2024 Q1 Crypto Market Venture Capital Report: Project Valuations Remain High, Infrastructure Still a Key Investment Focus

TechFlow Selected TechFlow Selected

2024 Q1 Crypto Market Venture Capital Report: Project Valuations Remain High, Infrastructure Still a Key Investment Focus

Sentiment and activity are improving, but remain far below the levels seen during the previous bull market.

Authors: Alex Thorn, Gabe Parker

Translation: TechFlow

Introduction

Bitcoin and the broader liquid cryptocurrency markets surged in the first quarter of 2024, reigniting optimism across the industry. The crypto venture capital market appears to be rebounding, although data available as of mid-April suggests a slightly more subdued picture than market sentiment might indicate. Overall, founders and investors alike report a more active fundraising environment compared to previous quarters. After three consecutive quarters of declining deal counts and invested capital, both metrics rose in Q1. While the rally in liquid crypto markets can boost sentiment in the venture community, anticipated rate cuts at the beginning of the year now seem less likely. Stubborn inflation data, coupled with generally strong U.S. economic performance, has led Federal Reserve officials to adopt a hawkish stance. As a result, futures markets have scaled back expectations for 2024 rate cuts from seven cuts predicted in January to just one or two. Higher interest rates will continue to challenge venture funds seeking to raise capital, and consequently, startups aiming to secure investments from these funds will also face headwinds.

Deal count increased by over 50% quarter-over-quarter, while invested capital grew by 29%. Categories attracting significant venture attention include Bitcoin Layer 2, re-staking, developer tools, other infrastructure, and gaming. Deal sizes remained flat quarter-over-quarter, but valuations surged nearly 100%, indicating that while capital remains tight, founders were able to leverage improved market sentiment to raise funds with less dilution.

Crypto Market Venture Capital

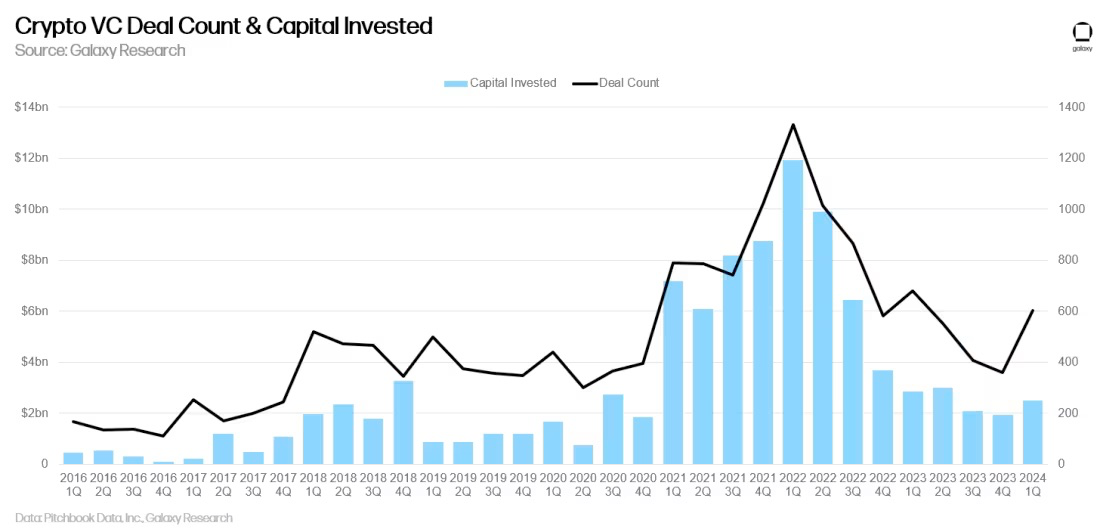

Deal Count and Invested Capital

In the first quarter of 2024, venture investors deployed $2.49 billion into cryptocurrency and blockchain companies (up 29% quarter-over-quarter), across 603 deals (up 68% quarter-over-quarter).

This marks the first increase in both capital invested and deal count in three quarters, perhaps signaling that Q4 2023 was the "bottom," though sustained quarterly growth—and more meaningful increases—will need to be confirmed in the coming quarters.

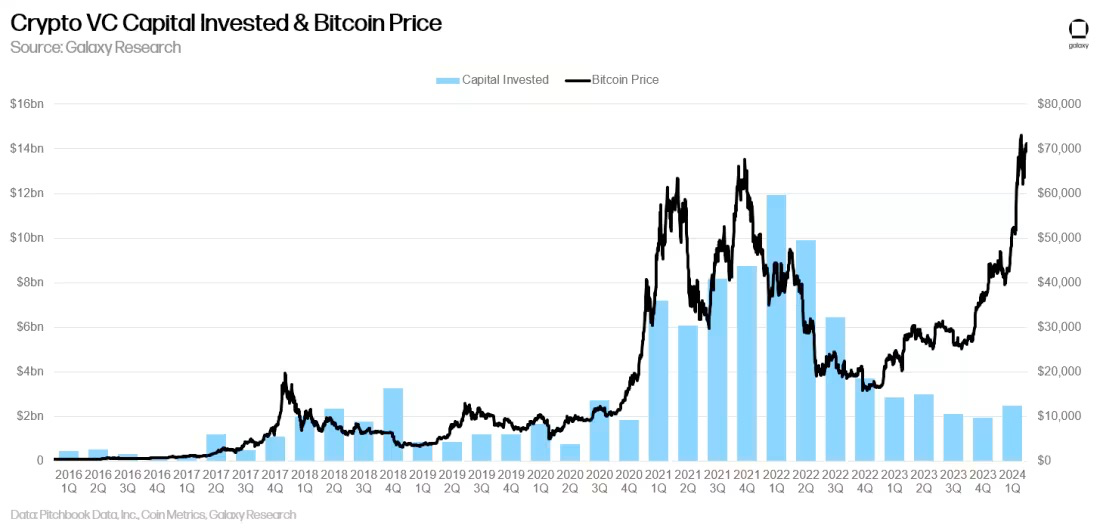

Invested Capital & Bitcoin Price

While venture investment in crypto typically correlates with Bitcoin’s price, this relationship broke down over the past year—Bitcoin rose sharply since January 2023, while venture activity largely stagnated. In Q1 2024, Bitcoin surged again, and invested capital rose as well, yet activity remains far below levels seen when Bitcoin last traded above $60,000. Native catalysts within the crypto sector (Bitcoin ETFs, re-staking, modularity, Bitcoin L2s, etc.) and macro headwinds (interest rates) have combined to create a notable divergence.

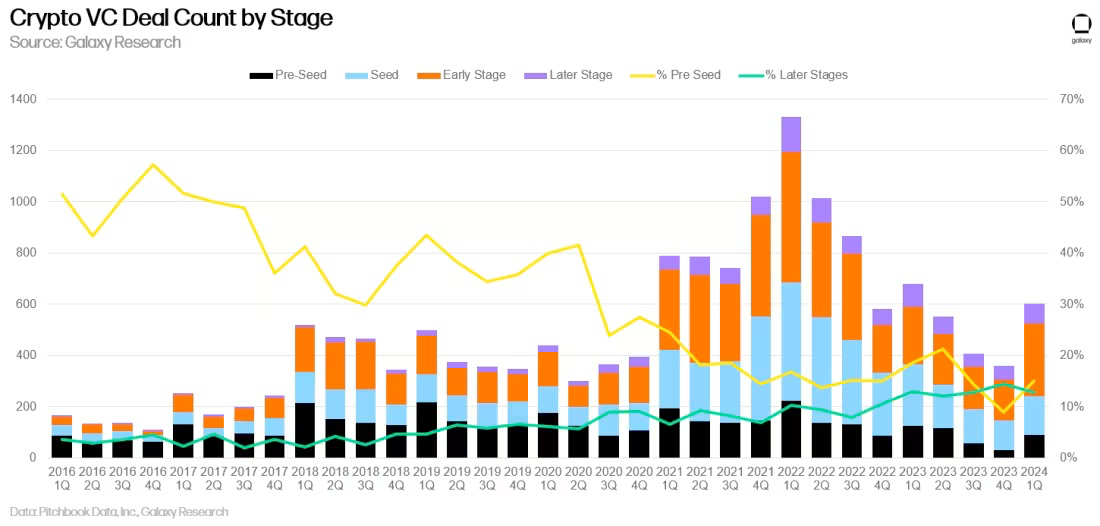

Venture Investment by Stage

In Q1 2024, approximately 80% of capital flowed to early-stage companies, while 20% went to later-stage ventures. Early-stage crypto-focused venture funds remain active, and many are still operating on capital raised during 2021 and 2022, enabling compelling early-stage startups to secure funding. However, many large generalist venture firms have either exited the space or significantly reduced their exposure, making it harder for later-stage startups to raise capital.

On the deal front, pre-seed rounds saw a slight increase in share, suggesting a rise in newly formed startups.

Valuations and Deal Sizes

Throughout 2023, valuations for venture-backed crypto companies declined sharply, reaching the lowest median pre-money valuation since Q4 2020 in the final quarter. However, despite median deal sizes remaining stable quarter-over-quarter, valuations rebounded in Q1 2024. Data suggests founders were able to raise similar amounts of capital as in Q4 2023 but with lower dilution. In contrast, the broader venture ecosystem saw the opposite trend—median deal sizes dropped by 50% quarter-over-quarter while median pre-money valuations held steady, indicating founders had to sell more equity to raise the same amount. The rise in valuations may stem from heightened market sentiment in Q1—despite limited new capital, founders leveraged improved sentiment to secure higher valuations.

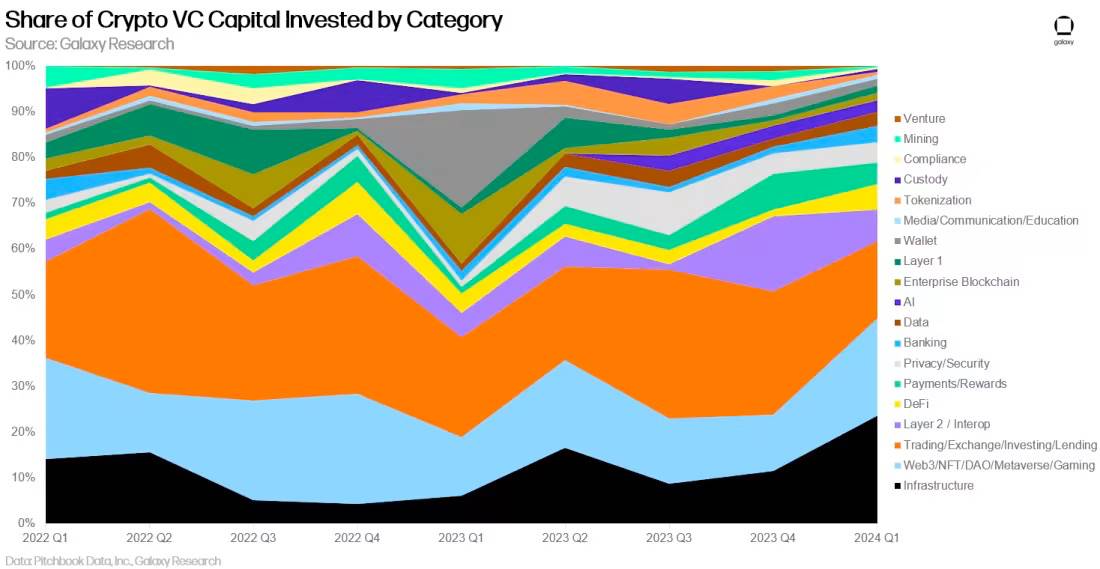

Investment by Category

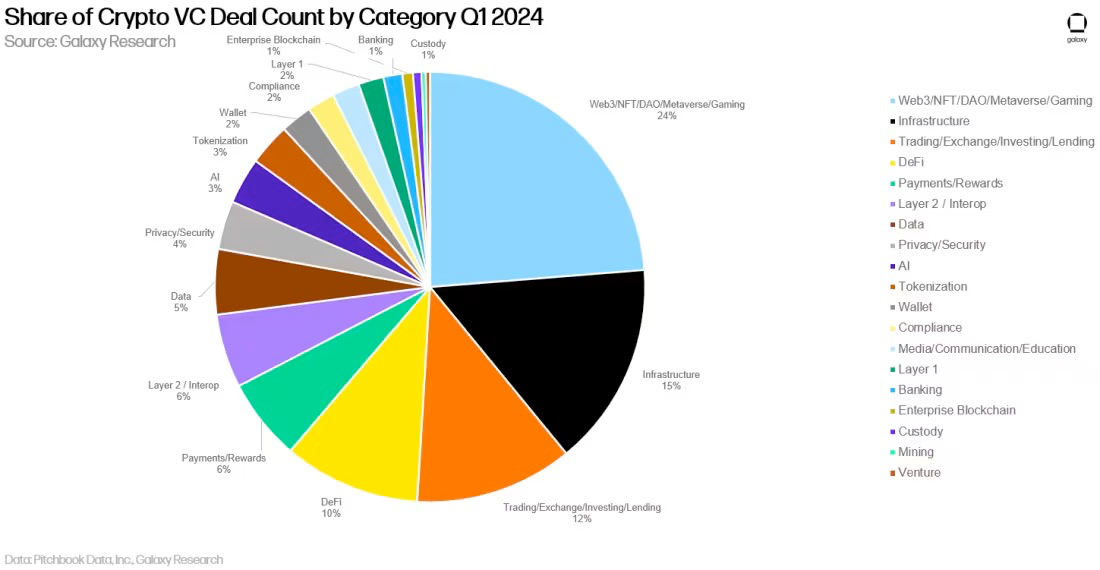

In Q1 2024, companies and projects categorized under “Infrastructure” raised the largest share of crypto venture capital (24%), led by EigenLayer’s $100 million round.

Web3 and Trading followed closely, accounting for 21% and 17% of invested capital, respectively.

In terms of deal count, Web3 led with a 24% share, driven primarily by an increase in gaming-related deals.

Infrastructure and Trading followed, representing 15% and 12% of all deals completed in Q1 2024, respectively.

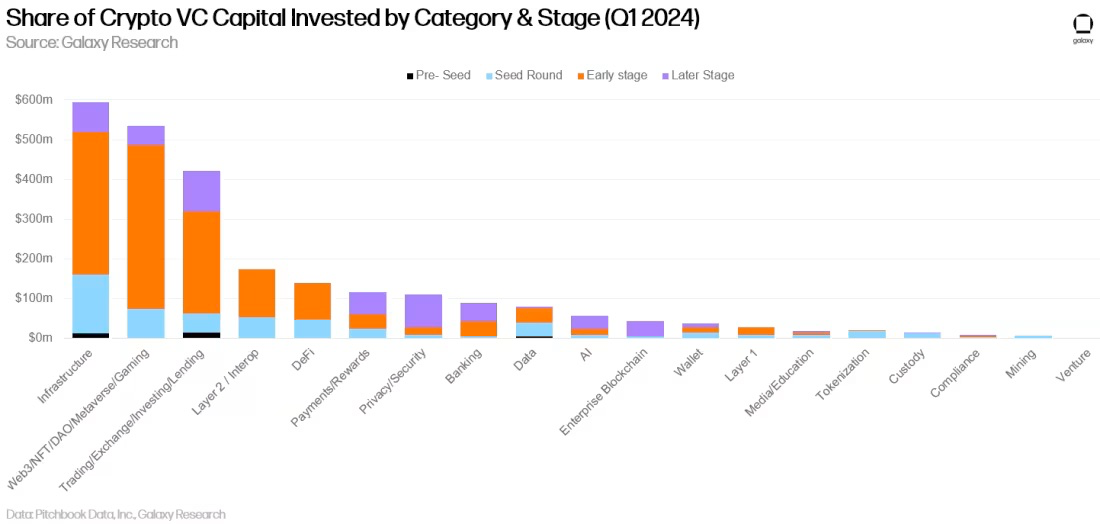

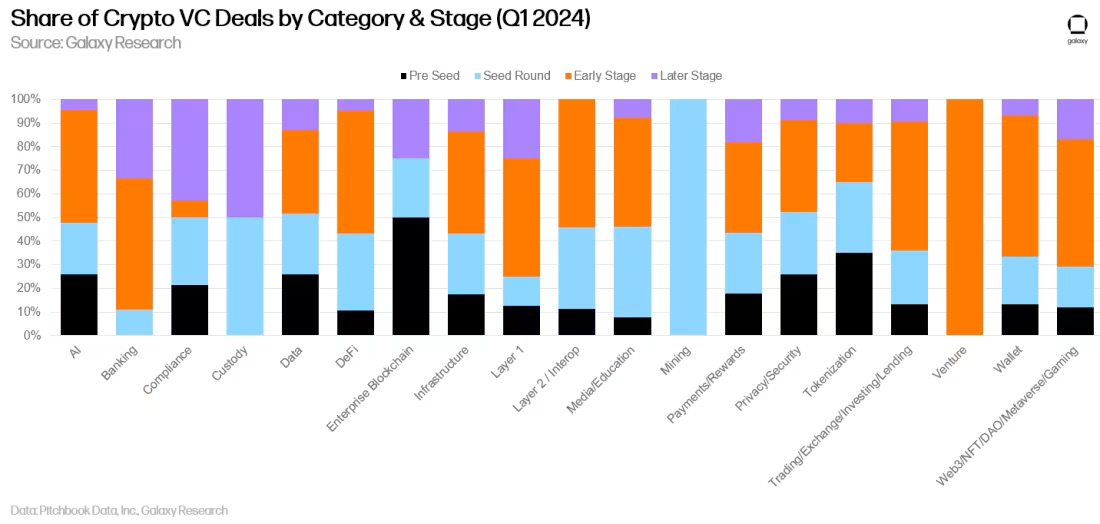

Investment by Stage and Category

Breaking down invested capital and deal count by category and stage provides clearer insight into which types of companies are raising funds within each category. The vast majority of capital in Infrastructure, Web3, and Trading flowed to early-stage companies and projects.

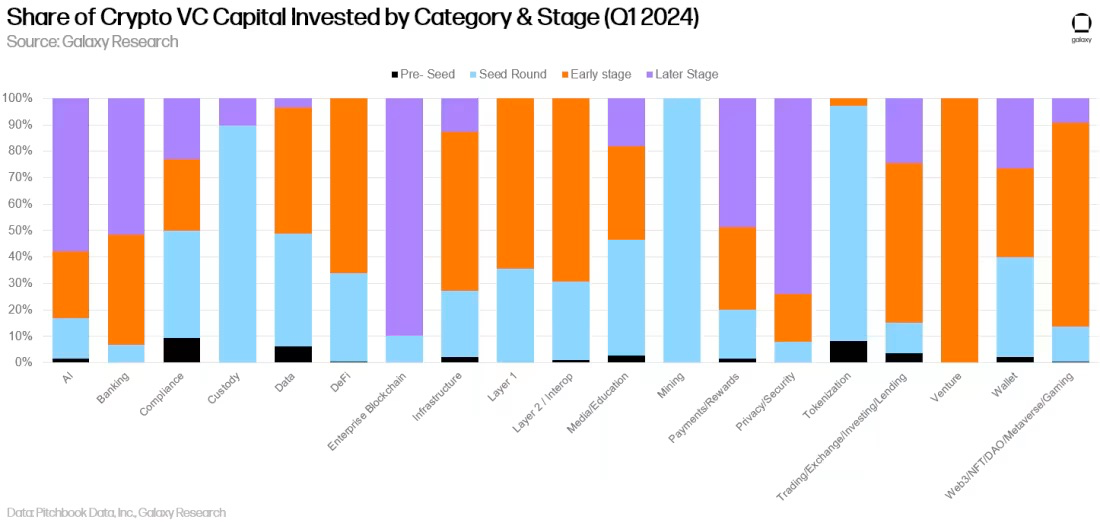

Examining the share of capital by investment stage within each category offers insight into how mature each investable category appears to investors.

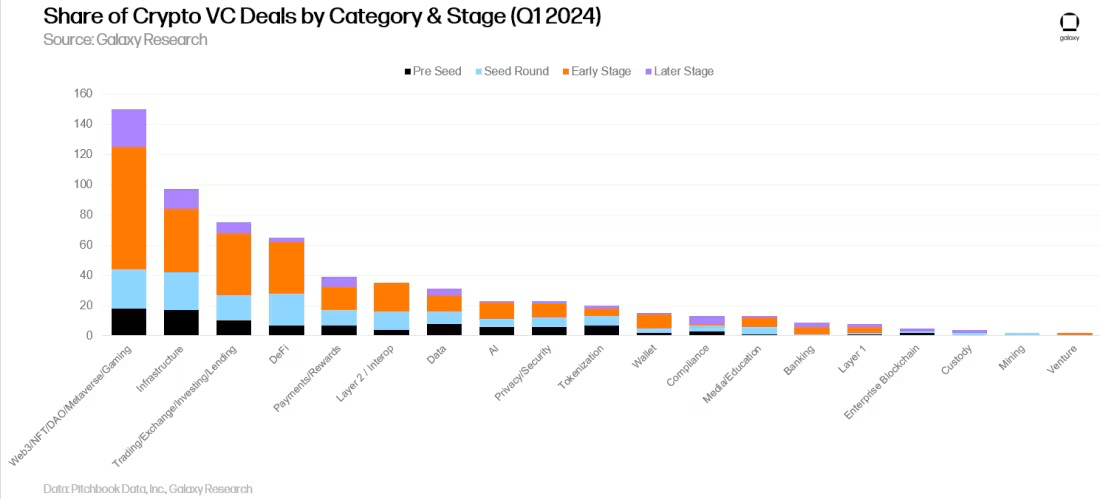

Deal count tells a similar story. The majority of deals completed across nearly all categories involved early-stage companies and projects.

Analyzing the share of deals completed by stage within each category provides deeper understanding of the development stage across investable categories.

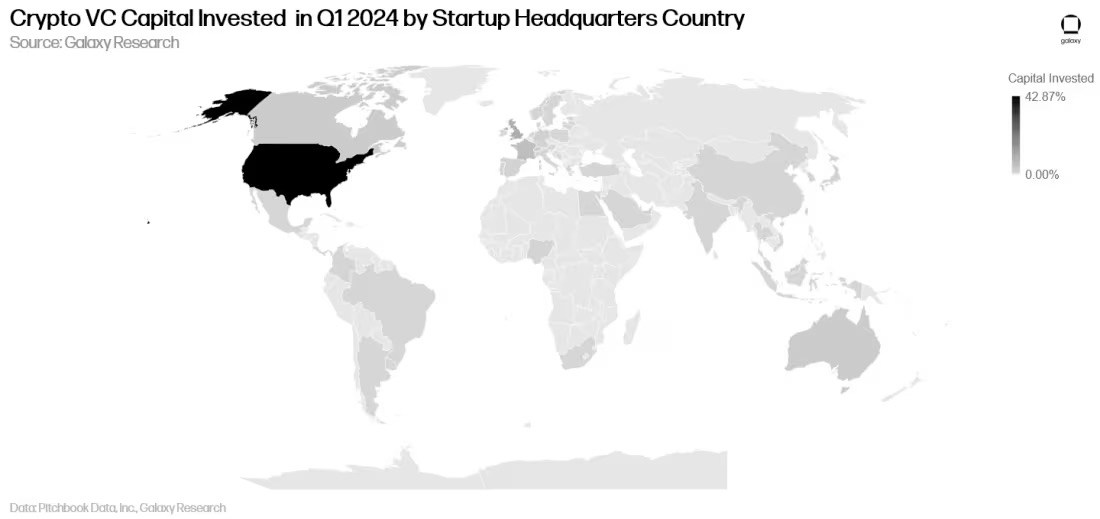

Investment by Geography

Despite a challenging regulatory environment, U.S.-based companies continued to complete the most funding rounds and raise the most capital from venture investors. In Q1 2024, over 37.3% of deals involved companies headquartered in the United States. Singapore accounted for 10.8%, the UK for 10.2%, Switzerland for 3.5%, and Hong Kong for 3.2%.

U.S.-headquartered companies attracted 42.9% of venture capital. Singapore followed with 11.1%, the UK with 9.7%, Hong Kong with 7.9%, and France with 5.6%.

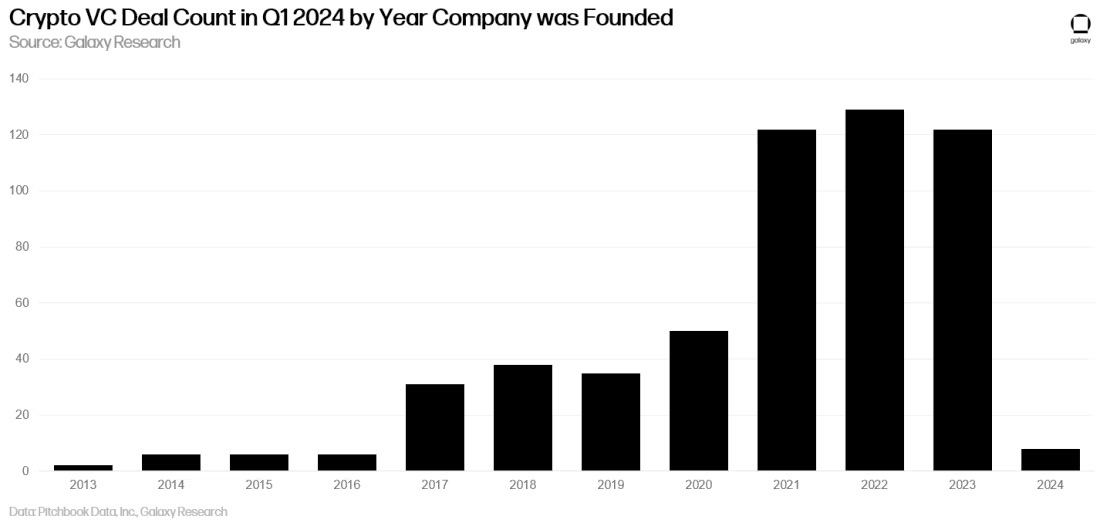

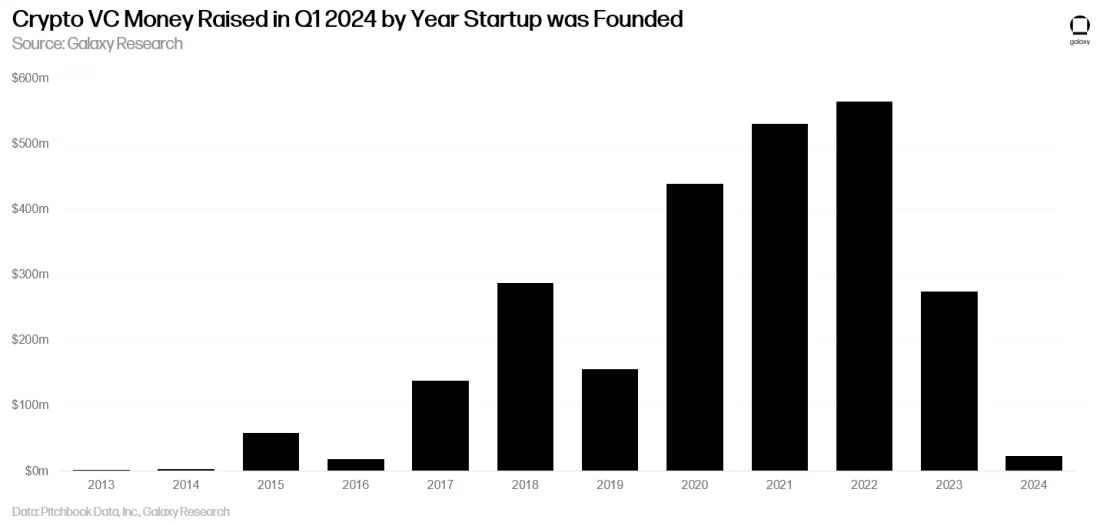

Investment by Cohort

The vast majority of deals completed in Q1 2024 involved startups founded between 2021 and 2023, which is expected given that 2024 has only just begun.

In terms of capital raised, companies founded between 2020 and 2022 received the most investment.

Crypto Venture Fundraising

Fundraising for crypto-focused venture funds remains challenging. A combination of macroeconomic conditions and turbulence in crypto market infrastructure has made some allocators less willing to commit to crypto at the levels seen in 2021 and 2022. At the start of 2024, investors widely expected significant rate cuts during the year, but throughout Q1, strong inflation data weakened those expectations, helping sustain a difficult fundraising environment for venture investors. While total capital allocated to crypto venture funds declined quarter-over-quarter, the number of new funds increased, with at least 22 new funds announced.

On an annual basis, average fund size in 2024 continues to decline, though the median size saw a slight uptick.

Regarding the sources of allocator capital flows, crypto-focused funds continue to struggle to raise from traditional allocators, capturing only a small fraction of newly allocated capital in Q1.

Key Takeaways

-

Sentiment and activity are improving, but still far below prior bull market levels. While digital asset markets have rebounded significantly from their 2023 lows, venture investment has clearly lagged. During previous bull markets (such as 2017 and 2021), venture capital inflows were highly correlated with liquid crypto asset prices. But in 2023 and 2024, venture investment remains well below prior peaks even as crypto prices recover. Several factors explain the stagnation: high interest rates suppress risk appetite; lingering bearish sentiment persists after the 2022 blow-up; and there may simply be too few later-stage companies capable of absorbing large venture investments. As a result, early-stage companies dominate venture activity in terms of both capital and deal count. Indeed, while total invested capital rose only modestly quarter-over-quarter, deal count jumped 50%, with the bulk occurring at Series A or earlier stages.

-

Early-stage deals dominated in Q1. Continued focus on early-stage investing signals long-term health for the broader crypto ecosystem. While later-stage companies struggle to raise, entrepreneurs are finding investors willing to back novel, innovative ideas. These projects are building scaling solutions, games, tools, and services at the intersection of artificial intelligence and cryptocurrency.

-

Bitcoin ETFs may pressure funds and startups. The launch of spot-based Bitcoin ETFs in the U.S. provides investors of all sizes with easy access to Bitcoin exposure. While highly liquid Bitcoin is not identical to investing in crypto startups, it may satisfy some investors’ and allocators’ desire for exposure to the crypto ecosystem. ETFs are regulated, available on nearly every brokerage platform, low-cost, and highly liquid. Bitcoin ETFs could also challenge crypto-linked equities, which historically served as an indirect investment channel into the industry.

-

Bitcoin L2 projects attracted strong VC interest. One of the most concentrated bets by crypto VCs in Q1 2024 was on Bitcoin L2 projects. The emergence of Ordinals in 2023, followed by the BRC-20 token standard and now the Runes standard, has prompted a shift in viewing Bitcoin as a platform network, not just a monetary network. Dozens of teams are attempting to build new types of second-layer networks on Bitcoin, many relying on and leveraging layer-2 scaling technologies developed in the Ethereum ecosystem (e.g., optimistic rollups, zk rollups, re-staking primitives, bridging protocols). Venture investors poured significant capital into these deals.

-

Web3 and Trading categories remain dominant in both deal count and capital, but Infrastructure saw a surge. Both in terms of capital raised and deals completed, Web3 and Trading categories remain leaders. However, in Q1 2024, “Infrastructure” ranked first in capital and second in deal count. This category is broad (as are the others), encompassing staking, re-staking, platform tools, sequencing services, and other tools for blockchain developers and users. EigenLayer’s $1 billion funding round led infrastructure investment.

-

Although small, newly launched funds are seeing some fundraising success, fund managers still face a tough environment. In Q1, the number of newly launched funds rose to 22 quarter-over-quarter, but total capital allocated to crypto-focused venture managers continued to decline. Average fund size ($108 million) fell quarter-over-quarter, while median fund size ($65 million) rose slightly. Since 2022, crypto venture funds have struggled to raise capital amid bankruptcies of several venture-backed crypto firms and rising U.S. interest rates, dampening allocator risk appetite. If liquid crypto prices and launch velocity continue to grow, and if several large VC funds successfully close sizable raises, we expect the venture market to loosen further and managers to achieve greater fundraising success.

-

The U.S. continues to dominate the crypto startup ecosystem. While the U.S. maintains a clear lead in both deals and capital, regulatory friction may push more companies abroad. For the U.S. to remain a long-term hub of technological innovation, policymakers must recognize how their actions—or inaction—impact the crypto and blockchain ecosystem.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News