Will the launch of Ethereum spot ETFs be bullish or bearish?

TechFlow Selected TechFlow Selected

Will the launch of Ethereum spot ETFs be bullish or bearish?

Regarding the upcoming ETF, market opinions are divided.

By Tuoluo Finance

The market is bleak, but Ethereum has certainly been making headlines.

Positive news continues to emerge around spot Ethereum ETFs. ConsenSys first announced that the SEC has halted its investigation into whether Ethereum is a security. Then came market rumors suggesting that spot Ethereum ETFs could be approved and launched as early as July 2. Adding fuel to the fire, Standard Chartered Bank reportedly plans to build a trading platform for Bitcoin and Ethereum.

Despite these developments, much of the news remains speculative, and the broader market hasn't improved. As Bitcoin briefly dropped below $60,000, Ethereum also fell back under $3,400. However, compared to Ethereum's late-May lows near $2,900 due to weak narratives, and considering the sharper declines in other major altcoins over the past week, the ETF anticipation has clearly provided strong price support for ETH.

At this juncture, the long-awaited spot Ethereum ETF appears imminent. The focus now shifts to how it will perform post-launch—will it trigger a "sell-the-news" selloff, or will institutional capital propel it upward? Market opinions on this are sharply divided.

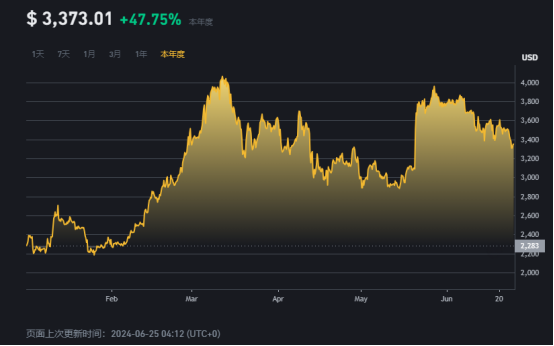

Ethereum’s price trajectory this year can best be described as volatile. In terms of key narratives, it's largely boiled down to two drivers: the Cancun upgrade and speculation around the spot ETF.

On March 13, the Cancun upgrade went live, pushing ETH to a high of $3,981. Since then, prices have swung in tandem with ETF-related developments—sliding when approval seemed unlikely, surging overnight after a dramatic reversal, and subsequently oscillating at higher levels alongside the broader market.

After the “618” selling spree, the crypto market re-entered a cooling-off period. With limited liquidity, prices became highly sensitive to sentiment. Amid recent ETF outflows and fears of Mt. Gox sell-offs, major value coins continued to slide. Yet relative to Bitcoin’s 7.72% weekly drop from $65,000, Ethereum showed greater resilience (-3.18%), demonstrating relatively stronger support. Looking beyond price action, Ethereum has seen several fundamental positives lately.

First, clarity on its non-security status. Last week, ConsenSys announced on social media that the U.S. Securities and Exchange Commission (SEC) had decided to end its 14-month investigation into Ethereum. While litigation between the two parties continues, this development marks a milestone in crypto regulation.

Halting the investigation implies the SEC will not pursue charges claiming ETH sales constitute securities transactions—a point aligned with the approval of Ethereum ETF 19b-4 filings. The implicit meaning of 19b-4 approval is the exclusion of Ethereum’s classification as a security. Prior to this news, there were persistent rumors that the SEC might still challenge Ethereum’s status, especially given the SEC chair’s repeated refusal to comment on Ethereum’s nature—even after ETF approvals.

Secondly, if Ethereum is no longer considered a security, its Proof-of-Stake (PoS) mechanism and staking activities likely fall outside securities regulations. This opens the door for spot Ethereum ETF issuers to potentially include staking functionality. Previously, due to the SEC’s opposition to staking, all applicants removed references to staking from their S-1 filings, raising concerns about ETF competitiveness. For investors, an ETF without staking yields—and with additional management fees—would naturally offer lower returns than simply holding ETH directly. Of course, such critiques often overlook the fact that under current U.S. regulations, large institutions like banks are prohibited from directly purchasing cryptocurrencies.

The second major positive is the approaching ETF launch timeline. While the SEC chair previously indicated a decision would come during summer 2024, the lack of a concrete date kept markets anxious. Recently, however, a clearer timeline has emerged. On June 21, Bloomberg ETF analyst Eric Balchunas announced on social media that Ethereum spot ETF issuers are expected to submit revised S-1 forms later that day. Following this, the SEC will notify issuers of final amendments and effectiveness, with the ETFs projected to go live on July 2. Given Balchunas’ accurate predictions on Bitcoin ETF listings and the Ethereum ETF reversal, this date carries significant credibility.

Additionally, Standard Chartered publicly stated it is building a trading platform for Bitcoin and Ethereum. If confirmed, this would expand access and lower investor entry barriers. However, traditional institutions face substantial challenges in launching trading operations, particularly regarding regulatory feasibility and infrastructure readiness.

Despite these accumulating positives, actual price performance remains underwhelming. As the ETF launch nears, market sentiment is deeply divided.

In terms of market scale, Bitcoin ETFs provide a compelling benchmark. According to Farside Investors, BTC-related products have attracted $14 billion in net inflows since January, managing over $50 billion in assets under management (AUM). But Ethereum ETFs face more skepticism.

Most analysts estimate Ethereum will capture only 15–20% of Bitcoin’s ETF share. JPMorgan analysts project Ethereum ETFs will attract just $1–3 billion in net inflows by late 2024. Mechanism Capital co-founder Andrew Kang shares a similar view, having published a detailed analysis on the potential market impact of a spot Ethereum ETF.

He argues that after removing hedging trades and spot rotations, real net inflows into Bitcoin ETFs amount to roughly $5 billion. Based on Eric Balchunas’ estimate that ETH flows may reach 10% of BTC’s volume, true net buying in the first six months post-approval could be around $500 million, optimistically reaching $1.5 billion.

He emphasizes that Ethereum is far less appealing than Bitcoin to traditional institutional investors such as pension funds, endowments, and sovereign wealth funds. First, institutional holdings of Ethereum are significantly smaller than those of Bitcoin. Before ETF approval, CME Ethereum futures represented only 0.3% of total supply, versus 0.6% for Bitcoin. Moreover, ETH has already rallied fourfold from its lows ahead of ETF approval, while BTC rose only 2.75 times, suggesting limited upside potential. Second, quantitatively, Ethereum performs poorly: its 30-day annualized revenue stands at $1.5 billion, with a price-to-earnings ratio as high as 300x—negative when adjusted for inflation.

A more practical issue is that, due to the unexpected timing of approval, issuers haven’t had time to persuade ETH holders to convert their holdings into ETF shares. Additionally, choosing the ETF means forgoing staking yield—the opportunity cost of not staking ETH. Andrew predicts ETH will trade between $3,000 and $3,800 before ETF launch, but drop to $2,400–$3,000 afterward. If BTC reaches $100,000 by Q4 2025 or Q1 2026, it could drag down Ethereum and altcoins, further lowering the ETH/BTC ratio, which he expects to range between 0.035 and 0.06 over the next year.

For every bearish take, though, there’s a bullish counter.

In response to Andrew Kang’s analysis, Degentrading pushed back, arguing Ethereum could hit $6,000 by September. He notes that in conversations with traditional finance professionals, enthusiasm for ETH—and even SOL—often exceeds that for BTC. Although Ethereum’s market cap is about one-third of Bitcoin’s, its liquidity is only around 10% of BTC’s. This means inflows of $3–4 billion could significantly move ETH prices. Furthermore, Grayscale’s existing ETH trust provides structural support, reducing downside pressure compared to Bitcoin. Deribit Insights recently added a bullish signal: premiums on ETH September $4,000 call options have exceeded $12 million, indicating rising medium-term optimism.

Regardless of external debates, ETF issuers have already begun a fee war. Last week, multiple spot Ethereum ETF providers submitted revised S-1 filings. To capture market share, most set fees below those of Bitcoin ETFs. VanEck disclosed a rate as low as 0.20%, closely matching Franklin’s 0.19%. Under this competitive pressure, firms like BlackRock are likely forced to keep fees under 30 basis points.

Previously, Cathie Wood’s Ark Investment Management exited the Ethereum ETF race, citing unprofitability. She noted that Bitcoin spot ETFs generated no profit for her firm due to extremely low investor fees—just 0.21%. While comparable to other Bitcoin ETFs, this remains far below fees charged by non-crypto ETFs.

In this context, enabling staking could enhance Ethereum ETF competitiveness. Though no issuer has yet revised their stance to support staking, profitability pressures may eventually force changes. However, if staking is implemented, issuers may run their own validator nodes for security and efficiency—potentially diluting market share from other Ethereum ecosystem projects.

Returning to Ethereum itself, as the largest application platform in crypto, ETH’s price reflects the overall health of the crypto ecosystem. Yet in recent years, as app and ecosystem growth has stalled, Ethereum’s hype cycles have increasingly revolved around upgrades. Beyond staking-driven activity, its role has become largely symbolic—as a flagship asset among major cryptocurrencies.

Compared to Bitcoin’s clear value proposition, Ethereum occupies a more ambiguous position in institutional eyes. It’s seen both as a blue-chip tech stock in the blockchain world—the undisputed leader—and simultaneously as a more replaceable investment product. Its value retention lags behind Bitcoin, sometimes falling without recovery, and its upside often trails major U.S. equities. Especially amid limited application innovation today, Ethereum’s ecosystem growth has slowed, meme cycles rotate faster, and claims of Solana overtaking Ethereum surface regularly.

While debate rages over whether Ethereum is a better investment than Bitcoin, no one disputes its foundational status and network effects. This is precisely why the Ethereum ETF draws such intense attention: capital flowing into Ethereum via staking can ripple through to altcoin markets, whereas Bitcoin-based capital typically does not.

Across various price forecasts, high volatility following ETF approval seems inevitable. A “sell-the-news” reaction followed by short-term weakness and long-term strength aligns with prevailing market expectations. Even before official approval, speculative trading in ecosystem tokens has already begun—perhaps another way to profit from the cycle.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News