Coinbase Research: The crypto market still lacks a strong narrative, and Q3 will be dominated by volatility

TechFlow Selected TechFlow Selected

Coinbase Research: The crypto market still lacks a strong narrative, and Q3 will be dominated by volatility

If concerns about a sharper economic slowdown intensify, rate cuts could be不利 to the market.

Source: Coinbase

Compiled by: BitpushNews Mary Liu

Summary:

-

According to Arkham data, Germany's Federal Criminal Police Office (BKA) may have completed its sell-off, reducing its holdings from approximately 50,000 BTC ($3.55 billion) in mid-June to 0 BTC as of July 12 (data截至 at 14:38 ET that day).

-

Concerns remain that rate cuts could be negative for markets if economic slowdown fears intensify amid worries about a potential U.S. recession later this year or early 2025.

-

Discussions and presentations at the seventh Ethereum Community Conference (EthCC), including a keynote by Ethereum co-founder Vitalik Buterin, reaffirmed Ethereum’s roadmap: serving as a maximally decentralized and secure Layer 1 (L1) settlement layer for various Layer 2s (L2s).

Market View

The third quarter started on a weak note, with oversupply driven by sales from price-insensitive Bitcoin holders. This includes Germany’s Federal Criminal Police Office (BKA), which began selling its seized Bitcoin on June 19. Although the scale of BKA’s sales—averaging $85 million per day—is not particularly large relative to the $10.6 billion in daily BTC spot trading volume (since June 1 on global centralized exchanges)—the agency’s mindless dumping unsettled the market and pressured Bitcoin prices.

On the positive side, according to Arkham Intelligence, BKA may have nearly completed its sell-off by July 12, as its holdings dropped to zero (though it remains uncertain whether some funds might be returned via CEXs). We believe this suggests much of the associated market panic should soon subside.

Meanwhile, repayments from the Mt. Gox Rehabilitation Trust, beginning July 5, are also affecting the market, though it remains unclear how much of the repaid BTC has actually been sold.

Exchanges approved to handle repayments include Bitbank, BitGo, Bitstamp, Kraken, and SBI VC Trade. However, processing times vary significantly across exchanges due to internal verification procedures—ranging from immediate (Bitstamp) to up to 90 days (Kraken).

We believe uncertainty is more damaging to the market than any actual selling, as major creditors (third parties who purchased claims) are likely hedged. Furthermore, we expect any real selling to be gradual and orderly, resulting in only moderate market impact.

Looking further ahead, what might drive market performance for the remainder of the quarter?

Recently, there has been growing concern in multiple reports about a potential U.S. recession later this year or in early 2025.

We hold the opposing view: productivity gains driven by accelerated post-pandemic tech adoption—including but not limited to generative AI models—will usher in a new multi-year economic cycle, possibly starting as early as Q4 2024. (Timing is difficult to predict.) Still, such divergent economic views are unusual, and interpreting increasingly complex signals presents a challenge.

That said, macro data already offers substantial evidence that the U.S. economy has slowed (ISM manufacturing, unemployment rate, domestic demand, etc.), and we acknowledge this.

In fact, we believe the U.S. economy likely peaked in Q2 2024—which is one reason we expect the Fed to begin cutting rates starting September 18 (too early to act in August, and no meeting then). Indeed, this week’s June CPI print—down 0.1% month-over-month and 3.0% year-over-year—came in below median expectations of +0.1% and 3.1%, potentially supporting a more dovish Fed stance.

The concern is that if fears grow over a sharper-than-expected economic slowdown, rate cuts could be bad for markets.

That is, if the U.S. enters a recession, retail investors may be reluctant to enter new stock or crypto positions.

Conversely, if the economy remains relatively strong while the Fed cuts rates, this could unleash additional liquidity and attract more retail participation.

Moreover, the U.S. election in November means fiscal expansion appears likely regardless of the winner. In our view, this strengthens the case for buying Bitcoin as an alternative to the traditional financial system.

Currently, we expect Q3 2024 price action to remain volatile, as the crypto market still lacks a strong narrative.

For example, the market remains undecided on whether potential inflows from a spot ETH ETF (experts expect a launch soon) are bullish or bearish, although we don’t see this as necessarily negative from a positioning standpoint. Even if inflows take time to materialize, this could leave room for outperformance and provide additional support for ETH. Overall, we believe the next two months may bring increased volatility until conditions start improving more clearly by end-September.

EthCC Highlights

The 7th Ethereum Community Conference focused on key technical themes including Layer 2 (L2) scaling and differentiation, ETH staking issuance, and cross-chain interoperability. Panel discussions and talks—including a keynote by Ethereum co-founder Vitalik Buterin—reaffirmed Ethereum’s roadmap: serving as a maximally decentralized and secure Layer 1 (L1) settlement layer for diverse L2s.

Ethereum continues to focus on being a settlement-layer L1, indicating its execution layer is unlikely to scale significantly in the near term (measured in gas per second). Instead, the focus is on increasing data availability bandwidth for L2s. However, this does not mean ETH utility is stagnant.

On the contrary, the diversity of L2s enables rapid competition among different technical approaches. L2 platforms like Optimism, Base, Arbitrum, and Starknet showcased their unique technological and ecosystem strengths at EthCC. The ability of L2s to rapidly iterate and compete is a distinctive advantage of the modular approach—and one of Ethereum’s strengths we’ve previously emphasized.

That said, universal interoperability between L2s remains a contentious issue. While many solutions appear technically feasible (with varying trade-offs), no single solution has emerged as a dominant standard across all chains. Communication standards often become “winner-take-all” markets due to network effects, but crypto interoperability faces additional challenges in resolving conflicting interests. Namely, the ability of interoperability protocols to monetize adoption of their standards makes this space nearly zero-sum. In our view, full interoperability remains an open challenge that may take months or even years to converge into a clear standard.

However, we do not believe interoperability barriers will hinder user onboarding in terms of crypto user experience (UX).

Account abstraction and smart accounts are gaining momentum. Beyond core infrastructure, more decentralized application (dApp) developers appear interested in leveraging gas abstraction and transaction bundling to streamline dApp experiences. Additionally, session key technology—which enables automatic transaction approvals under specific conditions—shows promise as a way to further reduce UX friction, especially in DeFi (swaps) and gaming.

Staking and restaking were also discussed topics.

Rising staking rates (currently 28% of total ETH supply) and the resulting decline in net staking APY may pose long-term challenges to the economic viability of solo stakers. Similarly, concerns were raised about the growth and centralization of liquid staking tokens (LSTs). While no definitive conclusions were reached, suggestions included lowering the base issuance curve (which could theoretically slow staking growth) and establishing LST standards to encourage greater LST diversity and competition. Meanwhile, restaking faces challenges regarding implementation timelines. No shared security layer has yet enabled payment and slashing functionality. Additionally, uncertainty remains about the significance of yields from active validation services (AVS) relative to the size of restaked ETH in the short to medium term (a risk we highlighted earlier this year).

To a large extent, main conference discussions centered on the infrastructure layer, despite numerous consumer-facing applications showcased at peripheral events. These included AI-interpreted blockchain data, permanent on-chain games, novel prediction markets, and more. That said, in our view, the ratio of infrastructure to applications still appears heavily skewed toward infrastructure projects.

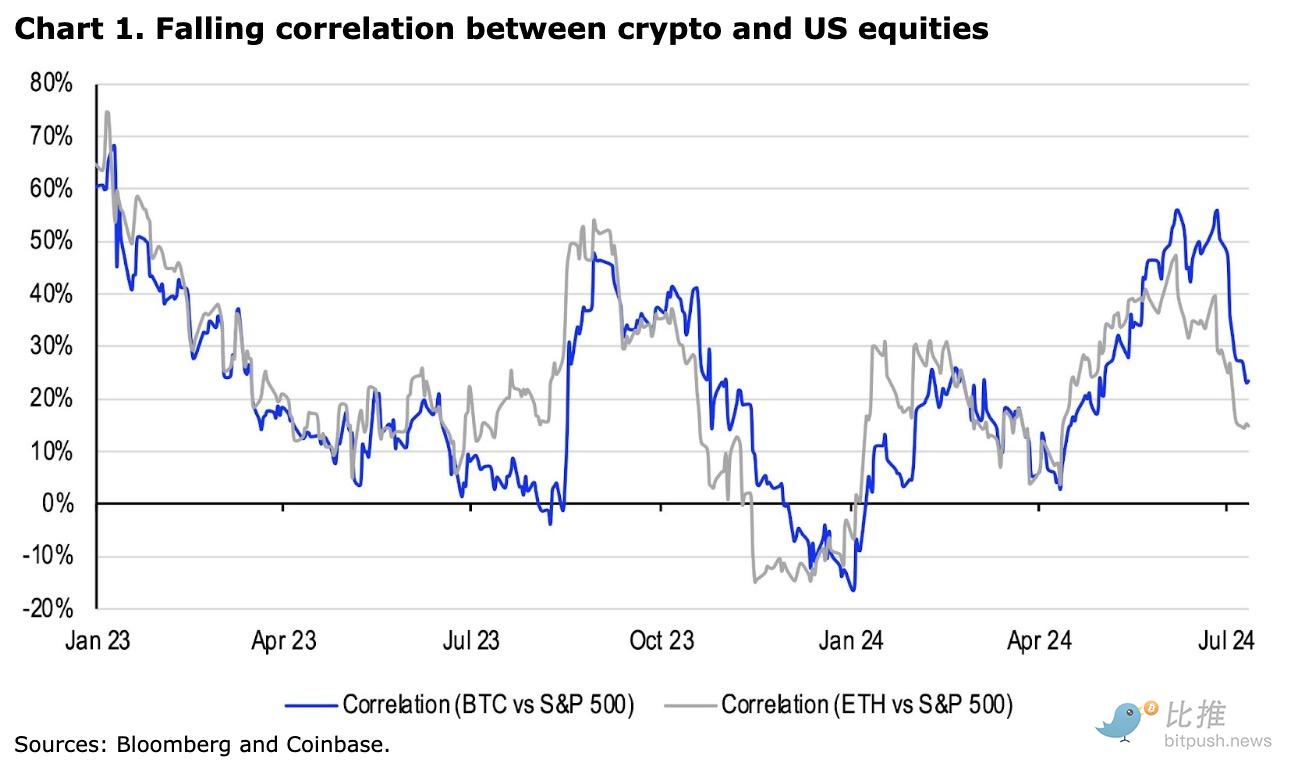

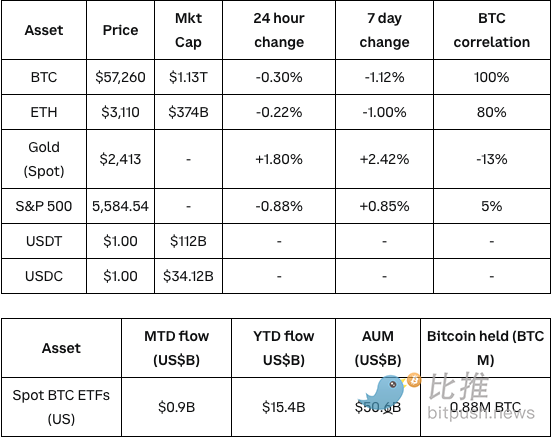

Crypto and Traditional Market Overview (Data as of 4:00 PM ET, July 11)

Source: Bloomberg

Coinbase Exchange and CES Insights

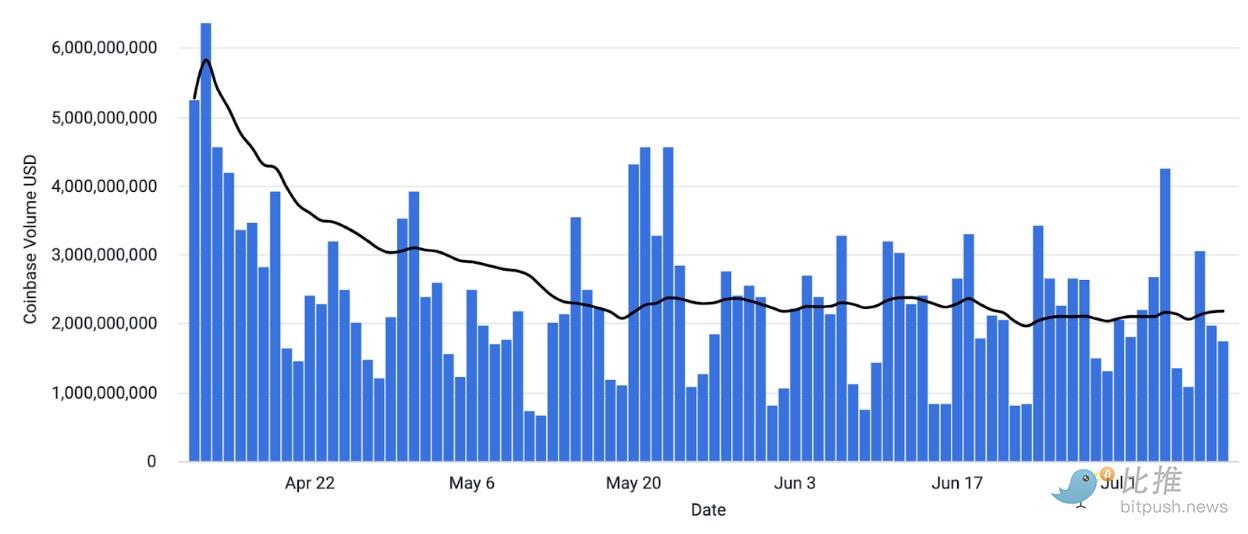

This week, Bitcoin consolidated below its 200-day moving average. Subpar CPI data failed to push the token higher, as supply concerns continue to weigh on the market. Ethereum traded in a tight range around $3,000, as traders await a spot ETF launch in the U.S. Positioning in the token remains light, but we’ve begun to see a shift from altcoins into ETH. Elsewhere in the market, SOL has held up relatively well during this month’s sell-off, leading some traders to believe it could outperform if the broader crypto market rebounds.

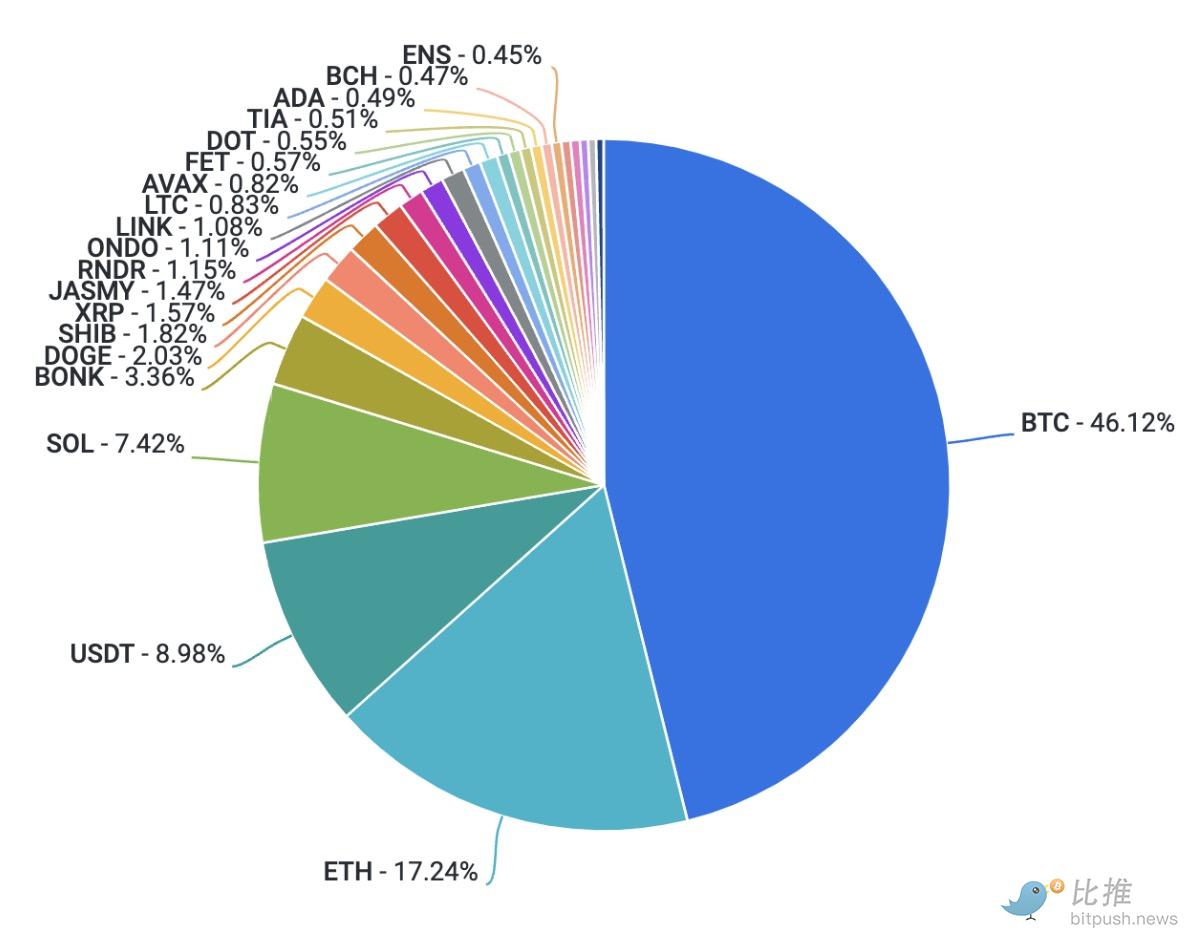

Trading volume (USD) on Coinbase platform

Trading volume on Coinbase platform by asset

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News