In-depth Analysis of the 8.5% Market Plunge: The Bank of Japan's Rate Hike and the Exit of "Mrs. Watanabes"

TechFlow Selected TechFlow Selected

In-depth Analysis of the 8.5% Market Plunge: The Bank of Japan's Rate Hike and the Exit of "Mrs. Watanabes"

In the U.S.-Japan alliance, the Bank of Japan plays a supporting role, while the U.S. dollar is the one that truly determines future trends.

Author: @Web3Mario

Summary: This week I've been studying Telegram Bot APIs, and the core framework for TON contracts is mostly complete—initially a small cause for celebration. However, Monday's sharp plunge across the entire crypto market cast a shadow over my mood. While I anticipated this to some extent, I didn't expect it to come so quickly and violently. Therefore, I’ve compiled my thoughts to share with everyone, hoping you can stay calm and avoid letting panic influence your investment decisions. In short, the recent significant pullback in risk assets led by U.S. tech stocks is primarily due to the Bank of Japan’s aggressive rate hike, which has disrupted or increased risks for many JPY carry trade positions. Specifically, three risks are involved: exchange rate volatility, interest rate reversal, and liquidity risk. In response, "Mrs. Watanabes" are now unwinding their positions to repay JPY-denominated debts and reduce exposure.

Abenomics and Japan’s prolonged low-interest-rate environment made the yen a key global funding and carry asset

Those with basic economics knowledge are likely familiar with the narrative of Japan’s “Lost Two Decades.” After the collapse of Japan’s bubble economy in the early 1990s, its economy fell into long-term stagnation—commonly known as the “Lost Decades.” During this period, economic growth slowed, corporate and consumer investment sentiment remained weak, and persistent deflation took hold. To combat this downturn, the Bank of Japan began implementing low-interest-rate policies from the late 1990s, cutting benchmark rates to near zero, aiming to stimulate economic activity by lowering borrowing costs. As traditional monetary tools lost effectiveness,

it was against this backdrop that former Japanese Prime Minister Shinzo Abe, upon his re-election in 2012, introduced a series of economic reforms collectively known as “Abenomics.” The core goals were to stimulate growth, end prolonged deflation, and address structural issues in Japan’s economy. Abenomics rested on a “three-arrow” framework. Here, I’ll only briefly discuss the first arrow—bold monetary policy—which included two main components: First, the Bank of Japan launched large-scale quantitative easing (QE), injecting massive liquidity into markets by purchasing government bonds and other assets to suppress interest rates and boost liquidity. Second, in 2016, the BOJ formally introduced negative interest rates, aiming to further lower interbank lending costs and incentivize banks to channel funds into the real economy, thereby stimulating consumption and investment and lifting inflation expectations. A quick note on “negative interest rates”: this does not mean lenders pay borrowers interest; rather, it refers to real interest rates being negative—i.e., nominal rates below domestic inflation.

Against this backdrop, a popular arbitrage strategy emerged—the JPY carry trade—and traders engaging in it earned an amusing nickname: “Mrs. Watanabe.” The JPY carry trade

refers to an investment strategy based on interest rate differentials. Its basic principle involves borrowing in a low-interest-rate currency (like the yen) and investing the proceeds in higher-yielding currencies or assets to capture the interest spread. The mechanics work as follows:

l Borrow Yen: Given Japan’s ultra-low interest rates (sometimes near zero), investors can borrow JPY at very low cost.

l Convert to High-Yield Currency: Exchange the borrowed yen into a higher-interest-rate currency, such as the Australian or New Zealand dollar.

l Invest in High-Yield Assets: Deploy the funds into bonds, deposits, or other instruments in the target currency’s country to earn higher interest income.

l Capture Interest Spread: Profit comes from the difference between the low cost of borrowing (in JPY) and the high return on investment (in foreign assets).

This type of carry trade also exists widely in DeFi. A typical example is LSD-ETH yield arbitrage: depositing stETH as collateral on platforms like Compound to borrow ETH, then swapping it back to stETH. If the borrowing rate for ETH remains below the stETH yield, a risk-free profit opportunity emerges. The same applies in the JPY carry trade market. Typically, there are two main paths: First, using USD-denominated assets as collateral to borrow JPY and directly buying high-dividend Japanese conglomerate stocks—this was part of Warren Buffett’s core portfolio in recent years. Second, borrowing JPY, selling it for USD, and then investing in high-yield financial instruments such as U.S. equities or Treasuries. This resembles the recursive lending strategies seen in DeFi.

This trade became especially popular after the U.S. officially entered a hiking cycle in 2022. As the Fed raised rates, other major economies followed suit to stabilize exchange rates and prevent capital outflows—except Japan, which maintained its low-rate policy. This made the yen the primary low-cost funding source during a tightening cycle. Some might argue RMB rates are also low, but given geopolitical dynamics and China’s financial sovereignty stance, the RMB isn’t suitable as a carry funding currency. Thus, it’s fair to say that the continued strength of U.S. “tech seven sisters” during this cycle owes much to yen-funded leverage.

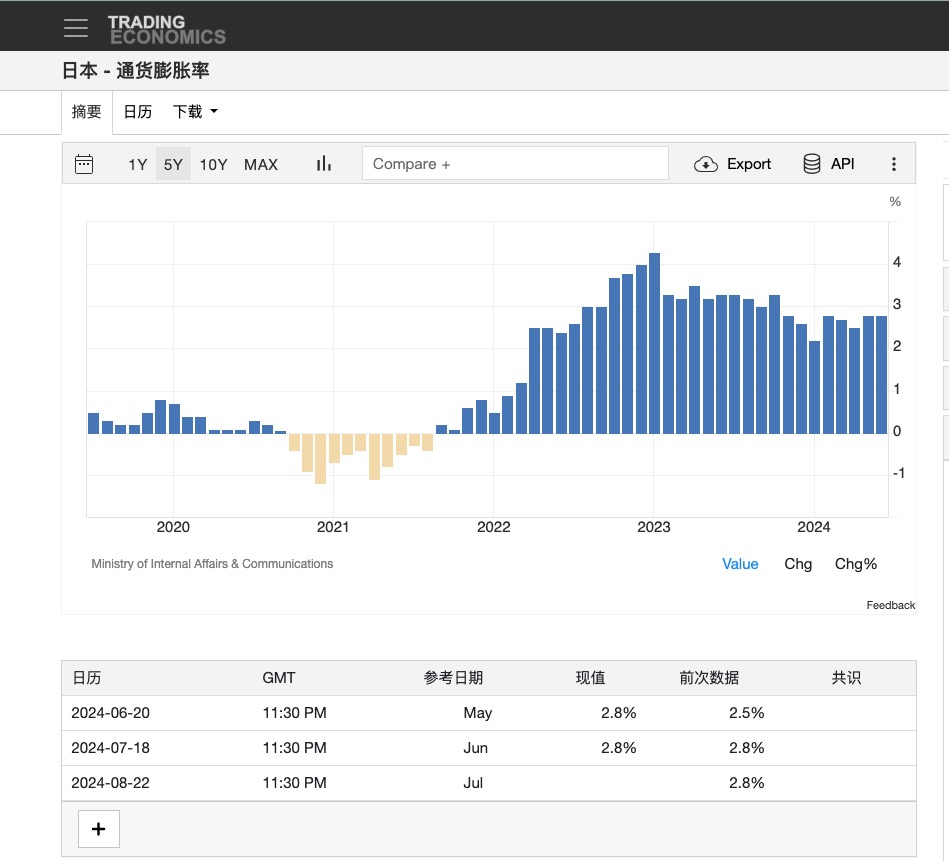

The impact on Japan has been mixed. On the positive side, thanks to the “Buffett carry path,” Japanese equities enjoyed sustained growth, creating a rare “wealth effect” domestically. Economic vitality often hinges on such wealth effects—when people easily accumulate wealth and remain optimistic about future returns, they’re more willing to leverage for investment or consumption, fueling economic momentum. With foreign capital driving the “Japan premium” rally, this wealth effect helped shift Japan from prolonged deflation to mild inflation—essentially fulfilling Abenomics’ original vision.

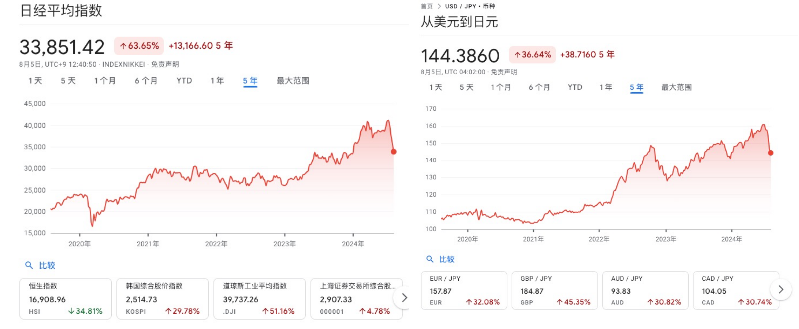

On the downside, the second carry path—converting vast amounts of JPY into USD to buy dollar-denominated assets—led to a prolonged depreciation of the yen. From 2021 to 2024, USD/JPY rose from a low of 103 to as high as 160, marking over 60% yen depreciation. However, since exchange rate fluctuations don’t strongly affect domestic citizens' perceived purchasing power, inflation in Japan still rose steadily despite the weakening yen.

The showdown between the Bank of Japan’s forward guidance and speculative markets has culminated—yen completes V-shaped reversal

After over two years of continuous trend, the tide finally turned recently—naturally as the dollar’s hiking cycle neared its end. In early 2024, newly appointed BOJ Governor Kazuo Ueda shifted course from predecessor Haruhiko Kuroda’s negative rate policy, beginning to signal potential rate hikes. But the market didn’t believe him and instead doubled down against the central bank. The result? The yen depreciated past 160 in the first half of 2024. One interpretation attributes this to speculators doubting the sustainability of Japan’s inflation, expecting a return to deflation once the U.S. enters a rate-cutting cycle. Another explanation points to hedging demands within complex JPY carry trade chains centered around NVIDIA. Japanese chipmakers (e.g., Sony, Tokyo Electron), Taiwan Semiconductor, and NVIDIA have shown strong stock correlation due to industrial and geopolitical linkages. For years, buying Japanese semiconductor stocks was a key way to capture alpha in the AI sector. But in 2024, U.S. markets showed clear “risk concentration”—capital fleeing to safety, particularly into NVIDIA. As Japanese chip stocks decoupled from NVIDIA, investors sought hedges: selling JPY to buy NVIDIA shares became an attractive move. This view comes from Fu Peng, an economist I highly respect—readers interested can refer to his official account for deeper analysis.

Regardless of the exact reason, this standoff ended last Wednesday when the BOJ unexpectedly raised rates by 15 basis points—far exceeding market expectations. The reversal was immediate: USD/JPY dropped sharply from 160 to 143 at the time of writing. The JPY carry trade era effectively ended, triggering mass unwinding of leveraged positions. Traders began selling dollar-denominated risk assets to convert back into yen and repay debts.

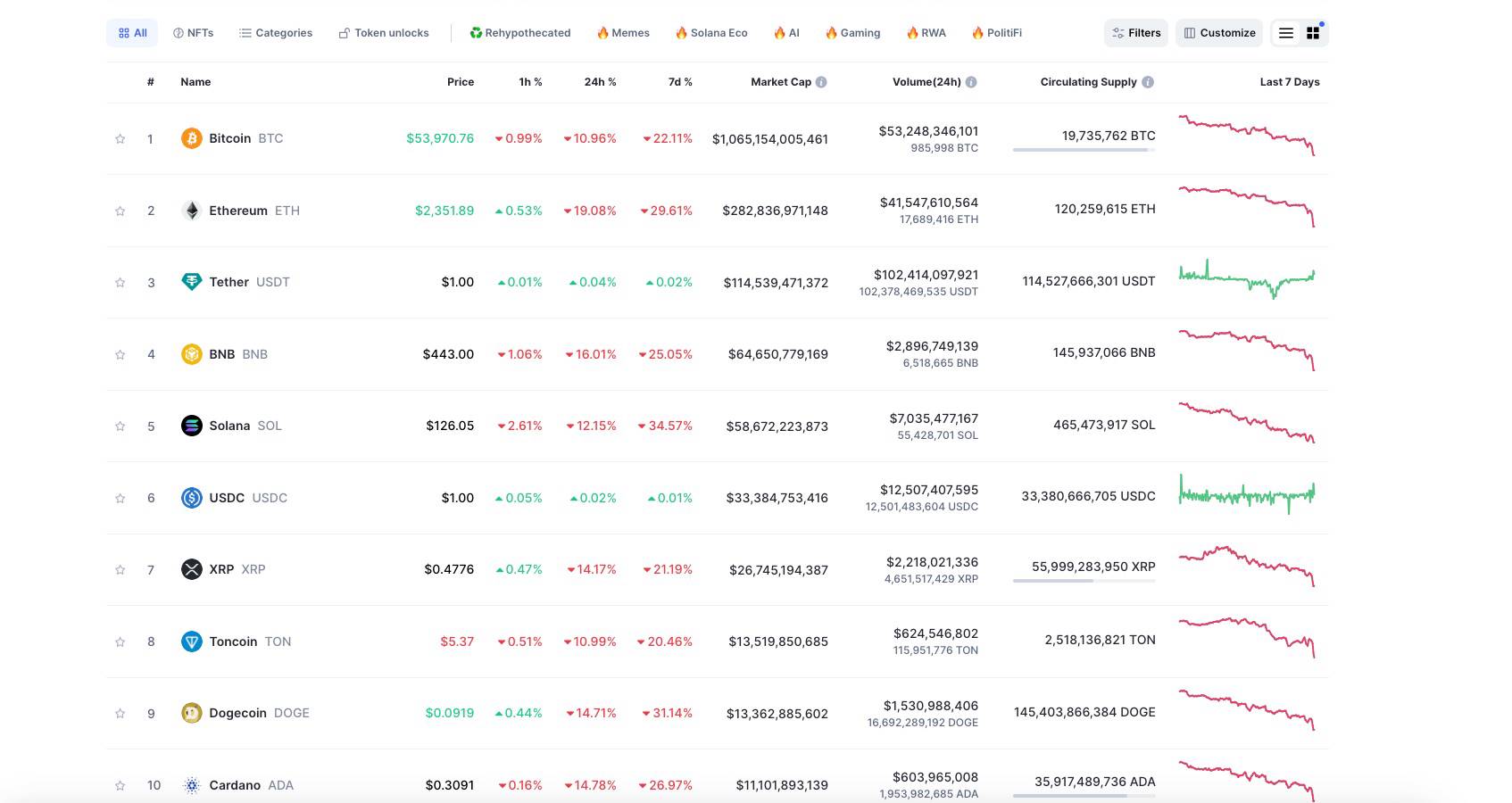

Thus, after the weekend allowed markets to digest the news, the unwind reached its peak—this is the root cause of the August 5 crypto crash. Supporting evidence: income-generating assets declined far more than zero-yield assets like Bitcoin. Ethereum, in particular, saw outsized losses, precisely because it was a core target of carry trades.

Within the U.S.-Japan alliance, the BOJ plays a supporting role—the dollar ultimately dictates future trends

Let me briefly outline my outlook. I urge readers not to be frightened by this correction. Although the scale of JPY carry trades is substantial, within the U.S.-Japan alliance, Japan remains in a supporting role. The recent rate hike was essentially coordinated with U.S. monetary policy. We know the U.S. has avoided recession so far largely due to stock market strength. Despite widespread distress among SMEs, the “tech seven sisters”—especially NVIDIA—have generated enough wealth effect to keep financial-sector-driven GDP from contracting. If the U.S. cuts rates prematurely, it could overstimulate risk markets and reignite inflation—an outcome policymakers want to avoid. Yet, given current economic conditions, the U.S. eventually must cut rates. Therefore, the Fed needs a credible justification—and that justification is a meaningful pullback in U.S. equities. From this perspective, the BOJ’s move becomes understandable: it’s helping set the stage for the Fed’s eventual pivot. Once the U.S. officially enters its easing cycle and liquidity loosens again, crypto assets will inevitably rebound. So stay patient, and remain optimistic. That said, for those using high leverage, reducing exposure may be an unavoidable necessity.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News