Web3 Project Token Issuance Compliance Guide: Decentralization Is Key

TechFlow Selected TechFlow Selected

Web3 Project Token Issuance Compliance Guide: Decentralization Is Key

This article will explain why decentralization is important, how decentralization creates compliance room, and provide some compliance strategies, from the perspective of Web3 legal practitioners and based on a series of articles by a16z about decentralization and token issuance.

Authored by: Will Wang, investment and financing lawyer, crypto researcher;

Chris Chu, crypto lawyer, former senior product manager at an exchange, on-chain data researcher

The ultimate goal of most Web3 projects is to issue their own tokens, especially during bullish crypto market cycles when rising token prices fuel FOMO sentiment. However, the path toward this pursuit of "freedom" is fraught with obstacles—sudden alerts from unknown dark forests, harsh crackdowns by regulators, or even prison sentences.

How to legally and compliantly launch a token is paramount for any Web3 project—but this is far from the endgame. True decentralization is the ultimate objective. Achieving it not only enables sustainable development but also creates greater compliance flexibility for the project.

Therefore, drawing insights from the perspective of Web3 legal practitioners and a series of articles by a16z on decentralization and token issuance, this article explains why decentralization matters, how it expands compliance opportunities, and offers practical compliance strategies—ultimately aiming to provide a preliminary compliance framework for Web3 token launches.

I. Why Pursue Decentralization?

Web1 was once hailed as the greatest tool for liberation, until Web2 platforms gradually transformed the internet into an engine of centralization. The relationship between network participants and platforms shifted from collaboration to competition; collective consensus online gave way to the singular narrative of centralized platforms. What was once a digital utopia became a digital prison—until the dawn of decentralized crypto networks.

Thus, the term "decentralization" has acquired almost panacea-like significance. Whether it's the non-violent resistance against government surveillance proposed in the Cypherpunk Manifesto, the order established through Code is Law among programmers, or political advocacy for digital libertarianism—these ideals are meaningful, yet they are not the primary reason decentralization is so crucial for Web3 projects.

(A Cypherpunk's Manifesto)

Crypto networks are decentralized systems built atop the internet. They use consensus mechanisms like blockchain to maintain and update network states (collective consensus in Web3 vs. single-platform control in Web2), while employing cryptocurrencies to incentivize shared ownership, co-creation, and joint development among participants (non-profit, no ownership in Web1 vs. ownership and incentives in Web3).

Decentralization is a defining feature of crypto networks—it shifts power from closed corporate entities in Web2 to open, permissionless networks. A truly decentralized crypto network resembles public infrastructure (public goods) rather than proprietary technology requiring strict licensing.

This shift toward openness and decentralization has the potential to rebuild the internet in ways that foster competition, safeguard freedom, protect privacy, and fairly reward contributors. Under the right conditions, it can attract global participation and enable exponential growth of the ecosystem. This shared consensus is one of the key reasons assets like Bitcoin and Ethereum continue to thrive despite skepticism.

In short, decentralization returns data ownership, governance rights, and other powers that rightfully belong to network participants back to individuals (Ownership), empowering them to collectively work toward common goals—the growth of the network ecosystem and enhancement of token utility.

II. How Decentralization Creates Compliance Space

Decentralization not only fosters collective alignment, enables global collaboration, and drives ecosystem flywheels—it also opens up legal compliance opportunities. We’ll examine how decentralization benefits Web3 projects from two angles: the SEC’s regulatory rationale and a comparison between decentralized ICOs and centralized IPOs.

2.1 The SEC’s Regulatory Rationale

The biggest “adversary” in the crypto industry is undoubtedly the U.S. Securities and Exchange Commission (SEC). The SEC maintains that nearly all tokens are “securities” and must be registered under U.S. securities laws. Since the 2017 ICO boom, tens of thousands of projects—including Ethereum—raised funds based on promises of technological breakthroughs, yet few actually delivered on those commitments.

The SEC seeks to apply securities law to such fundraising activities because ICOs often meet all criteria of the Howey Test for securities: an investment of money in a common enterprise with a reasonable expectation of profits derived from the efforts of others.

The clearest example is primary-market token sales (i.e., issuers selling tokens directly to investors), which are typically deemed securities offerings.

In the SEC v. Ripple case involving private placements in the primary market, even sales to institutional investors were considered securities under the SEC’s definition: (1) investment of money; (2) a common enterprise—Ripple used investor funds to operate its network, making investor returns dependent on Ripple’s progress; (3) expectation of profit derived from the efforts of others—investors expected gains via Ripple’s development efforts, including interest, income, or appreciation in investment value (the Increased Value of the Investment).

Indeed, Ripple publicly promoted XRP investments as potentially profitable and explicitly linked XRP’s value to Ripple’s own efforts.

(Understanding the SEC v. Ripple Case: Clarifying the Regulatory Fog)

Despite these positions, the fundamental goals of the SEC and crypto participants align: eliminating information asymmetry and creating a fair, transparent competitive environment.

The responsibility of Web3 network participants is to demonstrate that decentralized networks are viable and capable of meeting regulatory expectations—such as enabling a level playing field for broader stakeholders (developers, investors, users), using transparent ledgers, removing centralized control, and reducing reliance on management teams.

2.2 Centralized IPO vs. Decentralized ICO

Let us first compare a traditional centralized company going public via IPO with a decentralized project launching via ICO, then analyze how crypto networks may satisfy regulatory requirements.

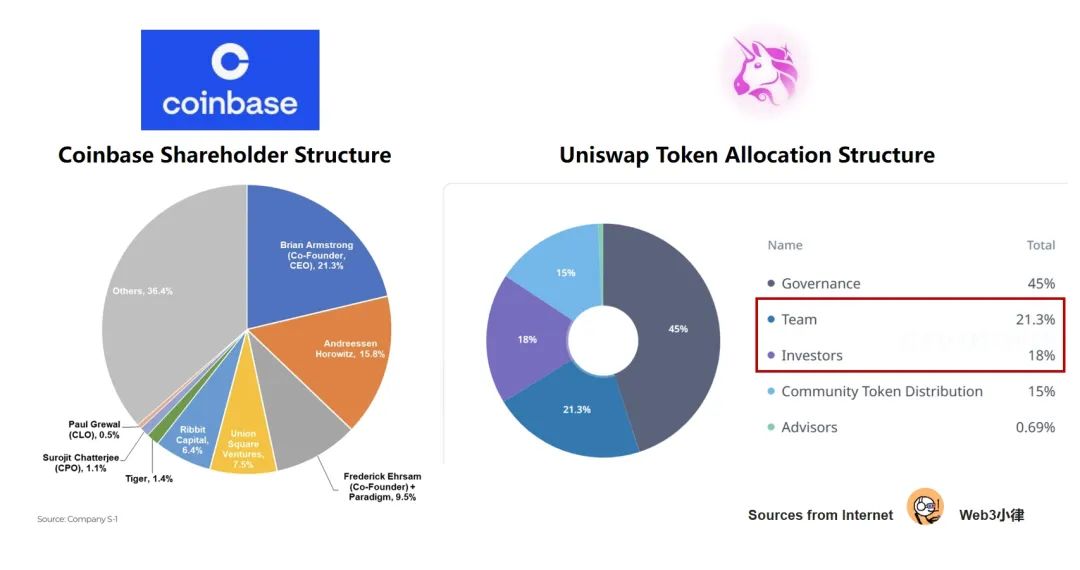

The essence of an IPO is issuing equity stakes to raise capital, primarily benefiting a small group of shareholders.

As shown in Coinbase’s IPO shareholding structure above, founders and early investors held at least 70% of shares. The stock price fluctuations had no direct benefit to users who traded daily on Coinbase. To put it bluntly: you trade constantly on Coinbase, contributing to its revenue—what do you get in return?

By contrast, the essence of an ICO is distributing the majority of tokens publicly (via fundraising, airdrops, etc.), shifting control from a centralized team to the entire community, thereby achieving decentralization and driving ecosystem growth.

Web3 development teams or management usually retain only a small portion of tokens; the vast majority are allocated for ecosystem building and rewarding early contributors, DApp users, and other network participants. As illustrated above, Uniswap’s team and investors kept only a small fraction, while 60% of tokens were reserved for ecosystem development and governance. More concretely: we can earn token rewards by providing liquidity, trading activity, or receiving grants for contributing to the ecosystem.

Clarifying that the purpose of token issuance is to achieve decentralization is critical for Web3 projects. Otherwise, projects fall into the predatory “insider dumping” logic and cannot sustain long-term success.

2.3 How Decentralization Expands Compliance Space

From the standpoint of token decentralization, applying the SEC’s Howey Test becomes significantly more difficult: (1) Investment of money—airdrops or similar methods don’t involve monetary investment; (2) Efforts of others—truly decentralized projects do not rely on managerial efforts; (3) Profit expectations—secondary market investors don’t necessarily depend on core team efforts for returns.

Moreover, decentralization helps fulfill one of the SEC’s core objectives: disclosure. When control is distributed across the community rather than concentrated in a management team, information can reach everyone equally.

In June 2018, SEC official William Hinman introduced the concept of “Sufficient Decentralization,” stating: “If a token or its underlying network is sufficiently decentralized—so that investors no longer expect a person (or group) to undertake essential managerial or entrepreneurial efforts—then the asset is not an investment contract.” Based on this reasoning, Hinman concluded that Ethereum does not constitute a securities offering because its network is sufficiently decentralized.

This underscores the importance of decentralization in U.S. regulation.

(Variant Fund, Sufficient Decentralization: A Playbook for Web3 Builders and Lawyers)

III. Token Launch Compliance Guide

3.1 Degree of Centralization Determines Compliance Risk

While decentralization creates compliance room, the SEC issued an updated “Framework for Digital Asset Issuance” in April 2019 and continues expanding its jurisdiction over crypto through enforcement actions (e.g., against Coinbase, Binance, Ripple, Uniswap).

Regardless, to minimize exposure to SEC scrutiny, Web3 projects should operate within the guidance provided by the SEC to mitigate risks.

Likewise, in any jurisdiction, before listing tokens on exchanges (IEO), projects typically require legal opinions from law firms certifying the token as “non-security” to avoid local securities regulations.

Clearly, the level of compliance risk a project faces depends heavily on its degree of decentralization. Fully decentralized Bitcoin remains the only crypto asset explicitly excluded from SEC securities classification, while Ethereum’s status is still being tested.

On this point, Miles Jennings, Head of Policy & Legal Compliance at a16z, stated clearly: “Decentralization is the only path available to eliminate the risks that securities laws aim to address. It is the North Star guiding projects forward—other strategies are merely temporary fixes.”

Of course, few projects can achieve full decentralization immediately. Most Web3 initiatives require a process of “progressive decentralization.”

3.2 Exclude All U.S. Factors

Most projects lack full decentralization at launch, meaning their tokens could theoretically be classified as securities by the SEC. For instance, in SEC lawsuits against Binance and Coinbase, dozens of listed tokens were labeled as securities. Additionally, public token distribution itself may be seen as a securities offering.

Therefore, a direct way to avoid U.S. regulation (especially the SEC) is to eliminate all U.S. connections—removing grounds for jurisdiction.

Similarly, this approach applies to China’s jurisdiction as well.

Hence, whether during private fundraising, token generation event (TGE), or secondary market trading, projects should avoid any U.S. factors (e.g., U.S. citizens, U.S. investors).

Practical steps include:

A. Early airdrop/incentive phase: Geo-block or block VPN access for U.S. users to prevent participation in airdrops, incentives, or public token sales;

B. Private sale phase: If issuing tokens privately to U.S. investors or employees, Web3 projects may still rely on exemptions under SEC Regulation S;

C. Public launch/trading: Issue tokens through non-U.S. entities and initially refrain from listing on U.S.-based platforms like Coinbase, Gemini, or Kraken.

In practice, most offshore foundations (e.g., Cayman Islands, BVI, Singapore) serve as issuing entities. If a token is decentralized, a nonprofit foundation governs distributed project rights. As an entity without shareholders, the foundation avoids conflicts of interest and focuses solely on ecosystem development.

In essence, if a project does not offer its token to Americans, even without “sufficient decentralization,” the risk of SEC enforcement drops dramatically. Therefore, avoid any public token sale aimed at fundraising targeting U.S. persons.

3.3 Operational Restrictions for Projects

Although the above strategies help address regulatory concerns around token fundraising (e.g., excluding U.S. factors), most Web3 projects inherently target global audiences and operate online. Thus, project teams must observe certain operational restrictions—particularly when discussing token value (on Discord, Twitter, Telegram, emails, etc.)—to avoid regulatory pitfalls. These include:

1. Protocol development

2. Business development

3. Marketing curation

4. Intellectual property

5. Governance decisions

3.3.1 Transitioning Project Identity Toward Decentralization

(Variant Fund, Sufficient Decentralization: A Playbook for Web3 Builders and Lawyers)

Before and after token launch, Web3 project teams entering the decentralization phase should avoid several pitfalls:

A. Before public sale, avoid discussing or referencing the value of your token, including potential airdrops, token allocations, or tokenomics. The SEC previously halted Telegram’s token launch due to such conduct;

B. At all times, avoid discussing token price or potential appreciation, or framing the token as an investment opportunity. This includes mentioning mechanisms expected to increase value (e.g., programmed token “burns” for price stability) or pledging continued funding via private capital;

C. After token launch and during decentralization, founding teams, management (including founders, dev companies, foundations, DAOs) should redefine their roles.

Web3 teams should refer to themselves as the “initial development team” instead of “core development team,” use “core contributor/contributor” instead of corporate titles. Foundation and DAO members should define themselves as nonprofit contributors advancing protocol/DApp/DAO growth.

Project teams easily fall into centralized language—even when highly decentralized—especially when habitually speaking in first-person about achievements, milestones, or announcements. Common traps include:

-

Avoid implying ownership or control over the protocol/DApp/DAO (e.g., “As CEO of the protocol…” or “Today, we launched X feature…”);

-

Avoid promising or guaranteeing ongoing work, or suggesting such work carries outsized importance to the ecosystem;

-

Avoid highlighting personal efforts to promote further decentralization;

-

Provide independent voices for the project’s DAO or foundation to prevent confusion. Better yet: distinguish the project’s development arm (e.g., Ondo Finance vs. Ondo Foundation, Uniswap Labs vs. Uniswap DAO), or ensure they don’t share naming with the protocol;

-

Ultimately, all communications should reflect decentralization principles, especially in public settings. Communication must be open and designed to prevent significant information asymmetry among individuals or groups.

Identity transformation is critical—remember: words have consequences, and you’re no longer the CEO holding all the power.

3.3.2 Public Access to Information

Beyond daily operations, Web3 teams should proactively disclose project progress and operations—this fulfills the SEC’s demand for transparency. Use accessible public channels: Notion pages, Discord channels, governance forums, weekly summary meetings, etc.

In decentralized crypto networks, code is open-source. Success lies not in hoarding secrets, but in execution. Withholding “confidential” information unfairly disadvantages investors and strengthens the perception of the token as a security.

3.3.3 Token Lock-Up Period

Additionally, Miles Jennings recommends extending token lock-up periods—at minimum, one year post-TGE. The SEC has previously blocked token launches by pointing to the absence of a one-year lock-up. This practice reduces legal compliance risks, mitigates downward price pressure from early selling, and signals confidence in the project’s long-term viability.

Once decentralized, no individual or company speaks for the project. The ecosystem becomes its own independent and unique entity.

IV. Exemplary Models of Decentralized Projects

There is no universally accepted standard for measuring full decentralization, but we can draw guidance from relatively compliant Western projects.

Uniswap, the most successful decentralized exchange, offers valuable lessons—especially given its operation in the sensitive domain of cryptocurrency trading under opaque U.S. regulation. Financial technology compliance is paramount.

We’ve mapped out Uniswap Labs’ compliance journey after spinning off the protocol—a model of regulatory-friendly decentralization. This separation aims both for progressive decentralization and greater regulatory flexibility.

A. Decentralized, Non-Security Token

The Uniswap protocol runs autonomously on-chain and is governed by Uniswap DAO, achieving decentralization. Its single-purpose UNI token serves as a governance token. This model avoids SEC securities classification and has received favorable judicial recognition.

B. DAO Legal Wrapper – Limited Liability for Members

Uniswap DAO established the Uniswap Foundation as a legal entity—analogous to a legal wrapper—protecting members’ limited liability and enabling interaction with the Web2 world to expand influence.

C. Independent Labs – Flexible Frontend Development

Uniswap Labs, the original developer and maintainer, operates as a separate legal entity and transitions into a major contributor. Freed from protocol constraints, it builds and maintains frontend products via backend protocol calls—ensuring sustainability, as seen with the monetized version of the Uniswap DApp.

D. Regulate Applications, Not Protocols

As advocated by a16z, decentralized on-chain protocols are just code—difficult to regulate. However, frontend applications developed by Labs can fully comply with regulations, shielding teams and products from regulatory risk. Like any app, frontends can implement KYC/AML/CTF checks, delist tokens flagged by regulators, or obtain required licenses.

Although on April 10, 2024, Uniswap Labs received a Wells Notice from the SEC indicating possible enforcement action, this relates more to the nature of its crypto trading business than to flaws in its decentralized legal architecture.

V. Regulatory Barriers in China’s Jurisdiction

The compliance strategies discussed above summarize best practices from leading projects, particularly in relatively open jurisdictions like the U.S. In contrast, China prohibits all crypto-related activities, making token issuance extremely risky.

Yet the essence of regulation in both jurisdictions is similar. Imagine earning shiny gold through gray-area tactics in a gray zone—and someone with enforcement authority sees it. The U.S. emphasizes rule of law and uses legal procedures, while China takes a blanket ban approach.

Therefore, projects should avoid any provable grounds for enforcement.

5.1 Criminal Risks During Token Issuance

While decentralization defines Web3, the real people behind projects—the operators and actual controllers of on-chain addresses—are subject to legal oversight. Project teams must avoid crossing China’s legal red lines during token issuance. Often, teams lure users with promises of high returns, promote projects publicly via Twitter, Telegram, or offline partnerships with grassroots teams targeting unspecified individuals—this model easily constitutes the crime of illegal public deposit-taking.

Founding teams may raise massive funds quickly via token sales. Without proper financial oversight or transparent fund usage disclosures, raised capital may be misused—for luxury cars, real estate, or personal crypto speculation—leading to irreversible losses and constituting the crime of fundraising fraud.

Furthermore, to accelerate user growth, projects often collaborate with KOLs and marketing teams, promoting hardware purchases or cloud computing power for returns, using referral-based multilevel commissions. This model easily constitutes organizing or leading pyramid schemes.

Reference: Understanding Criminal Risks for Project Teams Through the ‘Xirtam’ Incident

5.2 Guard Against Profit-Driven Enforcement Harm to Web3 Projects

Currently, some financially strained local governments engage in aggressive, profit-driven enforcement against Web3 projects. Tech firms collaborate with police to identify leads, resulting in arrests of domestic project executives and key personnel holding private keys. Authorities forcibly transfer seized project tokens or other cryptocurrencies to law enforcement-controlled wallets for disposal and liquidation.

Ideally, confiscated assets should go entirely to state coffers. But in practice, some regions partially or fully refund forfeiture proceeds to investigative agencies as办案经费 (case-handling funds), allowing cooperating tech firms to receive service fees.

This poses a systemic threat to Web3 business models.

Such enforcement causes panic and insecurity among community members. Disposal of assets via secondary markets triggers sharp token price swings. Regardless of final legal determinations, the project’s future becomes untenable. Ultimately, developers, loyal users, and investors bear the cost.

Thus, Web3 project teams must protect investors and ecosystem participants from profit-driven enforcement by relocating core product, technical staff, and multisig wallet managers overseas. Implement multisig controls over treasury addresses to eliminate single points of failure and safeguard user assets.

VI. Final Thoughts

The above framework provides a preliminary compliance roadmap for Web3 token launches. Different projects will face additional compliance considerations—data compliance for DePIN or DeAI, financial regulations for RWA or payment projects—which are beyond this scope. Always consult your own legal counsel before launching. Not Your Lawyer. Do Your Own Research.

This framework aims to empower Web3 teams to confidently explore token economics, ecosystem development, and decentralization—without bearing undue risks associated with token ownership.

Not every project will fit this model. Achieving decentralization takes time, and compliance comes at a cost. Project teams must develop thoughtful, deliberate playbooks for decentralized operations.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News