Arthur Hayes: How to navigate the collapse of yen carry trades?

TechFlow Selected TechFlow Selected

Arthur Hayes: How to navigate the collapse of yen carry trades?

Yellen might take action because inflation is surpassing the threshold.

Author: Arthur Hayes

Translation: Pzai, Foresight News

The views expressed in this article are solely those of the author and should not constitute the basis for investment decisions, nor should they be construed as a recommendation or advice to engage in investment transactions.

What do you do when markets fall but you need to win an election? If you're a politician, the answer is obvious: your primary goal is securing re-election. So you choose to print money and manipulate prices higher.

Imagine you are Kamala Harris, the Democratic presidential candidate. You're facing off against a formidable Orange Man (Trump). Everything must go smoothly because many problems have arisen since the last election cycle during which you served as vice president. The last thing you need on Election Day is a raging global financial crisis. Harris is a shrewd politician. Given that she was Obama’s protégé, I bet he whispered warnings in her ear about how disastrous it would’ve been if the 2008 global financial crisis had hit right before her doorstep during the election. President Joe Biden is out of the picture now, so let's assume Harris is calling the shots.

In September 2008, near the end of George W. Bush’s second term, Lehman Brothers collapsed, kicking off the global financial crisis. As a Republican president, Bush bore the blame, which partly boosted Obama’s appeal as a Democrat—someone from the other party who wasn’t responsible for the economic downturn. Obama then won the 2008 presidential election. Now back to Harris’s dilemma: how to respond to a potential global financial crisis triggered by Japanese firms unwinding massive yen carry trades. She could let it happen, allowing the free market to destroy over-leveraged corporations and inflict real pain on wealthy baby boomer financial asset holders. Or, she could instruct U.S. Treasury Secretary Janet Yellen to print money and fix it.

Like any politician, regardless of party or economic belief, Harris would instruct Yellen to use every monetary tool at her disposal to prevent a financial crisis. Of course, this means the printing presses will hum in one form or another. Harris wouldn’t want Yellen to wait—she’d demand immediate, forceful action. Therefore, if you agree with me that the unwind of these yen carry trades could collapse the entire global financial system, then you must also believe Yellen will act no later than next Monday (August 12) at the opening of Asian trading.

To help illustrate the scale and severity of the potential impact from Japanese corporate carry trade unwinds, I’ll first introduce an excellent research piece published by Deutsche Bank in November 2023. Then, I’ll walk through how I would structure a bailout plan if I were put in charge of the U.S. Treasury.

Widow Maker

What is a carry trade? A carry trade involves borrowing in a low-interest-rate currency and using it to buy financial assets denominated in a higher-yielding or appreciating currency. When repayment comes due, if the borrowed currency has appreciated relative to the asset’s currency, you lose money. If it depreciates, you profit. Some investors hedge their currency risk; others don’t. In this case, because the Bank of Japan can print unlimited yen, Japanese firms see no need to hedge their yen borrowings.

“Japanese firms” refers collectively to the Bank of Japan, corporations, households, pension funds, and insurers. Some entities are public, some private, but all share a common mission to improve Japan’s situation—at least, that’s the intention. On November 13, 2023, Deutsche Bank published an excellent report titled “The World’s Biggest Carry Trade.” The authors posed a rhetorical question: “Why hasn’t the yen carry trade blown up and dragged down the Japanese economy?” Today’s situation differs significantly from late last year.

The prevailing narrative is that Japan is drowning in debt. Hedge fund after hedge fund has bet on Japan’s imminent collapse—and lost. This is the infamous “Widow Maker” trade. Many macro investors have been too bearish on Japan because they fail to understand Japan’s integrated public-private balance sheet. For Western investors who prioritize individual rights, this is an easy psychological trap. But in Japan, the collective comes first. Thus, certain ostensibly private actors are effectively government proxies.

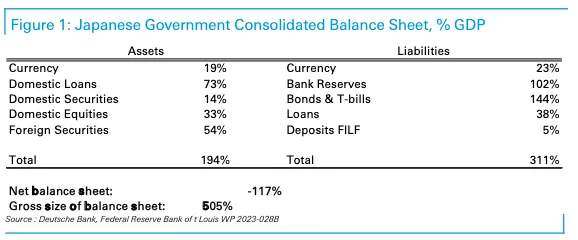

Let’s start with liabilities—the funding sources for these carry trades. This is where yen are borrowed, carrying interest costs. Two major items are bank reserves and bonds/treasury bills.

Bank Reserves—This is money banks hold at the Bank of Japan. The amount is large because the BOJ creates bank reserves when purchasing bonds. Recall that the BOJ owns nearly half of the Japanese government bond market. Thus, bank reserves are enormous—equivalent to 102% of GDP. These reserves cost 0.25%, paid by the BOJ to banks. By contrast, the Fed pays 5.4% on excess bank reserves. This funding cost is effectively zero.

Bonds and Treasury Bills—These are Japanese government bonds issued by the state. Due to BOJ market manipulation, JGB yields remain at rock-bottom levels. At time of writing, the 10-year JGB yield stands at 0.77%. This financing cost is negligible.

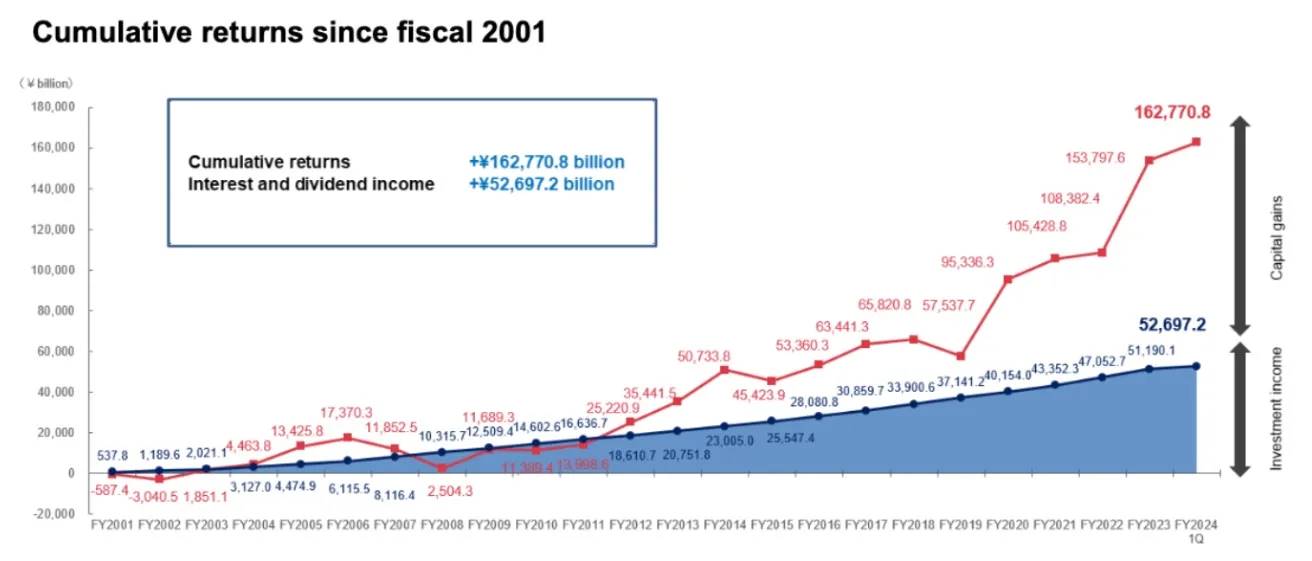

On the asset side, the broadest category is foreign securities—financial assets held abroad by both public and private sectors. The Government Pension Investment Fund (GPIF) is a major private holder of foreign assets. With $1.14 trillion in assets, it is among the world’s largest pension funds. It holds foreign equities, bonds, and real estate. Domestic loans, securities, and stocks also perform well when the BOJ controls bond prices. Finally, yen depreciation—resulting from massive yen-denominated debt—boosts domestic stock and real estate markets.

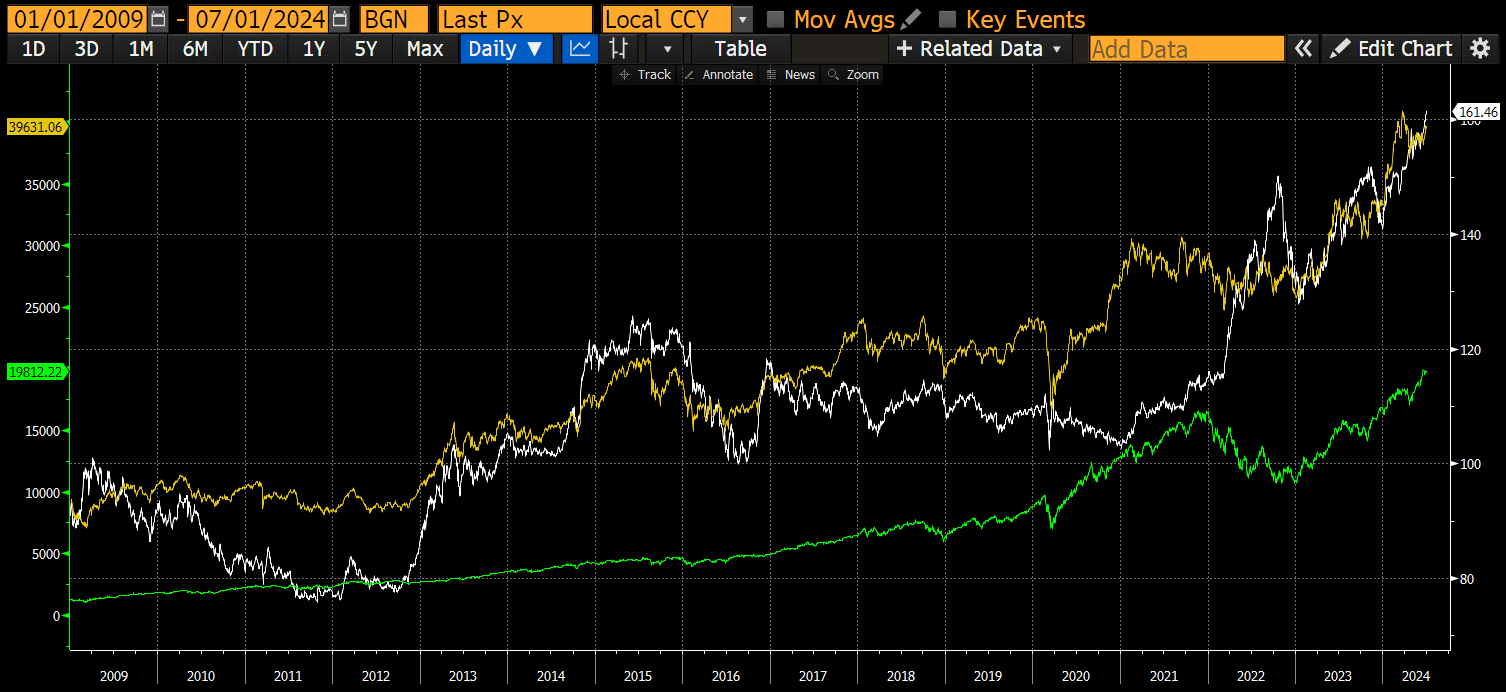

USD/JPY (white) rises, meaning the yen weakens against the dollar. Nasdaq 100 Index (green) and Nikkei 225 Index (yellow) rise in tandem.

Overall, Japanese firms fund themselves via financial repression enacted by the BOJ and earn fat returns thanks to a weak yen. That’s why the BOJ can maintain the world’s most accommodative monetary policy amid rising global inflation—it’s pure profit!

GPIF has performed exceptionally well over the past decade. A key reason: the yen has depreciated sharply. As the yen falls, returns on foreign assets soar.

Without stellar returns from its foreign equity and bond portfolios, GPIF might have posted a loss last quarter. Domestic bonds declined because the BOJ exited YCC (yield curve control via secondary market JGB purchases), pushing JGB yields up and prices down. Yet the yen continued weakening, as the rate differential between the BOJ and the Fed remains wider than SBF’s eyes when he discovered Emsam (an antidepressant he frequently used).

This trade is massive. Japan’s GDP is around $4 trillion, yet total exposure reaches 505%, with value-at-risk exceeding $240 billion. As Cardi B said in WAP: “I want you to pull up on my block like a Mack truck.” She was definitely rapping about the Japanese men orchestrating this spectacle in the “Land of the Setting Sun.”

Clearly, this trade has worked—but the yen has become too weak. Earlier in July, USD/JPY reached 162, which became unbearable as domestic inflation raged then and now. The BOJ doesn’t want to kill the trade abruptly but hopes to exit gradually… they always say that. Ueda took over as BOJ governor in April 2023 from Kuroda, the mastermind behind this massive trade. Kuroda wisely escaped. Ueda is the only qualified candidate dumb enough to try unwinding this trade and potentially commit career suicide. The market knows Ueda wants the BOJ to escape the carry trade, so the question has always been about the pace of normalization.

Unwinding

What would a disorderly unwind look like? What happens to the various assets held by Japanese firms? How much would the yen appreciate? To unwind this trade, the BOJ must raise rates by halting JGB purchases and eventually selling them back into the market.

On the liability side, what happens?

Without the BOJ’s constant suppression of JGB yields, they would rise with market demand, at least matching inflation. In June, Japan’s CPI rose 2.8% year-on-year. If JGB yields rose to 2.8%—above any point on the yield curve—debt servicing costs across all maturities would surge. Interest expenses on bonds and treasury bills would skyrocket. The BOJ would also need to raise interest on bank reserves to prevent capital flight. Again, given the conceptual framework, this cost would shift from near-zero to massive.

In short, if rates are allowed to rise to market-clearing levels, the BOJ must pay billions annually in interest to fund its positions. Without any asset sale revenues on paper, the BOJ would have to print massive yen to maintain liquidity on its liabilities. Doing so worsens the situation: inflation rises, and the yen depreciates further. Hence, they must sell assets.

On the asset side, what happens?

The BOJ’s biggest headache is how to sell its vast holdings of JGBs. Over the past two decades, the BOJ destroyed the JGB market through various QE and YCC programs. For all intents and purposes, the market no longer exists. The BOJ must compel another segment of Japanese firms to step in and absorb JGBs at prices that won’t bankrupt the central bank. When in doubt, turn to banks. After the 1989 real estate and stock bubble burst, Japanese commercial banks were forced to deleverage. Since then, bank lending has remained stagnant. The BOJ began printing because companies weren’t borrowing. Given bank health today, it’s time to reload trillions of yen worth of JGBs onto their balance sheets.

While the BOJ can make banks buy bonds, the banks need funding from elsewhere. As JGB yields rise, profit-seeking Japanese corporations and banks holding trillions in foreign assets will sell those assets, repatriate funds, and deposit them in banks. Banks and these firms will then purchase JGBs en masse. Capital inflows strengthen the yen, while JGB yields won’t rise to levels that destroy the BOJ’s business as it reduces holdings.

Japanese firms sell foreign stocks and bonds to repatriate capital, suffering losses primarily through falling asset prices. Given the sheer size of this carry trade, Japanese firms have become marginal price setters in global equities and bonds. This is especially true for any security listed in the U.S., as American markets are the preferred destination for yen-funded capital. Since the yen is freely convertible, many TradFi trading books reflect Japanese firm activity.

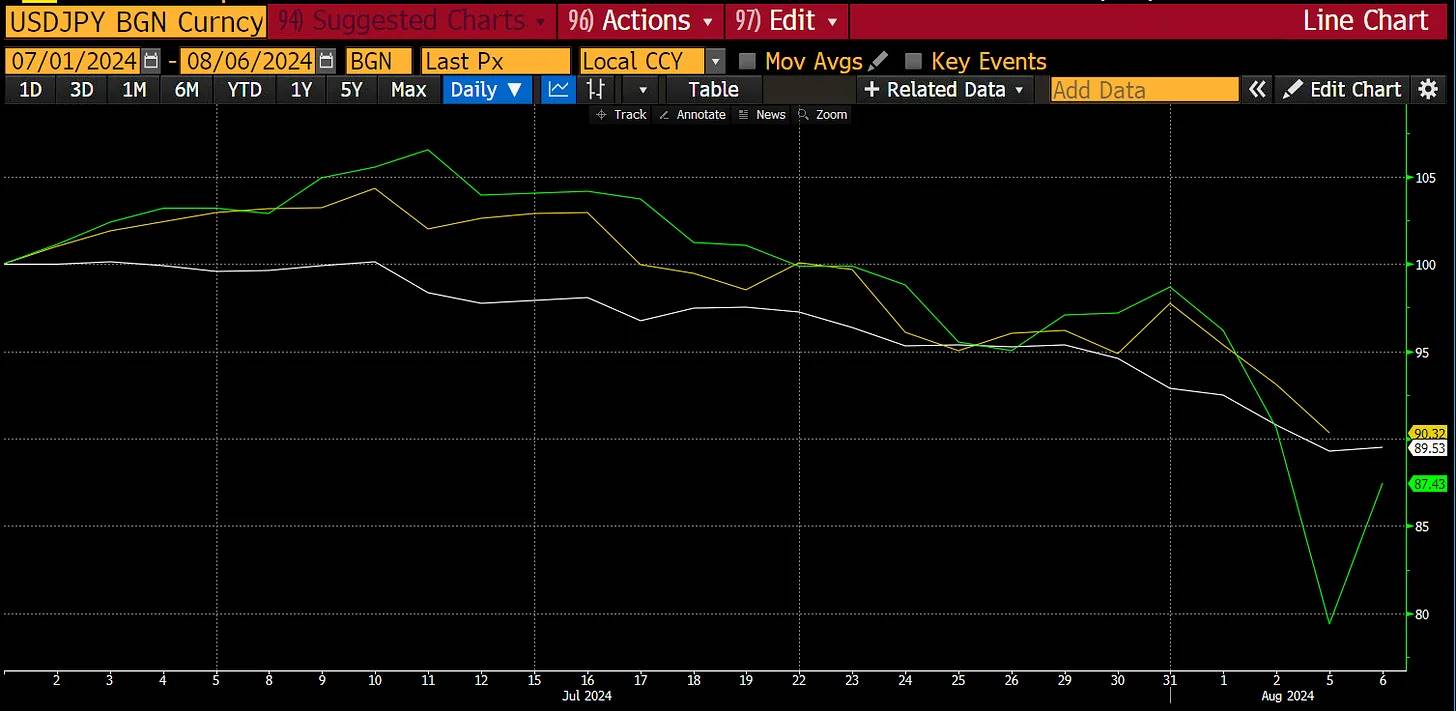

As the yen weakens, more global investors are encouraged to borrow yen and buy U.S. stocks and bonds. Everyone rushes to cover simultaneously when the yen strengthens, given their high leverage. Earlier I showed you a chart of what happens when the yen weakens. What if it strengthens slightly? Remember that early chart showing USD/JPY rising from 90 to 160 over 15 years? In just four trading days, it dropped from 160 to 142—that’s what’s happening now:

USD/JPY appreciated ~10%, Nasdaq 100 (white) fell ~10%, Nikkei 225 (green) dropped ~13%. Yen appreciation roughly correlates 1:1 with equity index declines. Extrapolating further, if USD/JPY hits 100—a 38% move—Nasdaq would fall to ~12,600, Nikkei to ~25,365.

A USD/JPY move to 100 is possible. A 1% reduction in Japanese firms’ carry trade exposure equals ~$24 billion nominally—marginal but substantial. Different participants within Japanese firms have varying priorities. We saw this with Norinchukin, Japan’s fifth-largest commercial bank. Part of their carry trade blew up, forcing them to begin unwinding. They’re selling foreign bond positions and hedging with forward USD/JPY FX contracts. This news broke months ago. Insurers and pension funds will face pressure to disclose unrealized losses and exit trades. Alongside them, all followers will be swiftly liquidated by brokers as currency and stock volatility spikes. Remember: everyone is unwinding the same trade simultaneously. Neither we nor the elites running global monetary policy know the full size of yen carry trade positions lurking in the financial system. This opacity means rapid overshoot corrections in the opposite direction as the market reveals this highly leveraged segment.

Spooked

I believe China and Japan saved America from deeper recession since the 2008 global financial crisis. China launched one of the largest fiscal stimulus programs in human history—infrastructure projects fueled by debt. China needed to import goods and raw materials globally to complete these projects. Japan printed massive yen via the BOJ to expand its carry trade. Japanese firms used these yen to buy U.S. stocks and bonds.

The U.S. government collected huge capital gains tax revenue due to the stock market rally. From January 2009 to early July 2024, the Nasdaq 100 rose 16-fold, the S&P 500 six-fold. Capital gains tax rates range from roughly 20% to 40%.

Despite record-high capital gains taxes, the U.S. government still runs deficits. To cover them, the Treasury must issue debt. Japanese firms are among the largest marginal buyers of Treasuries... at least until the yen started strengthening. The Japanese helped fiscally irresponsible politicians afford U.S. debt—Republicans through tax cuts, Democrats through welfare checks—all to buy votes.

Total U.S. outstanding debt (yellow) rises and shifts right. Yet the 10-year Treasury yield (white) fluctuates within a range, barely linked to growing debt.

My point: the U.S. economic structure depends on Japanese firms—and those copying them—continuing this carry trade. If this trade unravels, U.S. fiscal stability will be torn apart.

Bailout Plan

I speculate that coordinated intervention will rescue Japanese firms' carry trade positions because I believe Harris won’t let her electoral chances diminish due to some foreigners deciding to exit a trade she likely doesn’t even understand. Her voters certainly don’t know what’s happening, nor do they care. Their stock portfolios either rise or they don’t. If not, they won’t show up to vote Democratic on Election Day. Voter turnout will decide whether the clown emperor is Trump or Harris.

Japanese firms must unwind, but not by selling certain assets openly. This implies a U.S. government agency must print money and lend it to a member of the Japanese corporate sector. Allow me to reintroduce myself: my name is Central Bank Swap (CSWAP).

If I were “bad girl” Yellen, here’s how I’d conduct the rescue. On Sunday night, August 11, I’d release a statement (imagining myself as Yellen): “The U.S. Treasury, the Federal Reserve, and our counterparts in Japan have engaged in extensive discussions regarding the turbulent market conditions over the past week. During these conversations, I reaffirmed our support for utilizing the dollar-yen central bank swap facility.”

That’s it. To the public, this seems entirely harmless. It’s not the Fed capitulating with radical rate cuts or restarting QE. Because people know such measures would accelerate already uncomfortably high inflation. If inflation rages on Election Day and is easily traced back to the Fed, Harris loses.

Most American voters don’t know what CSWAP is, why it was created, or how it enables unlimited money printing. Yet, due to how it’s used, the market will correctly interpret it as a stealth bailout.

-

The BOJ borrows billions in dollars from the Fed, posting yen as collateral. These swaps can be rolled over indefinitely as long as the BOJ wishes.

-

The BOJ privately speaks with major corporations and banks, telling them Japan is ready to exchange dollars for U.S. stocks and U.S. Treasuries.

This transfers ownership of foreign assets from Japanese firms and banks to the BOJ. These private entities, now holding dollars, repatriate capital by selling dollars and buying yen. They then purchase JGBs from the BOJ at current high prices / low yields. The result: CSWAP balances explode, and this dollar amount equals the Fed’s money printing.

I drew an ugly box-and-arrow diagram to help visualize the flow. What matters is the net effect.

Federal Reserve—They increase dollar supply, or equivalently, exchange previously accumulated yen from carry trade growth.

CSWAP—The Fed owes the BOJ dollars. The BOJ owes the Fed yen.

BOJ—They now hold more U.S. stocks and bonds, whose prices rise as CSWAP balances grow and more dollars enter the system.

Japanese Banks—They now hold more JGBs.

As shown, U.S. equity and bond markets remain unaffected; Japanese firms’ total carry trade exposure stays unchanged. The yen strengthens against the dollar, and crucially, U.S. stocks and bonds rise due to Fed dollar printing. An added benefit: Japanese banks can now use newly acquired JGBs as collateral to issue unlimited yen loans. This trade revitalizes both U.S. and Japanese financial systems.

Timeline

I’m confident the Japanese corporate carry trade will unwind. The question is when the Fed and Treasury will print money to neutralize its impact on Main Street.

If U.S. stocks plunge sharply on Friday (August 9), with both the S&P 500 and Nasdaq 100 falling 20% from their recent July highs, some action may emerge over the weekend. For the S&P 500, that level is 4533; for the Nasdaq 100, 16,540. I also expect the 2-year Treasury yield to reach around 3.80% or lower—the same level seen during the March 2023 regional banking crisis, resolved via the Bank Term Funding Program.

If the yen weakens again, the crisis ends temporarily. Unwinding continues, albeit slower. I believe markets will flare up again between September and November as USD/JPY moves back toward 100. There will definitely be a response then—with only weeks or days left before the U.S. presidential election.

Trading crypto is very difficult right now. Two opposing forces shape my positioning.

-

Positive Liquidity Force: After a quarter of net restrictive policy, the U.S. Treasury will inject net dollar liquidity by issuing T-bills and possibly draining the Treasury General Account. This policy shift was outlined in the recent Quarterly Refunding Announcement. Briefly: from now through year-end, “bad girl” Yellen will inject $301 billion to $1.05 trillion. I’ll explain further in a follow-up if needed.

-

Negative Liquidity Force: This is yen appreciation. As yen debt becomes more expensive to repay, unwinding triggers coordinated global sell-offs across all financial assets.

Which force dominates depends on the speed of carry trade unwinding—which we cannot predict. The only observable signal is Bitcoin’s correlation with USD/JPY. If Bitcoin trades convexly—rising whether USD/JPY surges or plunges—I’ll know the market expects a rescue if yen strength overwhelms sufficient Treasury liquidity. That’s convex Bitcoin. If Bitcoin falls with yen strength and rises with yen weakness, it trades in sync with TradFi markets. That’s correlated Bitcoin.

If the setup is convex Bitcoin, I’ll aggressively accumulate near local bottoms. If it’s correlated Bitcoin, I’ll stay sidelined until the market finally surrenders. The biggest assumption is that the BOJ won’t reverse course—cut deposit rates back to 0% and resume unlimited JGB purchases. If the BOJ sticks to its plan from the last meeting, carry trade unwinding continues.

This is all the normative work I can do for now. As always, these trading days and months will determine your gains in this bull run. If you must use leverage, use it wisely and constantly monitor your positions. When leveraged, you better watch your Bitcoin—or shitcoin—closely. Otherwise, you’ll get liquidated.

That’s it. Now I’m off to enjoy the final stretch of my August vacation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News