Comparative Analysis of Farcaster/FT/UXLINK/Cyber: How to Find the North Star Metric for SocialFi?

TechFlow Selected TechFlow Selected

Comparative Analysis of Farcaster/FT/UXLINK/Cyber: How to Find the North Star Metric for SocialFi?

From the perspective of social network structure, Farcaster and UXLINK have relatively stronger social attributes, enabling the entire economy to maintain sufficient resilience.

Authors: Sirius & Joe

Social products have always been a highly controversial domain, whether in traditional internet or on-chain environments, with ongoing debates surrounding social applications. As Marx famously said, "the human essence is the sum total of all social relations." Abstracting the underlying logic of social products, we arrive at this principle: the core of any social product lies in helping users establish certain social relationships, generate interactions, exchange information, and expand their social networks within the application—achieving these goals constitutes a successful social product.

Therefore, based on different forms of social networks, countless well-known products have emerged in the traditional internet space—Facebook, WeChat, Soul, and others—each constructing social networks tailored to various social scenarios such as friends, strangers, or campus communities. These represent the conventional internet's approach to social products.

For Web3 social products, characteristics like financialized asset issuance add a "Fi" dimension beyond just social networking. How to issue assets based on social networks, or how to build social networks through assets, lies at the heart of Web3 SocialFi projects. Additionally, the decentralized, censorship-resistant liberal ideology imposes higher demands on content moderation for project teams, making the SocialFi sector one of the most challenging categories among all Web3 products to develop successfully.

In this article, we will analyze several relatively well-developed SocialFi products in the market—Farcaster, FriendTech, UXLINK, and CyberConnect—and explore the growth trajectories of SocialFi products.

From user addresses to asset value: How do we define genuine growth in SocialFi?

As previously mentioned, the core of SocialFi lies in the integration of social networks and assets. Whether issuing assets based on social networks or building social networks via assets—that is the fundamental logic of SocialFi products. Next, we will first dissect the aforementioned products from two perspectives—social network structure and asset issuance—before comparing them across multiple dimensions using selected metrics.

Social Network Structure

Farcaster’s social network topology mirrors Twitter’s—both are attention-based and relatively open networks. FriendTech refines and intensifies Twitter’s model into a closed, node-centric network. While Farcaster and FriendTech inherit Twitter’s attention-driven online social architecture, UXLINK emphasizes real-world social networks by bringing real-life connections onto the blockchain. CyberConnect, by contrast, forms social networks based on on-chain activities.

Asset Issuance Layer

Farcaster positions itself as a foundational layer for social interaction, exhibiting relatively weak "Fi" attributes but stronger community culture. Its core community-born asset is $degen. FriendTech v1 pushes asset issuance to the extreme, leveraging bonding curves to create Ponzi-like flywheels, assigning asset bubbles to each KOL’s social network, where value is fully reflected in room key liquidity. UXLINK strikes a more balanced approach with its dual-token model, resulting in a more stable and healthier system capable of sustainably incentivizing users to create value within the network. CyberConnect relies solely on its native token for governance and lacks strong incentives for social network expansion.

After qualitative analysis, we proceed to quantitative evaluation. We begin by selecting basic indicators across social and asset layers. For social attributes, we use protocol active user count; for asset aspects, we use the market cap of the protocol’s core asset.

Social Attributes

-

Active Protocol Addresses

-

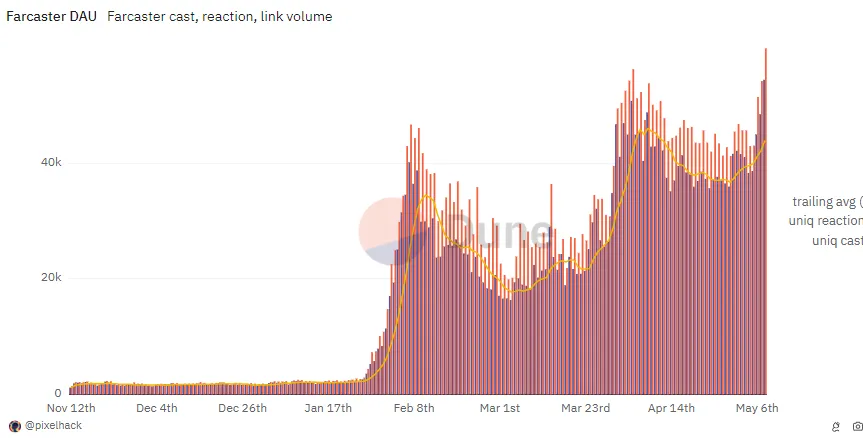

Farcaster’s DAU began rapid growth in February, dipped in March, then surged again with an influx of new users.

-

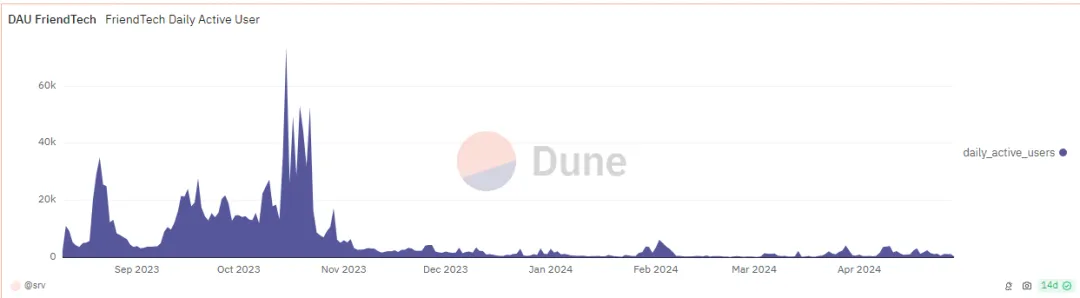

FriendTech

During FriendTech v1, users actively participated to earn points for potential airdrops. From late last year until April this year, delayed token launches eroded user confidence and led to attrition. After the v2 token release, most users chose to abandon the platform.

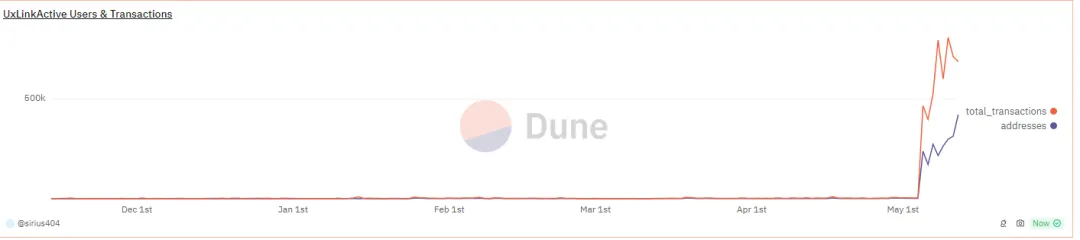

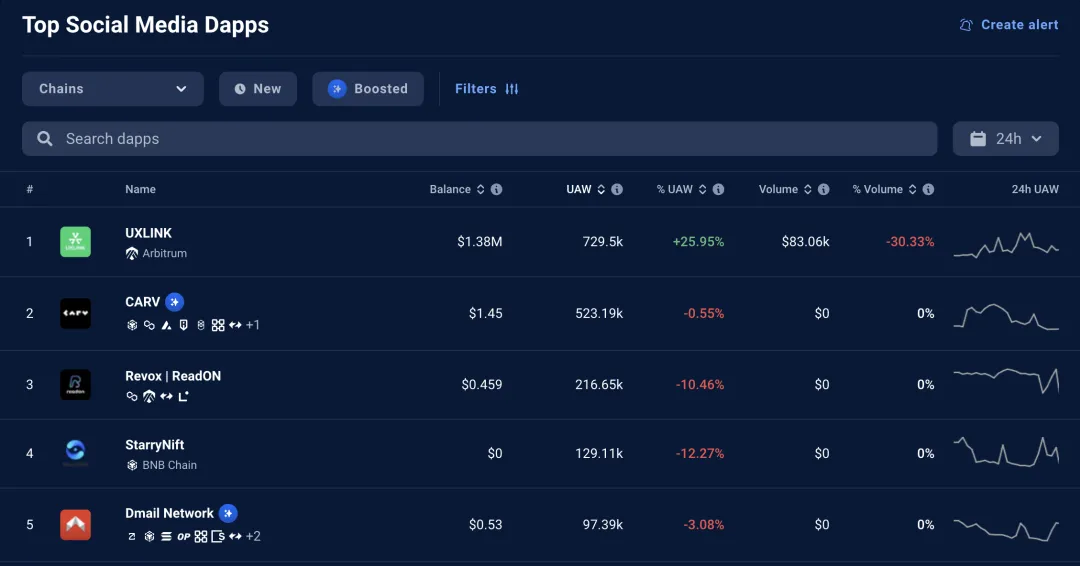

UXLINK has shown astonishing growth this year, reaching nearly 500K addresses in May, quietly amassing a user base several times larger than other protocols.

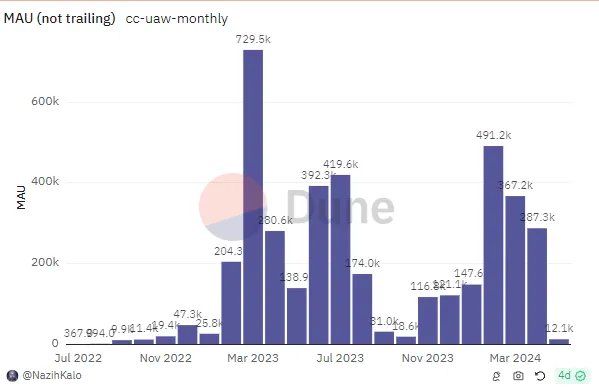

CyberConnect experienced a rebound in user numbers during the first half of this year but has since shown limited momentum.

Overall, UXLINK is undoubtedly the hottest blockchain social infrastructure today, with on-chain activity far surpassing its three main competitors in the SocialFi space. According to UAW (Unique Active Wallets), UXLINK boasts 729.5k active wallets—the highest among all Social Media Dapps.

In comparison, the concurrent UAW of the other three major SocialFi products lags significantly behind UXLINK. Although this metric primarily reflects short-term on-chain activity, it clearly shows that current Web3 social users’ attention is overwhelmingly captured by UXLINK.

Asset Attributes

-

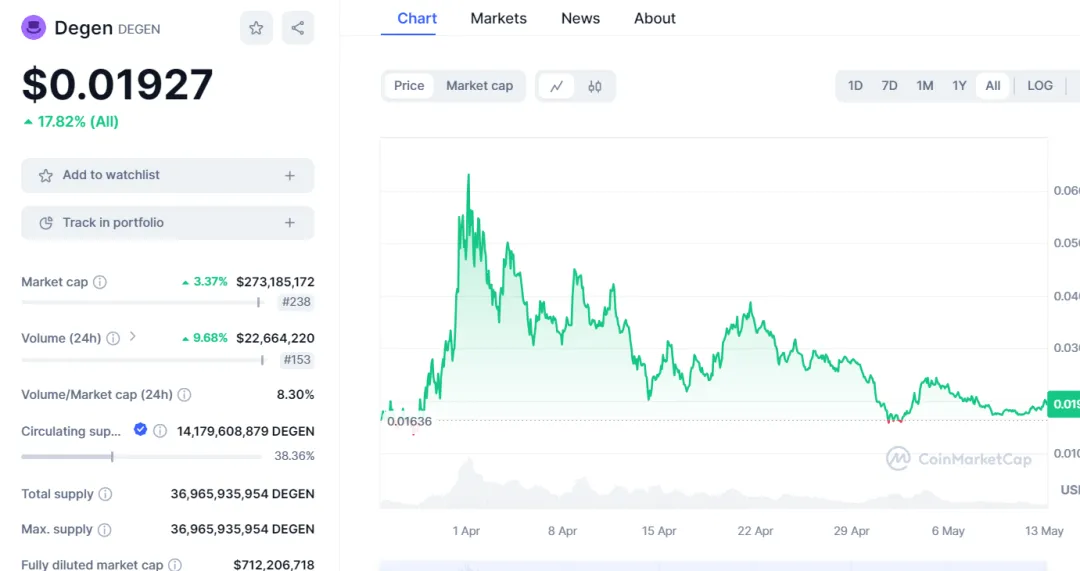

Farcaster has weak intrinsic asset properties; here we use the community-emergent asset $degen as a proxy. Its price spiked in April alongside Base ecosystem hype but has recently declined as the ecosystem cooled down.

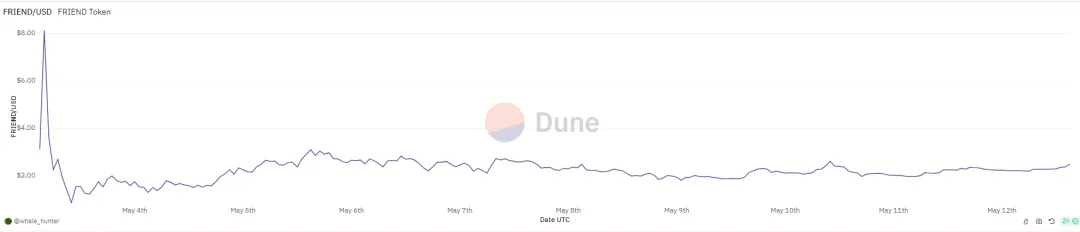

FriendTech launched its token in v2, and after absorbing initial airdrop selling pressure, the token price stabilized.

-

CyberConnect’s token has been live for over two years, rising in price during the first half of the year amid sector speculation, only to fall back to lows afterward.

-

UXLINK has not yet issued a token and is therefore excluded from this comparison.

Overall, UXLINK leads current Web3 SocialFi products in user growth due to its remarkable network expansion rate, while FriendTech attracts profit-seeking users through innovative asset issuance mechanisms.

Beneath the Surface: Strategic Focus and North Star Metrics

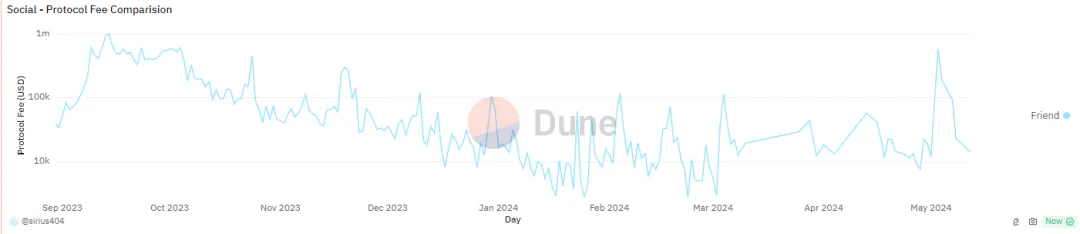

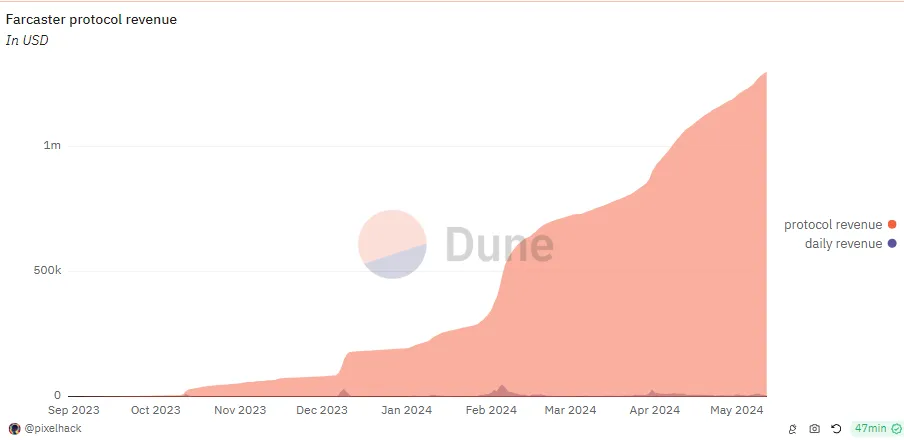

If we abstract user behavior in social products, it can be described as: “users expand their social networks within the product and engage in interactions to exchange information.” With added asset features, this behavior extends to include asset trading alongside information exchange. In SocialFi products, information sharing often occurs hand-in-hand with asset transactions, driving overall economic vitality. The product itself benefits from these economic activities. Therefore, in this article, we select protocol revenue as the North Star metric to evaluate a social product’s success.

-

FriendTech saw peak activity upon launch due to its innovative asset mechanism, followed by declining engagement as interest waned. However, the v2 token airdrop and novel club design reignited热度.

-

Farcaster experienced strong growth this year alongside the Base ecosystem boom, with new user inflows boosting protocol revenue.

-

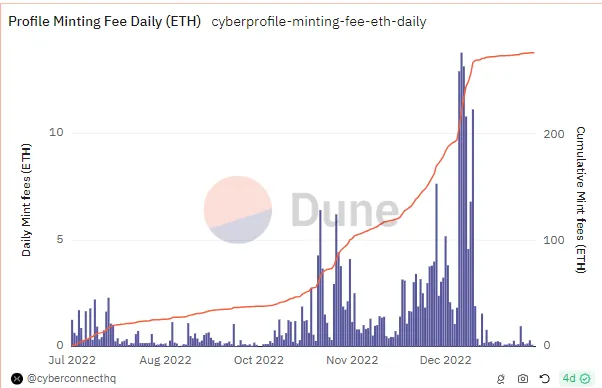

CyberConnect’s revenue dropped nearly to zero after its airdrop, indicating weak genuine social demand among users.

-

UXLINK’s economy is still in early stages, so data is unavailable and not included here.

In SocialFi, if one must choose between "Social" and "Fi," products centered on "Fi" will prevail—after all, in Web3, trading is the fundamental user need.

From Metrics to Product Design: How Should Products Evolve?

We observe that the rise and economic vitality of these representative SocialFi products are strongly tied to asset issuance—a clear indication that for Web3 products, asset issuance is the first principle, and trading represents the base user demand. All SocialFi products should consider how to embed user trading behaviors within their social networks.

For CyberConnect, there is no inherent trading scenario within the product. Early user activity was driven solely by airdrop farming rather than authentic social needs—this explains why its economic activity sharply declined post-airdrop.

For Farcaster, its decentralized front-ends during the “ice age” preserved a flame of revival among freedom-loving users dissatisfied with Twitter’s censorship. Positioned as a hub for the Base ecosystem, it gained traction as Base flourished, becoming a prime destination for high-alpha insights.

For FriendTech, initial airdrop incentives drove social behavior, while v2 enabled influencers to monetize through club creation and token issuance, providing tradable assets to ordinary users and sustaining economic activity. However, trading behavior remains underemphasized, and the Farcaster team appears to be downplaying the "Fi" aspect.

From a token launch perspective, FriendTech and UXLINK offer the most user-friendly designs, most likely to generate wealth effects and attract users. In terms of social network strength, Farcaster and UXLINK exhibit stronger social attributes, enabling greater economic resilience. We can look forward to their future developments, particularly regarding asset issuance built atop real-life social networks.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News