OKG Research: Is a Massive Bitcoin Sell-Off Coming? Insights from On-Chain Data

TechFlow Selected TechFlow Selected

OKG Research: Is a Massive Bitcoin Sell-Off Coming? Insights from On-Chain Data

Despite Bitcoin's recent underperformance, it has still delivered a positive year-to-date return of over 40%, outpacing the majority of traditional financial market assets.

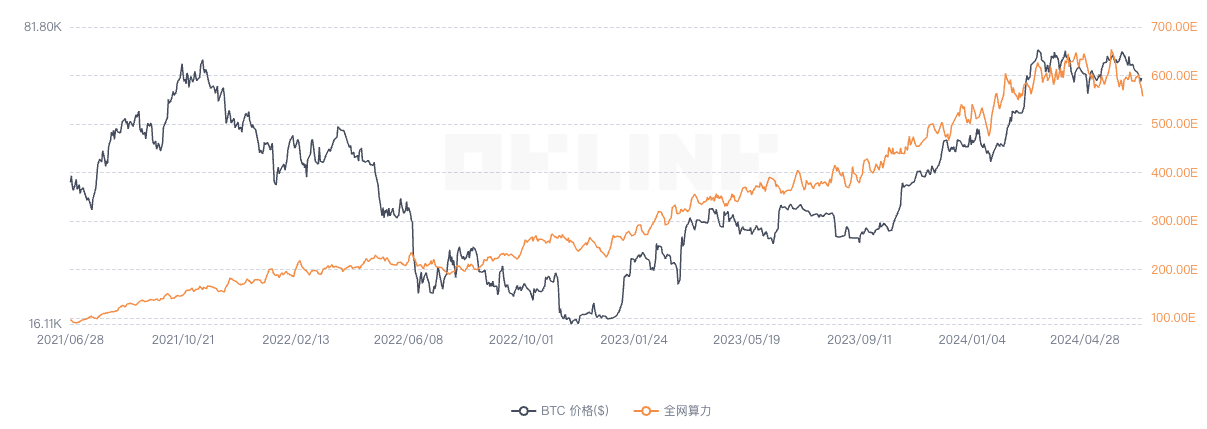

Miners play a crucial role in the Bitcoin network. However, due to the halving event and declining interest in inscriptions and runes—leading to significantly reduced transaction fees—their income situation has become increasingly bleak, with revenue per unit of hashing power hitting record lows. According to OKLink data, over the past two months, Bitcoin's network revenue per unit of hash rate has repeatedly fallen below $0.05. Although there was brief recovery at one point, it has now dropped back to relatively low levels.

As miner revenues deteriorate, many inefficient miners have been forced to exit the market, causing a significant drop in Bitcoin’s total network hashrate. Data from OKLink shows that over the last two months, the global Bitcoin hashrate has declined by 15% from its peak, and has remained in continuous decline over the past week.

At the same time as hashrate declines, miners have recently intensified their selling activity, becoming one of the largest sources of downward pressure on the market. IntoTheBlock data indicates that since the beginning of 2024, Bitcoin miners have collectively sold over 50,000 BTC, and miner-held Bitcoin reserves have gradually dropped to all-time lows. Compared to previous cycles where miners tended to be highly leveraged and long-term holders, today’s miners are more focused on short-term gains—likely due to the ongoing restructuring of mining capacity, with numerous public companies now serving as key drivers behind the industrialization and mainstream adoption of Bitcoin mining.

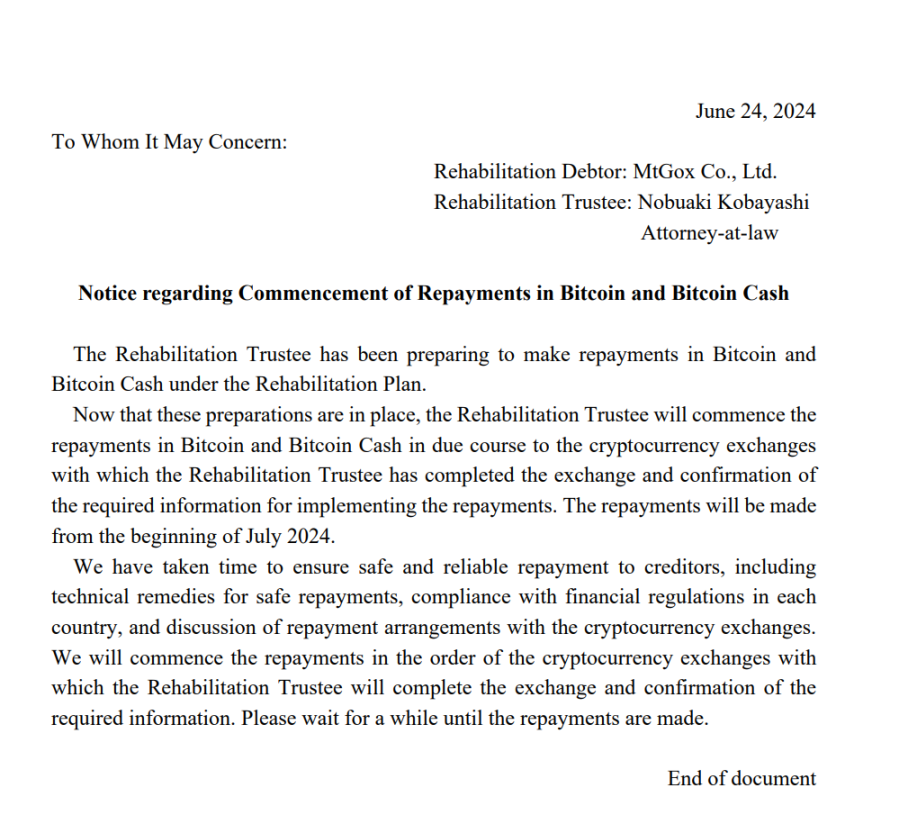

The Mt. Gox trustee’s announced compensation plan on June 24 also brings expectations of substantial selling pressure. While this isn’t the first time Mt. Gox has repaid debts, it is the first instance where repayments will be made directly in BTC and BCH. This means that once distributions begin, a large volume of BTC and BCH could enter the market. However, several analysts believe the actual market impact will be less severe than anticipated—and I agree. The reasons are as follows:

1. The final amount of Bitcoin entering the market through this payout is expected to be far below 140,000; according to Alex Thorn, Head of Research at Galaxy Digital, it may only be around 65,000 BTC;

2. Selling pressure will be dispersed after distribution. Creditors are unlikely to sell simultaneously, and given that markets have already priced in some of the expected Mt. Gox-related selling, the ultimate shock should be limited. More importantly, considering the current market phase, rational creditors may prefer to continue holding rather than immediately liquidating.

Whether it's miner sell-offs or potential pressure from Mt. Gox payouts, we believe the impact on the crypto market will be short-term and limited. Over a decade of experience has shown us that despite various challenges, the Bitcoin ecosystem—anchored by the strongest consensus in crypto—consistently demonstrates remarkable resilience and elasticity. Short-term selling pressure won't alter the long-term trend; if anything, it strengthens the ecosystem’s ability to absorb large-scale outflows.

Compared to short-term selling pressure, what deserves greater attention now is the "bleak" state of on-chain transactions and liquidity in the Bitcoin network.

Despite underwhelming recent performance, Bitcoin has still delivered over 40% positive returns year-to-date—outperforming most traditional financial assets. However, after reaching an all-time high in March, Bitcoin’s network transaction volume (left chart) has steadily declined. One reason is reduced demand due to fading interest in inscriptions and runes. Another is the lack of strong trading incentives for both short-term speculators and long-term investors within the current price range, resulting in persistently low on-chain turnover rates. On-chain active addresses (right chart) have also sharply decreased since March, now numbering fewer than 700,000—over 30% below 2024’s peak and nearly matching levels seen in 2018.

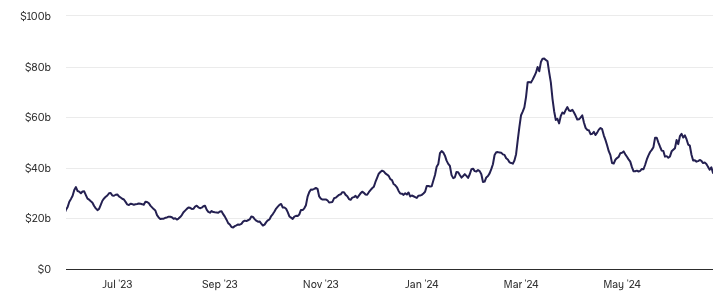

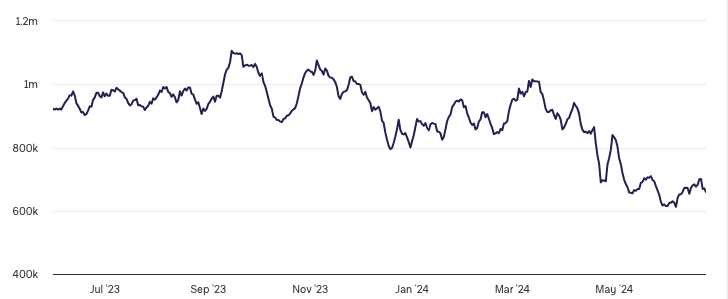

Beyond stagnant on-chain activity, Bitcoin spot ETFs have also shown weak performance recently. As the primary channel for external capital inflows into crypto this cycle, Bitcoin spot ETFs are a critical pillar supporting bullish sentiment. Earlier estimates by JPMorgan suggested that net inflows into the crypto market reached $12 billion this year, with approximately $16 billion flowing into Bitcoin spot ETFs. However, since early June, Bitcoin spot ETFs have experienced multiple days of net outflows. From June 7 to June 25, they have cumulatively lost nearly 20,000 BTC—worth about $1.228 billion at current prices. This performance has disappointed the market. Meanwhile, the quiet handling of seized Bitcoin by governments in Germany and the U.S. has further heightened market anxiety.

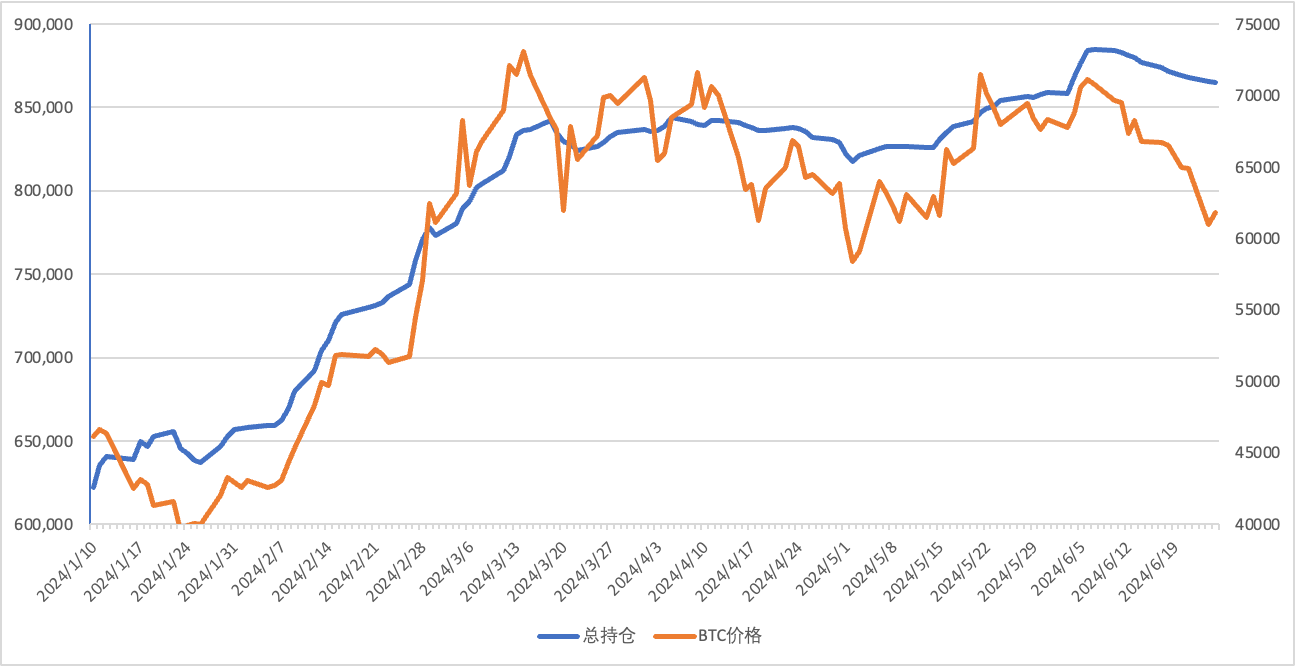

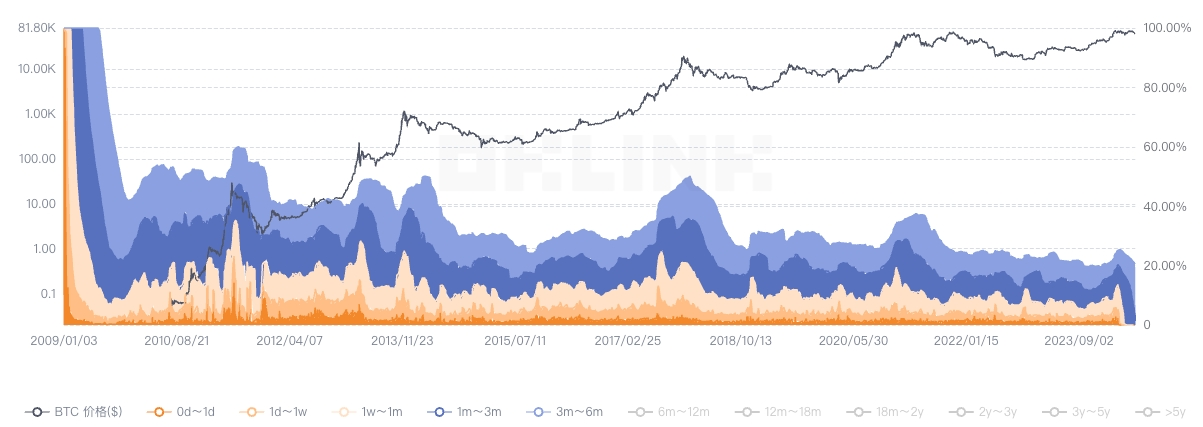

Although these figures may suggest Bitcoin is陷入困境 ("in trouble"), there are also many positive signs in the market. In prior cycles, one key indicator of a true market top was a sharp increase in the proportion of short-term holders (those holding for less than 155 days), often dominating market dynamics. This occurs because long-term holders gradually take profits near peaks, handing control to short-term traders and new entrants. However, according to OKLink data, long-term holders still dominate the current Bitcoin market. Coins held for less than six months account for less than 20%—far below the levels seen near previous cycle tops. This long-term-holder-dominated structure provides solid support at current price levels. Moreover, with nearly 80% of circulating Bitcoin currently in profit, most investors remain in favorable positions—making a broad-scale sell-off unlikely in the near term.

On another front, Bitcoin reserves on exchanges hit a new low in June. While it's a record low, this actually sends a clear signal: real selling pressure remains low. At the same time, low exchange reserves indicate the Bitcoin market is in a rapid accumulation phase—even if we don’t yet fully understand who exactly is moving Bitcoin off exchanges.

Of course, developments surrounding the U.S. Ethereum spot ETF also warrant close attention. Although the correlation between Bitcoin and Ethereum has somewhat decreased, it remains above 0.8—indicating strong mutual influence. If the launch of Ethereum spot ETFs in early July drives ETH to rebound again, Bitcoin may also benefit from renewed upward momentum.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News