter

The beauty of crypto is everyone’s on Twitter. It’s an open platform to build authentic relationships. Rushi from Movement is a great example—he effectively used Twitter to generate leads. Best approach? Warm intros—from people you chat with on Twitter or Telegram, or meet at conferences (though I find conferences quite inefficient). Spending a month actively engaging on Twitter before fundraising is the best way to build investor rapport. Founder-to-founder intros are ideal, but sadly, many are stingy when referring investors.

Even my investor friends who entered in 2020 and transitioned to builders this cycle struggled with pitching and securing warm intros. So yes—it’s genuinely hard.

Better Days Ahead

Startup failure rates are as high as 99%. Many things can go wrong—poor product-market fit, difficulty assembling the right team, weak execution, low sector ROI, or simply bad timing.

Yet in fundraising, I repeatedly see specific failure points. At the execution level, failures stem from poor founder-problem fit, inadequate research, incomplete documentation, or underdeveloped pitches. Mid-ROI sectors, oversaturated markets, and overreliance on cold outreach can quickly kill a deal.

What to Do After a Failed Raise?

This is tough to answer—if investor interest is low, should you still push forward? The answer: it depends.

Flexibility during fundraising is crucial. If you fail to close a round or consider quitting, remember—the design space remains wide open. If you show growth and learning, top investors will gladly back you again. Stay in learning mode always.

Hear from Anonymous, a repeat founder in the space. He shares this key lesson:

There’s a difference between knowing when to stop and actually admitting it. In [Project 1], I held on until the end because I believed (and still believe) VC was wrong—there will eventually be a market for options and derivatives in DeFi. But I knew from the start fundraising would be tough.

Looking back, the biggest mistake was fundraising ad-hoc and launching the product during fundraising—this quantified our opportunity before we were ready. Better to wait until you’ve raised enough to refine the product before going public. A hard-earned lesson.

Ultimately, [Project 2] succeeded precisely because I did the opposite: built credibility, attracted interest, and closed big deals. One investor gave me $2M to deploy freely—simply because my cap table was clean and I’d earned their trust as a serious builder.

—Anonymous, anonymous founder

Where to Go From Here?

My journey in crypto venture has been a rollercoaster. Fresh out of college, I entered during 2021’s boom. Since then, my investment bar has evolved. Today, I focus primarily on a founder’s ability to handle risk and failure. No DDQ captures this fully, but luckily, sifting through endless decks is no longer my KPI. This freedom allows deeper engagement with founders, helping me spot those I believe will succeed and invest more time in those relationships.

The truth is, fundraising is often gut-wrenching—a grind, not a triumph. But every failure brings growth. My conversations with founders and investors are now richer and deeper, centered on resilience, adaptability, and the courage needed to move forward.

In the end, the journey keeps moving forward. Stay resilient. Keep going.

Life’s fun, Anonymous. Don’t take it so seriously.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News