Arthur Hayes: Money printing will accelerate, where will the crypto market go?

TechFlow Selected TechFlow Selected

Arthur Hayes: Money printing will accelerate, where will the crypto market go?

At this moment, I would suppress the urge to take my chips off the table.

Author: Arthur Hayes

Translation: Tao Zhu, Jinse Finance

Some of you may feel like masters of the universe now because you bought Solana for less than $10 and sold it at $200. Others did something smart—exchanged fiat currency for crypto during the 2021–2023 bear market but trimmed positions as prices surged in Q1 this year. If you swapped shitcoins into bitcoin, you’ve earned a pass. Bitcoin is the hardest money ever created.

Bull markets don’t come around often; it’s ironic when you make the right decisions yet fail to maximize your profit potential. Too many of us try to reason our way through bull markets. As long as the rally continues, they buy, hold, and buy again.

Sometimes I catch myself thinking like a loser. When that happens, I remind myself of the overarching macro narrative that both retail and institutional investors are beginning to believe. Namely, all major economic blocs—the U.S., China, the European Union, and Japan—are devaluing their currencies to deleverage government balance sheets. Now that TradFi can directly benefit from this story via spot Bitcoin ETFs in the U.S. and soon in the U.K. and Hong Kong, they’re urging clients to use these crypto derivatives to preserve the energy purchasing power of their wealth.

I want to briefly explain the fundamental reason behind the significant rise of cryptocurrencies relative to fiat currencies. Of course, this narrative will eventually lose steam—but that time is not now. Right now, I’m suppressing the urge to take chips off the table.

As we exit the weak window I predicted due to U.S. tax season and the Bitcoin halving on April 15, I want to remind readers why the bull market will continue and prices will get even more absurd. Few things in markets can carry you from here (Bitcoin rising from zero in 2009 to $70,000 in 2024) to there (Bitcoin reaching $1 million). Yet, as sovereign debt bubbles begin to burst, the macro environment driving fiat liquidity surges—and pushing Bitcoin higher—will only become more pronounced.

Nominal GDP

What is the purpose of government? Governments provide public goods such as roads, education, healthcare, and social order. Clearly, this is a wishlist for many governments, which instead deliver death and despair… but I digress. In return for these services, we citizens pay taxes. A balanced-budget government delivers as much service as possible within a given amount of tax revenue.

However, sometimes governments borrow money to do things they believe will generate long-term positive value without raising taxes.

For example:

Building an expensive hydroelectric dam. Instead of raising taxes, the government issues bonds to finance the dam. The hope is that the economic returns from the dam meet or exceed the bond yield. The government attracts citizen-investors to fund future growth by offering a yield close to the economic expansion the dam will create. If the dam increases economic output by 10% over ten years, then the government bond yield should be at least 10% to attract investors. If the government pays less than 10%, its profits come at the expense of the public. If it pays more than 10%, the public profits at the government’s expense.

Let’s zoom out and discuss economics at the macro level. A nation’s economic growth rate is its nominal GDP, composed of inflation and real growth. If a government wants to drive nominal GDP growth via budget deficits, it’s natural and logical for investors to expect returns equal to the nominal GDP growth rate.

While it's natural for investors to expect returns equivalent to nominal GDP growth, politicians prefer paying lower yields. If politicians can create a situation where government debt yields are below nominal GDP growth, they can spend faster than Sam Bankman-Fried did on effective altruism charities. The best part? No need to raise taxes to pay for the spending.

How do politicians create such a utopia? They enlist the TradFi banking system to financially repress savers. The easiest way to ensure Treasury yields stay below nominal GDP growth is to instruct the central bank to print money and buy Treasuries, artificially suppressing yields. Then banks are told that government bonds are the only “suitable” investment for the public. Thus, the public’s savings are quietly funneled into low-yielding government debt.

The problem with artificially suppressed Treasury yields is that they encourage malinvestment. The first projects are usually worthwhile. However, as politicians strive for re-election-driven growth, project quality declines. At this point, government debt grows faster than nominal GDP. Politicians now face tough choices. Either recognize malinvestment losses today through a severe financial crisis, or endure slow or even zero growth tomorrow. Usually, politicians opt for prolonged economic stagnation because the future arrives after they leave office.

A good example of malinvestment is green energy projects viable only through government subsidies. After years of generous support, some projects fail to generate investment returns or charge consumers excessively high costs. Predictably, once government backing is removed, demand fades and projects stall.

During economic downturns, when the central bank presses the "Brrrr" button harder than Lord Ashdrake hits "sell," bond yields become increasingly distorted. Government bond yields remain below nominal GDP growth, allowing inflation to erode the real burden of government debt.

Yield

The key task for investors is understanding when government bonds are a good investment. The simplest method is comparing the year-over-year nominal GDP growth rate with the 10-year government bond yield. The 10-year bond yield should act as a market signal reflecting expectations of future nominal growth.

Real yield = 10-year government bond yield – nominal GDP growth rate

When real yield is positive, government bonds are a decent investment. Governments are typically the most creditworthy borrowers.

When real yield is negative, government bonds are poor investments. The investor’s trick is to find assets outside the banking system growing faster than inflation.

All four major economies have implemented policies to financially repress savers, resulting in negative real yields. China, the EU, and Japan ultimately follow U.S. monetary policy cues. Therefore, I’ll focus on America’s past and future fiscal and monetary conditions. As U.S. policymakers ease financial conditions, the rest of the world follows suit.

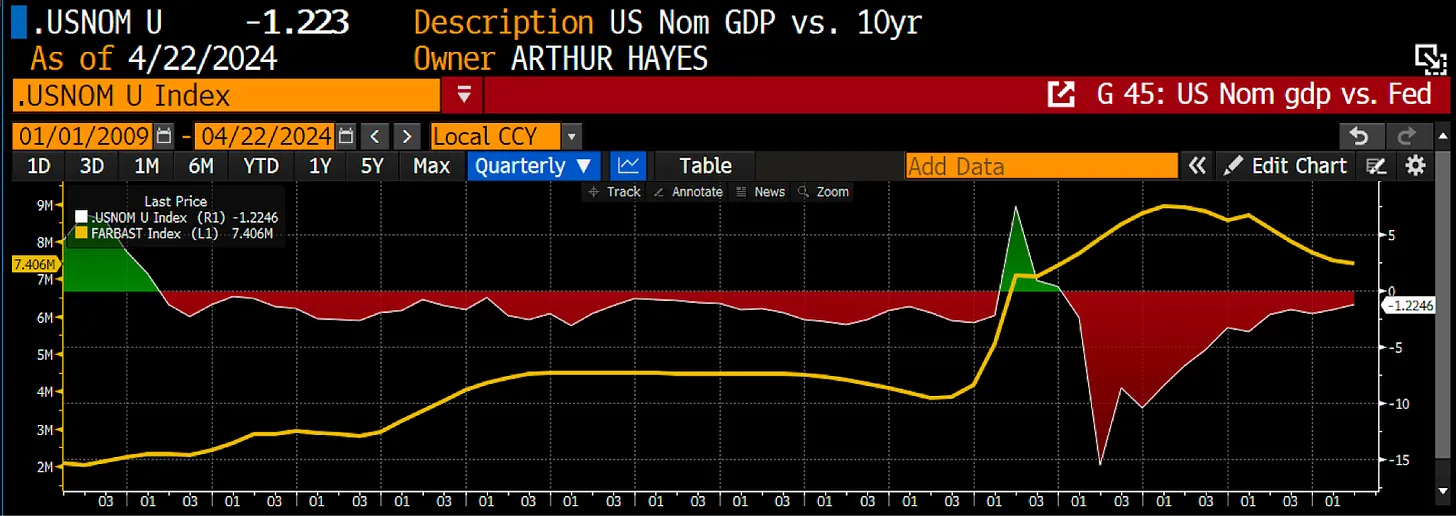

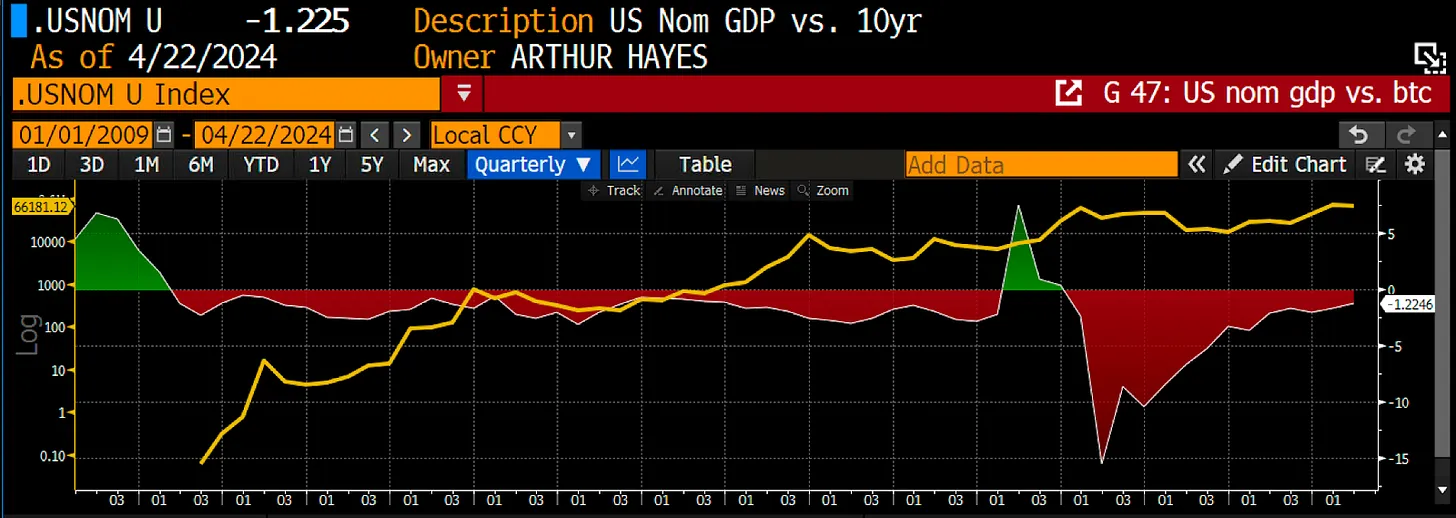

This chart shows the real yield (.USNOM index) in white and the Federal Reserve’s balance sheet in yellow. I start from 2009, the year Bitcoin’s genesis block was launched.

As you can see, following the deflationary shock of the 2008 global financial crisis, real yields turned negative. The index briefly returned to positive territory again due to the pandemic-induced deflationary shock.

Deflationary shocks refer to spikes in real yields caused by sharp declines in economic activity.

Except for 2009 and 2020, government bonds have been poor investments compared to stocks, real estate, and crypto. Bond investors achieved decent performance only by applying insane leverage to their trades. For hedge-fund puppet readers, this is the essence of risk parity.

This unnatural state occurs because the Fed expands its balance sheet by printing money to buy government bonds—a process known as quantitative easing (QE).

In periods of negative real yields, the safety valve—past and present—has been Bitcoin (in yellow). Bitcoin rises nonlinearly on a logarithmic chart. Its ascent is purely a function of a finite-supply asset priced against depreciating fiat dollars.

That explains the past, but markets are forward-looking. Why should you continue investing in crypto and remain confident this bull market has just begun?

Free Shit

Everyone wants something for nothing. Obviously, the universe never provides such cheap offerings, but that doesn’t stop politicians from promising benefits without raising taxes. Support for any politician—whether measured by ballot boxes in democracies or implied loyalty in more authoritarian systems—stems from their ability to generate economic growth. Once simple, obvious pro-growth policies are exhausted, politicians turn to the printing press, channeling funds into favored constituencies at the public’s expense.

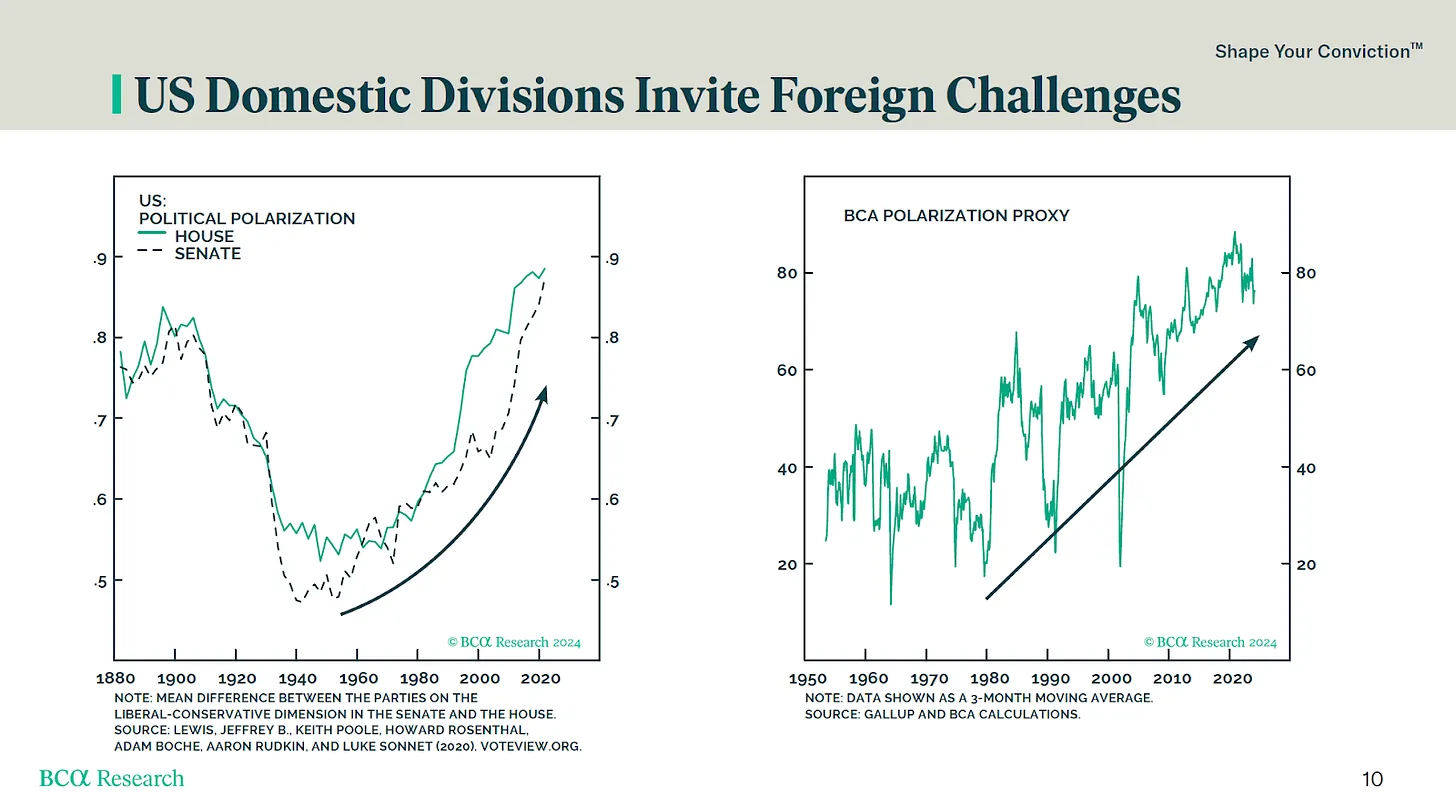

As long as governments borrow at negative real yields, politicians can offer free stuff to their supporters. Hence, the more partisan and polarized a nation becomes, the greater the incentive for the ruling party to spend money they don’t have to boost re-election odds.

2024 is a pivotal year globally, with many major nations holding presidential elections. The U.S. election is particularly crucial worldwide because the incumbent Democrats will go to extreme lengths to retain power (evidenced by questionable actions taken against Republicans since the Orange Man “lost” the last election). A large portion of Americans believes the Democrats unfairly denied Trump victory. Regardless of whether you believe this to be true, the fact that so many people hold this view ensures exceptionally high stakes for this election. As I’ve said before, U.S.-led fiscal and monetary policy will be mirrored by China, the EU, and Japan—that’s why this election matters.

The chart above, from BCA Research, shows political polarization in the United States over time. As you can see, voters haven’t been this divided since the late 19th century. From an electoral standpoint, this makes it winner-takes-all. Democrats know that if they lose, Republicans will reverse many of their policies. So the next question is: what’s the easiest way to secure re-election?

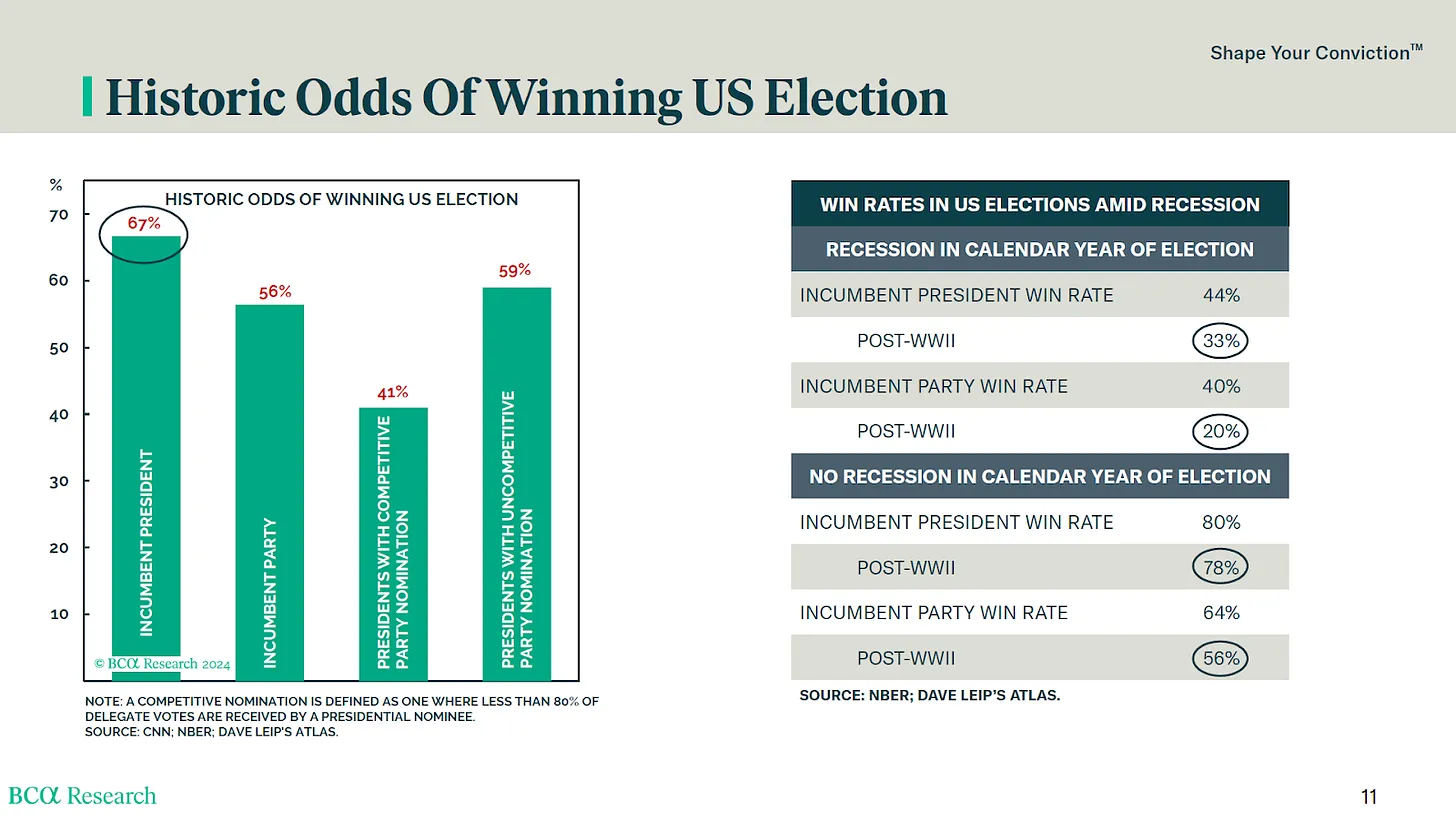

It’s stupid economics. Undecided voters base their choice on how they perceive the economy. As shown in the chart above, if the public believes the economy is in recession during an election year, the incumbent president’s re-election chance drops from 67% to 33%. How can a ruling party controlling monetary and fiscal policy ensure no recession occurs?

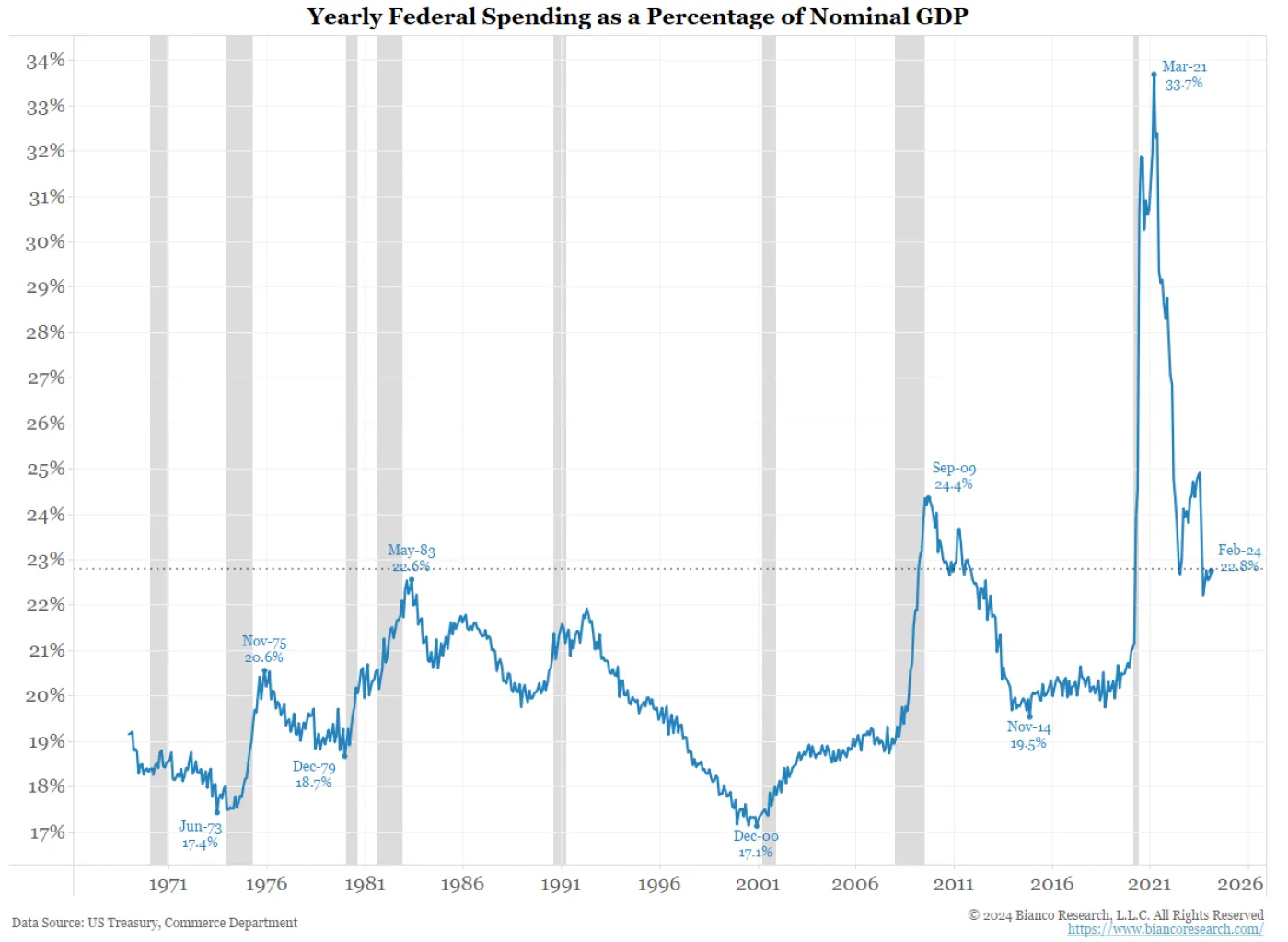

Nominal GDP growth is directly influenced by government spending. As shown in this Bianco Research chart, U.S. government spending accounts for 23% of nominal GDP. This means the ruling party can effectively print GDP at will, provided they borrow enough to sustain desired spending levels.

China decides its GDP growth target each year. Then the banking system creates sufficient credit to push economic activity to that level. To many Western-trained economists, the apparent “strength” of the U.S. economy is confusing, as many key indicators suggest a recession should already be underway. But as long as the ruling party can borrow at negative real rates, it can manufacture the growth needed to stay in power.

This is why President Biden-led Democrats are going all out to increase government spending. Then U.S. Treasury Secretary Janet Yellen and her Federal Reserve Chair Jerome Powell must ensure Treasury yields remain well below nominal GDP growth. I don’t know what euphemisms they’ll invent for money printing to keep real yields negative, but I believe they’ll take whatever measures necessary to keep their boss and his party in office.

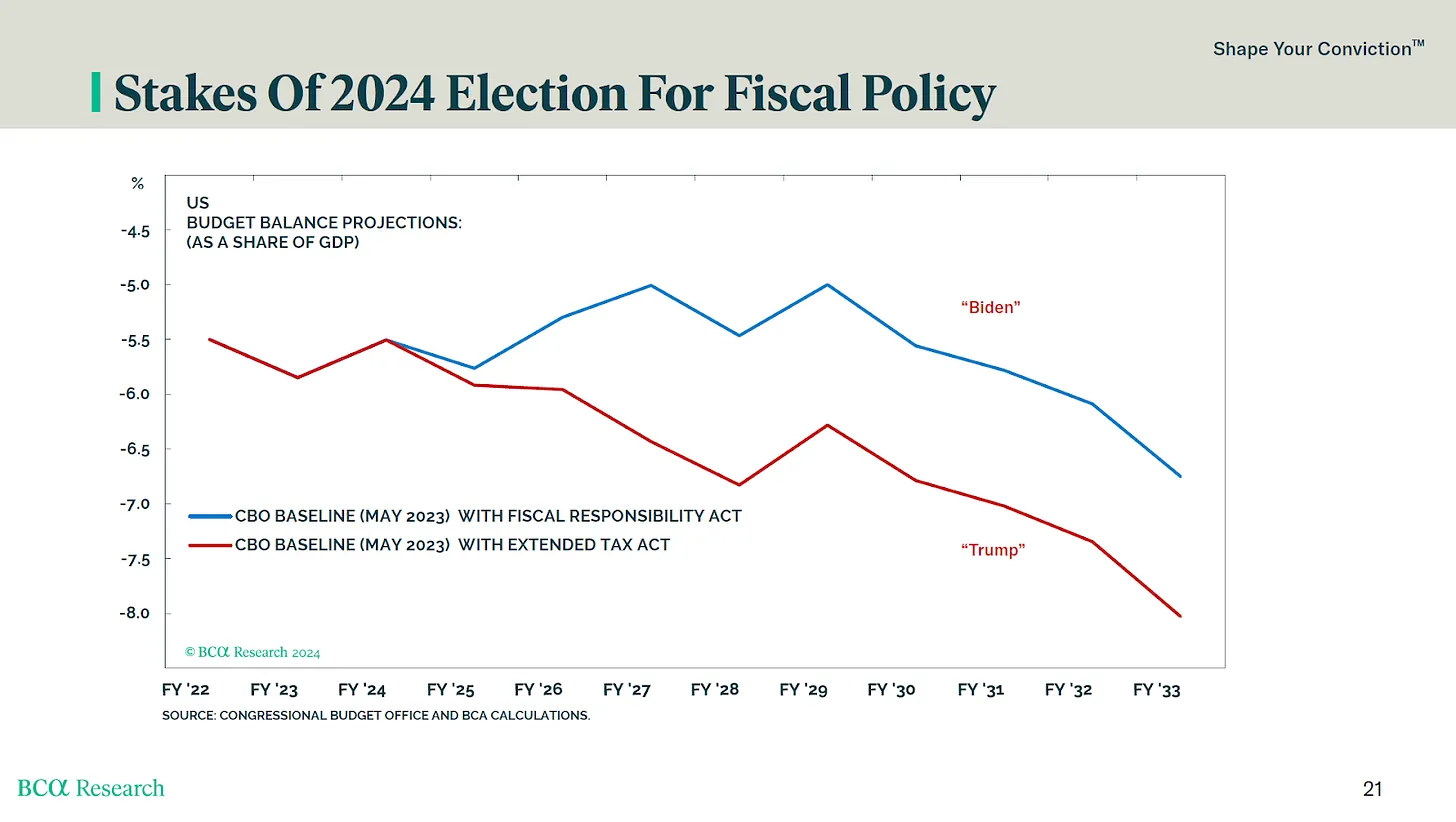

Yet the Orange Man might win. In that case, what happens to government spending?

The chart above estimates deficits under either Biden or Trump presidencies since 2024. As you can see, Trump’s spending is projected to exceed Slow Joe’s. Trump is seeking another round of tax cuts, which would further widen the deficit. Whichever elderly clown wins, rest assured—government spending won’t decline.

The Congressional Budget Office (CBO), forecasting deficits based on current and hypothetical political environments, expects massive deficits. Fundamentally, if politicians can borrow at 4% to generate 6% growth, why would they ever stop spending?

As outlined above, the U.S. political landscape gives me confidence in the trajectory of the printing press. If you thought the U.S. monetary and political elite’s response to “solve” the 2008 global financial crisis and the pandemic was absurd—you haven’t seen anything yet.

Wars on the periphery of American peace continue primarily on the Ukraine/Russia and Israel/Iran fronts. As expected, war hawks from both parties are content to keep funding their proxies with borrowed billions. As conflicts escalate and more nations get drawn in, costs will only rise.

Conclusion

As we enter the Northern Hemisphere summer, policymakers get a breather from reality, and crypto volatility will likely subside. This is the ideal time to slowly accumulate positions using recent crypto dips. I have a list of beaten-down shitcoins from last week. I’ll discuss them in my next article. There will also be numerous token launches, though none will match the popularity of Q1 releases. This offers a great entry point for those who weren’t early investors. No matter your appetite for crypto risk, the coming months will provide a golden opportunity to build exposure.

Your intuition is correct: as politicians spend money on handouts and wars, money printing will accelerate. Don’t underestimate the desire of the current elite to stay in power. Reassess your crypto beliefs only if real interest rates turn positive.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News