NYDIG: Cryptocurrency Regulatory Shifts and Ethereum ETF Predictions

TechFlow Selected TechFlow Selected

NYDIG: Cryptocurrency Regulatory Shifts and Ethereum ETF Predictions

In the future, macro events could become market drivers.

By Greg Cipolaro

Translated by Kate, Mars Finance

In this issue:

-

We review what may be the two most important weeks for regulation and legislation in the digital asset industry.

-

The U.S. Securities and Exchange Commission (SEC) abruptly shifted its stance, approving eight spot Ethereum ETFs for trading. We examine the implications and potential timing.

-

If ETH ETFs prove as popular proportionally as BTC ETFs, one could anticipate around $4.5 billion in inflows to the complex; however, the lackluster performance of ETH futures ETFs serves as a cautionary tale.

A pivotal moment for crypto policy and regulation

It has been a momentous fortnight for cryptocurrency regulation in the United States—perhaps the most significant period in its history. A rapid sequence of events unfolded, each seemingly positive for the broader crypto ecosystem, marking a sudden shift in policy ahead of the 2024 presidential election. Below, we unpack each development and its impact on the industry.

Senate votes to repeal SAB 121 (5/16)

Staff Accounting Bulletin 121 (SAB 121) is an accounting rule issued by the U.S. Securities and Exchange Commission (SEC), effective April 11, 2022, which contains prescriptive guidance on how public companies (or their subsidiaries) should account for custodial responsibilities. In essence, it requires such entities—including banks, exchanges, custodians, and any other fiduciaries safeguarding crypto assets on behalf of others—to record these assets on their balance sheets (as both assets and liabilities). The primary concern, especially for publicly traded banks, is capital charges, which affect capital adequacy and leverage ratios, making banks reluctant to hold crypto assets. While the House had already voted to repeal the rule, the Senate’s decision—supported by 12 Democrats—sent a strong political signal. The White House has since issued a strongly worded statement indicating the President will veto the bill, which he must do by next Tuesday. However, given the abrupt shift in political climate, the administration's final stance remains uncertain.

FDIC Chair steps down (5/18)

On Monday, May 18, embattled FDIC Chair Martin Gruenberg announced he would resign once his successor is appointed. He had faced mounting scrutiny following widespread allegations of sexual harassment and misconduct within the agency. While this departure is unrelated to the FDIC’s crypto policies, under Gruenberg’s leadership, the agency’s stance was decidedly unsupportive. A joint statement from the FDIC, OCC, and Federal Reserve after the FTX collapse stands out—warning banks that issuing or holding digital assets “is likely inconsistent with safe and sound banking practices.” While the impact of leadership change on the agency’s position toward crypto remains unclear, one thing is certain—there is room for improvement from the current state.

Trump begins accepting crypto donations (5/21)

Notably, presidential candidate Donald Trump’s shift in attitude toward crypto aligns with the current administration’s sudden openness. On May 8, Trump hosted a dinner at Mar-a-Lago for buyers of his NFT trading cards. Although not a crypto enthusiast during his presidency, reports indicate he actively courted support from the crypto community during the event. Then on May 21, Trump’s campaign began accepting cryptocurrency donations—the first major-party candidate to do so.

House passes FIT 21 Act (5/22)

The Financial Innovation and Technology for the 21st Century Act (FIT 21) is a market structure reform bill introduced by the House Agriculture Committee (notably, also passed by the Financial Services Committee). It lays the groundwork for a federal regulatory framework for the crypto industry, fulfilling a long-standing industry demand. Crucially, it would classify most cryptocurrencies as commodities, placing them under CFTC rather than SEC oversight. On Wednesday, it passed the House with bipartisan support, including 70 Democrats—about three times the Democratic backing received for the SAB 121 repeal. However, just before the vote, SEC Chair Gensler released a statement expressing opposition to the bill. That morning, the White House issued a statement on the bill that was markedly more cooperative compared to its earlier stance on repealing SAB 121. While the bill still needs Senate approval to become law, this White House statement marks a stark contrast to its previous crypto-related positions—and diverges sharply from the SEC Chair’s comments.

SEC approves spot ETH ETFs (5/23)

On Thursday afternoon, the SEC approved amendments to Form 19b-4 filings, allowing exchanges to list and trade eight spot Ethereum ETFs, making ETH the second cryptocurrency to receive SEC approval for an ETF. This reinforces the SEC’s view that ether is a commodity, not a security. However, trading cannot begin immediately, as the SEC typically requires about 30 days to review and approve registration statements. The launch of spot Bitcoin ETFs was exceptional—trading began the next day—because the SEC had already engaged in extensive consultations with issuers. In this case, however, the SEC has not held a single meeting with any issuer.

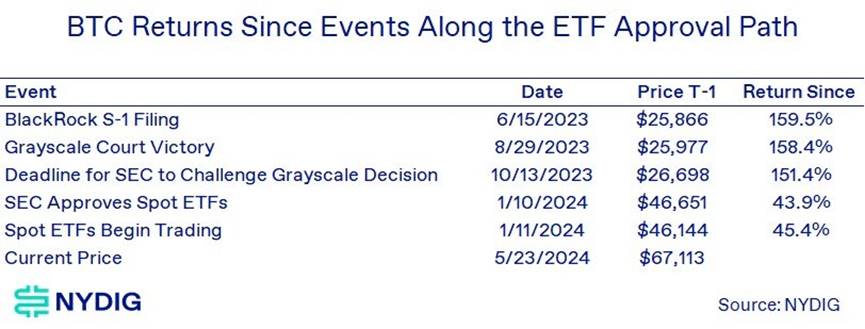

The SEC’s approval marks a sudden reversal in stance—one that many of us, including ourselves, did not foresee just a week earlier. Notably, the SEC commissioners did not vote on this matter, as they did for Bitcoin ETFs; instead, the Division of Trading and Markets approved the 19b-4 filings. Still, such action likely wouldn’t have occurred without commissioner-level support. Our understanding is that things shifted abruptly on Monday (May 20), possibly in response to the changing regulatory and legislative landscape outlined above. Prior to this, the SEC had maintained a hostile posture toward crypto, only permitting spot Bitcoin ETFs after losing in court. Right up to the May 23 deadline for spot Ethereum ETF approval, there were no signs the agency was inclined to approve—especially since it had held zero meetings with potential issuers, whereas it had conducted 24 such meetings ahead of Bitcoin ETF approvals. Consensys, the Ethereum development firm, even sued the regulator, alleging the SEC was preparing to classify ether, Ethereum’s native asset, as a security—which would have effectively killed any hope for a 33 Act ETF.

When will the ETFs start trading?

There is no fixed timeline for when the SEC deems registration statements effective, but the Division of Corporation Finance typically takes around 30 days to review filings. We may see meetings between issuers and the SEC (followed by amended submissions) as issuers refine their documents. Contentious issues like in-kind creation/redemption and staking appear unlikely to delay launches, at least initially. Our expectation is that, similar to spot Bitcoin ETFs, the SEC will remain neutral and allow all approved funds to begin trading simultaneously. All top players from the Bitcoin ETF race have returned for this new round, except WisdomTree and Valkyrie. WisdomTree manages the smallest spot Bitcoin ETF, while Valkyrie was recently acquired.

However, a key strategic shift is Grayscale’s decision to push forward its Grayscale Ethereum Mini Trust (ticker: ETH)—a (proposed) lower-cost alternative to the Grayscale Ethereum Trust (ticker: ETHE)—by filing a 19b-4 (though not part of the SEC’s initial approval). Our interpretation is that Grayscale aims to avoid a repeat of the spot Bitcoin ETF launch, where high fees on GBTC drove capital to competitors. However, the Grayscale Ethereum Mini Trust has not yet entered the formal SEC review process, so its launch timing is unclear. We also don’t yet know the fees for ETH or ETHE—the current fee for ETHE is 2.5%. We expect spot ETH ETF fees to fall within the range of Bitcoin ETFs, i.e., 20–30 basis points, with fee waivers based on AUM and tenure.

How big can Ethereum ETFs get?

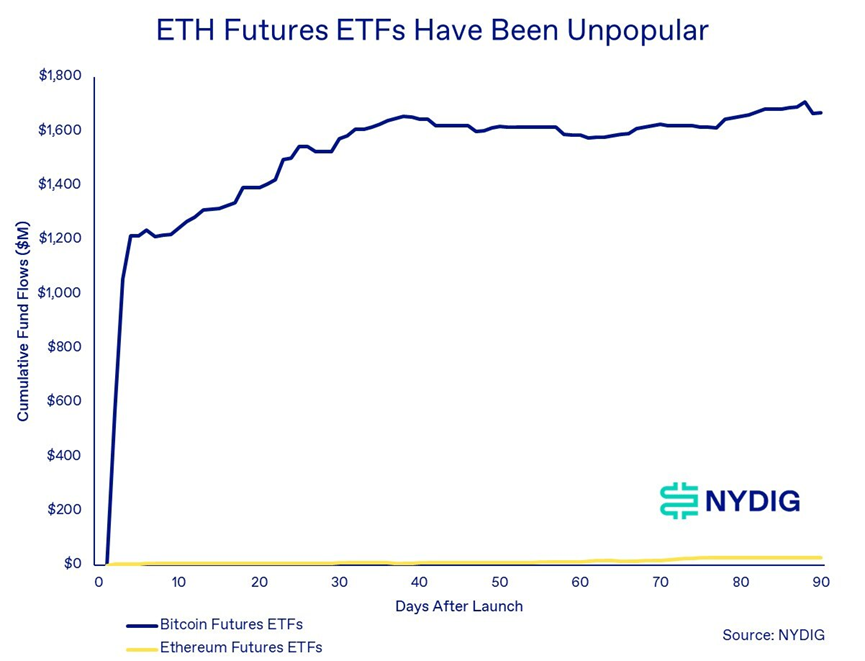

While predicting adoption is always challenging (the popularity of spot Bitcoin ETFs certainly exceeded our initial expectations), we now have some benchmarks from both spot and futures Bitcoin ETFs. Yet, some comparisons are misleading. For example, ETH futures ETFs launched last October have been extremely unpopular compared to BITO, the Bitcoin futures ETF, gathering less than 2% of the inflows in the first 90 days. This may largely reflect timing—the BITO launch coincided with the peak of the prior cycle, while ETH futures ETFs launched during a Bitcoin-dominant phase (which continues today).

It’s also possible investors value ETH for its utility—as the native currency of a platform for building and creating—rather than purely as a monetary or investment asset. Locking it into an ETF might contradict this utility-driven vision. A definitive difference is Bitcoin’s fixed supply versus ether’s uncapped issuance, encouraging different user behaviors—holding versus active use. Years ago, the Ethereum community attempted to frame Ethereum as “ultrasound money,” missing the point of Ethereum’s strength—its flexibility and functionality—instead trying to position it as a better version of Bitcoin (an argument that swayed few hard-money advocates).

With that in mind, using the spot Bitcoin ETF launch as a guide, we can make some assumptions about potential ETH ETF demand. Applying a similar ratio of initial inflows to market cap, we estimate potential inflows into ETH ETFs at around $4.5 billion—approximately one-third of Bitcoin ETF inflows (and a similar market cap proportion).

As for price impact, Bitcoin’s historical trajectory offers an important blueprint. However, it’s worth noting that Ethereum ETFs have skipped many of the procedural hurdles Bitcoin had to overcome before approval. The ultimate impact will depend on actual ETF inflows, and given the tepid reception of ETH futures ETFs compared to Bitcoin’s, results could vary significantly.

Will other digital asset ETFs follow?

Now that the question of ETH ETF approval has passed, the natural next question is: what other cryptocurrencies might see ETFs? The reality is, no other crypto has regulated derivatives trading on CME like BTC and ETH. Therefore, satisfying the SEC’s requirements around market surveillance and anti-fraud/anti-manipulation measures may pose a greater burden on applicants. The SEC has already claimed in various lawsuits that many other cryptos—such as SOL, ATOM, MATIC, ADA, FIL, and ICP—are securities. While no final rulings have upheld these claims, the SEC is unlikely to approve ETFs for such assets. More realistically, we may see a pause in new ETF applications as regulators, lawmakers, and the White House absorb the recent wave of changes.

Market dynamics

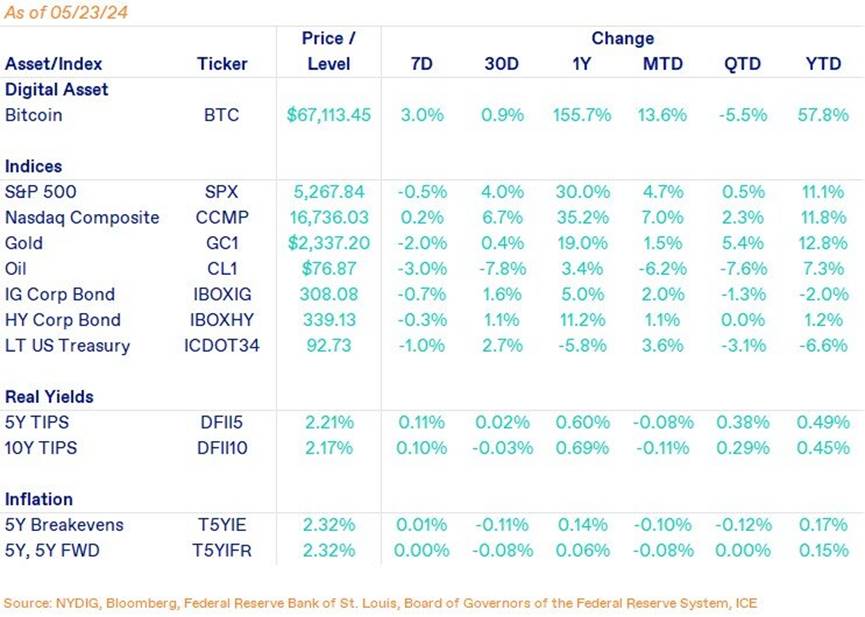

Bitcoin rose 3.0% this week, though not without turbulence. As the SEC prepared to approve ETH ETFs on Monday, Bitcoin appeared poised to reach a new all-time high. However, a rotation from Bitcoin into Ethereum beginning Tuesday, along with higher-than-expected PMI (inflation) data on Thursday, derailed that momentum. On Thursday, risk markets—including equities and crypto—reversed sharply, with Bitcoin experiencing particularly volatile swings by the 4 p.m. close. The cause of the late-day volatility remains unclear, as GBTC saw only minor outflows and total inflows across the spot ETF complex reached $108 million. The ETHBTC cross pair was especially volatile, dropping 5.7% before rebounding.

Looking ahead, if Thursday’s price action is any indication, macro-related events may become key market drivers, at least in the near term. The launch of spot ETH ETFs, tentatively expected in about a month, could influence demand for Bitcoin ETFs. While new capital may enter the ecosystem—especially given the improved regulatory backdrop—some flows into ETH ETFs may come at the expense of BTC ETFs, despite their fundamentally different investment theses.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News