Leading indicator of "U.S. recession trade" within the next month: U.S. Weekly Initial Jobless Claims

TechFlow Selected TechFlow Selected

Leading indicator of "U.S. recession trade" within the next month: U.S. Weekly Initial Jobless Claims

Initial U.S. jobless claims will serve as a key leading indicator for recession assessment over the next month.

Author: @Web3Mario

Summary: Last Monday I wrote an article analyzing the market and macroeconomic conditions, and I noticed significant interest from readers on this topic. My background is in science and engineering, and I've been working in Web3 product design, operations, and R&D. Although I'm not formally trained in economics, I’ve long had a strong interest in political economy and have consistently pursued self-study in this area. The reason my perspective might resonate with others could be that it’s more accessible to non-specialists—after all, I include explanations of key concepts that I myself encountered during my learning process, aiming to clarify them for those who share a similar journey. Moving forward, I’ll continue publishing content on related topics to learn and exchange ideas together with you all. Back to the main subject: In the comments on my previous article, I came across a viewpoint suggesting that such analytical pieces are essentially "Monday morning quarterbacking." Indeed, these analyses review past events and offer forward-looking perspectives. While I believe such retrospectives are necessary as part of the learning and improvement process, I also want to provide some genuinely forward-looking insights. That’s why in this article, we’ll discuss a macroeconomic indicator that has suddenly become critical over the past month—one likely to influence short-term risk asset prices in the near term: U.S. weekly initial jobless claims. This is the most direct differential metric for assessing the “U.S. recession trade.”

Brief Review of Current Market Conditions: Unwinding of Yen Carry Trades Fades, U.S. Recession Trade Takes Over

Let’s briefly review current market dynamics. Overall, the unwinding of yen carry trades is largely coming to an end. Market concerns have now shifted from uncertainty around potential Japanese rate hikes to fears of a hard landing in the U.S.—what’s known as the “U.S. recession trade.”

In my previous article, I highlighted that the primary driver behind the massive market volatility on Monday was the Bank of Japan’s (BOJ) aggressive rate hike. I also noted that within the U.S.-Japan alliance, Japan lacks full financial sovereignty and typically plays a supporting role. Thus, this wave of carry trade liquidation effectively concluded following the press conference by BOJ Deputy Governor Shinichi Uchida at 9:30 AM Beijing time on Wednesday, August 7. He provided detailed commentary on the rapid appreciation of the yen, the resulting stock market plunge, and the future direction of monetary policy. His remarks centered on three key points:

-

Recent volatility in equity and foreign exchange markets has had real impacts. If such volatility affects economic outlooks, the path for interest rates may shift accordingly.

-

The BOJ will not raise rates when financial markets are unstable; it remains committed to maintaining accommodative policy for now.

-

If current outlooks materialize, the degree of monetary easing will be adjusted. Interest rate policy is not lagging, and the central bank is closely monitoring how markets affect the economy with urgency.

In effect, this marks a temporary surrender by the BOJ to market forces—clearly signaling it won’t hike rates if doing so would destabilize risk assets, and may even maintain loose policy. This implies that yen carry trades still have room to persist, and with the BOJ effectively guaranteeing against yen volatility, such investment strategies are now implicitly backed by government-level hedging. As a result, immediately after Uchida’s remarks, the USD/JPY pair sharply rebounded, plunging back to 146, while both the Nikkei index and Japanese government bonds saw corresponding rebounds. In short, the recent panic-driven unwind of yen carry trades triggered by fears of BOJ tightening has subsided—at least in the short term—and markets no longer fear further aggressive rate hikes from Japan in the immediate future.

However, looking ahead, Japan’s medium- to long-term rate-hiking trajectory is essentially confirmed. The issue has simply transitioned from a short-term crisis into a longer-term structural challenge. The reasoning is straightforward: Japan’s current inflation rate stands at 2.8%. Meanwhile, yields on short-term Japanese government bonds have only recently begun to rise and remain low overall. This means real interest rates in Japan are still negative, implying that loose monetary conditions will continue to fuel inflationary pressures. With inflation already exceeding the globally accepted 2% target, and wage growth lagging behind price increases, Japan’s economic situation is increasingly strained. Traditional pillars of its economy—such as the automotive industry—are facing strong competition from countries like China, leading to less-than-robust labor market conditions. As inflation rises, so does the “misery index” for Japanese households. Therefore, rate hikes have become virtually the only viable option for the BOJ. Yet, for the sake of global financial stability, domestic pain must be endured a while longer.

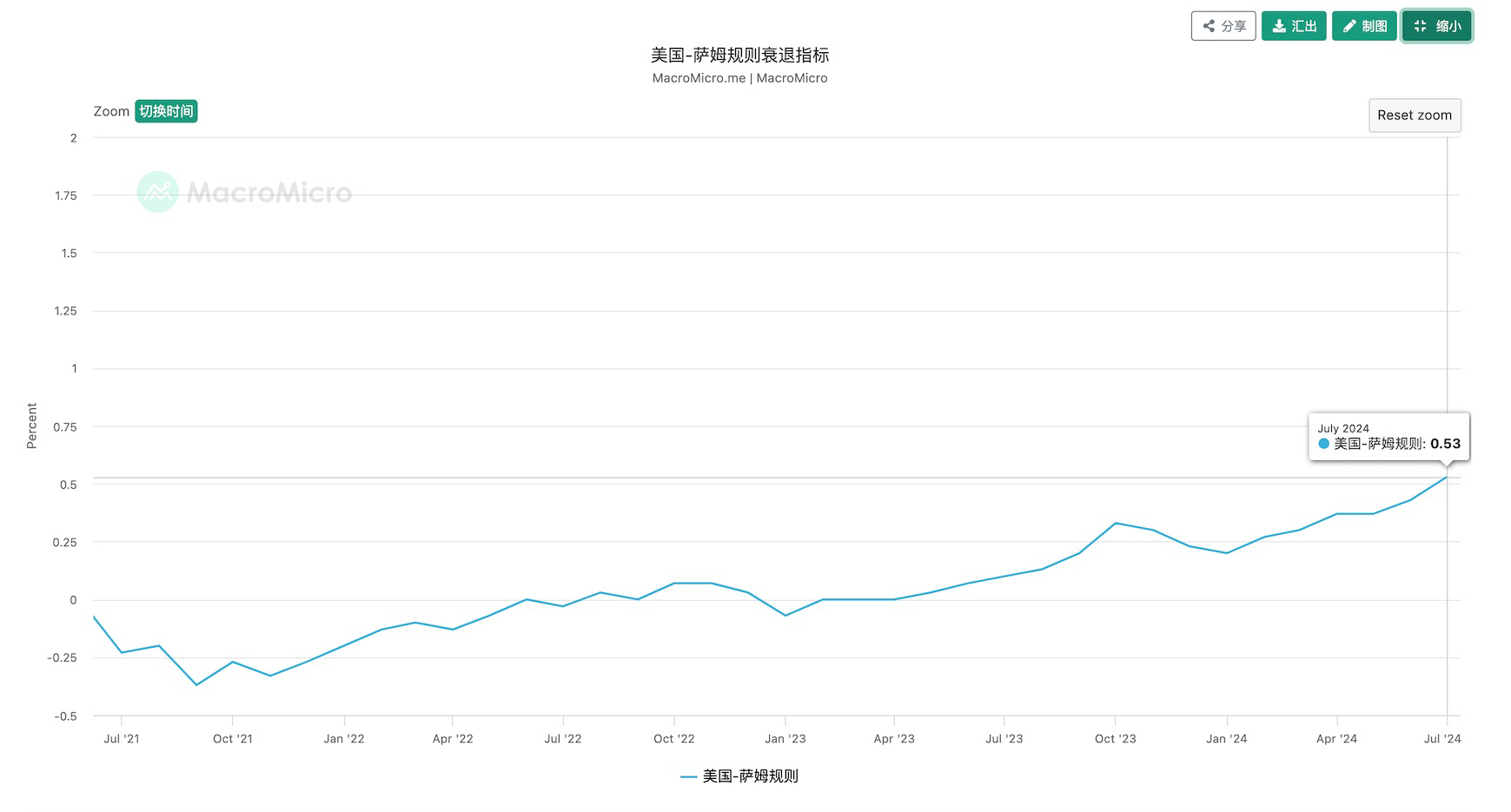

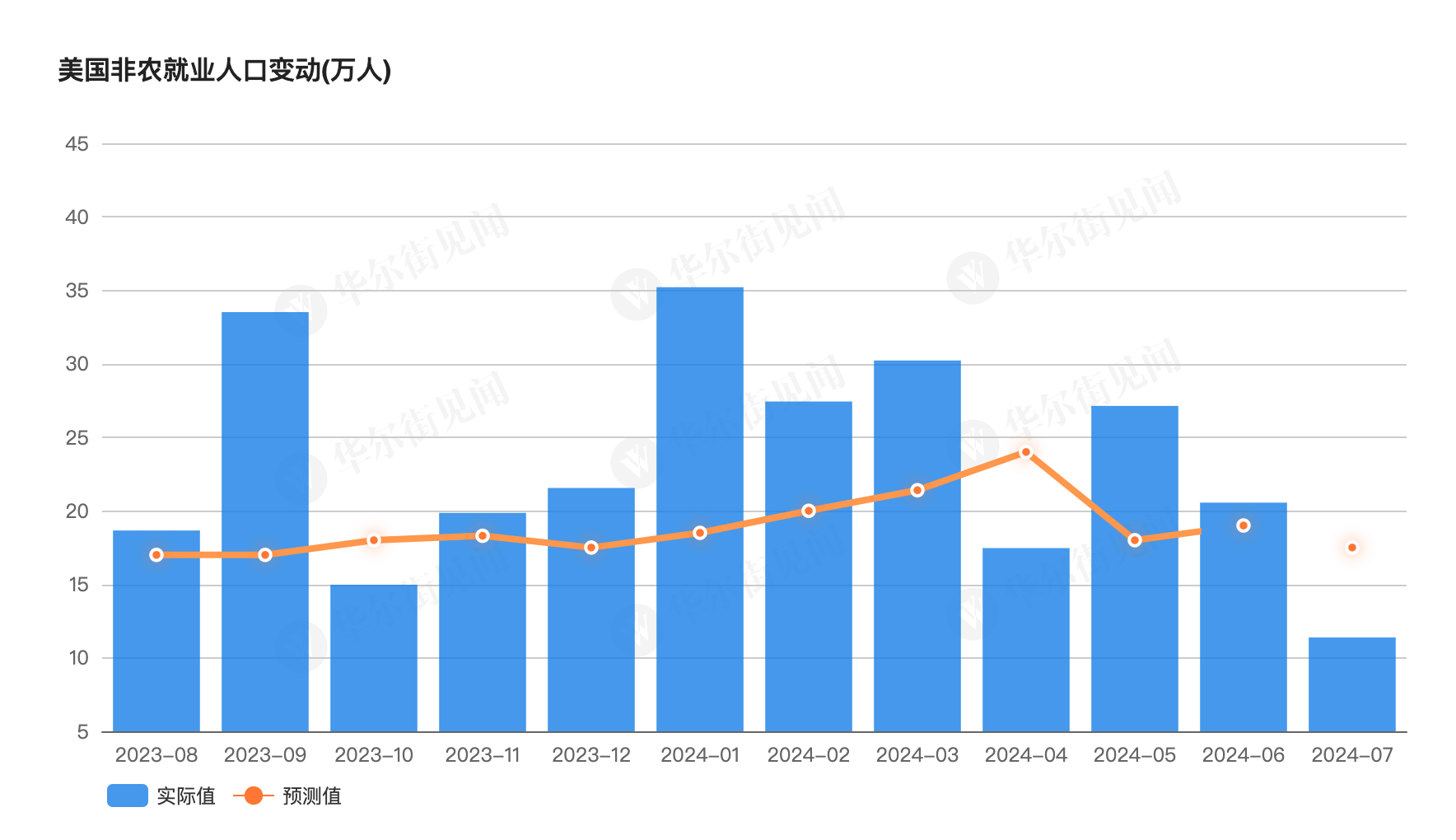

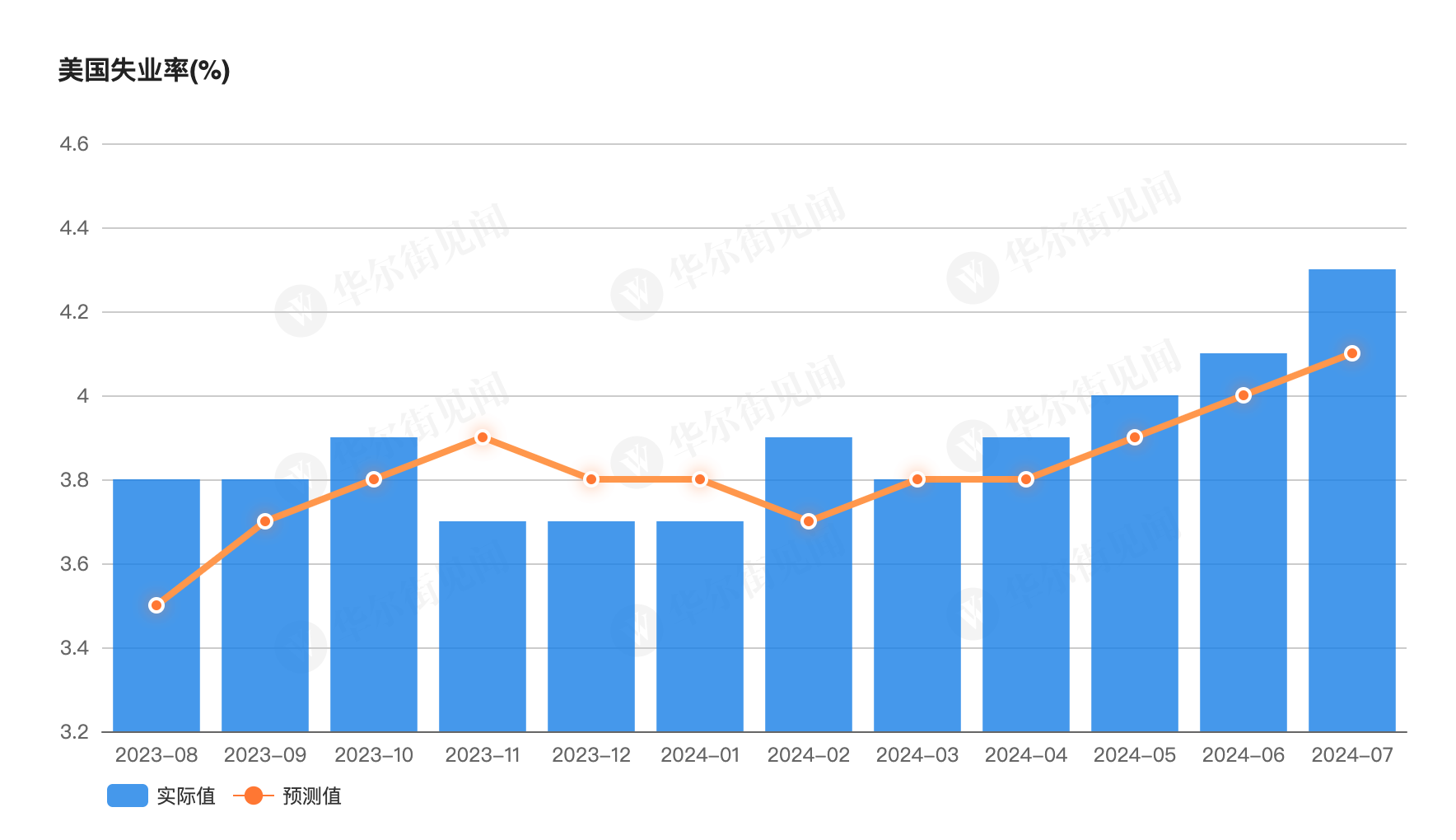

Market focus has now turned to the next major concern: the “U.S. recession trade.” Where does this fear come from? It traces back to two key macroeconomic data releases on August 2: the July Non-Farm Payrolls (NFP) report and the unemployment rate. First, NFP fell significantly short of expectations. Second, the July unemployment rate rose to 4.3%, triggering a widely watched early warning signal for recessions—the Sahm Rule.

Let me briefly explain how the Sahm Rule works. Proposed by Federal Reserve economist Claudia Sahm, it identifies a recession when the three-month moving average of the national unemployment rate exceeds the lowest point of the unemployment rate from the prior 12 months by 0.5 percentage points or more. Historically, every U.S. recession has met this threshold. In July, the Sahm Rule indicator reached exactly 0.53%, officially entering recessionary territory according to this rule—sparking renewed market anxiety.

Of course, once the threshold was hit, debates about the Sahm Rule’s validity quickly emerged. Institutions like Nomura, and even Claudia Sahm herself in an August 6 interview, argued that due to structural changes in the U.S. labor market, the rule may no longer be fully reliable and doesn’t necessarily confirm that the U.S. is already in a recession. Nonetheless, the fact that this debate gained traction underscores how closely the market is watching this indicator. For large institutional investors, risk management often outweighs return chasing. Hence, adopting a more cautious stance amid such uncertainty is entirely rational. This means that in the coming weeks, scrutiny over whether the U.S. is entering a recession will intensify—leading directly to the theme of this article: the leading indicator for the “U.S. recession trade” over the next month—U.S. weekly initial jobless claims.

U.S. Weekly Initial Jobless Claims Will Become a Key Differential Indicator for Assessing Recession Risks in the Coming Month

Why has this indicator suddenly gained importance? It stems from one interpretation of the higher July unemployment rate: some argue that poor employment figures were due to Hurricane Beryl, which lasted from June 28 to July 9, 2024. Damage to infrastructure and other external disruptions caused temporary distortions in the labor market. Thus, weak July data may not reflect underlying trends, making August employment figures critically important—they will determine whether this hurricane hypothesis holds.

However, given the release schedule for U.S. macroeconomic data, the August NFP and unemployment figures won’t be published until the first Friday of September—September 6. During this intervening month, markets need alternative indicators to anticipate the September outcome. Among these, the most crucial is the weekly initial jobless claims data, along with statements from Fed officials.

It’s worth emphasizing this indicator because, historically, it hasn’t been particularly prominent. But in the current environment dominated by recession fears, weekly jobless claims serve as a high-frequency differential proxy for the monthly unemployment rate. Since initial claims represent individuals filing for unemployment benefits for the first time, they offer a timely read on labor market health.

This data is released every Thursday at 8:30 PM Beijing time. A useful rule of thumb: when actual numbers come in below expectations, it signals strength in the labor market, reduces perceived recession risk, and tends to support gains in risk assets. Conversely, if the number exceeds forecasts, it indicates rising layoffs, increases recession probabilities, and typically pressures risk assets downward.

That said, regardless of data outcomes, investment strategies during this phase should remain relatively conservative. Managing leverage is paramount. Wait for clearer trend signals from the market before increasing exposure. After all, wealth creation is a long-term endeavor—not something to rush.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News