From Credit Card Networks to Stablecoin Market Opportunities

TechFlow Selected TechFlow Selected

From Credit Card Networks to Stablecoin Market Opportunities

In the credit card ecosystem, major companies have risen through coordination, innovative issuance, and enabling form factors—similar principles apply to stablecoins as well.

Author: Alana

Translation: TechFlow

Stablecoins represent the most transformative evolution in payment forms since credit cards, reshaping how money moves. With low-cost cross-border transactions, near-instant settlement, and global access to widely demanded currencies, stablecoins have the potential to improve financial systems. For those holding the U.S. dollar deposits that back these digital assets, they can also be a highly profitable business.

Currently, the total global supply of stablecoins exceeds $150 billion. Five stablecoins have more than $1 billion in circulation: USDT (Tether), USDC (Circle), DAI (Maker), First Digital USD (Binance), and PYUSD (PayPal). I believe we are moving toward a world with more stablecoins—a world where every financial institution will issue its own stablecoin.

I’ve been thinking about the opportunities emerging from this growth. Looking at the maturation of other payment systems, particularly credit card networks, may offer valuable insights.

How similar are credit card networks and stablecoin networks?

To consumers and merchants, all stablecoins should feel like dollars. In reality, however, each stablecoin issuer handles the dollar differently—due to variations in issuance and redemption processes, reserve structures backing each coin’s supply, differing regulatory regimes, audit frequencies, and more. Addressing these complexities presents a major business opportunity.

We've seen something like this before with credit cards. Consumers use assets that are nearly interchangeable but not perfectly so—these assets function as dollars (they're loans denominated in dollars), yet differ because individual creditworthiness varies. Networks such as Visa and Mastercard coordinate payments across the system. And stakeholders in both systems—consumers, issuing banks, acquiring banks, and merchants—look remarkably similar (and may eventually align even more closely).

An example might help illustrate the structural similarities.

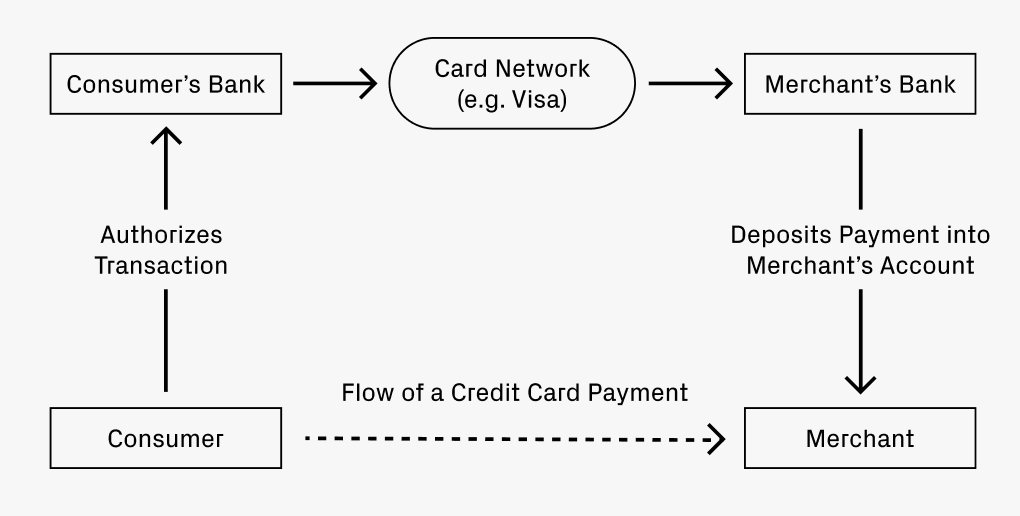

Suppose you go out for dinner and pay your bill with a credit card. How does your payment reach the restaurant's account?

-

Your bank (the card-issuing bank) authorizes the transaction and sends funds to the restaurant’s bank (known as the acquirer).

-

A switching network—such as Visa or Mastercard—facilitates the transfer and charges a small fee.

-

The acquirer then deposits the funds into the restaurant’s account, deducting a fee.

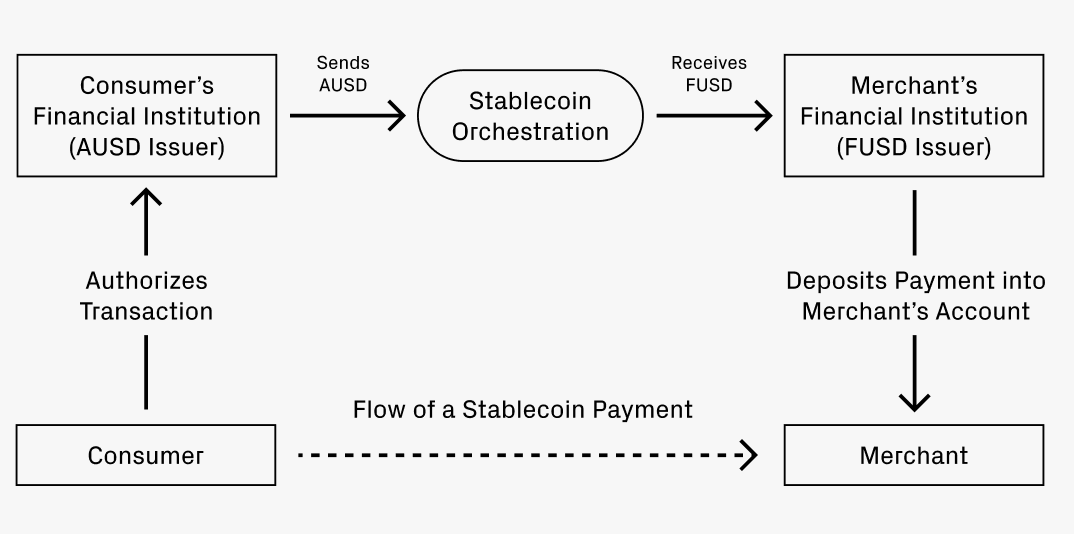

Now imagine you want to pay using stablecoins. Your bank, Bank A, issues the stablecoin AUSD. The restaurant’s bank, Bank F, uses FUSD. These are two different stablecoins, although both represent dollars. The restaurant’s bank only accepts FUSD. How is an AUSD payment converted into FUSD?

Ultimately, this process will resemble the credit card model very closely:

-

The consumer’s bank (issuer of AUSD) authorizes the transaction.

-

A coordination service facilitates the exchange from AUSD to FUSD and may charge a small fee. This swap could occur in several ways:

-

Path 1: Use decentralized exchanges (DEXs) for direct stablecoin-to-stablecoin swaps. For example, Uniswap offers multiple liquidity pools with fees as low as 0.01%. (3)

-

Path 2: Redeem AUSD into a U.S. dollar deposit, then deposit those dollars into the acquirer to issue FUSD.

-

Path 3: The coordination service nets flows across the network; this would likely only become feasible at scale.

-

-

FUSD is deposited into the merchant’s account, possibly with a fee deducted.

Where the analogy begins to diverge

The above outlines the clear parallels I see between credit card networks and stablecoin networks. It also provides a useful framework for understanding where stablecoins begin to meaningfully upgrade and surpass certain aspects of credit card systems.

The first difference lies in cross-border transactions. If the scenario above involved a U.S. consumer dining at a restaurant in Italy—where the customer wants to pay in dollars and the merchant wishes to receive euros—existing credit card networks typically charge over 3% in fees. In contrast, swapping stablecoins on a decentralized exchange (DEX) could cost as little as 0.05% (a 60x difference). Scaling this reduction across global cross-border payments reveals clearly how much productivity stablecoins could add to global GDP.

The second difference involves payments from businesses to individuals. The time between payment authorization and actual fund withdrawal from the payer’s account is extremely short: once authorized, funds can leave the account immediately. Instant settlement is both valuable and highly desirable. Moreover, many businesses employ a global workforce. The frequency and volume of their cross-border payments may far exceed those of typical consumers. The trend toward a globalized labor force should strongly drive demand for this capability.

Looking ahead: Where might opportunities lie?

If the structural comparison holds directionally, it helps illuminate potential entrepreneurial opportunities. In the credit card ecosystem, major players rose through coordination, innovative issuance, and enabling form factors. The same applies to stablecoins.

The earlier example mainly described the role of coordination. That’s because moving money is big business. Visa, Mastercard, American Express, and Discover all have market capitalizations of at least tens of billions of dollars, collectively exceeding $1 trillion. The existence of multiple successful card networks shows healthy competition and a large enough market to support major players. It’s reasonable to assume that in a mature market, coordination among stablecoins will similarly support competitive dynamics. We have only 1–2 years to build sufficient infrastructure for stablecoins to succeed at scale. New startups still have time to pursue this opportunity.

Stablecoin issuance is another area ripe for innovation. Just as corporate credit cards grew in popularity, we may see a similar trend of companies wanting their own white-label stablecoins. (TechFlow note: A white-label stablecoin is issued by a company or organization but carries the issuer’s branding and identity rather than that of the underlying technology provider.) Owning a spending instrument allows better control over accounting processes—from expense management to handling foreign taxes. This could become a direct revenue line for stablecoin coordination networks, or an opportunity for new startups (for example, similar to Lithic). Derivatives of this enterprise demand could spawn even more new ventures.

Issuance can also become increasingly specialized in many ways. Consider the emergence of tiering. With many credit cards, customers pay a premium fee to access better reward structures, such as the Chase Sapphire Reserve or AmEx Gold. Some companies—even airlines and retailers—offer exclusive co-branded cards. I wouldn’t be surprised to see similar experimentation with tiered stablecoin rewards. This too could open doors for startup innovation.

In many ways, these trends reinforce each other. As issuance diversifies, demand for coordination services grows. As coordination networks mature, the barrier to entry for new issuers falls. All of this represents massive opportunity, and I look forward to seeing more startups emerge in this space. In the long run, these markets will reach trillion-dollar scales and should be able to support many large companies.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News