The Evolution of Crypto Venture Capital (Part 1): Rebuilding a New World

TechFlow Selected TechFlow Selected

The Evolution of Crypto Venture Capital (Part 1): Rebuilding a New World

Go back to the past, where choices determine fate.

Author: Wenser, Odaily

In December 2017, when the cryptocurrency market cap hit $500 billion, Ethereum co-founder Vitalik Buterin issued a series of critical questions about the industry—raising concerns about banking services, censorship-resistant commerce, practical-use DApps, real interest rates, inflation resistance, and payment channels. Ultimately, he concluded that although progress had been made in these areas, it still fell far short of expectations relative to the market's valuation.

Today, after briefly surpassing $3 trillion in November 2021, the crypto market cap has settled around $2.4 trillion. Mass adoption remains distant. Venture capital tokens are criticized as "high FDV, low circulation" bloodsucking machines. Different sectors such as L1, DeFi, GameFi, NFTs, SocialFi, DAOs, infrastructure, and L2 have each taken turns in the spotlight before fading away. Meme coins, which originated back in 2013, returned to center stage in 2023 and continued to shine brightly in 2024 following the approvals of Bitcoin and Ethereum spot ETFs.

Looking back, the cryptocurrency industry began with Bitcoin and gradually grew into a sprawling tree with many branches. Ahead of this towering tree may lie another winter or perhaps the next warm spring. On this still modest yet fertile decentralized land, new ideals and wealth miracles continue to await us.

In this series, Odaily Planet Daily will briefly review and analyze past venture investment cycles in the crypto industry. While inevitably incomplete, we hope this provides useful supplementary perspectives for our readers.

(Note: This is the first part, covering pre-2022—the eras of Ethereum, exchanges, the public chain boom, and the "three summers" of DeFi/GameFi/NFT. The second part will cover the most recent cycle and attempt to abstract trends and methodologies across multiple investment cycles.)

Bitcoin Innovation Program: It All Begins With Ethereum

After the Bitcoin pioneering era from 2013 to 2015, Bitcoin increasingly became the domain of mining hardware manufacturers and major exchanges. The volatile market was calling out for "another wave of innovation diffusion."

When discussing the venture cycle from 2016 to 2018, Ethereum stands out as an unavoidable focal point. Its emergence and subsequent success established a second monumental milestone in the crypto industry beyond Bitcoin, triggering the first wave of explosive growth—the ICO (Initial Coin Offering) boom. Countless projects raised initial funding through ICOs, rapidly pushing the crypto industry into a chaotic phase filled with both promise and pitfalls. Idealists shared space with fraudsters, pirates, and thieves; visionaries mingled with the greed-driven. In such wild frontier periods, lies and truths intertwine, and innovation is often just one step away from scams.

A New Crypto Era: Greatness Cannot Be Planned

On July 22, 2014, Ethereum launched its ICO, offering 2000 ETH per BTC at the time, permissionless, without VC involvement or lockups. The ICO ultimately raised over $18 million in Bitcoin, with each ETH priced at approximately $0.30.

Notably, Ethereum co-founder Vitalik Buterin was only 20 years old at the time. The idea for Ethereum originated from a whitepaper he sent to friends in late 2013, proposing a new kind of Bitcoin based on a general-purpose programming language capable of powering diverse applications like social platforms, trading systems, and games. The fact that these ideas have since materialized validates his remarkable foresight into the trajectory of the crypto industry.

Photo of young Vitalik using an IBM computer

One important reason often cited for Vitalik’s entry into the crypto world stems from Blizzard removing the "Life Tap" ability of his beloved Warlock character in World of Warcraft. From then on, the world lost a devoted WoW fan but gained a passionate believer in decentralization.

Later that year, in December, Xiao Feng, CEO of Wanxiang Blockchain Labs and partner at Distributed Capital, learned about Vitalik and gave a speech introducing Ethereum—an event that would later lay the groundwork for what some call the "Shanghai upgrade of Ethereum." As Xiao Feng recounted in an interview: "Ethereum’s mainnet launched in July 2015. Before launch, the foundation’s tokens were locked. They had around $18 million initially, and even after spending some, they still had money left—I recall about $3 million remained. Since the mainnet hadn’t gone live yet, people naturally asked if funds were sufficient. There wasn’t a performance crisis per se, but questions persisted: Could this money last until mainnet launch? What if not? At the time, Vitalik happened to be in Shanghai and visited our office. I heard he had attended a meeting the night before where various parties pressed him for answers, though he didn’t respond immediately.

When I heard about this, my thought wasn't investment-oriented—it was simply about supporting a great endeavor and helping this young man. We genuinely wanted to help him.

Our plan was simple: offer $500,000 in cash upfront and signal ongoing support afterward. After signing a donation agreement and transferring the funds, the Ethereum Foundation promised to return tokens at the original donation price once their mainnet unlocked. We didn’t think in terms of investment returns—we just wanted to back this grand vision. Even if the mainnet failed to launch, we’d have supported something meaningful." Still, Vitalik later remarked in an interview: “Wanxiang’s $500,000 became Ethereum’s lifeline.”

Perhaps as the saying goes, “Greatness cannot be planned.” Ethereum’s development received crucial backing from Xiao Feng and Wanxiang Group—not because of financial calculations, but due to a desire to help a young visionary realize a bold dream. Simple as it sounds, the crypto industry, having weathered the 2013 bear market, desperately needed a new benchmark to restore confidence. Ethereum arrived right on time.

On July 30, 2015, Ethereum released Frontier, its first-phase version. The first Ethereum block was mined, marking the official start of operation for the blockchain network envisioned as a “world computer.”

Despite suffering a major hack in June the following year—The DAO, the world’s first DAO, raised $150 million but lost $60 million worth of ETH to an attacker—leading to a temporary $500 million drop in market cap, Ethereum successfully navigated the crisis. Thanks to leaders like Vitalik, early founders including Gavin Wood, and global community support from Chinese miners and capital firms, Ethereum completed a hard fork upgrade and stabilized.

Further Evolution: VC Tokens Were Once Meme Coins

On May 19, 2017, Ethereum’s price first broke $100, delivering over 300x returns to early investors (though ironically, this date would later become known as one of crypto’s darkest hours).

This reaffirmed Ethereum’s investment value and reignited the ICO frenzy.

In June 2017, Binance launched its platform token BNB via ICO. By July 2, the sale ended, raising $15 million in digital assets. On September 1, Binance announced a $15 million funding round led by Blackhole Capital and Fenbushi Capital.

In August 2017, Binance opened its platform to ICOs—500 million TRON (TRX) tokens sold out within 53 seconds at ~$0.01 each. Subsequently, RenRenICO, ICO365, and others joined the platform. Insiders revealed Tron raised roughly 7,000 BTC (~$200 million at the time) during its ICO.

In September 2017, Cardano (ADA—named after Ada Lovelace, daughter of poet Lord Byron and considered the world’s first programmer) concluded a two-year ICO, raising over $62 million at $0.0024 per token, completing its TGE in October at $0.02.

Top 10 ICO Projects of 2017

Amid growing ICO enthusiasm came endless waves of "whitepaper-first," "air coin" hype projects—fueling regulatory scrutiny.

On September 4, 2017, China’s central bank and six other agencies issued a notice declaring ICOs illegal—known as the "94 Event." While facing global regulatory pressure, the crypto industry continued evolving. Binance quickly relocated from Shanghai to Japan, began delisting users from restricted regions, and laid the foundation to become the world’s largest crypto exchange.

Yet looking back at fundraising methods at the time, today’s VC-favored “value tokens,” with their relatively decentralized distribution, low initial prices, and meme-like ticker symbols, could arguably be seen as meme coins themselves during that era.

Additionally, according to the "2017 China Internet Finance Investment and Financing Analysis Report," equity financing deals in blockchain rose from 4 in 2016 to 29 in 2017—a 625% increase. According to CoinMarketCap, the total market cap of cryptocurrencies exceeded $600 billion by the end of 2017, encompassing 1,334 digital currencies.

On January 17, 2018, Binance surpassed 6 million registered users—over 97% from overseas, spanning more than 180 countries. Soon, Binance overtook Huobi and OKCoin (now OKX) in trading volume, becoming the world’s top digital asset exchange. Thus, the triad of Binance, OKCoin, and Huobi emerged, while exchange-affiliated venture arms began building influential investment portfolios that would grow increasingly prominent as exchanges gained more influence.

It should be noted that ICO chaos drew global regulatory attention. In early 2018, Gibraltar announced plans to introduce the world’s first ICO regulation, attracting close scrutiny from UK and Singapore regulators. Switzerland’s financial regulator FINMA classified ICO tokens into three categories, treating asset-backed tokens as securities. Russian authorities proposed that ICO issuers must have at least 100 million rubles in nominal capital. Meanwhile, the U.S. applied existing securities laws to regulate ICOs.

Such oversight was clearly necessary. A Bloomberg report from July 2018 found that about 78% of ICO projects were identified as scams before going live. By July 2018, top-tier projects accounted for 70% of total ICO funds raised (in USD). Later developments like IE0 and IDO, along with various fundraising and asset issuance models, can all be seen as variations or evolutions of the original ICO concept.

The Big Trend: Public Chains Become Investment Favorites

In 2018, thanks to founder BM’s celebrity status and traffic and capital from early Chinese Bitcoin evangelists like Li Xiaolai, EOS raised $185 million in its first five days of ICO. After launching the “21 Super Node Election” campaign voted on by EOS holders, figures like Xue Manzi, Baozou Gongqinwang, Lao Mao, Yi Lihua, and Antpool publicly entered the node race, bringing massive attention and liquidity to EOS. Finally, on June 2, EOS concluded its year-long ICO with an impressive $4.2 billion raised.

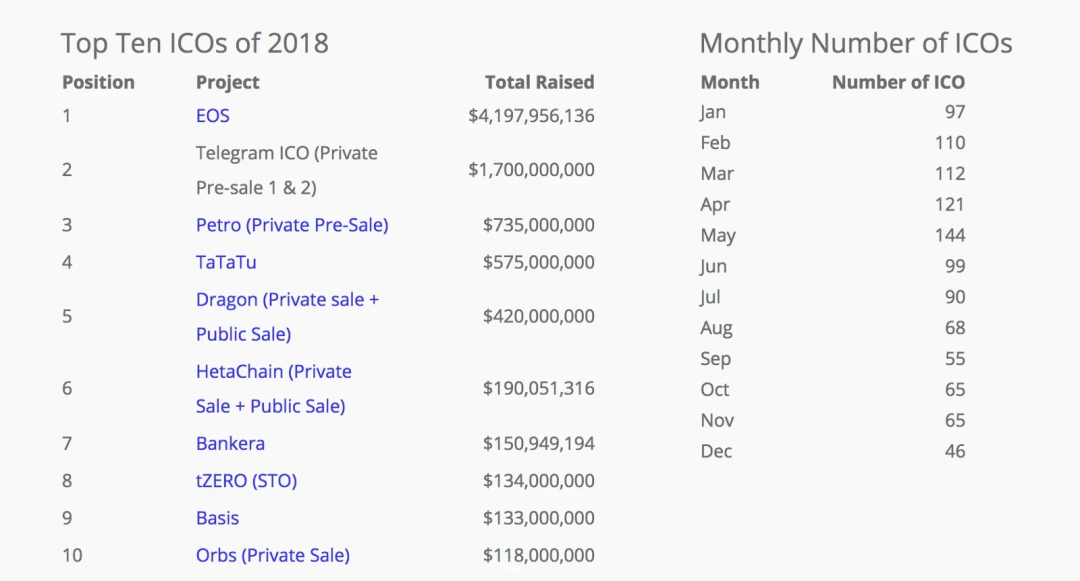

Top 10 ICO Projects of 2018

As Xu Chaoyi, managing partner at BKFund and director of strategic management at Distributed Capital, stated in a 2018 interview with 36Kr: “In 2018, BKFund focused primarily on blockchain public chains as the first-tier investments; vertical-specific public chains ranked second; specific vertical applications lagged behind, leaning more toward traditional internet apps migrating onto blockchain networks.” He openly admitted the logic behind this preference: “In the blockchain space, base-layer protocols or public chains command the highest valuations. Platform layers are lower, and business layers, especially vertical-specific ones, have much less imagination and lower valuations.”

Partly because the crypto industry was still in its early stages with significant infrastructure gaps, and partly because Ethereum set such a high bar, countless individuals and institutions rushed in hoping to replicate Wanxiang’s massive returns from supporting Ethereum. ‘Finding the next Ethereum’ became an obsession for many, explaining the popularity of projects like Cosmos and Polkadot later on.

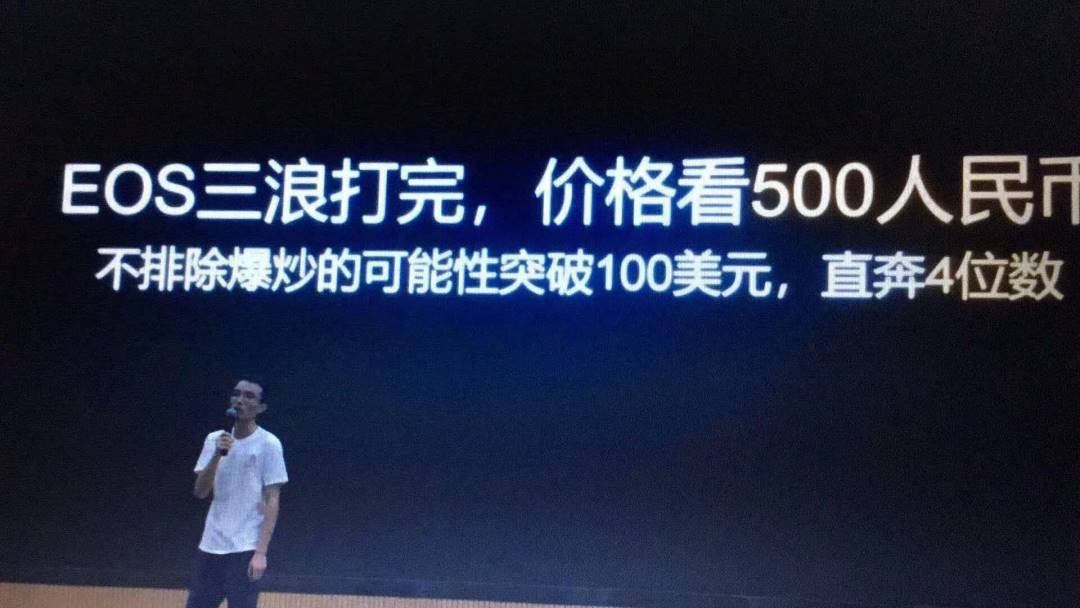

But clearly, the claim that ‘after three waves, EOS will break $1,000’ was merely a fantasy born in a bubble. And the cost of such fantasies proved severe—even devastating—as EOS’s price action later showed: ‘The market does not care about individual wishes.’

EOS “Three Waves” Classic Statement

After hitting a new market cap high of $850 billion early in the year, the crypto industry faced another round of “cleansing”—Bitcoin dropped from over $18,000 to around $3,200 by year-end, down about 82%; Ethereum fell from nearly $1,500 to below $100, reaching a low of ~$83. Bull-to-bear transitions, portfolio stress tests—these dramas play out constantly in the crypto world.

However, judging from H1 investment data, the arrival of crypto winter wasn’t as abrupt as expected—indeed, it seemed slightly hot. According to Securities Daily, blockchain投融资热度 climbed in H1 2018, recording 222 funding events. The U.S. and China together accounted for 179 deals, or 80.6% globally. Although China saw 141 deals versus the U.S.’s 38, funding amounts were comparable—6.4 billion yuan vs. 6.7 billion yuan. Of all rounds, 107 (48.2%) were seed/angel, totaling 1.6 billion yuan (just 10% of total funding). In terms of country-level breakdown, China recorded 73 seed/angel, 9 Pre-A, and 16 Series A deals, compared to 18, 0, and 6 in the U.S., respectively.

Wave After Wave: DeFi Summer, GameFi Summer, NFT Summer

Entering 2019, crypto venture investments turned more rational. Total funding declined nearly 40% compared to 2018, with 653 deals raising nearly $4.7 billion (~32.9 billion RMB). Additionally, there were 35 disclosed M&A events totaling over $3 billion.

Overall, 2019 felt like a transitional period—active in fundraising but concentrated mainly in digital asset domains represented by exchanges and financial applications. In February, Kraken raised $100 million. In October, A.TOP Exchange received 50,000 BTC in funding—one of the largest disclosed raises (though met with market skepticism). Indian fintech giant PhonePe secured $101 million in July and 4.05 billion INR in October. Payment firms Rapyd and Ripple raised $100 million and $200 million, respectively, in the second half. Exchanges led with 129 deals (20% of total), raising ~$2.22 billion (~40% of annual total).

From an investor perspective, 2019 marked a turning point—Western VCs began rivaling Chinese counterparts. U.S.-based Digital Currency Group topped the list with 14 investments, becoming the most active firm globally. Coinbase, founded in 2012, and its subsidiary Coinbase Ventures, launched in 2018, jointly ranked among top investors with 6 deals each—laying the groundwork for the next DeFi wave.

2019 Institutional Investment Rankings

Starting in 2020, waves of innovation across different sectors would take the world by storm—one trend rising as another faded.

DeFi Summer: Liquidity Mining Becomes Industry Standard

After Ethereum’s emergence, a key question lingered: “What can Ethereum actually do?” As Bitcoin’s consensus value grew through wider adoption, higher demands were placed on the practical utility of so-called “Crypto 2.0” systems like Ethereum.

Though the March 2020 crash cooled the market, DeFi Summer quietly arrived as Compound and Aave (formerly ETHLend) gained traction, and Curve, SushiSwap, Uniswap, and 1inch launched their own tokens.

Synthetix (SNX) introduced “liquidity mining” in July 2019, but it was Compound’s distribution of governance token COMP that truly brought the concept to life. Yearn Finance’s YFI becoming the first crypto asset ever to surpass Bitcoin in price cemented “yield farming” in popular consciousness. Staking also officially entered the mainstream and evolved into a core industry paradigm.

Users could now earn native protocol tokens by providing liquidity, sparking a new wave of token launches—projects realized issuing tokens was one of the most effective ways to attract users and liquidity.

After all, the pursuit of wealth remains the unforgettable “original intention” of every player in crypto.

Industry data shows that global crypto fundraising continued strong growth in 2020, with 434 deals completed throughout the year, many projects securing multiple rounds. Total disclosed funding reached $3.566 billion (excluding acquisitions).

According to Arcane Research, DeFi’s total value locked (TVL) grew ~2100% annually, unique addresses increased tenfold. Yet despite ample market liquidity, or perhaps because DeFi Summer intensified competition, DeFi project funding totaled ~$278 million—only 7.8% of the industry total. Average deal size was just $4.8 million, the lowest among all sub-sectors. BlockFi’s $50 million raise in August was the largest single DeFi deal of the year.

Yet a year after DeFi Summer, metrics tell a deeper story: TVL up 58x, user count up nearly 140x, borrowing volume up over 3474.1%, DEX trading volume surged up to 382.5x. DeFi’s impact on the entire crypto ecosystem was profound and far-reaching. That year, Polkadot (DOT) also raised ~$43 million via ICO, becoming another “star public chain.”

GameFi & NFT Summer: Axie Infinity’s Play-to-Earn Gold Rush + OpenSea’s Blue-Chip NFT Boom

Entering 2021, three types of events significantly impacted the industry:

First, in traditional finance: Coinbase went public on NASDAQ under ticker COIN, pushing “compliance to the extreme”; Roblox listed on NASDAQ, fueling the “metaverse” craze; Facebook rebranded to Meta.

Second, in crypto: The “FTX ecosystem” (including FTX exchange, Alameda Research, and affiliated projects like Solana) rose rapidly, positioning FTX as a major new force and briefly making it the second-largest exchange—though planting seeds for its 2022 collapse.

Third, in sector-specific projects: Axie Infinity and gaming guild YGG led the GameFi “play-to-earn gold rush,” while blue-chip NFTs like BAYC and CryptoPunks, along with OpenSea, drove the NFT Summer—which lasted until May 2022, culminating in the Otherside land sale burning 10,000 ETH in gas fees.

Meanwhile, “Web3” entered mainstream discourse in a more accessible, inclusive way, championed by Ethereum co-founder Gavin Wood, Polkadot founder, and a16z investor Chris Dixon, becoming the latest synonym for the “crypto industry.”

Solana, founded in 2017 by former engineers from Qualcomm, Intel, and Dropbox, leveraging a “Proof of History” mechanism for enhanced network efficiency, shined brightly this year. After raising $25 million in private and ICO rounds, it secured $40 million in March from OKX and MEXC, and $314 million in June led by a16z and Polychain Capital, with participation from 1kx, Alameda Research, Blockchange Ventures, CMS Holdings, Coinfund, CoinShares, Collab Currency, MGNR (Memetic Capital), Multicoin Capital, ParaFi Capital, Sino Global Capital, Jump Trading, Boys Noize, and others. Promoted as having “TPS far exceeding Ethereum,” it was hailed as the “next Ethereum killer.”

Multicoin Capital, a deep investor in Solana, earned thousands of times return—but soon, entering 2022, the market would teach everyone a lesson: “What makes you succeed can also become your downfall.” Path dependency leads directly to “gains and losses sharing the same root.”

Axie Infinity’s parent company Sky Mavis, famed for driving Southeast Asia’s play-to-earn craze, raised $7.5 million in May 2021 from Libertus Capital, with participation from Blocktower Capital, Konvoy Ventures, Collab Currency’s Derek Schloss, Stephen McKeon, and Dallas Mavericks owner Mark Cuban. Their next raise wouldn’t come until April 2022—but then jumped to $150 million. Founded in 2017, Axie achieved a milestone in November 2020 by listing AXS on Binance as the “most active blockchain game,” with only ~7,000 monthly active users at the time. Within months, it became synonymous with GameFi, pioneering the “Play-to-Earn” (P2E) model and paving the way for STEPN.

As for BAYC, despite celebrity endorsements from figures like Steph Curry and Snoop Dogg driving its floor price above 55 ETH, it had not yet raised funding during this period.

That year, OpenSea was unquestionably the NFT leader—after raising $2 million in seed funding in 2018 and $2.1 million in strategic funding in 2019, it secured $23 million in Series A in March 2021 led by a16z, with Cultural Leadership Fund and angel investors including Ron Conway, Mark Cuban, Tim Ferriss, Belinda Johnson, Naval Ravikant, and Ben Silberman. In July, it raised another $100 million in Series B, also led by a16z, achieving a $1.5 billion post-money valuation. This was still months before the peak of the NFT bubble—OpenSea still had more to show.

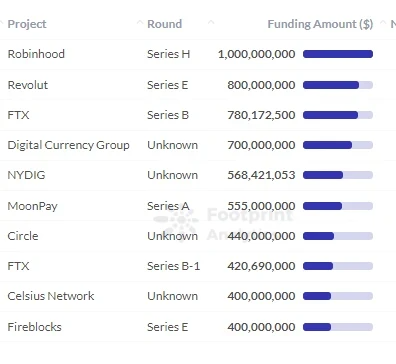

According to Footprint Analytics, 2021 saw 1,045 funding rounds totaling $30.27 billion—nearly a 790% increase from 2020. Top CeFi fundraisers included Robinhood, FTX, and Revolut. Top DeFi fundraisers were BitDAO, FalconX, and 1inch.

Notably, DAOs gained immense attention—Seed Club, Bankless DAO, FWB were seen as标杆 organizations—but were eventually somewhat “disproven” by the market.

CeFi Funding Rankings

And in November 2021, amid rapid ascent, the crypto market cap finally breached $3 trillion. After enduring the “5·19” crash earlier that year, another bull run emerged, accompanied by fresh narratives. More stories from venture cycles continue unfolding.

Crypto Market Cap Breaks $3 Trillion

Summary: Each Generation Has Its Gods, Every Cycle Has Its Masters

Looking back at the crypto venture cycle from 2016 to 2021, each phase, bull or bear, cycle had its own “main theme” and “meta answer.” Project leaders and key players rose and fell—some retired victorious, some vanished, some remain active today, others still searching for their “wealth code.”

In the upcoming second part covering 2022–2024—the most recent cycle—we’ll continue tracking people, events, and trends in the crypto venture landscape. While summarizing the past, we aim to extract lessons and insights for readers. Readers interested in discussion are welcome to reach out—additional perspectives and information are always appreciated.

See you in the next chapter of TechFlow's Evolution of Crypto Venture Cycles (Part 2).

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News