The Myth Behind the Rare Synchronized Decline in Dollar, Gold, and Bitcoin: Is It Due to Yen Interest Rate Hikes and the Reversal of Carry Trades?

TechFlow Selected TechFlow Selected

The Myth Behind the Rare Synchronized Decline in Dollar, Gold, and Bitcoin: Is It Due to Yen Interest Rate Hikes and the Reversal of Carry Trades?

The asset decline caused by the yen carry trade turmoil will eventually pass, but where will Japan's monetary policy and macroeconomy go from here?

Author: Kamiu

Opinions in a nutshell

-

After the major macro week in July, the U.S. dollar, gold, and Bitcoin all declined simultaneously—typically, these three assets tend to move inversely.

-

This was primarily due to increased margin requirements from unwinding yen carry trades, sharply raising demand for liquidity, leading to widespread liquidation of gold and Bitcoin positions to secure U.S. dollar funding.

-

The Bank of Japan's (BOJ) rate hike reflects its determination to defend the yen exchange rate. While this move does not clearly correlate with asset prices in the long term, it may have deeper implications for Japan’s macroeconomy, particularly impacting foreign trade and the rebuilding of high-end manufacturing.

1. The rare simultaneous decline in USD, gold, and Bitcoin in July occurred mainly due to a reversal in yen carry trades causing temporary liquidity shortages

Historically, a sharp concurrent drop in dollar-denominated gold and Bitcoin is a low-probability event. First, being priced in U.S. dollars means their prices naturally exhibit a negative correlation with the U.S. Dollar Index—when the dollar strengthens, gold and Bitcoin tend to weaken, so both typically move in tandem with shifts in the dollar index. Second, both Bitcoin and gold are assets outside the control of sovereign monetary authorities, possess anti-inflation characteristics, and have high liquidity. These shared intrinsic features generally lead their prices to move positively together.

As assets negatively correlated with the dollar index, when prices or yields of dollar-denominated assets like U.S. Treasuries fall, gold and Bitcoin would normally be expected to rise due to capital inflows. However, in early August 2024, despite weak U.S. economic data—including disappointing July non-farm payrolls and Q2 CPI pointing toward economic slowdown or even recession—and growing certainty of a Fed rate cut in September, the U.S. dollar index plummeted while gold and Bitcoin prices also dropped significantly.

We believe this was primarily triggered by the BOJ’s first interest rate hike since exiting Yield Curve Control (YCC), which reversed yen carry trades. After Japan’s economic crisis in the 1990s, to alleviate balance sheet issues and bank runs among primary dealers, Japanese monetary policy entered a prolonged low-interest-rate era to combat strong deflationary pressures, widening the interest rate gap between Japan and the U.S. In the 21st century, the 2008 subprime crisis hit Japan harder due to the BOJ’s delayed response, while an aging population intensified pressure on pension and healthcare spending, straining public finances. This ultimately led “Abenomics” to adopt more aggressive negative interest rates and large-scale QE expansion. Under this backdrop, the Japan-U.S. interest rate differential widened further, giving rise to yen carry trades.

Specifically, yen carry trade involves borrowing yen at extremely low rates, converting them into U.S. dollars, and investing in dollar-denominated assets. Traders engaging in such arbitrage are colloquially known as "Mrs. Watanabe." With long-term interest rate spreads between Japan and the U.S. consistently above 3% (reaching up to 5% in recent years), carry trades offered nearly risk-free returns, making them increasingly popular—measured by foreign investors’ financing volume in Japan. For example, Warren Buffett’s massive borrowing in yen to buy Japanese equities was driven by the fact that yen-denominated financing had the lowest cost among major currencies.

This time, the BOJ’s rate hike exceeded expectations, and Governor Kazuo Ueda delivered unexpectedly hawkish remarks, causing Japanese market rates, the yen exchange rate, and JGB yields to surge simultaneously. The Japan-U.S. interest rate spread narrowed sharply in a short period, rendering carry trades unprofitable or even loss-making. To avoid forced liquidation of leveraged positions, global “Mrs. Watanabes” had no choice but to unwind other safe-haven holdings (gold, Bitcoin) and convert them into U.S. dollars to meet margin calls. This generated sudden heavy selling pressure on Bitcoin and gold, resulting in the rare phenomenon of the U.S. Dollar Index, gold, and Bitcoin all plunging at once.

Therefore, the post-BOJ-hike crash in gold and Bitcoin was largely due to a cash flow-level contingency rather than broader macroeconomic fluctuations or fundamental changes in cryptocurrency markets. Currently, the long-term Japan-U.S. yield spread has fallen below 3%, and as shown in the chart below, the USD/JPY exchange rate has continued to plunge after the hike, increasing the cost and difficulty of yen carry trades. This suggests a sustained unwind of carry positions over the next 3–5 months, according to our preliminary estimate.

2. Historical data shows little implication for other asset prices beyond Japan-related ones during carry trade reversals

Beyond causing short-term dollar liquidity crunches and volatility in safe-haven assets, carry trade reversals historically do not significantly affect other asset classes besides the yen and Japanese government bonds, nor do they follow clear causal patterns. Since the collapse of Japan’s bubble economy in the 1990s turned the yen into a dominant carry currency, there have been five historical episodes of carry trade reversal. Each time, the unwind led to capital repatriation to Japan, accelerating yen appreciation and rising JGB yields. However, global equity markets responded inconsistently across these episodes.

In 1998, 2002, and 2007, although both Japan and the U.S. entered easing cycles, the BOJ eased less aggressively than the Fed, narrowing the interest rate differential and triggering carry trade reversals. In 2015, markets anticipated the Fed halting rate hikes; in 2022, the BOJ adjusted YCC and raised its 10-year JGB yield target. Although the Japan-U.S. spread did not narrow significantly in these cases, strong market expectations of future narrowing still caused carry trades to retreat. Yet, global stock performance varied widely: equities performed well in 1998 and 2022 but poorly in the other three instances, making it difficult to derive reliable predictive patterns.

3. However, carry trade reversal accelerates the yen’s rate hike cycle and could profoundly impact Japan’s macroeconomy

The yen exchange rate and carry trade reversal create a spiral reinforcement mechanism: central bank rate hikes narrow interest rate differentials, prompting carry trade unwinds; this triggers capital repatriation and yen appreciation; higher returns on yen-denominated assets further reduce incentives for carry trades, reinforcing the cycle. Faced with the yen’s steep depreciation this year, the BOJ decisively raised rates to stabilize its purchasing power—an overt effort to defend the yen that is understandable. However, regarding the long-standing concern that yen appreciation harms Japan’s economy, policymakers have yet to offer convincing solutions.

Here, we address a commonly cited “paradox”: Japan’s foreign trade accounts for a seemingly modest share of GDP, so why is the exchange rate’s impact on exports constantly emphasized? Why is Japan always described as an export-driven economy?

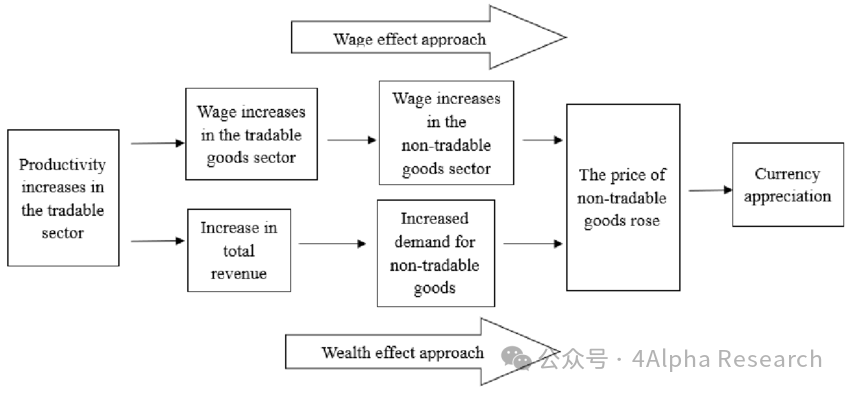

The answer lies in Japan’s export composition—mainly industrial manufactured goods, with automobiles as the dominant category. Auto production, especially internal combustion engine vehicles, supports extensive supply chains, generating vast employment in secondary industries (upstream parts factories) and tertiary sectors (services catering to industrial workers near clusters). Moreover, Japan’s auto manufacturing productivity far exceeds that of non-tradable service sectors. Due to the Balassa-Samuelson effect (shown in the chart below), high wages in the tradable manufacturing sector rapidly spill over into non-tradable sectors, driving overall economic growth—a multiplier effect much greater than what the narrow trade-to-GDP ratio suggests. Additionally, major Japanese automakers like Toyota and Honda build factories overseas and sell locally (e.g., joint ventures in China), revenues from which are not counted in Japan’s GDP, thus underestimating the true structural importance of export-oriented industries to Japan’s economy.

Given persistently weak domestic demand in Japan, a sharply stronger yen is hardly good news for the Japanese auto industry, already locked in fierce global competition with Chinese automakers, or for Japan’s semiconductor sector attempting to regain past glory. Over the past 30 years, Japan’s economy and policymakers have fought desperately against deflation. Even without explicit tightening, merely lagging behind the Fed’s pace of easing has previously triggered severe economic downturns. Now, with the BOJ showing its most hawkish stance in years, Japan’s near-term economic outlook faces renewed uncertainty.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News