Everyone's numb from the losses—do governance tokens really need to exist?

TechFlow Selected TechFlow Selected

Everyone's numb from the losses—do governance tokens really need to exist?

Two key characteristics required for governance tokens: control over economic value and reliability of control.

Author: Outerlands Capital

Compiled by: TechFlow

Governance tokens are a complex and controversial topic, with diverse opinions among crypto investors ranging from “novel innovation” to “fundamentally unnecessary.” We lean toward the former view and believe well-structured governance tokens can significantly enhance a project’s value.

Key Takeaways

-

In this article, we propose a four-quadrant framework for evaluating governance tokens based on two dimensions: the reliability of rights granted to token holders and their control over economic value.

-

After introducing the framework, we illustrate each quadrant through case studies and conclude with recommendations for builders and investors on how to design and assess governance tokens.

Introduction

Governance tokens are commonly defined as tokens that grant holders voting rights over certain project parameters, such as implementing product updates, capturing fees/revenue, or making business development decisions. While market participants often treat governance tokens as a distinct category, it is more accurate to view governance as a feature or attribute that any token might possess. Examples exist across every crypto subsector—from Layer 1s and DeFi to infrastructure and gaming.

In this article, we explore the utility of governance tokens and examine when they successfully—or fail to—unlock value for their underlying projects. We begin by outlining the role of governance tokens in cryptocurrency, addressing common criticisms and justifying their existence. This initial analysis reveals two critical characteristics required for effective governance tokens: control over economic value and the reliability of that control.

We derive a framework from these core features and apply it to case studies that highlight the differences between projects meeting versus failing our criteria. Finally, we summarize how projects and potential investors should approach the design and valuation of governance tokens.

Should Governance Tokens Exist?

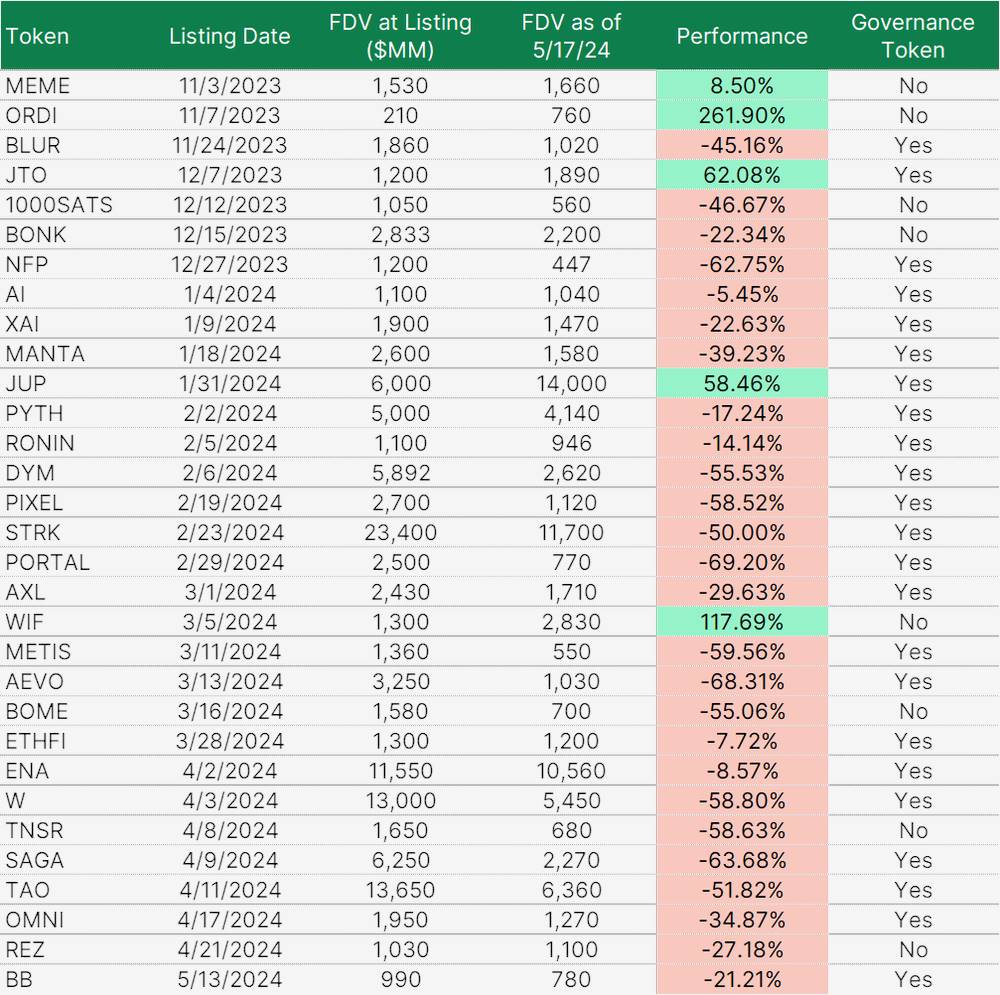

Figure 1: Performance of newly listed Binance tokens since November 2023. Source: @tradetheflow_, Outerlands Capital Research

Some market participants and builders argue that governance tokens have no reason to exist—or at least should be far fewer than currently observed. This view has been reinforced by relatively poor performance of newly launched venture-backed tokens, which often carry high valuations and struggle against large-cap tokens and meme coins.

Common criticisms include:

-

Protocols function equally well—or even better—without decentralized governance (or even without tokens), and token issuance only reduces efficiency.

-

Many teams launch tokens solely for early profit extraction, lacking genuine utility rationale.

-

The utility provided by governance tokens often has little impact for smaller investors who lack sufficient influence to shape strategic direction.

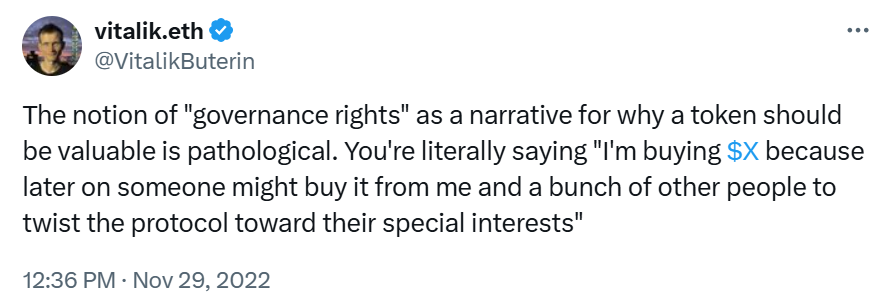

Notably, skepticism about governance tokens isn’t limited to fringe voices. Respected figures like Ethereum co-founder Vitalik Buterin and Hasu, strategy lead at Flashbots, have expressed doubts about their benefits.

Figure 2: Vitalik Buterin's comments on governance tokens

While some of the above points may hold true in specific cases, we believe all are ultimately incorrect. When properly structured, projects using governance tokens can retain the centralized advantages beneficial during early stages while unlocking additional value through decentralized governance. For example, teams can maintain control over strategic direction and product development while delegating authority over other key parameters—such as protocol revenue distribution or approval of new upgrades—to token holders. Projects can also strategically use airdrops and community distribution programs to align long-term stakeholders with protocol incentives. We believe governance tokens create value in two primary ways:

-

Governance tokens can help applications manage inherent risks in their business models. Crucially, they do so more effectively than non-tokenized governance systems because they provide aligned incentives. For instance, governance tokens can mitigate vulnerabilities arising from centralization vectors within protocols. Although Layer 2 networks like Optimism and Arbitrum continue developing their own technologies, they already secure billions of dollars in TVL on-chain. If a centralized entity like Offchain Labs (Arbitrum’s developer) could arbitrarily upgrade contracts or modify system parameters, it would pose significant risk—malicious code upgrades could result in fund theft. Yet, the technology remains under development and requires ongoing upgrades to stay competitive. By decentralizing these decision-making powers, projects become more resilient, as no single entity becomes an attractive target for malicious actors.

-

Governance tokens can offer tangible economic utility to holders in the form of real financial value. A notable example is GMX, a crypto derivatives platform that distributes a portion of trading fees to those who purchase and hold its token. Many centralized exchanges similarly offer fee discounts to their token holders. Other projects can adopt similar mechanisms to provide economic benefits in exchange for funding development or aligning incentives.

There are numerous governance tokens that meet at least one of these standards, and we remain optimistic about the emergence of more such tokens in the future.

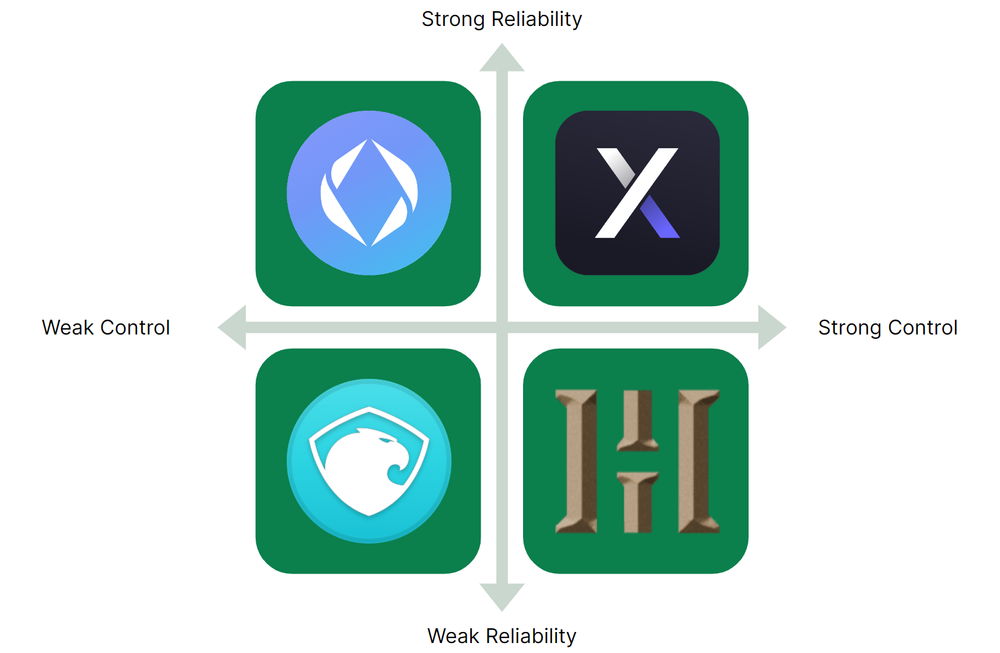

Outerlands Capital’s Governance Token Evaluation Framework

We evaluate governance tokens across four quadrants, where:

-

The Y-axis represents reliability—the strength of rights granted to token holders. Reliable tokens establish clear, enforceable rights that cannot be easily altered, giving holders greater certainty over their control of specific parameters. In contrast, unreliable tokens nominally grant voting rights but leave substantial uncertainty about whether the team or protocol will respect those rights. Chris Dixon makes a similar argument in *Read Write Own*, emphasizing the importance of a protocol’s ability to make strong commitments.

-

The X-axis represents control, defined as the degree to which token holders possess economic value or other utility. Tokens with strong control give ecosystem participants (users, investors, etc.) compelling reasons to hold them, whereas weak-control tokens offer little incentive.

Figure 3: The Four Quadrants of Token Governance. Source: Outerlands Capital Research

Characteristics of High-Reliability Tokens

Below are the attributes Outerlands Capital looks for in tokens with strong reliability:

-

A robust charter aligned with the core ethos of the project.

-

Amending the charter should require higher thresholds than other governance votes (e.g., supermajority of 2/3 and quorum of 10%).

-

-

A comprehensive governance process including:

-

Multiple proposal tracks balancing urgency and importance to ensure both efficiency and democracy:

-

Day-to-day operational functions (e.g., grants, payroll) should be managed directly by the team or designated subcommittees, enabling faster decisions than standard governance allows. Token holders should still have visibility and the option to raise objections if needed.

-

Critical decisions (e.g., major technical deployments, fiscal investments above a threshold, or risk management functions) should undergo multi-stage discussions lasting longer than one week.

-

-

A dedicated forum and voting platform that is accessible and easy for token holders to use.

-

The ability for token holders to delegate their governance power to knowledgeable or aligned parties.

-

A democratically elected emergency DAO/security council capable of responding to critical incidents like hacks, with the DAO retaining the ability to modify or remove the council.

-

On-chain execution/enforcement of important decisions (so token holders don’t need to trust the team to implement vote outcomes). These must be rigorously audited and properly constructed to prevent governance attacks, with reasonable timelocks included.

-

-

A foundation or other legal entity representing the DAO in the real world (may not apply to fully anonymous teams). This limits legal liability for governance participants and makes it easier for others to conduct business with the DAO (as they can interact with a more traditional corporate structure).

-

Strong enforcement of any specific utility promised to token holders (e.g., revenue distributions or regular buybacks). Ideally, this should be implemented directly at the protocol level or via smart contracts (the strongest form of commitment), though legal protections are also acceptable.

Characteristics of High-Control Tokens

Broadly speaking, high-control tokens grant holders authority over significant economic parameters. The most obvious mechanism investors should look for resembles traditional equity. A project that distributes revenue (with holders governing the distribution method) or conducts public market buybacks of its token can be easily evaluated based on cash flows. As the underlying business grows, the token shares in its success—making token investment a straightforward bet on the business. Investors can apply conventional metrics such as discounted cash flow analysis or relative valuation based on revenue/profit multiples.

However, beyond equity-like value capture, several other control factors may incentivize holding tokens. These include:

-

Other forms of economic utility, such as protocol fee discounts or priority access to products for users holding a certain amount of tokens.

-

Control over technical upgrades and deployment of new protocol versions, which may affect stakeholders’ economic interests.

-

Authority over changes related to tokenomics, including inflation/deflation and distribution, which could impact existing token holders’ voting power.

-

Influence over business development decisions affecting the protocol’s financial success, such as team salaries, partnerships, incentive programs, and payments to third parties like exchanges and market makers.

Case Studies Applying the Evaluation Framework

The following case studies illustrate tokens across the four quadrants, showing how governance can enhance—or undermine—a project’s fundamental value.

High Control, High Reliability: dYdX

Decentralized derivatives exchange dYdX (token: DYDX) exemplifies the high-control, high-reliability quadrant. Founded in 2017, dYdX offers perpetual contract trading across 66 markets (as of June 2024). In November 2023, dYdX upgraded to version 4 of its trading software, migrating to its own Cosmos app chain and significantly improving its tokenomics through changes to governance processes, token utility, and revenue accrual mechanisms.

Today, the DYDX token provides the following control mechanisms:

-

DYDX serves as the staking token for the application chain, meaning stakers earn yield from trading fees in exchange for securing the network. Like most PoS blockchains, DYDX stakers receive fees proportionally to their stake, creating a linear relationship between purchasing tokens and earning yield. Token holders who do not wish to stake can delegate their DYDX to others in exchange for a share of earned rewards. At current activity levels, the chain generates over $43 million annually in fees for validators⁹.

-

DYDX holders have the right to propose and vote on proposals that directly influence the development path of the dYdX chain. Recent proposals have included launching new perpetual markets, trading incentive programs, funding for the dYdX Foundation, and technical upgrades.

Through these enhancements, the DYDX token delivers multiple benefits to stakeholders, including access to governance, control over protocol revenue, and meaningful influence over future project development.

On the reliability front, the new token model plays a crucial role in the project’s integrity. Beyond technology, one of the core motivations for dYdX’s migration from an Ethereum-based rollup to Cosmos was achieving superior decentralization through a distributed set of PoS validators. This not only reduces regulatory risks associated with running a centralized sequencer but also enables direct revenue distribution to token holders via staking rewards—a strong, hard-to-reverse commitment compared to team-run revenue-sharing schemes. Similarly, all other governance proposals are executed on-chain after successful votes, ensuring enforceability.

Low Control, High Reliability: Ethereum Name Service (ENS)

The Ethereum Name Service (ENS) is a decentralized naming service for crypto wallets, websites, and applications, serving as an example of the low-control, high-reliability quadrant.

On the surface, ENS is one of the more successful projects in crypto, generating $16.57 million in revenue over the past year (as of May 2024), placing it among the top 25 highest-revenue projects tracked by Token Terminal. Nevertheless, the ENS token’s market cap ranks well outside the top 100 (despite only about 31.5% of supply being in circulation¹²). This outcome largely stems from the mission codified in the DAO’s charter, which includes:

-

Fees serve as an anti-squatting mechanism and to fund DAO operations. Profit maximization is not a priority. The average ENS domain renews for $5 per year—less than half of what popular Web2 providers charge. ENS could likely double fees with minimal demand loss.

-

Revenue accumulated in the ENS treasury should be used to develop the ENS ecosystem and ensure its long-term viability. Any surplus income should fund other public goods in the Web3 ecosystem.

This is not a critique of ENS Labs—the nonprofit responsible for core software development—for enshrining this charter before handing control to the DAO. ENS possesses several traits required for strong reliability, including vote delegation, on-chain execution, and multiple proposal tracks. The Cayman Islands foundation representing the DAO in the real world provides limited liability protection for participants (addressing legal concerns raised in cases like OokiDAO). For projects aiming to operate as nonprofits, ENS serves as a strong model.

However, its public-interest orientation limits token holders’ potential control over the project. Given the low likelihood of ENS increasing fees or distributing revenue in the future, the token holds limited appeal for investors and lacks a compelling upside narrative. Even if domain sales grow significantly, token holders should not expect to benefit from those revenues. The structure of the ENS charter makes it difficult to become a target for activist investors. As a result, only a few groups have strong incentives to acquire governance tokens:

-

Individuals deeply committed to the DAO who want to contribute to its growth and success. Such individuals are more likely to act as delegates rather than accumulate large amounts of tokens for themselves.

-

Projects wishing to collaborate with ENS, which must obtain or be delegated at least 100,000 tokens (currently worth ~$2 million) to submit proposals.

-

Projects already integrated with ENS that want to preserve the protocol as free public infrastructure.

While these groups are not entirely devoid of demand, they alone cannot generate the kind of powerful economic flywheel seen with dYdX.

High Control, Low Reliability: Hector Network

Hector Network represents a project in the high-control, low-reliability quadrant. It emerged in 2021 as one of many forks of Olympus DAO, claiming to be the reserve currency of DeFi.

Originally a replica of Olympus DAO on the Fantom blockchain, Hector evolved into an on-chain asset manager. New investors could deposit funds into its treasury via a bonding mechanism and receive newly minted tokens, while existing stakers retained their claim value. The team could then use treasury funds to build new projects and invest assets for returns. Meanwhile, token holders were granted control over key protocol parameters—including treasury investment decisions—giving the token high marks in our control dimension.

The Hector Network team attempted to generate value for the treasury by building multiple DeFi-focused products. However, due to poor execution and the 2022 market downturn, these products failed. Community dissatisfaction with the team grew, especially as the roadmap faltered while the team paid itself generous salaries (reportedly $52 million over 18 months).

When token holders sought to exercise governance rights over the remaining treasury, the absence of legal or smart contract protections left them vulnerable. The Hector Network team began censoring individuals in the project Discord and imposing governance restrictions. When the team eventually agreed to propose a treasury liquidation, only about $16 million remained, and the HEC token had lost 99% of its all-time high value.

Stronger governance safeguards for HEC holders could have steered the project differently. Inspired by traditional equity instruments, introducing protective measures would have been a good start. Specific redemption windows (e.g., contracts opening weekly every quarter), regular return distributions, and/or smart-contract-enforced investment locks could have allowed HEC holders to exit at par before the decline. Many had sounded alarms months before the DAO’s eventual dissolution, but due to weak reliability in governance, they were powerless to act.

Low Control, Low Reliability: Aragon

In some cases, governance tokens fail to deliver meaningful control over the underlying project and lack reliability in protecting the rights they purport to grant. A relevant example is Aragon—a project providing legal, technical, and financial infrastructure for DAOs to operate. Several major crypto projects, including Lido, Decentraland, and API3, use its services.

Although the team initially explored multiple use cases for ANT, earlier ideas failed to gain traction, leading them to repurpose ANT as a general governance token. Unfortunately, the vaguely defined governance powers offered little real control to holders, as evidenced by a lack of meaningful proposals and sparse community activity²⁴.

In June 2022, this changed when the Aragon Association and its community passed a proposal to transfer treasury funds to a DAO governed by token holders, scheduled for November 2022. However, the process was repeatedly delayed until the first transfer occurred in May 2023. By then, the treasury was worth approximately $200 million²⁶, and ANT was trading at a discount due to delays and holder frustration.

Declining confidence in the team attracted activist interest, including from Arca (a crypto hedge fund), which began buying tokens below treasury value to accelerate the transition of DAO control, increase transparency, and push for buybacks to restore ANT’s book value.

Instead of allowing token holders to exercise their purported governance rights over the treasury, the Aragon Association suspended further transfers, banned members from the project Discord, and accused activists of orchestrating a 51% attack, claiming holders only had governance rights over Aragon’s on-chain products and protocols.

The next six months were marked by turmoil, culminating on November 2, 2023, when the Aragon Association internally decided to dissolve and distribute treasury funds to token holders. The team did not allow ANT holders to vote on the plan, citing legal reasons, despite prior involvement in treasury transfers. Predictably, many terms were perceived by holders as unfair and team-favoring, leading to ongoing legal disputes.

A governance structure with greater control and reliability from the outset could have mitigated much of this pain—perhaps by granting holders dissolution rights before reaching this point or designing the token similarly to ENS. In the next section, we offer guidance to help project founders and investors avoid negative outcomes in governance design.

Considerations for Builders and Investors

Our governance token framework and accompanying case studies outline the general characteristics we believe define strong governance tokens. However, each token is unique, meaning specific governance functions and parameters should vary by project.

Still, builders universally should aim to create a roadmap that steadily progresses toward a defined end state. This means that if a project team decides to integrate decentralized governance, they should work to make token holders’ rights solid and explicit, ideally protected through strong commitments like legal agreements or smart contracts. Offering vague governance rights and then retracting them is worse than waiting for the right moment to decentralize decisions.

Builders should also determine whether a governance token is necessary at all. As discussed earlier, governance tokens can add value by managing risk or functioning as a form of equity. Regarding risk management, projects must decide whether certain decisions are better made by a decentralized group of token holders rather than a small centralized team. They can then design a governance token that grants holders control over those parameters.

If a governance token does not align with the team’s interests, and if other risks need managing, utility can still be offered without governance. For example, Chainlink’s LINK token does not confer governance rights but plays a vital role in securing the network through staking. LINK is also essential for bootstrapping the Chainlink oracle ecosystem and paying for services.

If there is no risk requiring management by token holders, and depending on jurisdiction and the team’s appetite for regulatory challenges, the path of crypto-equity may still be viable. However, investors considering new governance tokens should clearly understand what they are getting—control over a portion of fees, ability to initiate buybacks, etc.

Regarding control, not all projects should design tokens for profit-driven investors. This may stem from uncertain regulatory environments, alignment with public goods (also seen in nonprofits and public benefit corporations), or other reasons. While these factors reduce the investment appeal of the token, many are justified. Projects taking this path should set appropriate expectations so investors understand exactly what they are investing in.

Conclusion

The design and implementation of crypto governance remain unresolved, yet today many tokens with governance features clearly add value to their respective projects. Encouragingly, there are signs that the market is beginning to price governance tokens more effectively, with many of the worst offenders—including several highlighted in this article—forced to shut down or remediate their failures.

Our governance token evaluation framework aims to advance this trend by offering builders and investors a lens through which to design and invest in tokens—ultimately channeling more value toward projects that establish clear token holder rights (control) and actively protect those rights (reliability).

Finally, we emphasize that regardless of whether a crypto project is new or mature, it is never too late to identify shortcomings and make changes. The industry is still young and capable of rapid transformation—from weak to strong—especially with the help of frameworks like the one described in this article.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News